REC 8.71% Tax-Free Bonds Issue – August 2013

This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

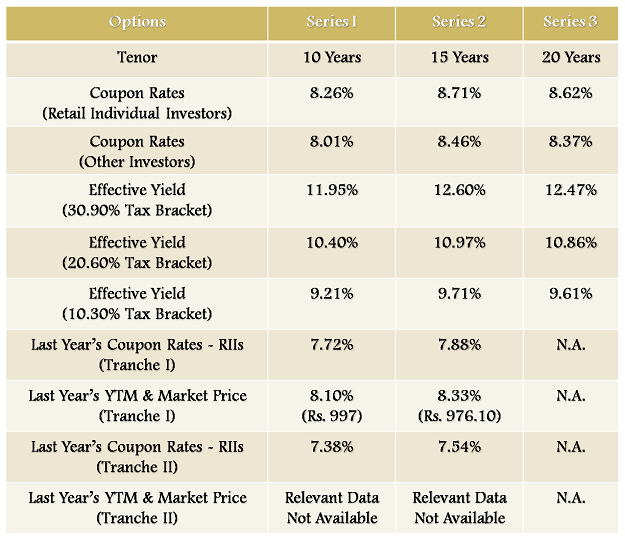

Rural Electrification Corporation (REC) will be launching the first public issue of tax-free bonds for the current financial year from 30th of this month. The company is offering quite attractive interest rates to the retail individual investors with 8.26% for 10 years, 8.71% for 15 years and 8.62% for 20 years. These rates are higher by approximately 0.70% to 1.50% as compared to the rates offered last year.

REC plans to raise Rs. 3,500 crore from this issue, including the green-shoe option of Rs. 2,500 crore. Though the official closing date of the issue is September 23rd, I think the issue should get closed before that due to oversubscription.

The government has allowed REC to issue Rs. 5,000 crore worth of tax-free bonds this financial year and the CBDT notification has mandated a minimum of 70% of this amount to be raised from public issues. As the issue size is Rs. 3,500 crore, if it gets fully subscribed this time itself, I think REC would raise rest of the money through private placements only and it will become the last issue of REC this financial year.

NRIs, QFIs & “Retail Individual Investor” – Non-Resident Indians (NRIs) on repatriable as well as non repatriable basis and Qualified Foreign Investors (QFIs) are also eligible to invest in this issue. The scope of a retail individual investor, investing upto and including Rs. 10 lakhs, has got broadened with the introduction of NRIs and QFIs (as individuals). It includes Hindu Undivided Families (HUFs) also through the Karta.

So, the investors have been classified into the following four categories:-

I – Qualified Institutional Bidders (QIBs) – 20% of the issue reserved

II – Non-Institutional Investors (NIIs) – 20% of the issue reserved

III – High Net Worth Individuals including HUFs, NRIs & QFIs – 20% of the issue reserved

IV – Retail Individual Investors including HUFs, NRIs & QFIs – 40% of the issue reserved

Interest Payment Date & Record Date – As this question gets asked by many of the investors throughout the year, it is better to mention it here itself as the date is known in advance this time. Interest will be paid on December 1st every year and the record date will be 15 days prior to that.

No Cumulative Option – There is no option of taking cumulative interest at the time of maturity with these bonds. Interest will be paid annually.

Safety, Ratings & Nature of Bonds – Being a ‘Navratna’ PSU, REC offers a high degree of safety as far as your investment is concerned and that gets reflected in the ratings assigned to this issue. The issue has been rated ‘AAA’ by four rating agencies, CRISIL, CARE, India Ratings and ICRA. It is the highest rating given by each of these companies. Also, these bonds are secured in nature against certain assets of the company.

Listing – REC bonds will get listed on the Bombay Stock Exchange (BSE) within 12 working days from the closing date of the issue. Investors have the option to apply these bonds as per their choice, either in physical form or in demat form.

TDS & Minimum Investment – As these are tax-free bonds, there is no question of TDS getting deducted, whether you take them in physical form or demat form. Minimum investment required is Rs. 5,000 only i.e. 5 bonds of Rs. 1,000 face value each.

Interest on Application Money & Refund – REC will pay interest to the successful allottees at the applicable coupon rate and at 5% per annum to the unsuccessful allottees.

Tax Treatment on Sale – Listed bonds held for more than 12 months qualify as long term capital assets and if sold thereafter, would attract a flat 10% capital gain tax, without indexation benefit. However, if the bonds are sold prior to holding them for more than 12 months, then short-term capital gain tax would be applicable, as per the tax slab of the investor.

Key Attractions of these Bonds: There were many issues with the tax-free bonds issued last year. There was a huge difference between the interest rate paid to the retail investors and the interest rate paid to other investors. Also, the subsequent buyer from the secondary markets was to get a lower rate of interest. Moreover, the cut from the G-Sec rate was also set on a higher side.

I think most of those issues have got rectified this year. Here are some of the key attractions of these bonds this year:

High Interest Rates – Due to the falling rupee and the unsuccessful measures taken by the Government and the RBI to control it from further fall, the yields of the benchmark government securities (G-Secs), against which the coupon rates of these tax-free bonds get fixed, have risen sharply in the last 45 days or so. 10-year benchmark yield touched a high of 9.47% before falling sharply to 8.25%. Thanks to this jump, the company has been able to offer such attractive coupon rates, especially for the 15 years period.

A word of caution. 10-year benchmark yield has again jumped back to close at 8.78% on August 27th. If the economic fundamentals of the country continue to deteriorate at the same speed as they have been doing, the yields could keep moving higher and the rupee could keep falling further against the dollar. But, I still hope India would come out of the current crisis soon and as the macroeconomic things get stabilised, these rates would look highly attractive again.

High Interest Rates, even if bought from the Secondary Markets – As per the CBDT notification – “The higher rate of interest, applicable to RIIs, shall not be available in case the bonds are transferred by RIIs to non retail investors”. So, the interest rates earned by the retail individual investors this year would remain higher even if they buy these bonds from the secondary markets subsequent to the offer period.

Your eligibility for a higher rate will depend on the number of bonds held in your name on the record date and the same will get tracked by your PAN number. Your holding should not be more than 1000 bonds per issue on the record date to get higher rate of interest.

Till last year, only the first allottees were eligible for a higher rate of interest and the subsequent buyers from the secondary markets were supposed to get a lower rate of interest. This factor will encourage the retail investors to participate in the secondary markets and thereby result in higher liquidity.

Low Differential – The differential between the rates offered to the retail individual investors and the other categories of investors has been cut down to 25 basis points (or 0.25%) only, as compared to last year’s 50 basis points (or 0.50%). This is the best step that has been taken this year. This factor would attract higher participation from the other categories of investors, both during the initial offer period as well as in the secondary markets.

I honestly think that these tax-free interest rates are very attractive. If I compare these rates with the interest rates on bank fixed deposits, the rates look quite similar, but with huge difference of tax applicability. I seriously hope India’s macroeconomic picture should start looking better in the days to come, only then we will be able to enjoy these high rates, otherwise inflation would again eat up all fruits of our hard work.

Link to Download the Application Forms of REC Tax-Free Bonds

If you need any further info or you want to invest in these bonds in Delhi/NCR, you can contact me at +919811797407

Hi Shiv,

How can a person buy bonds from retail market? Do the equity brokers allow that? I am not able to see them on my trading platform?

Paul.

Hi Paul… yes, these bonds get listed on the stock exchanges and equity brokers do facilitate trading in these bonds. I am not sure why you are not able to find them on your trading platform. Which platform you use?

Plz check this link, it has trading info of bonds listed on the NSE: http://www.nseindia.com/live_market/dynaContent/live_watch/equities_stock_watch.htm?cat=SEC

I was looking at the Series EQ. Saw the bonds now! Thank you for your help.

Thats great, thanks!

Hi Shiv, Thanks for the post. We know that there are many other companies too lined up this year which might come up with the issue. Do you think to wait for the rest of them or put all eggs into this one ? Please provide your thoughts.

Hi Karthik, I think it is always wise to diversify your portfolio, even if the returns are very attractive. As the coupon rates of these tax-free bonds are linked to the reference G-Sec rates, most of the companies which will issue these bonds even in September or October, the coupon rates would be similar i.e. plus/minus 0.25%. The chances of a sharp downturn in rates look very remote at present.

REC’s 15-year option looks attractive to me, dont know if others too will be able to offer similar rate. I hope they should be.

I have a question. Under HNI section of the instructions, it is mentioned like this

The following Investors applying for an amount aggregating to above `10 lakhs across all

Series of Bonds in this Tranche – I Issue:

What does this exactly mean?

My question is, how HNI is determined? I understand that one can invest upto Rs 10 lakhs and that falls under retail category. But if one person invests in more than one tax free bonds (from different companies) each Rs10 lakhs and still considered as retail investor? Or total of all tax free bonds should be Rs 10 lakhs to be considered as retail investor? Since PAN number is given when one apply for these bonds.

BTW, is this limit per year? Can you let me know?

Also, I read online about IIFCL tax free bonds 2013 (to be open in Aug 2013), but couldn’t find more information like when it will open, interest rates etc? Do you have information about that? Please let me know. Thanks,

BTW, your website gives lots of good information with no strings attached so far. Thank you for doing this.

Thanks Sundararajan for your kind words !!

Investors investing Rs. 10 lakhs per issue per company would be classified as Retail Investors. They can invest Rs. 10 lakhs in every issue of REC (and/or any other company) and still enjoy higher rate of interest. So, if REC & IIFCL come out with their 2 issues each this financial year, a retail investor can invest Rs. 10 lakhs * 2 * 2 = 40 lakhs.

As per my information, IIFCL would be launching its tax free bonds issue in September. Interest rates are linked to G-Sec yields, so will be announced by the company at some later date only.

Thank you for the detailed answer and explanation. That will really help.

Sundar.

You are welcome!

Shiv = Quite likely, the market price of bonds issued in 2011-12 and more so for those issued in 2012-13 will fall sharply. Are you tracking their market rate. Any comments

Hi… Yes, the prices have already fallen quite sharply, in fact, by approximately 6-10% in the last 1-2 months itself. NHAI N2 bonds, which were trading at around Rs. 1160 a month back, are now trading at around Rs. 1079. Bonds issued last year are all trading at below the face value of Rs. 1000 and the approximate yield range has jumped to 8.30-8.50%.

After reading the last comment, I have another question. Where can I see the current value of 2012 REC bonds or any other bonds from the pervious years. Also, can you let me know how much interest one can get from these bonds?

For example, one has invested in a bond for Rs10 lakhs with the interest rate of 8%. If the bond price goes below Rs10/unit and assume the total value of investment is say Rs 9 lakhs in next year. What is the interest amount that one will get, Rs80,000 or Rs 72000? Does one get Rs80k every year irrespective of the bond price or will it change based on current value of the bond? Can you let me know? Thanks,

Sundar.

Hi Sundararajan… Vignesh is right in stating that the interest amount will remain constant at Rs. 80,000 every year and it has nothing to do with the market price of these bonds. Even your principal investment value will remain constant at Rs. 10 lakhs at the time of maturity, if you hold these bonds for their full term. Whatever movement happens in the market price of these bonds will happen only in between the date of listing and the date of maturity.

Here is the link to check the bonds/NCDs of previous years which are listed on the NSE:

http://www.nseindia.com/live_market/dynaContent/live_watch/equities_stock_watch.htm?cat=SEC

Hi Sundar

Int remains constant throughout the tenure.

Coupon rate will be given always. But there will be change in capital invested that we need to declare as capital gain while cashing out.

And shiv one more query :

How much capital appreciation one could expect in this;at the end of 15 yrs ?

Pls shiv correct me if am wrong

Good article.

Question regarding this.

a) In case, the investor invest in these bonds (not for the full term) and need to trade it later (on BSE) for liquidity, is there a guarantee that there will be buyers for this on exchange, and if yes, will these always trade above the face value (given the market conditions, since I these are bonds I presume they will be?) – for capital protection.

b) Will the interest rate of these vary over the years as G-Sec int. rates vary?

Thanks Raghavendra!

a) Given the size of the issue and looking at the subscription figures, most likely there will be enough liquidity for the investors to cash out their investments. There is no guarantee that these bonds will always trade above their face value. Capital Protection does not mean that these bonds cannot go below their face value. But, as these are ‘AAA’ rated bonds, their is enough confidence that the company would pay back its interest and principal on time.

b) Interest rates will remain fixed throughout its tenure and will be paid on December 1st. YTM and market prices of these bonds will vary as per the market conditions.

Hi Vignesh,

Neither REC nor anybody else would give you a higher value for your bonds at the end of 15 years or at the time of maturity. You’ll get your principal investment back at that time.

Thank you for detailed info on REC isue. As seen the issue is due to close on 23 Sept. Is there any chance of getting it closed earlier. Could you please let me know what is the status of retail subscription?

Thanks and Regards

Hi Anand,

Here are the subscription figures of Day 1:

Category I – Rs. 205.30 crore as against Rs. 700 crore reserved

Category II – Rs. 573.22 crore as against Rs. 700 crore reserved

Category III – Rs. 559.01 crore as against Rs. 700 crore reserved

Category IV – Rs. 487.52 crore as against Rs. 1400 crore reserved

Going by the response, the issue should get closed well before September 23rd.

Hi Shiv,

REC tax free bonds offered this time contain the step down clause?

Hi Ashish… Step-Down feature has been removed from this year’s tax-free bonds. Category IV investors, with their bond holdings at 1000 bonds or less on the record date, will get higher rate of interest. Category I, II & III investors will get a lower rate of interest.

Dear Sir, Thanks for the wonderful detailed information about the tax free bonds…

Please advise me shall i sell REC Tax Free Bonds purchased last year in Dec’2012 as they carry only 7.38 % interest & should enter into the current REC bonds for 20 years at 8.62 % …?

( Even if the sell price for the same is a below par around 950 ….)

Hi Aryan… I think it is too late to do that now. The yields have already jumped higher and the prices have gone below their face value. Now, you should compare their YTMs with the coupon rates of current year’s bonds and then take a decision accordingly.

Apart from the minimum lock-in of 10 years, these bonds make an attractive investment option. How easy is it to trade on these bonds?? Do they have an active secondary market? Can these bonds be pledged and a loan taken against them, if required?

Hi Annapurna,

I would not call it a lock-in period of 10 years, rather it is the minimum tenor of these bonds. Also, there is good enough liquidity in the secondary market for these bonds from an investors point of view. These bonds get traded on a daily basis in the secondary markets.

Yes, these bonds can also be pledged and a loan can be taken against them.

Day 2 subscription figures:

Category I – Rs. 230.32 crore as against Rs. 700 crore reserved

Category II – Rs. 684.65 crore as against Rs. 700 crore reserved

Category III – Rs. 647.21 crore as against Rs. 700 crore reserved

Category IV – Rs. 856.42 crore as against Rs. 1400 crore reserved

Total Subscription – Rs. 2418.60 crore as against Rs. 3500 crore reserved

It appears to be over subscribed already as of today.

Retail upto 10 lakhs investment limit is at 2.14 times.

No point in applying niw, if not done already. Isn’t it ?

Category No.of Bonds/NCDs offered/ reserved No. of Bonds/NCDs odered for No. of times subscribed

1 category1 2000000 2303200 1.15

2 category2 2000000 6846455 3.42

3 category3 2000000 6472106 3.24

4 category4 4000000 8564213 2.14

Total 10000000 24185974 2.42

Hi Vej,

The data above is showing oversubscription only against the base issue size of Rs. 1000 crore and not overall issue size. Total issue size is Rs. 3,500 crore and it got subscribed to the tune of Rs. 2654.12 crore till today evening. If you are a retail investor, you’ll still get full allotment as the reserved amount for the retail investors is Rs. 1400 crore.

Why there is lack of interest by Category 1 investors (QIB)?

Hi Harshul… I think QIBs are foreseeing higher rate of interest in the issues to come and rightly so going by the yield movements.

Dear sir,

Thanks for provinding useful info.

when is the next tax free bond issue coming.

Pradeep

Hi Pradeep… HUDCO, PFC and IIFCL are expected to hit the markets soon, in the next 10-20 days I think.

HUDCO has filed its Draft Shelf Prospectus for FY 2013-14 on August 29th, so the issue will most likely hit the markets in the next 15-20 days.

HUDCO is AA rated company. can we expect interest rate to be 9 %p.a ?

thanks

HUDCO issue is rated ‘AA+’ as per its draft shelf prospectus. Though it is quite optimistic to expect interest rate to cross 9% mark and the probability is very low, but still it can happen.

PFC is going for a private placement of its tax-free bonds on Friday. Rates are 8.11% for 10 years, 8.48% for 15 years and 8.44% for 20 years, which means PFC’s rates for its public issue would be 8.36% for 10 years, 8.73% for 15 years and 8.69% for 20 years.

Source: http://in.reuters.com/article/2013/09/03/pfc-bonds-idINL4N0GZ1GD20130903

What does private placement mean ? Why do they for private placement also ? Basically what is the diff between them ?

Thanks Shiv !

Private placements are done privately between the issuer and certain investors. They are not open to public at large. The issuers are not required to file prospectus and there are lesser other formalities and hence private placements are cheaper mode of raising money.

As per the news article, it seems that the PFC issue will be limited to provate placement (“The issue is open only to sovereign wealth funds and pension and gratuity fund investors, as per the document.”).

Does it mean that it will not come out with public issue? The rates for public issue mentioned by you for PFC are not mentioned in article, neither the article talk anything about public issue.

Can you please throw some more light?

Hi cvshah77… PFC has been given permission to issue Rs. 5,000 crore worth of tax-free bonds and out of that, at least Rs. 3,500 crore will be through public issues. PFC has opted to go with private placements first and that is PFC’s discretion. PFC will definitely come with its public issue. The rates mentioned above would be applicable for public issues only.

Day 3 subscription update:

Category I – Rs. 230.37 crore as against Rs. 700 crore reserved

Category II – Rs. 709.14 crore as against Rs. 700 crore reserved

Category III – Rs. 709.71 crore as against Rs. 700 crore reserved

Category IV – Rs. 1004.91 crore as against Rs. 1400 crore reserved

Total Subscription – Rs. 2654.12 crore as against total issue size of Rs. 3500 crore

Which site provide details about the subscription for this issue ?

Hi Ajay,

The subscription details are available on NSE’s site as well as BSE’s site. Here are the links:

http://www.nseindia.com/products/content/equities/ipos/debt_ipo_current_rectf14.htm

http://www.bseindia.com/markets/publicIssues/DisplayIPO.aspx?id=706&type=DPI&idtype=1&status=L&IPONo=763&startdt=8/30/2013

Hi Shiv,

Thanks so much for day to day updates on the subscription.

One question though – The amounts being shown as reserved for various categories are assuming the greenshoe option right ? Can we assume that REC will use those allocations for sure ? Or they can allocate somewhere between 1000Cr to 3500 Cr of the total issue size ?

My application went in on the second day in Cateogry III. So just want to ensure I will be alloted 100% of my application size.

Also, just as a rough estimate, how much gain can be anticipated on these bonds in short term ? Is 10-15 % likely ?

Hi Sagar,

It is highly unlikely that REC will not accept oversubscription. If they had any such intention, then they would have closed this issue by now. You’ll get 100% allotment for sure.

Please define your short-term, do you mean listing gains or short-term for you means 6-9 months ??

Day 4 subscription figures:

Category I – Rs. 230.35 crore as against Rs. 700 crore reserved

Category II – Rs. 718.40 crore as against Rs. 700 crore reserved

Category III – Rs. 715.26 crore as against Rs. 700 crore reserved

Category IV – Rs. 1121.74 crore as against Rs. 1400 crore reserved

Total Subscription – Rs. 2785.75 crore as against total issue size of Rs. 3500 crore

Day 5 subscription figures:

Category I – Rs. 245.35 crore as against Rs. 700 crore reserved

Category II – Rs. 724.33 crore as against Rs. 700 crore reserved

Category III – Rs. 718.96 crore as against Rs. 700 crore reserved

Category IV – Rs. 1220.14 crore as against Rs. 1400 crore reserved

Total Subscription – Rs. 2908.78 crore as against total issue size of Rs. 3500 crore

Day 6 subscription figures:

Category I – Rs. 245.35 crore as against Rs. 700 crore reserved

Category II – Rs. 752.83 crore as against Rs. 700 crore reserved

Category III – Rs. 722.33 crore as against Rs. 700 crore reserved

Category IV – Rs. 1310.16 crore as against Rs. 1400 crore reserved

Total Subscription – Rs. 3030.68 crore as against total issue size of Rs. 3500 crore

I am bit confused about your figures above. As per the link that you gave, the allotted amount for Category 4 is 4000000 bonds. If per bond price is Rs1000, then the max is Rs 400 crore

only. The Rs. 1310.16 crore is correct. The column after this, says the subscription is already more than 3 times. If the max amount is Rs 400 crore then 3.x times of Rs400 crore is Rs1300 crore. Am I missing something? I would like to know where do you get the Rs 1400 crore reserved.

Hi Sundar,

Rs. 400 crore is as per the base issue size of Rs. 1000 crore. But, Rs. 1400 crore is as per the total issue size of Rs. 3500 crore. 40% is reserved for the Category IV and 40% of Rs. 3500 crore is Rs. 1400 crore.

Hi,

I am a person who falls in 30% tax bracket. Why would this tax free bonds will be beneficial for tax purposes for me if NCD of AAA rated private companies with yield of 10% can be availed by FMD/debt funds. I can certainly take advantage of indexation in debt funds to bring down my tax liability.

Why should a person in 30% tax bracket should invest in such bonds. Do you think that CPI is going to decrease drastically in next 5 years? Or are there some rules in DTC which would impact taxation of debt mutual funds?

I always invest in growth option of debt mutual funds and never in divident option. So dividend distribution tax is not much of a concern for me.

Hi Sanjay,

I never say debt funds/FMPs are a bad option. They are also good investment options and one should invest in them to diversify their debt portfolio. They also invest in these tax-free bonds and NCDs etc. But, by investing directly in tax-free bonds, you can save on the expenses that debt funds/FMPs charge and earn higher rate of interest yourself. There are many NCDs which are yielding 12-15% and are about to mature in 1-3 years, this way you can earn more than FMPs. You are just required to research somewhat.

Default risk of private firms is very big concern for me. So I do not invest in NCDs of private firms directly. I buy FMP in the hope that Fund Manager will do due diligance of default risk and FMP also has lower expenses. For example, I invested in “HDFC FMP-XXVII-1875D” in the hope to lock in to higher yield at the same time to decrease the risk as it invests in AAA rated NCD.

About the debt funds : they are also supposed to make investment in high yield and low risk debt of private firms. I feel okay to pay 1 to 1.5 % expense ratio for that due diligence.

Another reason I prefer to invest via mutual funds is my portfolio size remains manageable.

It would be great if you can write article on how to evaluate dynamic bond funds on that perspective.

Personally, I invest in Mutual Funds when I feel it is beyond my abilities & expertise to do it on my own. What equity funds do or FMPs do, I think I can do majority of it on my own, so I rarely invest in equity mutual funds or FMPs. At the same time, they have there own positives also, like good research team for equity funds and favorable taxation rules for FMPs. I invest in Gilt funds bcoz I think I cannot invest in G-Secs on my own.

In your case, I dont think HDFC FMP 1875 days is going to give you more than 9% pre-tax returns. At the same time, you can invest in corporate NCDs like SBI bonds, IFCI bonds, STFC bonds etc. & earn around 11-12% pre-tax returns yourself. But, if the differential is lower at around 1% or so, then you are right to take MF’s help to manage your money. Paying 1-2%, for something you cannot do on your own, is perfectly fine.

With tax-free bonds, my point is that I’m getting 8.71% tax-free for the next 15 years. No MF scheme gives such tax-free returns for 15 years. At present, interest rates are higher. Say, anytime in the next 5-7 years, I’m able to get 10-15% returns due to their capital appreciation, my total returns would be more than 10.50% annually. I will feel happy with those returns and I am not required to pay 1-2% extra to MFs for doing it on my behalf.

I have been thinking of writing a post on Dynamic Bond Funds for quite a while now, but have failed to do so. But, will do that soon for sure.

Thanks a lot for such a detailed and prompt reply. I was really positively surprised.

I just read in some websites that AAA NCD yield has gone above 10% and based on that I invested in that FMP. May be I was very naive in doing that.

I came to know that SBI dynamic bond fund has 1.7% expense ratio and it has hevaily invested in long term gilt. Now I am wondering whether to invest in this fund or some other dynamic bond fund.

Thanks for your kind words Sanjay !!

That is the biggest problem with dynamic bond funds. Suppose, I have a view that the interest rates are going to rise and I should invest in a dynamic bond fund which has a least exposure to gilts or high duration securities.

I search about it and invest in one such fund, but, a few days later, the fund manager changes his view to invest in securities with a high duration. If the rates actually rise, I’ll find myself trapped in it and my portfolio will suffer losses. So, it is better to invest in a fund which invests as per your own objective.

What are the latest subscription figures?

Hi Anuj… subscription figures till September 6 (Day 6) are stated above.

Thanks Shiv for prompt reply.

Since exchanges were closed fron 7-9, how can we get the latest figures?

Actually I want to apply but not sure if there is any scope of allotment.

These are the latest figures Anuj. The bidding will start today again. I think the retail portion will get oversubscribed today. If you apply early in the morning today before 12 noon, there is quite a good chance that you’ll get 100% allotment. If this issue sees undersubscription in the QIB category, then the retail investors will get allotment beyond Rs. 1400 crore.

Thanks. I have applied in the morning.

That is great!

Day 7 (or September 10, 2013) subscription figures:

Category I – Rs. 245.35 crore as against Rs. 700 crore reserved

Category II – Rs. 760.54 crore as against Rs. 700 crore reserved

Category III – Rs. 734.63 crore as against Rs. 700 crore reserved

Category IV – Rs. 1432.09 crore as against Rs. 1400 crore reserved

Total Subscription – Rs. 3172.60 crore as against total issue size of Rs. 3500 crore

So, now that the retail investor category has got oversubscribed, I think the retail investors should not further invest in this issue. If, at any point of time, the Category I investors pour a further Rs. 455 crore in this issue, then the retail investors applying now onwards will not get any allotment.

Hi Shiv,

Coupon rates on any other Tax Free bonds issues finalized which is going to open in near future?

Thanks,

Ajay

Hi Ajay,

There is no info about the coupon rates of any of the forthcoming issues, but I think HUDCO rates should be higher than the REC rates.

I understand that Category IV is already over subscribed. I have planned to submit application tomorrow. Is there any chance to get alloted since the total subscription is still less than the max? Or is it strictly by category? Please let me know. Thanks,

Firstly, it is by each category and in case there is under subscription in any of the categories, then it will get allotted to the Category IV investors first. So, now onwards, Category IV allotment will solely depend on how Category I investors invest in this issue. I think it is better to avoid this issue now and wait for the next issue.

Day 8 (or September 11, 2013) subscription figures:

Category I – Rs. 245.35 crore as against Rs. 700 crore reserved

Category II – Rs. 847.44 crore as against Rs. 700 crore reserved

Category III – Rs. 738.59 crore as against Rs. 700 crore reserved

Category IV – Rs. 1473.59 crore as against Rs. 1400 crore reserved

Total Subscription – Rs. 3304.97 crore as against total issue size of Rs. 3500 crore

Still no change in the subscription numbers of Category I.

Day 9 (or September 12, 2013) subscription figures:

Category I – Rs. 245.35 crore as against Rs. 700 crore reserved

Category II – Rs. 847.84 crore as against Rs. 700 crore reserved

Category III – Rs. 750.57 crore as against Rs. 700 crore reserved

Category IV – Rs. 1505.73 crore as against Rs. 1400 crore reserved

Total Subscription – Rs. 3349.49 crore as against total issue size of Rs. 3500 crore

REC has decided to close the issue on Monday, September 16th, a week before the official closing date.

HUDCO tax-free bonds issue is expected to open on September 17th. Coupon rates are expected to be higher than the REC issue at 8.65% for 10 years, 8.76% for 15 years and 8.74% for 20 years.

Source: http://www.business-standard.com/article/companies/hudco-s-rs-4-800-cr-tax-free-bond-issue-to-open-sep-17-113091300132_1.html

Day 10 (or September 13, 2013) subscription figures:

Category I – Rs. 245.35 crore as against Rs. 700 crore reserved

Category II – Rs. 873.02 crore as against Rs. 700 crore reserved

Category III – Rs. 755.22 crore as against Rs. 700 crore reserved

Category IV – Rs. 1531.80 crore as against Rs. 1400 crore reserved

Total Subscription – Rs. 3405.38 crore as against total issue size of Rs. 3500 crore

September 16th, Monday, the issue is getting closed. So, if Category I investors do not invest further in this issue, the Category IV investors will get 100% allotment.

Next issue is from HUDCO

http://www.business-standard.com/article/companies/hudco-s-rs-4-800-cr-tax-free-bond-issue-to-open-sep-17-113091300132_1.html

small size

Small Size ??

Sir,

The link says “The core issue size will be Rs 750 crore”. REC Was 1,500 cr and with option to scale up to 3.5 k cr. please let me know if i am wrong.

REC’s base issue size is Rs. 1,000 crore as against HUDCO’s Rs. 750 crore. But, overall HUDCO issue size is bigger.

Final Day (or September 16, 2013) subscription figures:

Category I – Rs. 245.36 crore as against Rs. 700 crore reserved

Category II – Rs. 923.12 crore as against Rs. 700 crore reserved

Category III – Rs. 759.92 crore as against Rs. 700 crore reserved

Category IV – Rs. 1585.62 crore as against Rs. 1400 crore reserved

Total Subscription – Rs. 3514.02 crore as against total issue size of Rs. 3500 crore

100% allotment to all the categories of investors including Category IV retail individual investors (RIIs), except Category II.

Dear Sir,

When are these REC bonds (Offer closed on 1 September 2013) expected to be allocated?

Thanking you. Best regards, RAKESH

Hi Rakesh,

Correcting you first, this issue closed on September 16, 2013 and not September 1. I think yours is a typing error. Allotment of REC bonds is expected to happen before October 2nd and listing is expected to happen on October 3.

Fed surprises everyone by the decision to delay tapering !

G-Sec yields already around 8.18 as of now. So I think this bond should see some nice listing gains.

Are 10 to 15% gains feasible here on listing ?

For a little longer horizon of about 6 months, 15% should be easily feasible right ? Taking into account first tax free payout (8.4%) + Apprx. 10% capital gain – short term taxes ?

Also falling g-sec rate would indicate that one should not miss on HUDCO opportunity right ?

Hi Sagar,

1. 10-15% gains not possible on listing, unless 10-year G-Sec yields fall below 7.50%.

2. Not easily feasible to earn 15% in 6 months, but not impossible. For this to happen, Indian rupee is required to reach 55 against the dollar, 10-year G-Sec yields to fall below 7.50%. REC will pay interest only for 2-3 months on December 1st.

3. Yes, it seems today that HUDCO opportunity should not be missed, but one should not remain in a hurry as it will take its own time to get subscribed.

Thanks Shiv.

Yes, I made a mistake about #2, I was assuming it will pay out complete interest on Dec-1.

I got a credit from REC 2013 bond saying refund credited to my bank account. Does that mean the bond isn’t alloted ? I did apply before closing date on category IV. Eventhough it was over subscribed at that time, I assumed based on your comment, it might have been allotted. (since category I was less subscribed). Or is it related to something else? I will be disappointed if I didn’t get the allotment. Please let me know. Thanks,

That is strange. Amount has been debited from account for the bonds. how did you apply – physical forms /online trading site ?

sorry typo in my above post

I meant “Amount has been debited from my account for the bonds.”

Hi Pradeep,

I think you applied through ASBA for the REC bonds and now you will get bonds allotted equivalent to the money debited from your account.

Sir,

The bonds have been credited to my demat account. Congrats to all allotees. 🙂

Great!

Hi Sundar,

It must be the interest on your application money. Please check the exact amount of credit. I think the retail investors should get 100% allotment, even if applied for it on the last day.

REC tax-free bonds to get listed on the stock exchanges on September 30th i.e. Monday.

Here are the BSE codes for the same:

8.26% 10-year bonds – BSE Code – 961778

8.71% 15-year bonds – BSE Code – 961779

8.62% 20-year bonds – BSE Code – 961780

Thanks for the update !

Quick question, I don’t yet see the bonds alloted in my ICICI direct account. Can I expect that to happen by today or Mon ?

Also, I believe REC will payout the interest on application money to successful allotees as well. Would this be paid out in next few days ?

Hi Sagar,

Bond allotment process for the bonds allotted in the demat form gets completed before the listing happens on the stock exchanges. So, you can expect the bonds to get allotted either by today evening or maximum by tomorrow morning.

I am not sure, but I think they have already started paying the interest money. They have paid interest till September 23rd only, as the Date of Allotment is September 24, 2013. You should check your bank account.

Hi Shiv,

Aren’t these REC bonds going to be listed on NSE too? I ask this since, NSE’s website continues to show REC-N1 to N4 only.

Request you to confirm.

Thanks,

Mayank

Hi Mayank,

I think I’ve committed a mistake here. These bonds are not getting listed on the NSE. I don’t know from where I got this info about its NSE listing, I think it must be some product note. I apologize for the error, I’ll rectify it right now.

Hi Shiv,

Thanks for the clarification. I’m sure it’s quite confusing with the recent deluge of debentures & bonds. Appreciate your efforts in writing timely post on the various debentures being offered.

Thanks,

Mayank

Thanks Mayank!

Actually, I must have seen or heard about it somewhere while writing that post, otherwise it has never happened like this.

Also, issues which do not get listed on the NSE, do not show bidding details on the NSE website. But, REC issue bidding details were also getting updated there, so that also created some confusion.

Link to check the allotment status of REC Tax-Free Bonds:

http://mis.karvycomputershare.com/ipo/

REC tax-free bonds got listed today on the stock exchanges and trading at a marginal premium to its face value of Rs. 1,000. It touched a high of Rs. 1,009 and a low of Rs. 1,000.

http://www.bseindia.com/stock-share-price/rural-electrification-corporation-limited/871rec28/961779/

IIFCL tax-free bonds issue opens October 3rd. Tentative coupon rates are 8.26% p.a. for 10 years, 8.63% p.a. for 15 years and 8.75% p.a. for 20 years. The issue is rated ‘AAA’ as compared to ‘AA+’ for the HUDCO issue & ‘AAA’ for the REC issue.

Hi Shiv,

What is the date of year when we will be getting annual interest on REC Bonds?

Hi Akhilesh,

It is December 1st every year.

PFC Tax-Free Bonds Issue opens on October 14th. Coupon Rates are as under:

8.92% for 20 Years

8.79% for 15 Years

8.43% for 10 Years

NHPC tax-free bond issue opens on October 18th. Coupon Rates are as under:

8.92% for 20 Years

8.79% for 15 Years

8.43% for 10 Years

The rates offered are absolutely same as the PFC rates. It is also rated ‘AAA’. The issue closes on the same date i.e. November 11th.

Just came to know that REC bonds are redeemable. Can you please clarify about when the PSU can redeem bonds and is there any “call protection” ?

Also, can you list out out of tax free bond issuances so far, which are redeemable and which are not?

Is there any reinvestment risk with such tax free bonds?

Hi Sanjay,

None of these bonds are redeemable before maturity and there is no “Call Option” with any of these companies or “Put Option” with their investors.

Reinvestment risk is there with the interest you get annually and it is higher for 10 year bonds as compared to 15 year bonds or 20 year bonds.

I had invested in REC series 2 ( 15 yrs ) – for coupon of 8.46. While checking the rates today, I am surprised to see the CPM as 1320 !!!! Is this some sort of a mistake ? 32% returns in debt 🙂

http://www.bseindia.com/NewStockReach/StockReach_Debt.aspx?scripcode=961776

Hi Sagar,

Only a single trade of 50 bonds got executed yesterday at Rs. 1,320 and this price is somewhat misleading. Its fair price should be between Rs. 1,135 to Rs. 1,155 in normal trading.

Though 32% return is unusual with debt instruments, there are tax-free bonds which have given 20%+ returns in just 8-9 months time, like NTPC, NHB etc.

http://www.nseindia.com/live_market/dynaContent/live_watch/get_quote/GetQuote.jsp?symbol=NTPC&series=N6

http://www.nseindia.com/live_market/dynaContent/live_watch/get_quote/GetQuote.jsp?symbol=NHBTF2014&series=N6

Why does a Bond with face value Rs. 1000/- trade at Rs. 1135-1154? If one buys for Rs. 1135-1154, the effective interest will be very low compared to

original interest rate i.e. 8.46% or 8.71% for 15 year Bonds?

Yes, that is correct. What you are calling as effective interest is termed as yield to maturity (YTM) and it is currently moving between 7.40% to 7.65%. So, if you buy these bonds at the current market price and hold them till their maturity, you will earn 7.40% to 7.65% annualized return.

These bonds are trading at a higher price due to a high demand in the market. Investors are willing to pay such high prices in order to earn tax-free interest.

I think the most TFBs, issued in the last financial year are cum-interest for FY 2014-15 and so the actual YTM may be even higher, if the receivable interest for the current financial year is adjusted in the purchase price. Still the actual YTM depends upon the actual interest payment date in the current financial year for each such TFBs.

YTM considers the accrued interest as well, so it should not be higher than the calculated ones, given the listed YTMs are calculated in the correct manner.

Its going to be one full year in next couple of days since this series of REC bonds were allocated. Post 1 yr the gains will be taxed at flat 10%. May be there could be some selling and profit booking. There may be a chance to buy these at a lower price. Given the rally in GSEC yields within past couple of weeks, it would not be a bad idea to add some more.

Quite possible.

Any news about Tax Free Bonds being offered in FY 2014-15?

No tax free bonds will be issued this financial year and probably going forward also.

Hi Shiv

Great post. I am only a beginner who is trying to figure out investment options in Bonds (REC’s, etc). Just wanted to know the basics. If I am buying 100 bonds (5000 x 100 = Rs.5 lacs) Then the coupon rate that we call is that like interest rate (6% annually?)

If so, then after that is there a final principal amount which we return or does principal amount too comes up with some interested accumulated.

Hope my question was clear (without confusing you)

Looking forward to your answer. Thanks 🙂

Thanks Manpreet,

With REC 8.71% bond, the investor will get 8.71% as the interest. 8.71% is also called its coupon. So, the annual interest payment will be Rs. 43,550. On maturity, you’ll get Rs. 5 lakh back without any premium or discount.

Today I see a drop of almost 6-7% , prices falling by almost 80.

Any specific reason ? Just because of approaching interest payment date ?

These bonds have got “ex-interest” today, that is the reason behind their price fall.

Any new tax free bonds coming now?

Or in pipeline for 2014-2015 ?

Also advise if any good buy option from secondary market

for a lomger term of 20 years tax free bonds at present .

Thanks.

The union budget for FY-2014-15 as not provided for tax free bonds in the current year. Regarding choice of ‘good option’ from secondary market, answer lies with the price on a given day, your time horizon etc. Please consider the interest payment date. Otherwise, generally speaking there is not much difference between various bonds – all issuers are PSUs. You can consider credit rating of various issuers if it is important for you.

Dear Shiv,

I had purchased 500 REC Tax free Bond, Series 2bonds, category III, (INE020B07GH7), as retail investor, interest 8.32 when it was offered in March 2012.

I subsequently bought 15 bonds from open market in April 2012, interest 8.12. Though these two transactions were at separate times I am being treated as HNI and received less interest and following message from REC. I am loosing Rs.1000/per year. Shall I sell the 15 bonds purcshased form the open market. Reqeust, advice.

As per the terms of prospectus if the investor is holding more than 500 bonds than interest as applicable for Retail Bonds will not be paid to him, those investors will fall under the category of High Networth Individuals.

Accordingly as you are holding total 515 bonds interest has been paid to you as applicable for HNIs i.e @ 8.12%.

Best regards

Dear Anand,

Yes, you need to sell these additional 15 bonds to qualify for a higher rate of interest.

Thank you very much Dear Shiv

Regards

You are welcome Anand !!

Hi,

The interest credited seems to be erroneous. I was expecting 8.71% interest for the 1000 bonds (Rs. 87100/-) However there is credit of Rs. 612/- only.

Anyone else facing similar issue?

I have written to [email protected] and

[email protected]

Hopefully should get a reply soon.

– Hemant

Hi Hemant,

I hope you get a reply soon.

Yes. I got immediate response and the amount was deposited too.

That’s great !!

Today is the interest payment date. I haven’t yet received though … Hopefully by tomorrow I guess ..

Hi Sagar,

I hope you’ve got the interest credited.