I had a lengthy conversation with a friend who currently lives in the US, and wanted to start investing. We touched upon various options, and I thought it would be a good idea to do a quick post with the broad outlines of our conversation. We spoke about investing options at length but before you get to those, you should ponder on the following two questions:

- How do you save?

- Where will you eventually settle?

How do you save?

The first thing I asked her was how do you save? This might sound like a strange question but I’m a great believer of saving first, and spending later. If you don’t have a way to auto debit some money into your savings account, you should give it a try. Set a fixed amount every month or even every fortnight that automatically goes to your savings account or your brokerage account and forget about the money.

If you wait to invest only what’s left after spending you will miss out on several opportunities to save that you didn’t even know existed. Without saving, there is no investment, so thinking through a plan for savings is necessary in order to build any sort of wealth.

Where will you eventually settle?

For a lot of NRIs this is a difficult question – and in my experience if you don’t feel strongly about returning to India, I’d say assuming that you will stay in the US for a long time is a safe thing. This matters because you should have access to funds in the country you plan to stay, and there is no point of owning a house in India if you are never going to live in it. Better keep the bulk of your investments close to where you are.

Answering the two questions above will help you evaluate whether the options listed below are appropriate for you. With that said, here are some options that Indians living in the US can invest in.

1. Â Real estate in India:Â If I were to do a poll of all my friends living in the US, I think the number one investment option that would come to the fore is real estate in India. There is hardly anyone who doesn’t own a plot or a flat somewhere in India, and at least on paper almost all of them have appreciated. This is perhaps the most popular investing option for Indians in US.

2. Real estate in US:Â I’m mentioning it here only to maintain continuity, as I feel buying real estate in the US as an investment is not as popular today as it was before the crash of 2008, but regardless, this is an option available to you.

3. Buying Gold Coins: Buying gold coins is a lot easier and efficient in the US than it is in India, as you can sell them easily later one without the fear of a jeweler screwing you out of your money, and that has been a popular investment also.

As you can perhaps tell, so far none of these are investment options that I recommended to my friend.

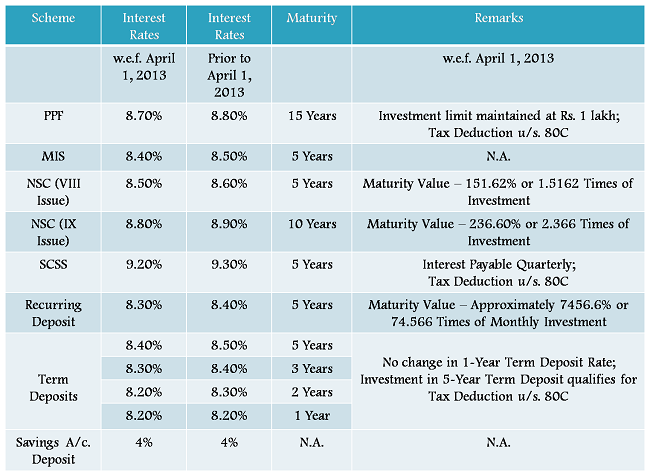

4. NRE Fixed Deposit Account in India:Â NRIs and Indians living in US can open a NRE fixed deposit account, and this is a good option if you think you will need money in India at some point. You will be able to get 8 or 9 percent tax free, and that’s a really good rate of return on a very low risk investment.

Now, a lot of people compare the 0 percent interest rate you get in the US to the 9 percent you get in India without considering the difference of inflation in the two countries, and without the effect of exchange rates. I sometimes see people transferring money to India and being unhappy with an exchange rate of Rs. 54 or Rs. 55 and these guys don’t realize that just a few years ago people were transferring money in 40s and sometimes even the late 30s. If you are going to need money in the US in a few years, and the INR depreciates even more then the difference in interest rates isn’t going to help you at all.

So, this is one thing to be careful about.

5. Buying stocks and mutual funds in India:Â NRIs can open a Demat account that is linked to their NRE or NRO account and then invest in some select stocks and mutual funds. That is one option for people who want to invest in the Indian market and are comfortable with equities.

6. Buying India based ETFs listed in the US: There are several ETFs that are listed in the US that invest in securities in India, and you can buy those if you want to get exposure to India. You can open a trading and brokerage account in the US even on a visa and then you can buy ETFs from that account.

7. Buy US based shares or Index Funds:Â This is not much different from the point above, just that instead of buying funds that have exposure to India, you now buy funds that have exposure to the US. You invest in equities in this too but the underlying is American instead of Indian shares. In the same vein, you can invest in shares that have an underlying in any economy in the world.

8. Buy US based bond funds:Â My friend wasn’t very comfortable with equities so I said that there are bond funds also that you can invest in. I am not sure how many Indians will do this given the low returns on these but as I said earlier, you can’t really compare this with INR returns as the inflation and exchange rate volatility is different.

Conclusion

I feel that the options are fairly limited and the lack of good debt options makes it so that people either invest in fixed deposits in India, or get used to equity.

My recommendation to her was to get used to equity and begin by opening a brokerage account in the US and buy index funds in small quantities. I suggested that she send some money to her brokerage account every fortnight, and then use half of that to buy one or two index funds. Let the rest lie there for when there is another panic, and then use that money to buy equities when they fall.

This is of course easier said than done and not everyone can do that. I think I’ll be able to help her do this and in a few years time frame, she will be completely bought into equities, and be able to use it to her advantage.

I will be keen to hear what others think of the options I listed out and which ones you think can be added, and what have you done that has worked for you.

A lot has been written on FDI (Foreign Direct Investment) and FII (Foreign Institutional Investor) already, and I found a great succinct explanation from Business Line explaining the difference between FDI and FIIÂ investments as one flowing into the stock market (FII) and the other flowing into the primary market (FDI), and all other differences emerging out of that one key point.

FDI (Foreign Direct Investment) is when a foreign company invests in India directly by setting up a wholly owned subsidiary or getting into a joint venture, and conducting their business in India.

IBM India is a wholly owned subsidiary of IBM, and is a good example of FDI where a foreign company has set up a subsidiary in India and is conducting its business through that company. What’s amazing about IBM is that, it is now the largest Indian IT company in India. It is serving Indian customers, and a large domestic market that was not tapped by the Indian players themselves.

Foreign companies partnering with Indian companies to set up joint ventures is more typical and Starbucks partnering with Tata Global Beverages Limited is a recent example of FDI through joint venture, but there are several others in the insurance, telecom, food industry etc.

FII is when foreign investors invest in the shares of a company that is listed in India, or in bonds offered by an Indian company. So, if a foreign investor buys shares in Infosys then that qualifies as FII Investment.

It is easy to see why you would prefer FDI to FII investments. FDI investments are more stable because companies like IBM set up offices, hire employees, and have a long term plan for the country. IBM can’t just pull out a few million dollars from India overnight, which is what FII investors do from time to time and that leads to market crashes.

In India, attracting FII has been easier than FDI because of the policy uncertainty and procedural delays. An RBI study has the following para on FDI slowdown and it is easy to see how it is tied to the politics in the country.

Both FDI and FII investments are good for the economy, but I feel that FDI is where the focus should be and this is where India is lagging behind badly. There are several things that can be done to improve FDI investments, and hopefully, things will get done before India hits another crisis.