Shriram City Union Finance NCDs Issue – November 2013

This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

As Muthoot Finance NCD issue gets preclosed on Monday, Shriram City Union Finance (SCUF) is also launching its issue of non-convertible debentures (NCDs) from the same day, November 25th. The company plans to raise Rs. 200 crore from the issue, including Rs. 100 crore of green shoe option.

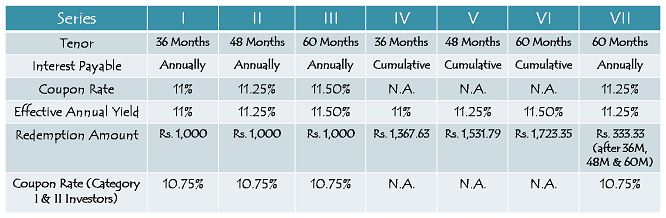

SCUF has decided to offer an annual coupon rate of 11% for a period of 36 months, 11.25% for 48 months and 11.50% for 60 months to the retail investors and high networth individuals (HNIs).

Institutional investors, non-institutional investors, corporates etc. will be paid a lower rate of interest, which has been fixed at 10.75% per annum across all seven options, for all the tenures – 36 months, 48 months or 60 months.

It will be a month-long issue which is scheduled to close on December 24th i.e. Tuesday. As the issue size is small, the company has the option to preclose it as and when it gets oversubscribed. If it gets a poor response, the company may extend it also.

Retail investors category investing up to Rs. 5 lakh would get 40% pie of the issue. Individual investors investing more than Rs. 5 lakh in a single name would be categorised as HNIs and 40% of the issue size has been reserved for this category of investors also.

Categories of Investors & Allocation Ratio – The investors have been classified in the following four categories and each category will have a certain percentage fixed in the allotment:

Category I – Institutional Investors – 10% of the issue is reserved

Category II – Non-Institutional Investors & Corporates – 10% of the issue is reserved

Category III – High Networth Individuals including HUFs – 40% of the issue is reserved

Category IV – Resident Indian Individuals including HUFs – 40% of the issue is reserved

NCDs will be allotted on a first come first served basis.

NRI Not Allowed – Non-Resident Indians (NRIs), foreign nationals and qualified foreign investors (QFIs) among others are not eligible to invest in this issue.

Ratings & Nature of NCDs – The issue has been rated as ‘AA’ by CARE and all these NCDs are ‘Secured’ in nature. It indicates reasonable safety for your investment amount.

Listing, Demat & TDS – SCUF has proposed to list its NCDs on the Bombay Stock Exchange (BSE) as well as on the National Stock Exchange (NSE). Investors have the option to apply these NCDs in physical form as well as demat form. However, trading of these NCDs will happen only in the demat form.

Interest earned on these NCDs is taxable as per the tax slab of the investor and TDS will be applicable if the interest amount exceeds Rs. 5,000 in a financial year. NCDs taken in the demat form will not attract any TDS on the interest income.

Minimum Investment – Minimum investment in this issue has been fixed as Rs. 10,000 i.e. 10 bonds of face value Rs. 1,000.

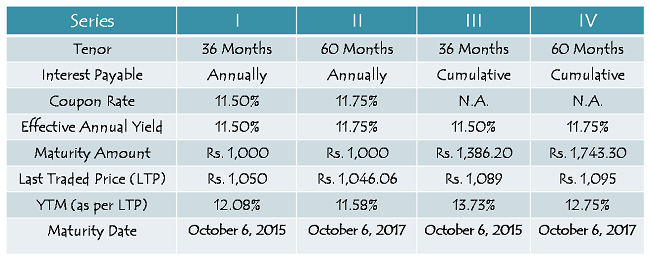

Performance of Last Year’s SCUF NCDs

As you can check from the table above, SCUF NCDs issued last year, with maturity periods of 36 months and 60 months, are trading at yields of 11.58% to 13.73%, much above the coupon rates offered in the current issue.

Also, with a private company being the issuer, it is always advisable to go for the least possible tenure offering attractive coupon/yield. As compared to the current issue, last year’s NCDs carry lower risk as the maturity period has become shortened.

Interest rates have also risen since its last issue. So, I would say if anybody wants to make an investment in SCUF NCDs, it is better to go for already listed NCDs rather than subscribing for them in the current issue.

Looking at the subscription figures of recent NCD issues of IIFL, Shriram Transport Finance, Muthoot Finance etc., it seems to me that the investors are not performing any due diligence before subscribing to these NCDs, rather these NCDs are getting sold to them by their brokers. Personally, I would avoid this issue for my own investments.

Application Form of Shriram City Union Finance NCDs

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in SCUF NCDs, you can contact me at +919811797407

Good post Shiv.

thanks

–kishor

Thanks Kishor!

Thanks Shiv. Always look forward to your posts.

You are welcome Ikjot !!

Shiv,

Thanks for the article, I do read and take directions from your articles. As I requested before, did you guys write any article regarding the companies that are defaulting on corporate FDs? for example Bilcare, Avon, Ind-Swift, Unitech (late payment), Birla Power, Sejal Glass and many more? I think it is alarming that so many companies are defaulting and robbing retail investors’ money.

-Amit

Hi Amit,

I had posted an article on Company FDs in August last year – https://www.onemint.com/2012/08/21/best-company-fixed-deposits-returns-wise-safety-wise-be-wise/

It was not precisely on companies defaulting on these deposits, but I mentioned certain factors that investors should consider before investing their money in company fixed deposits. Honestly speaking, I don’t find a single reason for me to invest my money in corporate fixed deposits. As always, the government hasn’t done enough to protect investors from getting cheated by these companies.

Hey Shiv,

You mention that NCDs taken in demat form will have no TDS.

What does that exactly mean?

Investor gets the full amount and then has to pay tax later through his IT return.

Is that so?

Ashish

Hi Ashish,

Yes, that is what it exactly means.

Thanks for your kind confirmation Shiv.

You are welcome!

Hi Shiv,

What are your views on the forthcoming India Infoline Housing Finance NCD?

http://www.indiainfoline.com/Markets/News/India-Infoline-Housing-Finance-to-raise-Rs.-250cr-via-bond-issue/5827290546

Hi Manish,

I’ll cover IIHFL NCD issue in a day or two.

Dear Shiv,

I am wanting to invest in this issue of SCUF NCDs for 60 months period. Please tell me which option is better. To go for the annual option (series III) or the cumulative one (series VI) as both are having the same coupon rate of 11.50%?

(2) Secondly, in the series VII annual interest payment for 60 months, they are redeeming 33.33% in three instalments. So this makes it that the prinicipal amount itself is returned in three instalments, then what about the interest earning (over and above the principal)?

(3) Finally please explain how to choose one option among the three options of 60 months tenure in such or similar issues?

Thanking You!

Hi Saurabh,

1. I don’t which option is best suited to you, I would personally go for the annual interest option.

2. Interest will be paid on the remaining principal amount after partial redemption.

3. It is difficult for me to explain any such thing on this forum.

Alright! Shiv,

Thank you for the response! 🙂

You are welcome Saurabh!

Shiv, is there any taxable bond, where NRIs are allowed to invest. I am asking taxable, because their yields are high, and if NRI is not in tax bracket in India, it s good net 11-12% yield for him.

I read HUDCO tax free bond, had allowed NRI investment, but yield is low

At present, no taxable NCD issue is open for subscription which allows NRIs to invest.

Dear Shiv

One suggestion – What is better Secured NCD with higher interest or Tax free bond with lower interest, for comparison you may refer to Sriram secured NCD VS HUDCO tax free bond

Dear Kunal,

There are various things you need to analyse before you conclude which one is better. For an investor in the 30% or 20% tax bracket, HUDCO tax-free bonds stand much superior as compared to SCUF NCDs.

As a finance student atm, I am a little confused about the prices of last year’s bond issue. If the YTM is greater than than the coupon rate than the bond should be trading at a discount and should have a price that is less than face value. Given the prices in the second table, the bonds should be trading at a premium and have YTM<Coupon rate as their price is above par.

Is this logic sound? Could someone please tell me where it might be wrong?

Hi AJ,

The prices are higher here because the interest is accrued in the prices.

Hi,

I have applied for NCDs of Shriram City Union Finance. Have the allocations been made? I found no evidence that I have allocated any NCDs. Could you please enlighten me as to the status, particularly in terms of whether allocations have been made? Also, other than my own Demat account is there any other Web site where I can check whether I have been allotted any NCDs of this company?

Hi,

SCUF NCD issue got closed on December 24th and the allotment will be made in the next 12 working days. Shriram Insight is the Registrar to this issue. You can check the allotment status on this site after 10 days or so – http://www.shriraminsight.com/

Good Information Has Shared this blog. Thank for sharing

very good kindly intimate me also

we are very much thankful to you for detail now kindly provide me brief for ncds of shriram city union finance i.e. date of issue , interest offered, maturity date and maturity value as well as for edelweiss finance and iifl also please have me your contect no.

also let me know the code of nse for tradimg and bse code no for the same ncds