SREI Infra 11.75% NCDs Issue – August 2013

This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

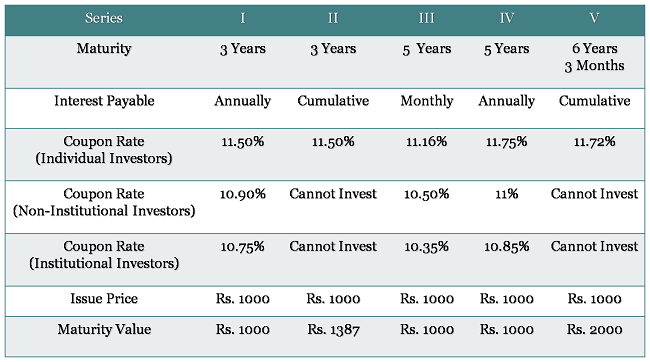

SREI Infrastructure Finance Limited is going to launch its second public issue of non-convertible debentures (NCDs) of the current financial year 2013-14 from Monday, August 24th. It is going to offer a maximum of 11.75% per annum to the individual investors for 5 years tenor and a minimum of 10.35% per annum to the institutional investors for 3 years tenor.

SREI Infra plans to raise Rs. 200 crore from this issue, including the green-shoe option of Rs. 100 crore. The issue is scheduled to close on September 17th or earlier, depending on the response for the issue. NCDs will be allotted on a first-come-first-serve basis.

Categories of Investors & Basis of Allotment – The investors would be classified in the following three categories and each category will have certain percentage fixed for the allotment:

Category I – Institutional Investors – 20% of the overall issue size

Category II – Non-Institutional Investors (NIIs) including corporates – 20% of the issue

Category III – Individual Investors including Hindu Undivided Families (HUFs) – Rest 60% of the issue

NRIs and foreign nationals among others are not eligible to invest in this issue.

Tenors and Rate of Interest

SREI came up with its first issue in April this year and as compared to that issue, the second issue looks attractive from the retail investors’ point of view. As compared to 10.75% for 3 years and 11% for 5 years in its last issue, this time the company is offering 11.50% and 11.75% respectively.

The bonds will be issued for a tenor of 3 years, 5 years and 75 months (6 years and 3 months) with monthly interest, annual interest and cumulative interest options. The monthly interest option is available only with 5 years period and will carry coupon rate of 11.16%, which effectively is 11.50% per annum.

“Double Your Money” Option – Series V NCDs offer to double your money in a period of 6 years and 3 months and effectively yield 11.72% per annum. Though it is quite attractive to hear doubling of money, I think it is better to go for shorter tenors in case of company NCDs.

Ratings & Nature of NCDs – CARE has assigned ‘AA-’ rating and Brickwork Ratings has given ‘AA’ rating to this issue. Moreover, these NCDs are secured in nature and the claims of its investors will be superior to the claims of any unsecured creditors of the company.

Listing, Demat & TDS – These NCDs are proposed to be listed on the Bombay Stock Exchange (BSE) only. Investors have the option to apply these NCDs in physical form as well as demat form, except for Series III NCDs, which carry monthly interest and will be allotted compulsorily in the demat form.

The interest earned will be taxable as per the tax slab of the investor and TDS will be applicable if the interest amount exceeds Rs. 5,000. But, NCDs taken in the demat form will not attract any TDS on the interest income.

Minimum Investment – There is a minimum investment requirement of Rs. 10,000 i.e. at least 10 bonds of face value Rs. 1,000.

Profile & Financials of SREI Infrastructure Finance Limited – SREI was initially registered with the RBI as a deposit taking non-banking financial company (NBFC). Effective March 31, 2011, SREI got converted into non-deposit taking NBFC and the RBI classified it as an Infrastructure Finance Company (IFC). Later, SREI got notified as a Public Financial Institution (PFI) by the Ministry of Corporate Affairs.

The company provides financial services to its customers engaged in infrastructure development and construction, with particular focus on power, road, telecom, port, oil and gas and special economic zone (SEZ) sectors in India with a medium to long term perspective.

SREI has a national presence with a network of 198 offices all over India and over Rs. 33,330 crore of consolidated assets under management (AUM). SREI’s loan disbursements have grown at a CAGR of approximately 44% in the last four years, with consolidated disbursements of Rs. 15,667 crore for the period ended March 31, 2013 and Rs. 18,600 crore for the year ended March 31, 2012.

Total income on a standalone basis for the period ended March 31, 2013 and March 31, 2012 stood at Rs. 1,666 crore and Rs. 1,181 crore respectively. Net profit for the same periods was registered at Rs. 94.96 crore and Rs. 57.96 crore respectively.

The grey area, with which the whole of the infrastructure finance industry is suffering, has also affected SREI Infra badly. Gross NPAs of the company as on March 31, 2013 stood at 2.77% as against 1.58% as on March 31, 2012, while Net NPAs were at 2.30% as against 1.18%.

SREI Infra NCDs are definitely better than some of the riskier company FDs like Unitech, Gitanjali Gems, Jaiprakash Associates or other lesser known companies. Investors, who are willing to take low to moderate risk and looking for higher returns than bank FDs or comparable company FDs, can think of investing in these NCDs. But, I think it should not be more than 5 to 10% of your total debt portfolio. Investors in the 30% tax bracket should definitely wait for the tax-free bonds or go for the tax-efficient debt funds or FMPs, as these investments should result in higher effective yields for them.

Hi Shiv, Do you know the taxability of income for the doubling option in 6yrs 3months? Will tax be payable at maturity or annually?

Hi Vikas,

Ideally the tax on the interest income of these NCDs should be paid on maturity only, if the investor keeps it till its maturity. If the investor decides to sell the bonds before maturity, then there is no question of paying tax on the interest income, in that case only capital gain tax is payable.

Thanks Shiv.

I read that for KVPs, tax is paid annually on the interest accrued. The NCDs with the doubling option are similar to KVPs, right? So, shouldn’t tax be payable annually as well?

Hi Vikas,

KVPs are history now, but the tax is payable on an annual basis on both KVPs as well as NSCs. It is justified also bcoz KVPs and NSCs are not tradable and there is no scope of any capital gain and hence, there is no capital gain tax. Whereas NCDs are tradable and there is scope of booking capital appreciation.