Interest Rates on Post Office Small Saving Schemes – FY 2013-14

This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

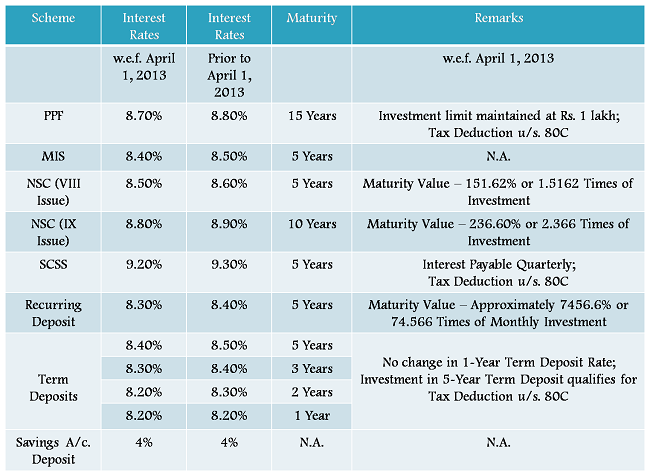

Interest rates on most of the Post Office small saving schemes have been reduced by 10 basis points (bps) or 0.10% effective April 1, 2013. The change has become an annual exercise now and it gets announced in March every year. Here is the link to the statement issued by the finance ministry on Monday, March 25th.

Except 1-year time deposit, all other saving schemes will now carry 0.10% lower rate of interest. Your Public Provident Fund (PPF) account will now earn you 8.70% per annum tax-free rate of interest as against 8.80% earlier. 5-year and 10-year National Savings Certificates (NSC) will now carry interest rates of 8.50% and 8.80% per annum respectively, as against 8.60% and 8.90% now.

Post Office Monthly Income Scheme (POMIS) will also earn you lower at 8.40% vs. 8.50% earlier. The interest rate on Senior Citizens Savings Scheme (SCSS) also stands reduced to 9.20% as against 9.30%.

Here is the table having the interest rates applicable for FY 2012-13 and FY 2011-12:

Interest rate differential between PPF and Tax-Free Bonds

Tax-free bonds as a fixed income investment have become reasonably popular among investors now and since the interest income earned on both tax-free bonds and PPF is tax-free, most financial advisors/analysts compare these two instruments before recommending it to their clients.

Till financial year 2011-12, PPF was fetching 8.60% per annum which got increased to 8.80% per annum effective April 1, 2012 and at the same time, tax-free bonds were getting issued at 8.30% per annum. So, the interest rate differential was only 0.30% which made tax-free bonds a very attractive investment avenue for high net worth individuals (HNIs).

Now, the interest rates on tax-free bonds have fallen to approximately 7.50% per annum as compared to PPF which will now yield 8.70% effective April 1, 2013. This has increased the interest rate differential to 1.20% and hence makes PPF the best fixed income investment for most of the individual investors.

Honestly speaking, I was expecting the interest rate on PPF to fall below 8.50%. As an investor, it is a pleasant surprise to still get 8.70% on PPF but as an Indian and as an equity investor in Indian stock markets, I am disappointed as I think the interest rates have been set on a higher side and it is going to put one more strain on the finances of Indian government. It makes me think again if the government is still serious about containing its fiscal deficit or it wants to keep everybody silent one year before the elections, ignoring its already bad financial condition.

Considering the fact that the consumer price index is hovering around 10.5% and is not likely to fall the inflation adjusted return which was already negative is in furthur minus.These schemes are all hugely popular in India and the equity culture has to catch up to beat inflation..I hope this will happen.

1. The interest rate on PPF upto Apr-2012 was 8% (not 8.8%) for many years. It was then linked to the market conditions as per specified formula and fixed at 8.8% for 2012-13 and now 8.6% for 2013-14.

2. One should be careful while comparing PPF and tax savings bonds. They have different objectives and rules – especially liquidity during first 6 years.

1. Rate of interest on PPF got hiked twice, from 8% to 8.6% w.e.f. December 1, 2011 & then to 8.8% w.e.f. April 1, 2012. Now, it has been lowered to 8.7% w.e.f. April 1, 2013. So, there was a time when the interest rates were 8.6% for a short period of 4 months.

2. Tax saving bonds are no longer available. Probably you want to say Tax-Free Bonds, right? From investment perspective, PPF and tax-free bonds are comparable to the closest, if not completely. Liquidity is an issue with PPF.

i have invested in HDFC crest 2yrs back with 50000 premium every yr. But the growth is very slow. please suggest what to do.

what is the interest rate of SBI ppf account. they give us only7.75 P.a

Hi Chamarthisailaja… An investor should never mix his/her life cover needs with the investments he/she makes. Life insurance policies are poor products for investment purposes as they carry high expenses and very low transparency is there. Please consult an unbiased financial advisor to know what to do with your HDFC Crest policy.

PPF interest rate is same across all post offices and all banks. It is 8.70% per annum this financial year.

Please tell me per year interest on R/D post office.[1000 P.M Maturity Amount rs.74453]

It is 8.30% per annum.

It is ridiculously low considering even PSU Banks offer around 9%.Is any one investing in such deposits.?Do you have any data or know any data source giving out actual investments made in PO savings schemes on a year to year basis?Thank you.

Yes, a large number of investors invest in these Post Office Small Saving Schemes including RD. As on 31st March 2012, there were 8,59,21,440 RD accounts with an outstanding balance of Rs. 62,662 crore in the 1.54 lakh post offices across the country.

You can access the Annual Reports of the DoP from this link to get more info:

http://www.indiapost.gov.in/Annual_Reports.aspx

Thanks a lot for this info.The numbers are huge and incredible.I wonder what is the attraction?Perhaps the commercial banks penetration across the country is very low.

I think Postal Deposits are considered as the safest by the rural population. Door-to-door collection service is also a very important factor for Postal RD’s growth. Also, you are right, commercial banks’ penatration is low across the country.

Please tell me per year interest on R/D post office.[1000 P.M Maturity Amount rs.74453 8.30%].Total int is Rs 14453 Per year amount interest please tell me

Dear Rajesh,

As the deposit is made on a monthly basis, the interest amount would vary every year. It would be approximately Rs. 553 in the first year.

Thanks for information.Please tell me 2nd 3rd 4th 5th year interest also.

It is approximately as follows:

2nd year: Rs. 1625

3rd year: Rs. 2791

4th year: Rs. 4054

5th year: Rs. 5430

Thanks a Lot

Excellent…Crisp..to-the-point….Jargonless article. Thank you Shiv. Keep up the Good Work.

Thank you Kranti !!

PO Sr citizen saving scheme 2004-pl give RBI cir no/or any authority for interest rates for FY 2012-13 and Fy 2013-14.Thanks.

Here you have the links to the notifications Mr. Sehgal:

http://finmin.nic.in/the_ministry/dept_eco_affairs/budget/InterestRate_SmallSaving_25032013.pdf

http://www.finmin.nic.in/the_ministry/dept_eco_affairs/budget/InterestRate_SmallSaving_26032012.pdf

Is it essential to withdraw annually the interest accrued in a Post Office Time Deposit Scheme for 5 years @8.5%? Please help by replying. I understand that it is rebateble under section 80 c. Please confirm.

Thanks

dear sir

pls follow in system.

Hi

I want to invest in Post office SCSS

Amout 1 Lac

What will be the maturity amout after five yrs..

Will this be best scheme or should i think for something else.

sugessions pls.

Hi sir i want to know scheams in post office which is low investment.Best returns on monthly,Quarterly,Halfyearly,Annualy.

Whether Rd post scheme can be extended to further 5 maturity if Rd rate calculator be conformed for 10 years Rd scheme

Please

Sir I have opened a term deposit account for 5years in Post office on 28/07/2012 for Ra. 31200.

What will be my total amount in maturity

I am invest 1,000/- in post office (RD) per month from April 2013.

After 5 years there will be a lot.

Dear sir.how deposite in post office.invest amount on maturity.No payment on time .Your postmaster & suprident take money then done payment after some days.

With thanks

Pramod poddarbettiah.

sir Maine august 2013 me post office main1000 per month ki rd kholi thi august 2018 me rd puri ho hai hai, to maturity value kitni hogi batane ki korea kare.

sir Maine august 2013 me post office main1000 per month ki rd kholi thi august 2018 me rd puri ho hai hai, to maturity value kitni hogi batane ki Kirpa kare.