This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

The Finance Ministry on March 31st announced the applicable interest rates for all the Post Office Small Savings Schemes, including PPF, Sukanya Samriddhi Yojana (SSY) and Senior Citizens Savings Scheme (SCSS). Except for SCSS and SSY, the government has kept all other interest rates unchanged, including 8.7% for its most popular scheme, PPF.

To encourage more and more people to get the Sukanya Samriddhi Account (SSA) opened, the Government has decided to ride against the tide and has increased its interest rate to 9.20% from 9.10% earlier, an increase of 0.10%.

As the interest rate on Sukanya Samriddhi Yojana is subject to a revision every financial year, this rate of 9.2% will remain applicable only for the current financial year, 2015-16 and will be further revised in March 2016 for the next financial year, 2016-17.

But, this move of keeping its interest rate higher makes me feel that the Modi Government will continue to keep its interest rate higher going forward as well. I think, like the current financial year, they will try to keep a differential of approximately 0.50% between PPF and Sukanya Samridhi Yojana.

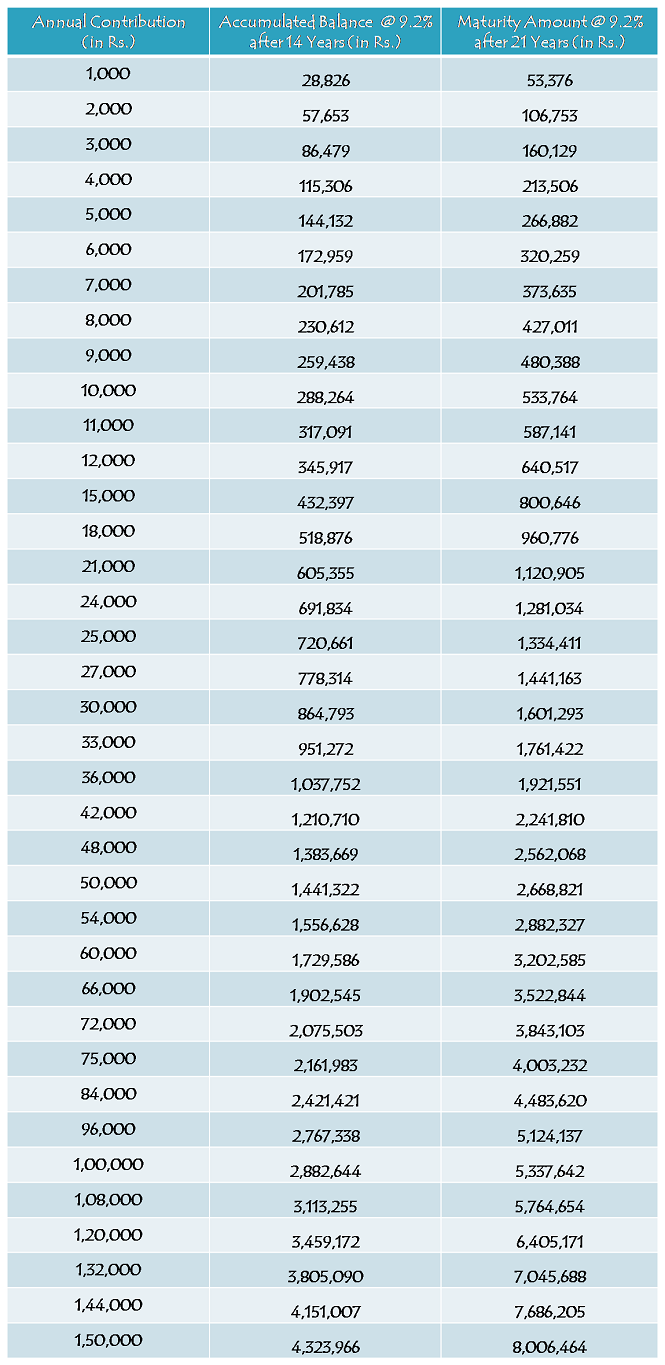

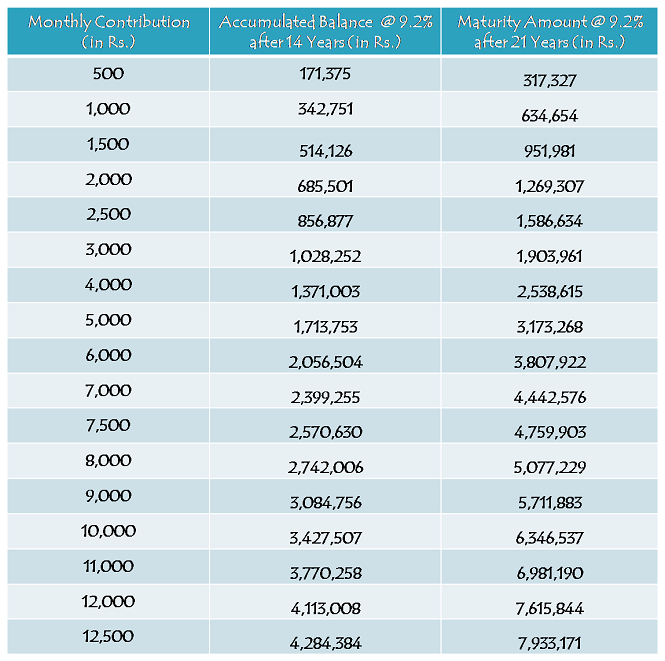

I had posted an article last month in which maturity values were calculated with 9.1% rate of interest throughout its tenure of 21 years. But, as the interest rate has been updated to 9.2% and as most of the investors are yet to open this account, I thought there is a need to have a new post having maturity values calculated as per the new rate of 9.2%.

So, here you have the tables in which maturity values are given as per your annual contributions as well as monthly contributions:

Yearly Contribution Table

Monthly Contribution Table

As different investors will have have different amounts and different timings of their deposits, it is natural that their maturity values will also be different. So, these maturity values are only indicative based on certain assumptions and here you have those assumptions:

* Rate of Interest has been assumed to remain 9.2% for all these 21 years.

* Yearly contributions have been assumed to be made on April 1 every year i.e. the beginning of the financial year.

* Monthly contributions have been assumed to be made on 1st day of every month.

* Although it is not mandatory, a fixed amount of yearly/monthly contribution has been assumed.

* It is also assumed that no withdrawal is made throughout these 21 years.

As people are looking for more and more information about this scheme, I would like to again highlight the main features of this scheme here:

Who can open this account? – Parents or a legal guardian of a girl child up to the age of 10 years, can open this account in the name of the girl child. So, if your daughter is born on or after December 2, 2003, you can get this account opened for her in a post office or an authorised bank branch.

Which documents are required to open this account? – You need birth certificate of the girl child, along with the identity proof, residence proof and two photographs of the parents/legal guardian, to open an account under this scheme. You can approach any post office or a branch of any of the authorised banks to get this account opened.

9.2% Tax-Free Rate of Interest for FY 2015-16 – As mentioned above, this scheme will carry 9.2% rate of interest for the current financial year and it was 9.1% for the previous financial year. Similarly, interest rate will be revised every year in March and will be applicable for the applicable financial year afterwards.

Scheme Matures in 21 years or on Girl’s Marriage, whichever is earlier – The scheme gets matured on completion of 21 years from the date of opening of the account or as the girl child gets married, whichever is earlier. Please note that the girl attaining the age of 21 years has no relevance to maturity period of this scheme.

Deposit for 14 years only – You need to deposit a minimum of Rs. 1,000 and a maximum of Rs. 1,50,000 only for the first 14 years, after which you are not required to deposit any amount. Your account will keep earning the applicable interest rate for the remaining 7 years or till it gets matured on your daughter’s marriage.

NRI/OCI Investment – It is still not clear whether Non-Resident Indians (NRIs) or Overseas Citizens of India (OCI) are allowed to open an account under this scheme or not. But, as it is not allowed with most of the post office small saving schemes, I think the government will not allow them to invest in this scheme either. I’ll update this post as soon as I get any information regarding the same.

Partial Withdrawal – It is allowed to withdraw 50% of the balance for higher education as the girl child attains the age of 18 years. Except for this period, it is not allowed to withdraw any amount during the whole tenure of this scheme.

Nomination Facility – Nomination facility is not there with this scheme. In an unfortunate event of the death of the girl child, the balance amount will be paid to the parents/ legal guardian of the girl child and the account will be closed immediately.

You can check all the features of this scheme from this post – Sukanya Samriddhi Yojana – Tax-Free Small Savings Scheme for a Girl Child

You can also check the updated list of banks and download the application form to open an account from this post – Sukanya Samriddhi Yojana – Updated list of Authorised Banks to Open an Account, Specimen Application Form & Passbook. If you have any query or something related to all these posts, please share it here.

Sir.my daughter 2 years old.before i am sended u sms by mail. Plz suggest me.

Hi Suman,

I haven’t received any mail from your id.

Can my daughter who is citizen of uk open an account for her daughter who is 8 years old?

Hi Raju,

Foreign Citizens are not allowed to open this account.

Sir,mere daughter 2 years later hai. How many years I will deposit the amount. And when I receive the amount attest 19 to 20 lakes. That for which amount I will deposit monthly or yearly.plz help.as soon as possible.

Hi Suman,

Aapko 14 saal paisa deposit karna hai, tab tak aapki beti 16 saal ki ho jaayegi. Aapki second query clear nahin hai.

My daughter is 8.5 yrs old. What is the maturity amount i will get after 21 yrs if i invest Rs. 1000/- monthly.

Approximately Rs. 6,34,654 @ 9.20% interest. However, 9.20% is not fixed.

ensure this open sukanya samriddhi accounts RBI Notification March 11, 2015 abi thak kishe bank ne account nahe khola

Surenderji, PNB & IDBI Bank ne ye accounts kholne shuru kar diye hain. Please visit any of their branches to get this account opened.

kab tak bank me sukanya samriddhi ka account open hoga

sir,

my daughter will be completed 10 years coming on 26th May, 2015. Can i open this account (SSY), i would like to invest Rs. 1000 each month & there after can I increased Rs. 500/- every year.

Hi Rajesh,

Yes, your daughter is eligible for this scheme. Also, you can increase or decrease your investment amount as per your comfort.

Hi…

Meri 4 month ki beti hai ager main her saal Rs.50000.00 jama ker raha hu to mujhe after 21 years kitne paise milenge….Remember every year..

Hi,

At an assumed rate of 9.20% per annum and Rs. 50,000 contribution every year, your daughter will get approximately Rs. 26,68,821 after 21 years from the account opening date.

Hello sir,

Mare 2 betiya ha 8 or 6 saal ki.agar me yearly 1000 Rs.jama karvata hu to maturity ke baad mari batiyo ko kitna paisa milega.

Hi Mahendra,

Rs. 1,000 har saal ke hisaab se maturity ke time aapki betiyon ko Rs. 53,376 milenge. Maturity amount aapke contribution aur rate of interest pe depend karega.

Respected sir,

please correct me if i am wrong.

agar Mahendra ji ki beti abhi 6 saal ki hai to scheme ki maturity 21 ki age tak sirf 15 saal bachte hain.. 15 saal ke compound interest ke hisab se amount Rs. 31477 hota hai.

1. aur inki badi beti 8 saal ki hai to scheme ki maturity ke liye 13 saal bachte hain, to kya ye scheme ki maturity ke baad bhi Rs. 1000 daal sakte hain ?

2. Kyunki 14 years ke baad aur paise nahi daalne hain lekin jab tak amount withdraw na ho interest tak milte rahega ?

3. Agar inki beti 30 ki age pe withdraw karna chahti ho, tak kya 30 ki age tak compound interest milega ?

dear sir,

plz share bank name who started this scheme. Is SBI started? if no when they do this?

Hi Vikas,

PNB & IDBI Bank have started opening these accounts. SBI has still not started opening these accounts and I have no idea by when they will do that.

Hi Shiv,

But I have checked with both IDBI and PNB bank and they told me that they do not have any update or so for SSY account. Can you please provide more details like which branch and bank this is happening for sure.

thanks.

No schemes for boys,after all all r not rich

No, there is no special scheme for boys out there.

Sir meri beti 5 year ki he or mine ssy ka acaunt khulwaya he 1000 manthly he to is hisab se 182000 + 9.20 ke alawa sarkar ky degi hame ya fir hamare hi paise hamko ritan dekar ki ya hame ssy ka koi extra bonus degi

Nahin Kaluramji, is scheme mein koi bonus nahin milega.

Meri ladki 1.5 year ki hai

Hi Javed,

Please check this post, ismein saari details hain – http://www.onemint.com/2015/03/03/sukanya-samriddhi-yojana-tax-free-small-savings-scheme-for-a-girl-child/

Sir mujhe plan batayenge

agar 1000 rs per month jama krenge to 21year bad kitna milega

Please check the table above, it is Rs. 634,654 as per 9.20% rate of interest.

Is there any income tax on maturity?

Hi Bhuvnesh,

There is no tax to be payable on maturity.

sir,, mai ye janana chahta hun ki agar beti ki shadi maturity se pahle hoti hai to kya 21 sal bad jo paisa milna tha utna milega ya kam ?

Hi Anshu,

Beti ki shaadi maturity se pehle hone pe aapko kam maturity value milegi.

Sir meri do beti hai keya dono ka Accounts open ho sakta hai and aur id proof keya lge ge meri ek beti 5 yares hai ek kevl 2 month pls answer thanks

Hi Rajkamalji,

Yes, aap dono betiyon ke accounts open karwa sakte hain. Aapko apni betiyon ka sirf birth certificate copy provide karna hai, id proof aapko apna dena hoga.

Sir

my daughter age is 1o yr & i opened SSY on her name

Can i deposit Rs 150000 per yr for the next 14yr i.e (2029) or

i can deposit Rs 150000 per yr for the next 8 yr only i.e (2023) or

in both the case how much i will get after maturity age @21 i.e (2036)

or maturity age will be 2025 (21 yr of girl age)

Considering all details how , when, i can get the maximum benefit.

Hi Mr. Basant,

1. You can deposit Rs. 1.50 lakh per annum for a period of 14 years i.e. till 2029 or till your daughter gets married, whichever is earlier.

2. Your daughter’s account will get matured in 2036 or when she gets married, whichever is earlier. With Rs. 1.50 lakh annual contribution & 9.20% rate of interest, maturity value after 21 years would be Rs. 80,06,464.

Dear Sir,

I have just opened SSY account for my daughter who is 10 years old. I shall deposit Rs. 50,000 per year. Please let me know the maturity amount when she is 14 years old and 21 years old.

Dear Mr. Sanjay,

This scheme will not mature when your daughter’s age is 14 years or 21 years. You need to deposit money for 14 years from the account opening date and it will mature when your daughter gets married or when she turns 31 (10 age + 21 years), whichever is earlier. For maturity values as per your yearly/monthly contributions, please check the tables above.