Liquid funds are getting increasingly popular these days because of the high interest rates, safety, and tax advantage that they offer.

Liquid funds invest in treasury bills, government securities, call money, repo and reverse repos and other such instruments that are quite safe in nature and have a short maturity. This means that they are good for parking that part of your money that you would have otherwise put in a bank savings account.

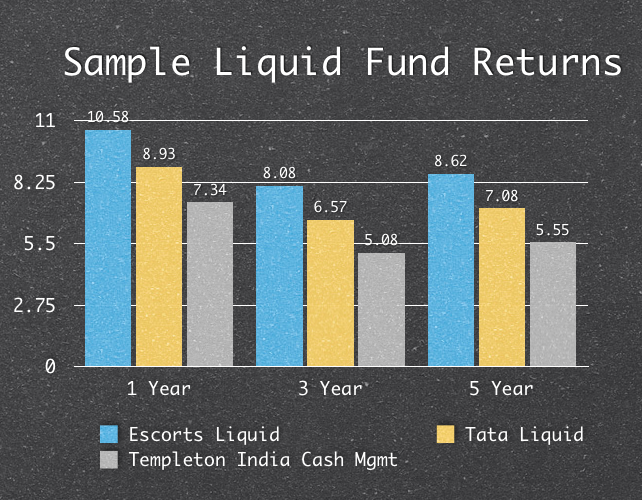

There are a large number of liquid funds available in India and to give you an indication of the returns they have generated in the past few years, I took the returns of 3 funds that were rated high, medium and low for the long term by Value Research.

You can see those returns in this chart.

As you can see, last year has been particularly good for liquid funds, and that is beginning to show in the fund inflows as well. ET reports that during the month of May 2012, liquid funds had the largest inflow of funds in any category and got over Rs. 25,000 crores.

Liquid Fund Tax Benefits

Liquid funds are taxed long term capital gains at 10% without indexation and 20% with indexation. The short term capital gains are charged at the marginal tax rate of the investor and the dividend distribution tax is charged at 25% but that’s in the hands of the fund house and not the investor, so the returns that you see in the chart above have taken care of that.

In general, liquid funds do not have exit loads, and the ones that I checked showed this to be true, however I’m not sure that this is true across each and every liquid fund that exists in India.

Liquid Funds versus Savings Account

It used to be that liquid funds were a lot better than savings accounts because their returns were higher than savings account interest rates and they were taxed at a lower rate than the savings account interest income.

While this is still true, two things have reduced their advantage in recent times.

The first one is that savings bank rates have been liberalized and you can get 6% or so in a savings bank account now, and secondly, bank fixed deposits for short periods like 3 months can now give you as much as 8.25%, and you can always move some part of your emergency funds to these short term deposits especially when a lot of these can be opened electronically and don’t have a penalty when you break them.

I feel that liquid funds definitely have a place in your portfolio if you are in the higher tax bracket but you can’t focus too much on it because the absolute difference that you get by investing in a liquid fund versus a savings bank account shouldn’t be a lot. If it is a lot, then you have to ask yourself where else you can invest this money for a longer duration to get better returns.

This post was from the Suggest a Topic page

I’ve heard people say that if you have a lumpsum, then invest it in a liquid fund and then initiate an STP to transfer it to an equity fund over a long period. My question is that whether my liquid fund investment would be subject to any short term capital gains tax, since the STP would be initiated almost immediately.

HI anusha, I work for for fund house you can send mails to us, Thanks

Hi, Manshu!

I wanted to know whom to approach for investing in liquid funds. Say, I want to invest in Tata Liquid Fund… Where do I head? And whom should I consult?

Erm… I’m new to Liquid Funds. I didn’t really understand even after having read the article twice. Could you please provide links that might help a beginner?

That’s certainly very disappointing for me Anusha….Here are a couple of links that might help you. Do you have any questions about them though? Maybe I can answer those and that may help you understand better.

For starters, they are a type of mutual fund, and within mutual fund they are very short term debt funds which means they invest in fixed income low risk instruments.

http://articles.economictimes.indiatimes.com/2009-03-09/news/27644816_1_liquid-funds-money-market-instruments-reasonable-returns

http://investorskool.blogspot.com/2008/08/what-is-liquid-fund.html

Thanks, Manshu! Now I have a fair idea. It’s a kind of mutual fund that is good for short term returns that are slightly higher than FD rates, and they are one of the safest instruments. Is that right?

Liquid funds are for parking very short term money. Essentially all funds “pending for deployment” in the next 3 months should be swept into liquid fund. Liquid fund are alternative to both saving bank account and fixed deposits, as they offer higher interest rates than former and can be redeemed without any penalty (whereas FD premature closure attracts penalty + lower interest than card rate).

Thanks, Ankurm! 🙂

Does any of the liquid funds provide debit card?

I heard that few of the cash managament funds offer such service.

Reliance does provide a debit card…

Ur welcome

Hi

What is the risk factor in these funds? Thats key for me. Citi and SCB both are offerring 9.25% for 187 days FD .Is it guaranteed return in liquid funds or do you I risk losing some amount?

The return is not guaranteed harinee so the return could very well be less than this amount. Even the principal is not guaranteed but as far as I know, no liquid fund has gone below face value so far.

Principal has not gone below face value as Liquid funds mostly invest in debt papers 60 days will be MTM). At present, valuation is based on accrued interest. Anyways, valuation risk is very low for lower duration instruments.

see this: http://capitalmind.in/2012/07/the-owner-of-deccan-chargers-defaults/ as an example of the kind of risk for these funds. Personally, I try to look for large AUM and diversified holdings so that risk to any one company is low/limited – of course, can’t be guaranteed safe…. but it should be good enough.

In this case Deccan was only 1.3% of Pramercia liquid fund. Further, it seems to be a only delay of repayment (due to timing mismatch) and not default. The link talks about fund house taking a hit, if at all how will that be accounted for?, as the fund units are held in a trust and AMC is only a manager.

hi manshu, the returns in the chart are before tax for the growth option; you could cross check from moneycontrol.com.

In general, the clincher for liquid fund vs bank FD is zero penalty and non -time dependancy. When i say time dependency, it means if you invest in FD, the card rate only applies if you stay invested for entire term. Eg In March you invested in a 6 month FD at 8.5%, but you break it in 3 months (i.e. June), your effective rate will be rate applicable for 3 month i.e. 7.5% minus penalty of 1%= 6.5%. Whereas for liquid fund you would have got 9-10% for 3 months. So, if you dont know when exactly you will need money, go for liquid fund. As regards, saving bank a/c, unless you have with Kotak or Yes it doesnt make much sense.

Yes, the returns will be before tax as they generally are since they can’t assume when you sold what indexation you took and all that.

I guess that works both ways because if you happened to have a lemon fund then you may hold it for the entire duration and it still doesn’t generate enough returns. It’s only recent performance where almost everyone has done well but if you go back a few years there have been funds that didn’t do so well. Right? What do you think about this uncertainty element, especially for someone who is not in the high tax bracket?

Actually, my experience with FD has been worst, there has been greatest opportunity loss when i prematurely broke it. But, if you are able to match your horizon with FD, then FD is good bet. Even in that scenario, if you have 3-6 month time horizon, Ultra short term fund scores over both FD and Liquid fund, as dividend is taxed at 12.5%. Ofcourse, all these make sense for higher tax bracket people only, for lower tax bracket, FD is safest bet.

So next post on ultra short term fund then 🙂

Thanks Ankur!

Welcome. Good idea to do ultra short term fund. ICICI pru has the widest variety of debt funds, and their website clearly explains suitability for different kind of investors.

Gr8 Manshu…so we want to see ur write up on ultra shoert term debt fund soon…tht wd be really gr8.!!!

Does HDFC CASH MANAGEMENT FUND-TREASURY ADVANTAGE fund come in this category??

http://www.valueresearchonline.com/funds/h2_typecomp.asp?type=1&objective=2

The above link will display all the Ultra Short Term Debt Funds.

Waiting for the article from Manshu! 🙂

I have seen that many of the debt funds of Birla sun life like BSL cash manager or savings funds are consistence in their returns. overall I was reading and made an assesment birla has the strongest asset base in debt catagorey.

By strongest asset base, do you mean they have the largest assets under management as far as debt funds go?

Yet another informative article….thanks for the info..

Could u please elaborate on the taxation implications of a liquid fund for a LLP (Limited Liability Partnership) Firm?? How do we decide on the option of Growth vs Dividend Re-investment??

Thanks a lot !!!

For a LLP? Not sure about that, let me see if I can find it. I remember there was an excellent answer to the growth versus dividend reinvestment option somewhere earlier on the site that someone put up.

As far as I remember they are quite similar and I think it’s better to go for the growth option. Let me see if I can hunt that answer as well.

Taxation in liquid funds is same as in case of Partnership/LLP or Domestic company. Which means if opted for dividend option (reinvestment or payout) the rate is 32.445% (30%+5% surcharge+3% cess). , and as far as captal gain is concerned

STCG: added back in your total incom and taxed accordingly

LTCG : 10% without indexation or 20% with indexation (plus surcharge and cess).

Now as far as question of selection of growth and Dividend re investment option, it woould hardly make any difference as taxation is almost the same, and thus without getting into detail go for Growth option.

As liquid funds are meant for very short term parking of funds, so in any case you don’t want to get into the calculation of DDT when there’s not much difference.

It makes difference when an individual(in high tax bracket) wants to park money in liquid funds

Plz correct me if i am wrong… If LLp firm is taxed at 32% in a liquid fund , then investing in a short term bank FD for 7-8% would also be a good option ( anyways the firm is taxed at 30%).

So my query now is-

is it beneficial to stay invested in a liquid fund for over a year so tht we can avail for LTCG which wud be more tax efficient ??

Or if I have a horizon of 6-8 Months, would a short term debt fund be a more appropriate option??

Kindly comment….

Thanks

@ Sameer …If horizon is of more than 6 months, then go with short term debt funds

hi sameer refer this link http://dev.capitalmind.in/2006/10/mutual-funds-dividend-option-or-growth/ .u ll get the answer from this link and it ll clear all ur doubts related to this topic also i suggest u to watch this video on this link http://capitalmind.in/2011/01/marketvision-videos-navs-dividend-vs/.

Thanks manish..