This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

As National Housing Bank (NHB) tax-free bonds issue is about to get launched from Monday, Indian Railways Finance Corporation (IRFC) would also be coming out with its issue from January 6. Like many of the investors, I am also disappointed with the coupon rates IRFC has announced to offer and also with its decision not to offer the 20-year option.

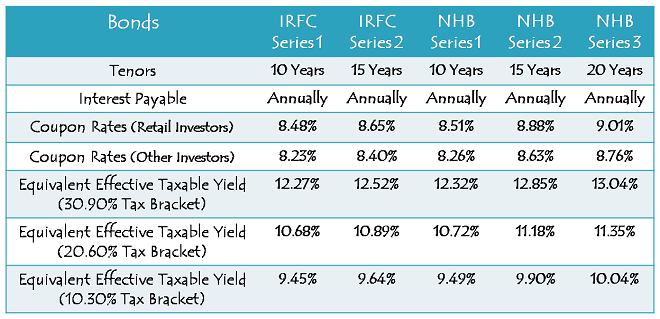

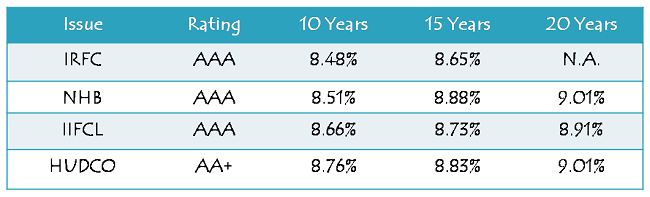

If any of you doesn’t know already, IRFC has decided to offer 8.48% per annum for the 10-year option and 8.65% per annum for the 15-year option. These rates are lower than the rates NHB issue will carry i.e. 8.51% p.a. for 10 years and 8.88% p.a. for 15 years. As both these issues are ‘AAA’ rated and both companies are government organisations, I think people would be more enthusiastic about NHB bonds.

Though at one place in the prospectus the closing date has been mentioned as February 20, 2014, it has been stated as January 20, 2014 at all other places. Looking at the illustrative example it gets clear that it is indeed January 20th.

Size of the Issue – IRFC is authorised to issue tax free bonds worth Rs. 10,000 crore this financial year, out of which it has already raised Rs. 1,337 crore through a couple of private placements. With base issue size of Rs. 1,500 crore, IRFC plans to mop up all of the remaining Rs. 8,663 crore with this issue, including the green-shoe option to retain additional Rs. 7,163 crore.

I would call IRFC move to be brave enough to target such a large amount to be raised within a span of just eleven working days, which others have not been able to do even with two tranches of longer durations.

Coupon Rates on Offer – People who were hoping to get even higher interest rates and planning to diversify their portfolio with this issue and the NHB issue, have been left disappointed by the interest rates IRFC has fixed to offer. Coupon rates of IRFC have been 0.23% lower with the 15-year option and 0.03% lower for the 10-year option as compared to the NHB issue. As always, the non-retail investors will get 0.25% less rate of interest every year.

As compared to IIFCL as well, which is currently offering 8.66% p.a. for the 10-year option and 8.73% p.a. for the 15-year option, the rates are lower. So, the investors can still subscribe to the IIFCL issue if they haven’t already, as it is still undersubscribed in the retail investors category.

Rating of the Issue – IRFC is the financing arm of the Indian Railways with zero non-performing assets. It earns assured net interest margins (NIMs) from the Ministry of Railways (MoR) and other related entities like Rail Vikas Nigam Limited (RVNL) and RailTel.

Most importantly, in case of any default or shortfall in the money required to redeem these bonds, the MoR will be required to fund the payments due to the bondholders. So, there is minimal risk involved with these bonds and probably that is the reason all rating agencies, CRISIL, ICRA and CARE, have assigned ‘AAA’ rating to the issue.

NRI/QFI Investment – Non-Resident Indians (NRIs) are eligible to invest in this issue, on a repatriation basis as well as on a non-repatriation basis. Qualified Foreign Investors (QFIs) are also eligible to invest in the issue.

Investor Categories & Allocation Ratio – The investors have been classified in the following four categories and each category will have certain percentage of the issue size reserved during the allocation process:

Category I – Qualified Institutional Bidders (QIBs) – 10% of the issue i.e. Rs. 866.30 crore is reserved

Category II – Non-Institutional Investors (NIIs) – 30% of the issue i.e. Rs. 2,598.90 crore is reserved

Category III – High Net Worth Individuals including HUFs, NRIs & QFIs – 20% of the issue i.e. Rs. 1,732.60 crore is reserved

Category IV – Resident Indian Individuals including HUFs, NRIs & QFIs – 40% of the issue i.e. Rs. 3,465.20 crore is reserved

Listing – The company has decided to get these bonds listed on both the stock exchanges i.e. National Stock Exchange (NSE) as well as the Bombay Stock Exchange (BSE). The bonds will get allotted and listed within 12 working days from the closing date of the issue.

Minimum & Maximum Investment – Unlike NHB, the face value of a bond in this issue has been fixed at Rs. 1,000 and as always, the minimum investment would remain Rs. 5,000 i.e. at least 5 bonds of Rs. 1,000 each. Retail Investors’ investment limit stands at Rs. 10 lakhs, beyond which they will be considered as HNIs and will get a lower rate of interest.

Demat not Mandatory – An investor, as per his/her own choice, can subscribe for these bonds in either of the forms, demat or physical. Though it is mandatory to have a demat account to sell these bonds, you may subscribe to them in certificate form as well and can get them converted to demat form whenever you want.

Interest on Application Money & Refund – IRFC will pay interest to the successful allottees on their application money, from the date of realization of application money up to one day prior to the deemed date of allotment, at the applicable coupon rates. Unsuccessful allottees will get interest @ 5% per annum on their refund money.

Interest Payment Date – IRFC has decided to make its first interest payment on April 15, 2014 and subsequent interest payments will also be made on April 15 every year.

What would make you invest in this IRFC bond issue?

With NHB offering higher rate of interest for all maturity periods from Monday and IIFCL, HUDCO still open for subscription with higher rate of interest, what is that one thing which you think differentiates this IRFC issue from the rest of the issuers? Please share your views about it and let’s see if it makes sense to other investors also.

Application Form of IRFC Tax Free Bonds

NHB Tax-Free Bonds – Bidding Centres

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in IRFC tax-free bonds, you can contact me at +919811797407

NHAI Tax-Free Bonds issue opens January 15th. Coupon Rates – 8.52% for 10 years and 8.75% for 15 years. 20-year option is not there. It is rated ‘AAA’ and closes on February 5, 2014.

Thanks for the information. Glad I waited for NHAI before investing in IRFC 🙂

Great! 🙂

Great Shiv! I was tracking NHAI site frequently, but got the update from your site and now checked the NHAI site again. No other site has given this update and you have notified as soon as NHAI published the same. 15 Years is attractive though it is not as good as NHB coupon rate. Considering the reputation of last issues of NHAI, I am expecting the same response that NHB received and mostly allotment will be partial in this case also. Those applying should target 70% allocation and will have to be ready for that.

Thanks George!

I would differ from your view that the response for this issue would be as great as the response for the NHB issue. I think the response would be closer or better than the IRFC issue, but not like the NHB issue. NHAI issue in 2012 got huge subscription as it was the first such issue after a very long time and the interest rates it offered were higher as compared to the FD rates. But, that is not the case this time around.

One positive thing for this issue would be that the investors would be putting their refund money from the NHB issue into these bonds. So, around 25% of the NHB money is expected to get pumped into these bonds.

I agree with Shiv. NHB has a better credibility than NHAI though both are AAA. NHAI Interest rates offered are 25bps less than NHB. NHAI Issue size is much larger than NHB. NHB offered 20 year option and NHAI doesnt have that. All these put together NHAI will get much lower response than NHB , but bettter than IRFC. I am expecting issue to be closed in a week.

Regards

Ramadas

Shiv, For NHB also, I have suggested 1-2 days and you were of the opinion that it will take a week. I do agree with you that NHB was a better bet than NHAI. But market perception NHAI has proven in bond market and good interest is there. Considering that the size is around 3.69 K crore issue, I think the issue is not very large and considering the recent interest in TF bonds and low interest rate of IRFC, I will expect better response that you have suggested. 15 Yrs is offering good coupon rate and the difference with NHB is just 13 Basis points. May be retail can go to 2nd day, but other categories are likely to get subscribed on day1.

I wish I get proved wrong again with this issue also !! 🙂 Nothing better than a quick closure.

Agree with you! Either way, quick closure is better for the investor. Less waiting period.

Hi, 2 questions:

1. The NSE website (IPO current issues)shows this issue as oversubscribed, but as per ur numbers there is still a long way to fully subscribe this issue…can you pls clarify.

2. Is it worthwhile buying tax free bonds in secondary market…given that many are available at similar yields to new issues. What all should be considered while buying tax free bonds in secondary market.

Thanx in advance! I have found ur website recently and find it very helpful. Keep up the good work.

Thanks Jaspreet!

1. The issue has been oversubscribed as per the base issue size of Rs. 1,500 crore, whereas I have considered the total issue size of Rs. 8,663 crore including the green-shoe option.

2. After considering the brokerage charges, if the yield to maturity (YTM) of the listed bonds is higher than the coupon rates of the new issues, then you can consider buying it from the secondary markets.

Hi, 2 questions:

1. The NSE website (IPO current issues)shows this issue as oversubscribed, but as per ur numbers there is still a long way to fully subscribe this issue…can you pls clarify.

2. Is it worthwhile buying tax free bonds in secondary market…given that many are available at similar yields to new issues. What all should be considered while buying tax free bonds in secondary market.

Thanx in advance! I have found ur website recently and find it very helpful. Keep up the good work.

Regards,

Jaspreet

Yes, apart from me, there are several individuals I know, who would have surplus finds due to maturity of their Tax Saver FDs, FDs, SCSS and ELSS MFs. So last week of March is an important time for reinvestments.

Please do tell us if you are expecting some good issues or other investment avenues including TF Bonds during the last week of March especially good for senior citizens.

Please donot treat it as a personal issue but a common issue.

Thanks.

I’ll try to work on this topic and present you the analysis to the best of my abilities. But, at present, tax-free bonds look to me as the best fixed income investment option and maturity proceeds of an investment could be considered for these bonds.

Apart from this IRFC and NHAI any other Tax Free Bond expected during this FY? I am keen to know, if any Issue will be open between 20-31 March 2014 as my SCSS deposit matures then. Is it a good idea to premature that? What will be the cost for that?

IIFCL will launch its 3rd tranche and IRFC will launch its 2nd tranche sometime this year. Apart from that, IREDA, Ennore Port, Cochin Ship Yard and Airport Authority will also come up with their issues. But. I am not sure about the timing of their issues, so I cannot really comment whether any issue will be available at the fag end of this financial year or not.

Premature withdrawal of any investment requires proper analysis and it would differ from case to case.

Day 4 (January 9) subscription figures:

Category I – Rs. 160.30 crore as against Rs. 866.30 crore reserved

Category II – Rs. 469.91 crore as against Rs. 2,598.90 crore reserved

Category III – Rs. 398.84 crore as against Rs. 1,732.60 crore reserved

Category IV – Rs. 698.72 crore as against Rs. 3,465.20 crore reserved

Total Subscription – Rs. 1,727.76 crore as against total issue size of Rs. 8,663 crore

Day 3 (January 8) subscription figures:

Category I – Rs. 160.30 crore as against Rs. 866.30 crore reserved

Category II – Rs. 450.35 crore as against Rs. 2,598.90 crore reserved

Category III – Rs. 351.54 crore as against Rs. 1,732.60 crore reserved

Category IV – Rs. 650.87 crore as against Rs. 3,465.20 crore reserved

Total Subscription – Rs. 1,613.06 crore as against total issue size of Rs. 8,663 crore

I was surprised by the Business Line recommendation to avoid the IRFC issue, but then it makes sense to subscribe to the IIFCL issue which is offering higher rate of interest and the 20-year option as well.

http://www.thehindubusinessline.com/money-wise/irfc-bonds-give-this-one-a-miss/article5549091.ece

Please notify me of followup coments via e-mail

Day 2 (January 7) subscription figures:

Category I – Rs. 160.30 crore as against Rs. 866.30 crore reserved

Category II – Rs. 440.70 crore as against Rs. 2,598.90 crore reserved

Category III – Rs. 325.70 crore as against Rs. 1,732.60 crore reserved

Category IV – Rs. 577.62 crore as against Rs. 3,465.20 crore reserved

Total Subscription – Rs. 1,504.32 crore as against total issue size of Rs. 8,663 crore

I presume these are ‘cumulative’ subscription figures as at end of day-2?

Yes, these are cumulative figures.

Day 1 (January 6) subscription figures:

Category I – Rs. 150.30 crore as against Rs. 866.30 crore reserved

Category II – Rs. 422.11 crore as against Rs. 2,598.90 crore reserved

Category III – Rs. 308.23 crore as against Rs. 1,732.60 crore reserved

Category IV – Rs. 462.53 crore as against Rs. 3,465.20 crore reserved

Total Subscription – Rs. 1,343.17 crore as against total issue size of Rs. 8,663 crore

Hi Shiv

This is excellent. Looks like there is suddenly huge interest in tax free bonds. In spite of around 500 crore of additional retail money locked in NHB refunds and interest rate of IRFC much lower compared to earlier issues , 460 crore of retail subscription in IRFC is very good. What do you think is prompting retail to show a sudden interest in tax free bonds? After a series of TFB issues , i was not expecting such a welcome response for IRFC

Regards

Ramadas

Hi Ramadas,

I think more and more retail investors are joining the party of high tax-free interest rates these bonds are offering. I think this is due to print media and online coverage of these bonds in large numbers. Also, people who missed out on earlier issues or who have large corpus of investible surplus, are also investing on the first day itself.

Some of the factors I mentioned in the NHB post are applicable to this IRFC issue as well. Let’s see what coupon rate NHAI carries for its tax-free bonds.

Commenting to subscribe the comments feed. I have parked the amount most likely to get refunded from NHB to IRFC today. Probably this will be my last tax free bond purchase. Already hold NHAI from previous years issue.

That’s great Bhaskar!

Hi Shiv,

A basic question

My demat statement shows the following entry for the last years IRFC bonds.

INDIAN RAILWAY FINANCE CORPORATION LIMITED 7.34/7.84 BD 19FB28 FVRS1000 LOA UPTO 18FB13/- Beneficiary Balance

From the above I could make out that

7.84 stands for interest rate

19FB28 : bond is upto 19th Feb 2028

FVRS1000 : face value Rs 1000/-

what is LOA UPTO 18FB13?

And how should I know the interest payment date from this entry?

If you could enlighten about the same it would be great. Thanks.

Hi Hemant,

I am not sure what this LOA exactly stands for, but I think it seems to me as “Letter of Allotment” dated February 28th, 2013.

Interest Payment Date is February 19th every year.

http://www.bseindia.com/markets/debt/scripwise_tradereport_new.aspx?pagename=di&Scrip_ID=961756&isin_no=INE053F07579&scripcode=961756

makes sense. Thanks for the reply Shiv.

You are welcome Hemant!

Hi Shiv,

Is this correct that bonds issued in 2012 had reduced interest rates for purchases made in secondary market? If so what is the case with recent issues (specially bonds issued in last 2-3 months)?

Yes Ikjot, that is right. It used to happen last year for the bonds issued during FY 2012-13. This “step-down interest rate” clause is not applicable for the bonds issued during FY 2013-14.

I mentioned this positive development in the following post during August 2013 – http://www.onemint.com/2013/08/16/tax-free-bonds-notification-fy-2013-14/

Thanks Shiv.

You are welcome!

Deadly silence! No queries, No answers, Nothing more to learn? Have all of us become Financial Literates about Tax Free Bonds?

Any news about fortcoming issues during January, their compatative analysis and coupon rates expected?

NHAI issue is expected to open sometime this month. Coupon rates are not announced as yet and comparative analysis is not possible till the rates are not announced.

While waiting for the coupon rates, can we have some data on the financials of NHAI. The highlights of the balance sheet etc. As you know if the NHAI were to have a higher coupon like NHB ( Which I am not expecting, It will be mostly on par with IRFC 8.5-8.7 for 10 Year bond and 15 respectively), it is likely to get subscribed on first day itself and we will not have much to discuss. My experience of NHAI first issued bonds, they have done better than others. One of the reason was they had same coupon rates across and liquidity was better for the same season.

Hi George,

I think there are better things to be covered in a post than just NHAI financials which in any case we’ll have to cover in its tax-free bonds issue as well. What do you think?

Unlike other companies, I found some difficulty in figuring out the financials of NHAI from draft prospectus and also from their site. Since there are many issues coming and most of them are rated AAA by credit agencies, I feel it is very important to know the financial stability of the organization considering that the bonds are secured and asset base is very important. I have only requested to consider covering key futures based on Draft prospectus since there is not much time for people due to the oversubscription likely to happen. I leave it for you to cover what you think important in the post.

Sure George, let me give it a try if I am able to cover it before the issue details get announced by the company.

“Application Form of IRFC Tax Free Bonds”……The Application Forms are NOT available at this link, given in your post above ??

Application forms are yet to get uploaded on this link, it will get done sometime in the next couple of days time.

Sir, IRFC application forms have got uploaded now, you can download it from the above pasted link.

Can PVT CO issue TAX free bond

No Santonu, private companies are not allowed to issue these bonds.

I mean new issues coming up

My take is like this. NHB & IRFC both are strong institutions given the fact that they both are supported by RBI and MOR. One can consider investing in both to take care of diversification based on their investment. I will look at investing in 10 years bonds in IRFC and 15,20 years in NHB. The difference of interest rate of IRFC and NHB in 10 years is small. You also can wait to invest in IRFC rather than jumping on the first day considering the size of the bond. It will take full 1 month unless something drastically change in market interest rate. Thos looking for 10 years can wait to subscribe in IRFC which will give them a chance for looking at no issues like NHAI also.

I agree with your thoughts George !! With IRFC, we don’t have one full month to decide though. But, you are right, no need to jump on to it in the first few days.

Looking at the size, I will expect the IRFC to extend the closing day by 2 more weeks.

hmm, quite likely, shifting it to February 20, 2014 probably… 🙂

Having invested in HUDCO 1 & 2, PFC, NHPC, NTPC and IIFCL in last 2-3 months. I’m now putting a big chunk of my investment in NHB 20 year option . Also due to it being subsidiary of RBI I believe its equally safe as IRFC and btw am skipping IRFC issue just because of low interest rates. But still keeping some funds aside for NHAI in case it has better rates.

I would call it a good strategy !!

Would not quite agree on this. Yield on NHB per lakh would be Rs 8510/- and on IRFC Rs 8480/- on 10 yr option…a difference of only Rs 30/- per lakh per yr !

Considering the inherent strengths of both, NHB & IRFC it would be worthwhile investing in both the issues especially in view of the fact that interest rates for remaining Tax Free Bonds Issues are likely to move south. Also, some of the scheduled issues may not see the light of the day as in previous years.

10 yrs horizon is a safe bet in the current scenario. The temptation for 15/20yrs , with marginal interest rate differential, is best avoided.

Different people have different opinions Sir. Most of the investors go for the 15-year or 20-year options and that makes me think that NHB is a better option than IRFC. There is liquidity factor also.

I agree with you that diversification is a must with all our investments, but relatively speaking, I’m more biased towards the NHB issue.

Thanks Shiv for this post on IRFC TFB!

As you mentioned, I will go for IRFC mainly for diversification purpose.

Though both NHB and IRFC are AAA, I would prefer IRFC because the name IRFC/Railways is more familiar/known/popular than NHB. 🙂

yes that is true. i feel IRFC will exist has long as railways will. railways is really old institution, i dont see it disappering unless everyone get a helicopter to fly 😉

That applies to the RBI as well Pradeep, but your point is equally valid.

hmm, right… thanks Amlan for sharing it first !!