This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

IFCI Limited, in which the Government of India owns 55.53% stake, is coming out with an issue of secured redeemable non-convertible debentures (NCDs) from October 20th i.e. the coming Monday. IFCI plans to raise Rs. 250 crore in this issue with an option to retain oversubscription to the tune of Rs. 2,000 crore.

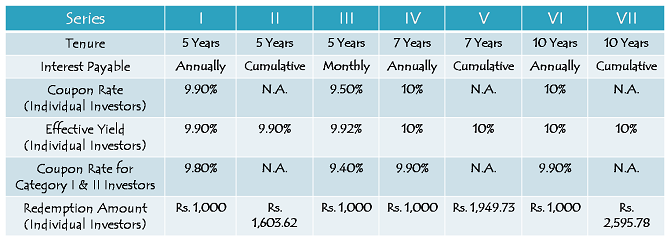

IFCI has decided to issue these NCDs for a period of 5 years, 7 years and 10 years and it is going to offer interest rate of 9.90% per annum for 5 years and 10% per annum for 7 and 10 years. The only exception is the 5-year monthly interest option, in which the coupon rate has been fixed as 9.50%. There is no monthly interest payment option with 7-year and 10-year investment periods.

Though the issue is scheduled to remain open for just over a month to close on November 21, I expect the issue to receive a good response from all categories of investors and get closed this month itself.

Categories of Investors & Allocation Ratio – The investors would be classified in the following three categories and each category will have the following percentage fixed during the allotment process:

Category I – Institutional Investors – 20% of the issue size is reserved

Category II – Domestic Corporates – 20% of the issue size is reserved

Category III – High Networth Individuals including HUFs – 20% of the issue size is reserved

Category IV – Retail Individual Investors including HUFs – 40% of the issue size is reserved

Allotment will be made on a first-come first-served (FCFS) basis.

Coupon Rates for Category I & II Investors – As shown in the table above, IFCI has kept the differential between the coupon rates offered to the individual investors and non-individual investors as 0.10% only. Though such an insignificant difference leaves me surprised somewhat, I think this move would make these NCDs quite attractive to the non-individual investors and one can expect a relatively quicker subscription in these categories.

NRI Investment Not Allowed – Foreign investors, including foreign nationals and non-resident Indians (NRIs), are not allowed to invest in this issue.

Credit Rating & Nature of NCDs – While Brickwork Ratings has assigned a credit rating of ‘AA-’ to the issue with a ‘Stable’ outlook, ICRA has given it a credit rating of ‘A’ again with a ‘Stable’ outlook. Moreover, these NCDs are ‘Secured’ in nature and in case of any default in payment, the investors will have the right to claim their money against certain receivables of IFCI.

Minimum Investment – These NCDs carry a face value of Rs. 1,000 and one needs to apply for a minimum of 10 NCDs, thus making Rs. 10,000 as the minimum investment to be made.

Maximum Investment – Anticipating a good demand from the retail investors, IFCI has kept Rs. 2 lakhs as the maximum amount one can invest in the retail investors category. Individuals investing more than Rs. 2 lakhs will be categorised as high networth individuals and there is no such cap on the investment amount for such investors.

Allotment in Demat/Physical Form – Investors will have the option to get these NCDs allotted either in demat form or physical form as per their choice, except for Series III NCDs. As Series III NCDs pay interest on a monthly basis, IFCI will allot these NCDs compulsorily in demat form.

Listing – These NCDs will get listed on both the stock exchanges, Bombay Stock Exchange (BSE) and National Stock Exchange (NSE), within 12 working days from the closing date of the issue.

Taxation & TDS – Interest earned on these NCDs will be taxable as per the tax slab of the investor and tax will be deducted at source if NCDs are taken in physical form and the interest amount exceeds Rs. 5,000 in any of the financial years. However, there will be no TDS on NCDs taken in a demat form.

Moreover, if these NCDs are sold after holding for more than 12 months, the investor is liable to pay long term capital gain (LTCG) tax at a flat rate of 10%. However, if sold prior to the completion of 12 months, short term capital gain (STCG) tax is applicable at the slab rate of the investor.

Interest Payment Date – IFCI has not fixed any date in advance for the purpose of its annual interest payment and that is why its first due interest will be paid exactly one year after the deemed date of allotment.

For monthly interest option as well, first interest payment will be made exactly one month from the deemed date of allotment and subsequently on the same date every month, subject to bank holidays.

Interest on Application Money & Refund – IFCI will pay interest to the successful allottees on their application money, from the date of realization of application money up to one day prior to the deemed date of allotment, at the applicable coupon rates. However, unsuccessful allottees will be paid interest @ 4% per annum on their money liable to be refunded.

Premature Withdrawal & Put/Call Option – Neither IFCI has the call option to redeem these NCDs nor will the investors have the put option to liquidate their investments. Once allotted, IFCI will not entertain any request for redemption of these NCDs. Investors will have to have a demat account in order to sell these NCDs on the stock exchanges.

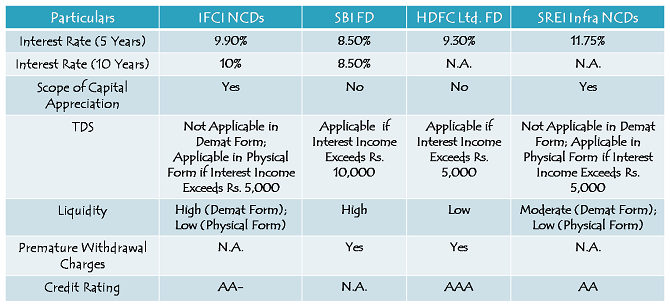

IFCI NCDs vs. SBI & HDFC FDs vs. SREI Infra NCDs

Should you subscribe to IFCI NCDs?

With CPI as well as WPI inflation falling sharply, Brent crude prices declining from $114 per barrel to $84-85 per barrel, commodity prices also correcting substantially and 10-year Indian G-Sec yield falling from 9%+ to 8.39%, I think the interest rates should still head lower going forward. In the present macroeconomic scenario, it makes sense to subscribe to these NCDs. Long term investors in the 30% tax bracket will do well to invest either in debt mutual funds or explore tax-free bonds from the secondary markets.

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in IFCI NCDs, you can contact me at +919811797407

Dear Sir,

I am in 30% bracket and want to invest in taxfree bonds from the secondary market. Kindly provide the current listed tax free bonds with their nse/bse code, ytm, cost price, coupon rate, interest rate etc and advice on the best ones to take.

Thanks and regards

Priti

Hi Priti,

Here is the list of tax-free bonds which got issued last year:

http://www.onemint.com/2014/02/01/tax-free-bonds-fy-2013-14-interest-payment-date-date-of-allotment-maturity-date-bse-code-nse-code-other-info/

Dear Sir,

please enlist govt or govt controlled company / bank etc bonds with interest rate of 9.90 and more.

thanks in advance

dear shiv.

i want to buy : from secondary Market– BSE Code – 935321; NSE Code – NH

1. can we buy for more then Rs 2 lacs still qualify retail category (higher interest) as during application time upper limit was Rs 2 lac only for retail category .. ??

2. Would you advice sell Hudco9.01 bonds 30 % premium & buy these Ifci for Rs 10 lacs (if non-taxable IT file)?

I await your valuble guidance ….

Hi,

1. As an individual investor, you can buy as much as you want and still get a higher rate of interest. Higher rate of interest has nothing to do with a retail investor or an HNI investor.

2. It is a difficult choice to make, but I would say IFCI NCDs look attractive to me for a person whose taxable income is below the threshold limit for filing ITR.

IFCI NCDs got listed on both the exchanges yesterday i.e. December 4th.

Here are the BSE and NSE codes for the same:

Series I – 9.90% interest, payable annually – BSE Code – 935311; NSE Code – NC

Series II – 9.90% cumulative interest – BSE Code – 935313; NSE Code – ND

Series III – 9.50% interest, payable monthly – BSE Code – 935315; NSE Code – NE

Series IV – 10% interest, payable annually – BSE Code – 935317; NSE Code – NF

Series V – 10% cumulative interest – BSE Code – 935319; NSE Code – NG

Series VI – 10% interest, payable annually – BSE Code – 935321; NSE Code – NH

Series VII – 10% cumulative interest – BSE Code – 935323; NSE Code – NI

Deemed date of allotment has been fixed as December 1, 2014. These NCDs will get matured after 5, 7 and 10 years respectively.

Interest will be paid on December 1st every year under the annual interest payment option and on 1st of every month under the monthly interest payment option.

dear shiv.

pl. give listing details..

when is the allotment ?

Day 20 (November 20th) Subscription Figures:

Category I – Rs. 237.31 crore as against Rs. 400 crore reserved

Category II – Rs. 317.21 crore as against Rs. 400 crore reserved

Category III – Rs. 130.88 crore as against Rs. 400 crore reserved

Category IV – Rs. 98.81 crore as against Rs. 800 crore reserved

Total Subscription – Rs. 784.22 crore as against total issue size of Rs. 2,000 crore

This issue is closing tomorrow.

I am hopeful that the Modi government would do one thing or the other to change the fortunes of the company in the coming months and years. Still I think the rates should have been at least 0.25% higher to make it more attractive for the retail investors. Let’s see how it goes.

Dear Sir,

Can we have latest subscription figures please.

Day 12 (November 10th) Subscription Figures:

Category I – Rs. 114.84 crore as against Rs. 400 crore reserved

Category II – Rs. 165.45 crore as against Rs. 400 crore reserved

Category III – Rs. 60.12 crore as against Rs. 400 crore reserved

Category IV – Rs. 70.01 crore as against Rs. 800 crore reserved

Total Subscription – Rs. 410.41 crore as against total issue size of Rs. 2,000 crore

nice info…got to learn about new numbers of oct 2014….

Whether a Educational Charitable Trust can invest their funds in the 12% NCD?

Which 12% NCD you are talking about Avadhoot?

Day 7 (October 30th) Subscription Figures:

Category I – Rs. 74.38 crore as against Rs. 400 crore reserved

Category II – Rs. 131.98 crore as against Rs. 400 crore reserved

Category III – Rs. 26.97 crore as against Rs. 400 crore reserved

Category IV – Rs. 42.19 crore as against Rs. 800 crore reserved

Total Subscription – Rs. 275.53 crore as against total issue size of Rs. 2,000 crore

sir pl. give subscription figures

after Day 4 ..

Thanks Shiv..Information helped me

You are welcome!

I want to invest in a NCD for 5 Years..currently there are 2 issues in offering…SREI and IFCI,..on interest rate front SREI takes it all; also that the credit ratings are at par for both these issues..

But still Want to know shud it be IFCI or SREI???

It is PSU v/s PRivate ????

Yes ifci ncd 2014 good investment. I am giving 1.20 % commission on total investment. Mb no 9462659179.

Day 4 (October 27th) Subscription Figures:

Category I – Rs. 34.49 crore as against Rs. 400 crore reserved

Category II – Rs. 121.77 crore as against Rs. 400 crore reserved

Category III – Rs. 18.66 crore as against Rs. 400 crore reserved

Category IV – Rs. 27.86 crore as against Rs. 800 crore reserved

Total Subscription – Rs. 202.78 crore as against total issue size of Rs. 2,000 crore