This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at shivskukreja@gmail.com

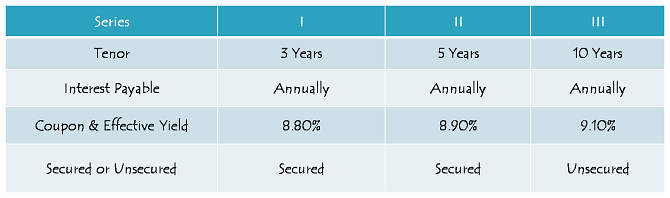

Tata Capital Financial Services Limited (TCFSL) is launching its public issue of secured redeemable non-convertible debentures (NCDs) and unsecured subordinated redeemable NCDs from the coming Monday, September 10, 2018. The issue is rated ‘AAA’ by the rating agencies CRISIL and CARE and will carry an effective annual rate of 9.10% for 10 years, 8.90% for 5 years and 8.80% for 3 years.

The company aims to raise Rs. 7,500 crore from this issue, including a green-shoe option of Rs. 5,500 crore. The issue is scheduled to close on September 21, but in case of oversubscription, the company will have the option to foreclose it.

Before we dig further to find out if the issue is worth investing, let us first check some of the key features of this issue.

Size & Objective of the Issue – Base size of the issue is Rs. 2,000 crore and there is a provision for the company to exercise the green-shoe option to raise an additional Rs. 5,500 crore in case of oversubscription, thus making it a Rs. 7,500 crore issue. The company plans to use at least 75% of the issue proceeds for its lending activities and to repay its existing loans and up to 25% of the proceeds for general corporate purposes.

Coupon Rate & Tenor of the Issue – As mentioned above, the company is issuing these NCDs for a period of 3 years, 5 years and 10 years. These NCDs will carry coupon rates in the range of 8.80% to 9.10%, with annual interest payment as the only interest payment option.

Unsecured, Subordinated 10-Year Option – NCDs issued for a period of 10 years would yield you 9.10% on an annual basis, but would also be unsecured and subordinated in nature. That would mean the investors of these NCDs will have no or fewer rights to seek compensation by selling certain assets of the company in case it defaults on its regular interest payments and/or principal repayment.

Minimum Investment – Investors need to apply for a minimum of 10 NCDs in this issue with face value Rs. 1,000 each i.e. an investment of Rs. 10,000 at least.

Categories of Investors & Allocation Ratio – The investors have been classified in the following four categories and each category will have the below mentioned percentage fixed in the allotment:

Category I – Institutional Investors – 20% of the issue i.e. Rs. 1,500 crore

Category II – Non-Institutional Investors – 20% of the issue i.e. Rs. 1,500 crore

Category III – High Net-Worth Individuals (HNIs) – 30% of the issue i.e. Rs. 2,250 crore

Category IV – Retail Individual Investors (RIIs) – 30% of the issue i.e. Rs. 2,250 crore

Allotment on First-Come First-Served Basis – Subject to the allocation ratio, allotment will be made on a first-come first-served basis, as well as on a date priority basis, i.e. on the date of oversubscription, the allotment will be made on a proportionate basis to all the applicants of that day on which it gets oversubscribed.

NRIs Not Allowed – Non-Resident Indians (NRIs), foreign nationals and qualified foreign investors (QFIs) among others are not eligible to invest in this issue.

Credit Rating & Nature of NCDs – CRISIL and CARE have rated this issue as ‘AAA’ with a ‘Stable’ outlook. Moreover, these NCDs will be ‘Secured’ in nature for a period of 3 and 5 years, and ‘Unsecured’ in nature for 10 years.

Listing, Premature Withdrawal Option – These NCDs will get listed on both the stock exchanges i.e. Bombay Stock Exchange (BSE) as well as National Stock Exchange (NSE). The listing will take place within 12 working days after the issue gets closed. As there will be no option of a premature redemption, the investors can always sell these bonds on the stock exchanges.

Demat A/c. Mandatory – Demat account is mandatory to invest in these NCDs as the company is not providing the option to apply for these NCDs in physical or certificate form.

TDS – Though the interest income would be taxable with these bonds, NCDs held in demat form will not attract any TDS. The investor will have to pay tax on the interest income while filing his/her income tax return.

Should you invest in Tata Capital Financial Services NCDs?

India has clocked 8.2% GDP growth in the first quarter of the current financial year, and with rising crude prices, 10-year bond yield has again jumped to cross the psychological mark of 8%. So, in a rising bond yield scenario, investors expect banks and companies to offer higher interest rates on their deposits.

However, the company has decided to offer even lower interest rates than offered by the companies in the last six months or so, probably because it has been rated ‘AAA’ by the rating agencies and the brand name of Tata behind it.

I consider these coupon rates offered by a private company to be below my expectations. One can consider investing in gilt funds or other debt funds as compared to these low-yield NCDs. However, conservative investors can consider investing in these NCDs, as it is not easy to find many ‘AAA’ rated issues these days offering coupon rates higher than the bank FDs.

Investors, who fall in the lower tax brackets and are looking for relatively safer options to invest their investible surplus, can think of investing in this issue. Again, I think one should go for the shortest possible time period to invest with a private company. So, either a 3-year option or 5-year option should be chosen to invest in these NCDs.

Application Form – Tata Capital Financial Services NCDs

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in Tata Capital NCDs, you can reach us at +91-9811797407

Dear Shiv,

Any idea where we can check allotment status and when is it getting allotted, listing dates etc. Many thanks.

I do see the following in my bank statement for the full amount, had applied on the first day morning itself in retail quota –

27-Sep-2018 (27-Sep-2018) TO TRANSFER

TRANSF TO TATA CAPITAL NCD ALLOTMENT

Sir,

I would like clarity on your advice to Mr Poddar.

My query is posted above .

Can you please reply.

Now that the issue has not been subscribed to the expected level, what is going to be the likely time for allotment and listening of the NCDs.

Has there been any adverse development in Tata groups that may have an adverse impact on these NCDs.

Thank you.

What is the allotment date and listing date?

Day 4 (September 14) Subscription Figures:

Category I – Rs. 28.20 crore as against Rs. 1,500 crore reserved – 0.02 times

Category II – Rs. 110.43 crore as against Rs. 1,500 crore reserved – 0.07 times

Category III – Rs. 180.57 crore as against Rs. 2,250 crore reserved – 0.08 times

Category IV – Rs. 1,323.50 crore as against Rs. Rs. 2,250 crore reserved – 0.59 times

Total Subscription – Rs. 1,642.70 crore as against total issue size of Rs. 7,500 crore – 0.22 times

As of Wednesday Tata Capital NCD is subscribed over 2 times in the retail portion (category IV), other categories are not fully subscribed yet. If I apply now in category IV is there a chance me getting allotment (will they allot the unsubscribed portion from other categories to category IV ?). Thanks.

Thank you for your articles on One Mint on Tata Capital Financial Services 9.10% Non-Convertible Debentures (NCDs) – September 2018 Issue

& IndiaBulls NCD. What are the closing dates for these NCDs?

Hi Rakesh,

Tata Capital issue closing date September 21, Indiabulls issue closing date September 28.

Sir,

Very often my comments go into awaiting moderation mode and then cannot be seen.

what can be done about that?

Hi Vanita,

If your comments are simple, do not have any complicated or foul language, then they should not go in for moderation.

total 7500 isue including green shoe am i correct

Day 2 (September 11) Subscription Figures:

Category I – Rs. 18.08 crore as against Rs. 400 crore reserved – 0.05 times

Category II – Rs. 103.84 crore as against Rs. 400 crore reserved – 0.26 times

Category III – Rs. 159.80 crore as against Rs. 600 crore reserved – 0.27 times

Category IV – Rs. 1,162.31 crore as against Rs. Rs. 600 crore reserved – 1.94 times

Total Subscription – Rs. 1,444.02 crore as against total issue size of Rs. 2,000 crore – 0.72 times

Subscribed to series 2 today. AAA rating, being secured NCD and Tata reputation was the reason. Would have chosen 10 year option if it had been secured NCD. Had subscribed to tax free bonds few years back which in hindsight was a very wise choice. Sold small part of equity portfolio to invest in Tata capital. Lets see how it goes.

Thanks for sharing!

today’s subscription figures please

https://nseindia.com/products/content/equities/ipos/debt_ipo_current_tcfslncd.htm?cat=DA

overall 0.61 times subscribed but category 3 subscribed 1.61 times. They have greenshoe option so hopefully everyone who applied today may get allocation.

Shiv may please add his very useful commentary.

Hi Bhaskar,

It is highly likely that the company would retain all retail subscription till the issue gets subscribed to the tune of Rs. 7,500 crore.

very accurate information

Thanks K T Jadhao!

aadhar housing finance care for 10years

monthly 9.35% anually 9.75% on 14th Sep

Thanks Mr. Nitesh for sharing this info!

Very well said. You are an expert. Would have been nice if you had also recommended category for better allotment.

Hi Mr. Poddar,

As the HNI category is not getting subscribed at a faster speed as compared to the retail category, it seems it is better to apply in the HNI category.

Hello Sir,

We retail investors can choose which category to apply under?

We can apply as HNI category or NII category also?

I thought we do not have any choice..a retail investor has to apply

in retail category is what i understood.

Shiv Sir,

Can u please answer my above query?

It is in reply to Mr Poddar’s Query.

Interest rate for senior citizen?

Hi Mr. Shah,

Interest rate is the same for senior citizens as well.

Please let me know any good Investments

mahindra Finance Ncd unsecured 9% annually is trading at 1030 so definitely tata capital ncd unsecured 9.10% will list at 20 to 30 rupees premium and is rated triple rating by both icra and care and these are most reiable credit agencies so it dosent matter secured or usecured just go for it

Dear Sir,

As per the News today on CNBC Aawaz, there is additional interest for retail investors. But in above details, it is not given. What is correct position?

Thanks

Hi Rahul,

The table above incorporates that extra 0.10% for the retail investors.

Coupon rate is almost at par with any other NBFC. But coupon payment frequency is yearly. Had it been with option of quarterly or half yearly, the effective rete would have been more. But since there is no other option issue is less attractive.

Hi V R Lagu,

These days issuers are issuing these NCDs with effective rates being equal for monthly, annual and cumulative interest payment options. So, no extra benefit in having monthly option available as far as interest rate is concerned.