This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY)

Pradhan Mantri Suraksha Bima Yojana (PMSBY)

88% of India’s total labour force of 47.29 crore belongs to the unorganised sector, in which the workers do not have any formal provision of getting a regular pension payment on retirement. Moreover, due to increasing labour wages and better medical facilities, these people also face a risk of increasing longevity. So, this work force would require some kind of assured income guarantee to sustain itself in the coming years.

Launching Atal Pension Yojana (APY) from June 1, 2015

To encourage workers in the unorganised sector to voluntarily save for their retirement, the government of India will be launching a new scheme, called Atal Pension Yojana (APY), from 1st June, 2015. Finance Minister Arun Jaitley announced this scheme in his budget speech on February 28th.

This scheme will replace the UPA government’s Swavalamban Yojana – NPS Lite and will be administered by the Pension Fund Regulatory and Development Authority (PFRDA). The benefits of this scheme in terms of fixed pension will be guaranteed by the government and the government will also make contribution to these accounts on behalf of its subscribers.

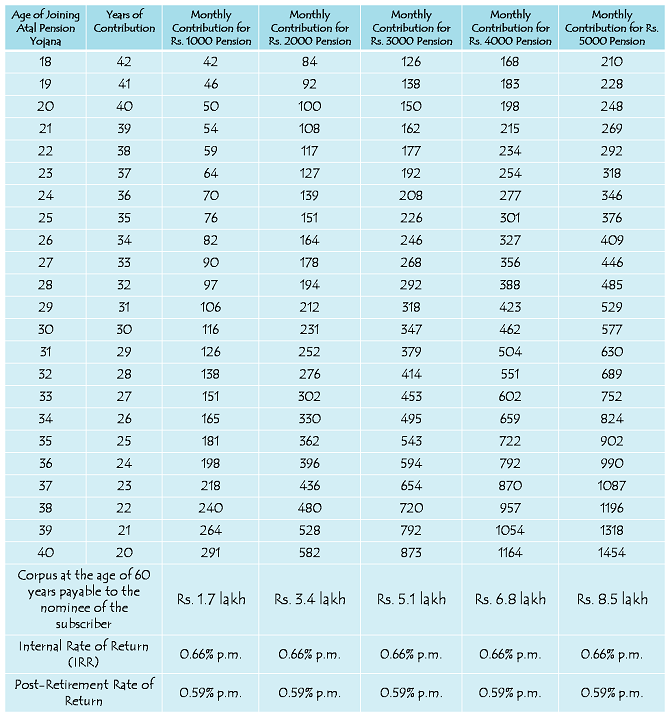

Under this scheme, a subscriber would receive a minimum fixed pension of Rs. 1,000 per month and in multiples of Rs. 1,000 per month thereafter, up to a maximum of Rs. 5,000 per month, depending on the subscriber’s contribution, which itself would vary on the age of joining this scheme.

The minimum age of joining this scheme is 18 years and maximum age is 40 years. Pension payment will start at the age of 60 years. Therefore, minimum period of contribution by the subscriber under APY would be 20 years or more.

The Central Government would also co-contribute 50% of the subscriber’s contribution or Rs. 1000 per annum, whichever is lower, to each eligible subscriber account, for a period of 5 years, i.e., from 2015-16 to 2019-20, who join the NPS before 31st December, 2015 and who are not income tax payers. The existing subscribers of Swavalamban Scheme would be automatically migrated to APY, unless they opt out.

Who is eligible for Atal Pension Yojana?

Any Citizen of India, aged between 18 years and 40 years, who has his/her savings bank account opened and also possesses a mobile number, would be eligible to subscribe to this scheme.

Government Funding – Indian Government would provide (i) fixed pension guarantee for the subscribers; (ii) would co-contribute 50% of the subscriber contribution or Rs. 1,000 per annum, whichever is lower, to eligible subscribers; and (iii) would also reimburse the promotional and development activities including incentive to the contribution collection agencies to encourage people to join the APY.

Who is eligible for Government Co-Contribution in Atal Pension Yojana?

Subscribers of this scheme, who are not covered under any other statutory social security scheme and are not income tax payers, would be eligible for the government’s co-contribution of up to Rs. 1,000 per annum.

Social Security Schemes which are not eligible for Government Co-Contribution

- Employees’ Provident Fund (EPF) & Miscellaneous Provision Act, 1952

- The Coal Mines Provident Fund and Miscellaneous Provision Act, 1948

- Assam Tea PlantationProvident Fund and Miscellaneous Provision, 1955

- Seamens’ Provident Fund Act, 1966

- Jammu Kashmir Employees’ Provident Fund & Miscellaneous Provision Act, 1961

- Any other statutory social security scheme

Minimum/Maximum Pension Payable – This scheme will pay a minimum pension of Rs. 1,000 per month and a maximum pension of Rs. 5,000 per month, depending on the subscriber’s own contribution per month.

Minimum/Maximum Period of Contribution – As the minimum age of joining APY is 18 years and maximum age is 40 years, minimum period of contribution by the subscriber under this scheme would be 20 years and maximum period of contribution would be 42 years.

Atal Pension Yojana – Contribution Period, Contribution Levels, Fixed Monthly Pension and Return of Corpus to the Nominees of Subscribers

Internal Rate of Return (IRR) – Thanks to the government funding of Rs. 1,000 per annum per subscriber account for 5 years, your account would generate an IRR of approximately 0.66% per month or 8% per annum. This pension amount per month is fixed and the government has made it clear that if the actual returns on the pension contributions are higher than the assumed returns, such excess return will be credited to the subscribers’ accounts, resulting in enhanced pension payment to the subscribers.

Minimum Contribution – A subscriber aged 18 years will have to contribute a minimum of Rs. 42 per month in order to get Rs. 1,000 pension per month starting 60 years of age. For a 40 years old subscriber, his/her minimum contribution would be Rs. 291 per month. The contribution levels would vary and would be low if subscriber joins early and increase if he joins late.

Maximum Contribution – A subscriber aged 40 years will have to contribute Rs. 1,454 per month in order to get Rs. 5,000 pension per month starting 60 years of age. For a 18 years old subscriber, his/her contribution for Rs. 5,000 monthly pension would be Rs. 210 per month.

Can I increase or decrease my monthly contribution for higher or lower pension amount?

The subscribers can opt to decrease or increase pension amount during the course of accumulation phase, as per the available monthly pension amounts. However, the switching option shall be provided only once in a year during the month of April.

What will happen if sufficient amount is not maintained in the savings bank account for contribution on the due date?

Non-maintenance of required balance in the savings bank account for contribution on the specified date will be considered as default. Banks are required to collect additional amount for delayed payments, such amount will vary from minimum Re. 1 to Rs. 10 per month as shown below:

(i) Re. 1 per month for contribution upto Rs. 100 per month

(ii) Rs. 2 per month for contribution upto Rs. 101 to 500 per month

(iii) Rs. 5 per month for contribution between Rs. 501 to 1,000 per month

(iv) Rs. 10 per month for contribution beyond Rs. 1,001 per month.

Discontinuation of payments of contribution amount shall lead to following:

After 6 months account will be frozen.

After 12 months account will be deactivated.

After 24 months account will be closed.

Subscriber should ensure that the Bank account to be funded enough for auto debit of contribution amount. The fixed amount of interest/penalty will remain as part of the pension corpus of the subscriber.

Post-Retirement Rate of Return – Considering a retirement corpus of Rs. 1.7 lakh and monthly pension of Rs. 1,000, this scheme is going to generate a return of 0.59% per month or 7.1% per annum for its subscribers. I think this return is also on a lower side.

Nomination Facility – This scheme will also provide the nomination facility to its subscribers. In case of the subscriber’s death after attaining 60 years of age, the whole corpus generating the pension income to the subscriber would be returned back to the nominee of the subscriber. In case of untimely death of the subscriber before 60 years of age, the balance would be returned back to the nominee of the subscriber.

Where to open APY Accounts – You need to approach points of presence (PoPs) and aggregators under existing Swavalamban Scheme. These agencies would enrol you through architecture of National Pension System (NPS).

Points of Presence & Aggregators

Application Form – Here you have the links to the application form for subscribing to Atal Pension Yojana – Application Form in English – Application Form in Hindi

I think a subscriber should opt for a minimum monthly contribution of around Rs. 167 or so, which would make it approximately Rs. 2,000 annual contribution. 50% of Rs. 2,000 i.e. Rs. 1,000 would be contributed by the government as well. So, the subscriber will get the maximum benefit of government funding.

As mentioned above, the scheme would start from June 1, 2015. So, interested people will have to wait till then to open an account. If you have any other query regarding this scheme, please share it here.

Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY)

How to apply all these schemes through online.. It will be very useful for techies if allowed to apply the schemes through online, If there is any such let me know.

Thanks

Hi Naveen,

You can apply PMJJBY & PMSBY through net banking platform of your bank, but APY is still not there on any online platform.

Hi shiv sir,

If in future I will get gov job then empolyer will enroll me in NPS (National Pension Scheme) and I have atal pension yojna then will both scheme valid for me and will gov contribution continue to my account in APY at the same time

Hi Atul,

This is something I have no clue about. You’ll have to approach any of the administrators with this query.

Can I open Atal pension yojna in the name of my wife.

Hi Vinay,

Every Indian citizen is eligible for this scheme.

Can 1 apply for this ataal pension yojana even if I have some other ongoing pension plans or vice versa

Yes, you can get yourself enrolled for APY even if you have other pension plans. But, you won’t get the government contribution of Rs. 1,000 per annum.

Dear sir, my self working in private company,I want to open atal pension scheme for my wife,account holder of UCO bank, cooch behar, west Bengal,India,pin-736101,several times I am going to above said bank,unfortunately bank unable to give this form

Please do the needful.

Hi Mr. Sauren,

Here is the list of POP – SP where you can get the APY account opened w.e.f. June 1, 2015 – https://npscra.nsdl.co.in/pop-sp.php

1. I have my bank account in ICICI bank. Can I apply for APY in ICICI bank

2. I am working in private sector and my EPF is deducted from my account & company also contribute and I am income tax payer. can I apply for APY

3. I am tax payer. Can I get government contribution in APY account

4. If any one not get government contribution then how much he need to pay to get same benifite

1. Here is the list of POP – SP where you can get the APY account opened w.e.f. June 1, 2015 – https://npscra.nsdl.co.in/pop-sp.php

2. Yes, you can apply for this scheme. But, you’ll not get any government contribution.

3. No

4. This is something I don’t know. Either the contribution amount would be higher or the pension amount would be lower.

Sir

I have following questions

1. I am a defence personnel, am i eligible for this.

2. If i am not eligible will my wife will be eligible who is a housewife.

3 is there any maturity amount will we get

4 if i or my wife eligible what amount monthly we had tp pay if we opt 5000

Hi Pritam,

1 & 2. Every Indian citizen is eligible for this scheme. But, if you are a tax payer or covered under any other social security scheme, then you’ll not get the government contribution of Rs. 1,000 per annum.

3. After 60 years of age, your nominee will get the corpus of Rs. 1.70 lakhs to Rs. 8.50 lakhs.

4. Contribution amount will depend on the subscriber’s age.

Sir i have ppf account can i enroll with apy. please reply me as soon as possibe. As i have submitted apy form to my bank.

Yes Mohit, you are eligible for APY. But, if you are a tax payer or covered under any other social security scheme, then you won’t get the government contribution of Rs. 1,000 per annum.

I pay provident fund which is compulsory and is deducted at source and my employer contributes to it is as well on my behalf.

so is it that i would not be eligible for this Atal Pension Yojana

Hi Jai D,

All citizens of India are eligible for APY. But, if you are already covered under EPF, then you will not be eligible to get the government contribution.

sir, Nps is for unorganized sector ???,n where it is open plz tell procedure n amount n years

Hi Resham,

Atal Pension Yojana (APY) and NPS Lite are for the unorganised sector. You need to contribute up to the age of 60 years in APY and here is the list of POP-SP for opening APY account – https://npscra.nsdl.co.in/pop-sp.php

hiii,

I want Open Atul Pension Yojna policy but this policy not available in our bank of baroda, mumbai 400 004

now what should i do……

Hi Manish,

Please check this link, it has the list of POP-SP where you can get your APY account opened w.e.f. June 1, 2015 – https://npscra.nsdl.co.in/pop-sp.php

the be aware money and the toll free number 18001801111& 1800110001 these all are saying that after age 60 if something happens to husband his pension of 5000 and if wife is alive after 60 then her pension amount of 5000 total 10000 she will receive till her death and after her death the nominee will get 17 lacs please clear my doubt

Hi Nitesh,

I would like to stand corrected on this. You are right, the spouse will also get the pension amount in case the husband dies after 60 years of age. But, on the death of both of them (subscriber and spouse), the pension corpus would be returned to the nominee(s).

Why NPS is a better pension plan as compared to APY ? Please discus. Because i have no idea about NPS scheme.

Hi Satya,

I think NPS has the potential to generate higher returns than APY.

what instalment I have to pay for wife’s pension for 5000 I have to pay monthly 990 or 1087 her birth date is 10 – 11 – 1978

I think it should be Rs. 990.

Not only U take somuch effort and give all this info

But u answer to every question (even if it is answered earlier).

Its really great of u.

Thanks Mr. Rao for your kind & encouraging words!

sir,Is there any last date of this scheme???

There is no last date as such for this scheme Reshma.

Are there any similar or better pension schemes available at this moment?

Also i am just a MBA student so am i eligible? What exactly is unorganized sector? What documents will be required as a proof to show that the person is from unorganized sector?

some financial website & toll free number are saying that after husband”s death after age 60 here wife will get her husband’s pension of 5000 and if wife also passes away then the corpus of 8.50 lacs will be given to nomine so is this correct

Can you please share the link of one of those sites or the toll-free number Nitesh?

Sir,

Is it possible to open NPS and APY for same individual..

if Yes,then minimum how many years i have to contribute in NPS

You need to contribute till the age of 60 years in an NPS account.

Yes, you can open both NPS and APY, but you won’t get the government contribution in APY. Also, NPS Lite – Swavalamban Yojana would be merged with APY w.e.f. June 1, 2015.

1.when will be starting Form filling process of APY in bank?

2.can we open PMJJBY PMSBY in one bank(ex. In sbi) and APY in other bank(ex. In Bank of india) saving account?

3.If subscriber will died between contribution period so in that case nominee will get corpus amount or only paid preemium+interest earned?

Hi Atul,

1. June 1, 2015 is the date when they will start accepting APY forms.

2. Yes, that is possible.

3. Only the deposited amount + interest earned thereon will be payable on death before 60 years of age.