Shriram Transport Finance NCD Issue – 2013-14

This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

Regular readers of OneMint must be quite familiar with NCDs or non-convertible debentures. There have been many such NCD issues in the past couple of years and here is one such public issue for this financial year. Shriram Transport Finance Company Limited (STFCL) will be launching this issue from July 16th and the same will get closed in a couple of weeks time on July 29th.

Size of Shriram Transport NCD Issue, Ratings and Safety

The size of the issue is Rs. 750 crore, including an option with the company to retain over-subscription to the tune of Rs. 375 crore. The issue has been rated AA/Stable by CRISIL and AA+ by CARE.

These NCDs are also secured in nature, which means some specific immovable property or other assets will be mortgaged in favour of the Debenture Trustee to cover 100% of the principal and interest payments. In case the company is not able to pay your principal investment back at the time of maturity or goes insolvent before that, the investors have the right to claim their payments by getting the assets liquidated.

Categories of Investors

The investors would be classified in the following four categories:

- Category I – Institutional Investors

- Category II – Non-Institutional Investors (NIIs)

- Category III – High Net-Worth Individuals (HNIs)

- Category IV – Retail Individual Investors (RIIs)

50% of the issue is reserved for the Retail Individual Investors i.e. for the individual investors investing up to Rs. 5 lakhs, 30% of the issue is reserved for the High Net-Worth Individual Investors i.e. for the individual investors investing above Rs. 5 lakhs. 10% of the issue is reserved for the Institutional Investors and the remaining 10% is for the Non-Institutional Investors. NRIs and foreign nationals among others are not eligible to invest in this issue. The allotment will be made on a first-come-first-served basis.

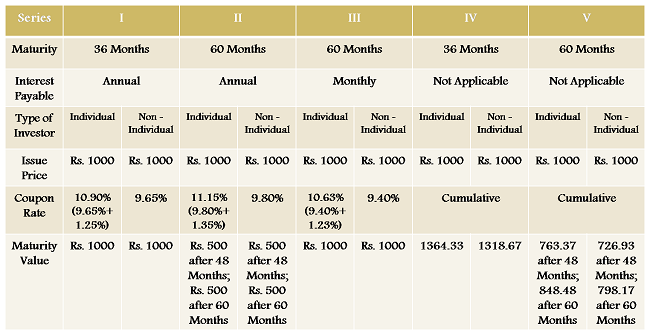

Tenors and Rate of Interest of Shriram Transport NCD

The bonds will be issued for a tenure of 36 months and 60 months with annual interest option and cumulative interest option. The bonds will offer the base coupon rates of 9.65% per annum and 9.80% per annum for a period of 36 months and 60 months respectively. For Series II and Series V, 50% of the face value will be redeemed after completion of 48 months and the remaining 50% will be redeemed after 60 months from the date of allotment.

Like last year, category III & category IV investors i.e. individual retail and HNI investors including HUFs, will be given an additional incentive over and above the base coupon rate and it will be 1.25% per annum for 36 months and 1.35% per annum for 60 months, making it an annual coupon rate of 10.90% and 11.15% respectively. So, irrespective of your investment amount as an individual, you will keep getting the higher rate of interest, even if you are an HNI with investments in excess of Rs. 5 lakhs.

There is a monthly interest option as well but it is available only under 60 months period and that too with a lower rate of interest of 10.63% per annum, including the additional incentive of 1.23% per annum.

The company has decided to keep the minimum investment requirement of Rs. 10,000 i.e. 10 bonds of face value Rs. 1,000.

Listing on the Stock Exchanges and TDS

These NCDs will get listed on the National Stock Exchange (NSE) as well as on the Bombay Stock Exchange (BSE). Investors will have the option to apply these NCDs in physical form also, except for Series III NCDs, which will be allotted compulsorily in the demat form.

The interest earned will be taxable as per the tax slab of the investor and TDS will be applicable if the interest amount exceeds Rs. 5,000. But, if you take these NCDs in the demat form, the company will not deduct any TDS on it.

Financials of the company

During the year ended March 31, 2013, total income of the company increased by 11.37%, from 5,894 crore to 6,564 crore and the net profit jumped 8.27% from 1,257 crore to 1,361 crore. Assets under management (AUM) figure stood at Rs. 49,676 crore as against Rs. 40,215 crore of last year, a jump of 23.53%. Net interest margins (NIMs) also jumped to 3.64% as against 2.91% of previous year.

Gross NPAs and Net NPAs of the company stood at 3.20% and 0.77% as on March 31, 2013 as against 3.06% and 0.44% respectively as on March 31, 2012.

A couple of significant points to be mentioned here. Shriram Capital is the promoter company of Shriram Transport Finance Company Limited (STFCL) and it has applied for a banking license with the RBI for which the deadline ended earlier this month on July 1st. Also, Ajay Piramal, the Chairman of Piramal group, recently acquired 10% stake in Shriram Capital for a reported Rs. 650-700 crore, valuing the promoter company at Rs. 6,500-7,000 crore. These two events speak in favour of the company and strengthen investors’ confidence also.

Link to Download the Application Form

Any idea why only few companies are going for these NCD issues? I see only Shriram and their various arms our earlier Gold finance companies issuing public NCDs. If it is a cheap source of capital, then why don’t other companies issue it?

Hi Ashok,

I’m not sure why exactly some other companies dont come up with public issues of NCDs to raise money. Even if they issue NCDs, they do it through private placements.

Though the returns from this NCD look attractive, I may not invest in them because I already invested in an earlier Shriram issue and I don’t want too put too many eggs in the same basket :-(.

Wish other companies also came up with Public NCD offers

It is always wise to diversify your portfolio, even if the returns are very attractive. Some other companies will also hit the market, probably sometime later this year.

I have inc.sted in NcdIf DTDC. It has matured. The coy. Withdrew the Ncd without making payment.

What is the procedure for obtaining payment?

Correction .not DTDC but STFC

HI. SHIV,

Looking at the past experience(last year) how much discount will these ncds list at ?

How is the response as per your reckoning ? would it be wise to buy on listing?

thnx.

Hi Anek,

There is not much euphoria in buying these bonds this time around. So, I dont think there would be too many sellers or buyers at the time of listing. But still there will not be any premium for sure. If the brokerage charges are not very high (ICICI Direct charges 1%), then one can consider buying these bonds on listing.

In this bond (STFC NCD) there are 5 series types classified, and the redemption amount mentioned in the forms are not very well to be understood by everyone, without calculating the percentage returns.

I tried my best to understand them to take the decision. However, still I’m not clear on the percentage return, where the redemption amount is in two parts in different time period. As in series II it mentions 50% in 48 months and the balance in 60 months. And in series V it mentions Rs.763.37/- at the end of 48 months and Rs.848.48/- in 60 months.

So how can the percentage return be calculated in such a case? And how the best option be choosen?

Hi Saurabh,

It is very simple:

Rs. 500 * (1.1115)^4 = 763.37

Rs. 500 * (1.1115)^5 = 848.48

(Note: The difference in actual redemption amount is due to calculation taking into account actual maturity period in days)

Hi,

If I buy these bonds, will my money get locked for 3 years? Can I get out after a year and get interest on pro-rata basis?

Hi Rahul,

There is no lock-in period with this investment. You can sell these NCDs whenever you want on the stock exchanges in the secondary markets, like shares are bought and sold.

If you go for the annual intreset option, it’ll be paid once every year on April 1st. If you sell your NCDs sometime in between the interest payment dates, the company will not pay the interest on a pro-rata basis. But it will get reflected in the market price of these bonds as it would keep going up till the NCD goes ex-interest before the interest payment date.

Hi Shiv. I had small doubt on tax calculation of NCD bought from open market. (this does not pertain to Shriram transport, I have a general doubt in mind). Heres the case:

Assume, I purchase a 1 year cumulative NCD at 995 from secondary market and hold it till maturity. My total holding period is less than 1 year and upon maturity I receive 1125 from the company (1000 principal + 125 interest). Now will this income will be treated capital gains or interest income or both (125 interest & 5 capital gain)?. Can you guide please. Thanks

Hi Ankur,

In this case, Rs. 125 is the interest income and Rs. 5 would be the treated as the capital gain.

Ok. thanks

after Shriram transport NCD issue which other NCD Issue is due to be anounced and when

Hi George,

Traditionally, Shriram City Union Finance issue follows Shriram Transport Finance issue. So, you can expect it to hit the markets soon. Gold finance market is down, so it is unlikely that you’ll see Manappuram, Muthoot, Religare Finvest, IIIFL etc. to come up with such issues. No other company has announced its plans and the date of any such issues.

Thanks for your reply . I have Bonds of IIFL with interest payable annually every April . If I sell these bonds now at a premium of say Rs 70 per bond , how will the accrued Interest from May13 till date be paid.

Hi George,

Interest will be paid in April to the buyer who buys these bonds from you today, including the accrued interest. You will only get the premium of Rs. 70.

sir,

I want to know, if on the first day I have applied for shriram transport finance NCD the issue then how much allotment shall I get? and how many times the issue has subscribed , I got information that issue has closed earlier on 24-07-2013.

Hi Satyaprakash,

You’ll get 100% allotment. The issue size was Rs. 750 crore, including the green-shoe option and it got oversubscribed to the tune of Rs. 750 crore and 67 lakhs. Yes, it got closed on July 24th.

when is the listing of the aforesaid ncds. ?

Listing date has not been announced as yet, but the allotment has been made:

https://www.integratedindia.in/ncd_allot1.asp

Listing to happen tomorrow, August 7th, 2013, on both the NSE as well as the BSE.

Source: http://www.bseindia.com/markets/MarketInfo/DispNewNoticesCirculars.aspx?page=20130805-18

when are the Muthoot finace NCDs comming

Muthoot NCDs issue is opening from September 2nd.

Dear Shiv,

I had bought Shriram Transport Finance NCDs Series N4 having coupan of 11%, during its public offer. These NCDs had a tenure of 5 years with a call / put option after 4 years. As 4 years are already over, the company is ready to accept the NCDs from the investors who wish to exercise put option (The company is not exercising its call option). I understand that the company will pay face value (Rs.1000) + accrued interest (about Rs.51) to the investors who exercise put option. As the present market price is about Rs.1037, with very poor liquidity, I wish to exercise put option and invest the proceeds in some other NCDs / Bonds. Do you think this is a wise decision ? If not, please explain the reason.

Also, please suggest an equivalent or better rated, secure NCD / Bond (other than tax-free bonds, as I have already invested a good portion of my funds in them), available in secondary or primary market with same or better yield and a long duration. In my priority order capital protection comes first, good return comes second, liquidity comes third and tax liability comes last (as I am in 10% tax bracket).

I am considering L&T Finance NCDs series N4 which have about 6 years left till maturity and have a coupan of 10.24% payable semi-annually and available at a price of 1025. Its YTM shown on NSE website is 11.07, but as per my calculation it is about 9.5. Please confirm which is correct. Also tell me whether these NCDs are a good option for me. If you have a better option, please suggest.

Thanks

TCB

Dear Shiv,

The only purpose of the above querry is to take advantage of low prices of bonds /NCDs due to high interest rates prevailing at present. I am not in need of funds. So I will exercise put option only if a better option is available, in terms of my priorities mentioned above.

I think the L&T Finance N4 NCD mentioned above has just gone ex-interest. Kindly confirm and also suggest the best option.

Thanks

TCB

Yes, L&T N4 NCDs pay semi-annual interest and it has gone ex-interest last week itself.

Hi TCB,

Yes, it is definitely a good idea to exercise your Put Option with STFC N4 NCDs. There are better yields available in both primary and secondary markets. STFC itself will be coming out with one such public issue in the next 7-10 days, so if you are comfortable with the company, you can subscribe to it.

You can also check out STFC’s or L&T’s already listed NCDs which are carrying higher yields. I think SBI N5 NCDs are better than L&T’s N4 NCDs. L&T N4’s NSE YTM is incorrect, it is definitely below 10%. Considering your tax bracket & safety as the top priority, NCDs are a better option than tax-free bonds but then you should get a higher yield than 10-11%.

Dear Shiv,

As suggested by you in one of your posts, I am thinking of buying NCDs from series NL, NS, NU, NV, NW, NX, NY, NZ depending on yields. I am an individual investor. If I buy these NCDs from market, can you please tell me whether I will get coupan of individual investor or non-individual investor ?

Thanks

TCB

Sorry, I didn’t get your question. If you are buying these bonds in your own name, then why the question of non-individual coming into the picture? There is no “Step Down Interest” clause with these NCDs.

Dear Shiv,

Kindly advise whether I should invest in NTPC Tax free bonds under HNI or distribute the investment under Retail category , considering post issue liquidity and better price , as I intend to sell the bonds after 3-5 years . I am currently a HNI investor

Sir, I had sent NCD Certi. No.10165 (of Digdha M Patel ) dated 15.7.2014 for 75 NCDs of Rs.1,000/- each for redeemption to your Mahape, Navi Mumbai office on 20.7.2017. Payment is till date not received. Kindly send payment OR guide to whom should I contact for payment against redemption.