HUDCO 9.01% Tax-Free Bonds Tranche II – December 2013 Issue

This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

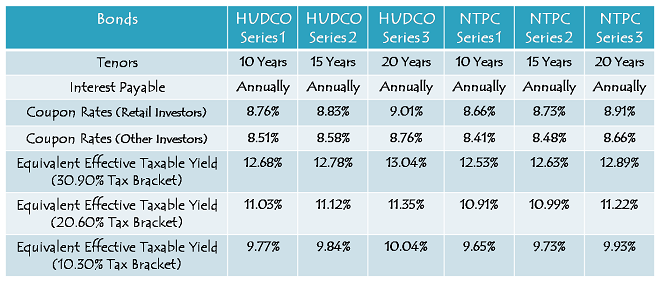

After a month long break, tax free bond issues are back and the 10-year options are looking much healthier now carrying annual coupon rates of 8.76% and 8.66% for ‘AA+’ rated HUDCO issue and ‘AAA’ rated NTPC issue respectively, as against its previous highs of 8.43% for ‘AAA’ rated PFC & NHPC issues and 8.39% for ‘AA+’ rated HUDCO issue.

While this jump has come due to a consistent rise in the yield of the benchmark 7.16% 10-year government bond, the coupon rates with 15-year option and 20-year option have been the highest ever with the HUDCO issue as it is rated ‘AA+’ and carries a leverage of 10 basis points (or 0.10% per annum). I’ll cover the HUDCO issue today and the NTPC issue tomorrow.

HUDCO is launching the second tranche of its tax free bonds from Monday, December 2nd and it will be the first ever tax free bond issue to cross the psychological mark of 9% coupon rate.

Size of the Issue – HUDCO has set the base issue size at Rs. 500 crore with an option to retain oversubscription up to Rs. 2,439.20 crore. The company has already raised Rs. 2,560.80 crore in its first tranche and through a private placement. I think this issue is attractive enough for it to become the last issue from HUDCO’s stable.

Rating of the Issue – Like Tranche I, this issue has also been rated ‘AA+’. CARE and India Ratings are the two companies which have passed their opinion to assign this rating to the current issue.

Again, the bonds are ‘Secured’ in nature as certain receivables of the company will be charged to the extent of amount to be mobilized under the issue. Also, as HUDCO is wholly-owned by the government of India, I would consider the investors’ investments to be comfortably safe in the issue.

OK to NRI Investment – Non-Resident Indians (NRIs) are eligible to invest in this issue, on a repatriation basis as well as on non-repatriation basis. Qualified Foreign Investors (QFIs) are also eligible.

Investor Categories & Allocation Ratio – As always, the investors have been classified in the following four categories and each category will have certain percentage of the issue size reserved for the allocation:

Category I – Qualified Institutional Bidders (QIBs) – 10% of the issue is reserved

Category II – Non-Institutional Investors (NIIs) – 20% of the issue is reserved

Category III – High Net Worth Individuals including HUFs, NRIs & QFIs – 30% of the issue is reserved

Category IV – Resident Indian Individuals including HUFs, NRIs & QFIs – 40% of the issue is reserved

First Come First Served Allotment – Subject to the allocation ratio, allotment will be made on a first come first serve (FCFS) basis in each of the investor categories, based on the date of upload of each application into the electronic system of the stock exchanges.

Listing – Bombay Stock Exchange (BSE) is the only exchange on which these bonds will get listed and the exchange has given its in-principle listing approval to the bonds issued under this tranche. As with all the recent issues, these bonds also will get allotted and listed within 12 working days from the closing date of the issue.

Demat/Physical Option – Investors can apply for these bonds either in physical form or in demat form, as per their comfort and requirement.

No Lock-In Period – These bonds are offering good rate of interest which is tax-free also under Indian taxation laws. As your investment does not provide any tax deduction, there isn’t any lock-in period with these bonds. As these bonds get listed on the BSE, you may sell them whenever you want at the market price.

Interest on Application Money & Refund – HUDCO is the only company which pays the same rate of interest as the applicable coupon rate is on the application money as well as on the money due for a refund. So, with the 20-year option, you’ll get 9.01% as the rate of interest on your application money as well as the refund amount.

Minimum & Maximum Investment – Investors are required to put in a minimum investment of Rs. 5,000 in this issue i.e. at least 5 bonds of Rs. 1,000 face value each. Retail Investors’ investment limit stands at Rs. 10 lakhs, beyond which they will be considered as HNIs and will get a lower rate of interest.

Interest Payment Date – HUDCO has not announced the interest payment date of this issue as yet. I will update this post as and when it gets announced at the time of listing.

While it will be a bonanza for the fixed income investors, I’ll consider this to be a bad situation for the commercial banks, the government and the borrowers. Let’s check how.

Many people have been breaking their fixed deposits to invest in these tax free bonds. It is putting a lot of pressure on the banks to either hike their deposit rates or increase premature withdrawal charges.

As the money is moving out of taxable instruments like fixed deposits, post office schemes etc., the government is also losing out a big amount in tax revenues.

Higher rate of interest will force banks to hike their lending rates also in order to maintain their net interest margins (NIMs) and this outcome will put an additional burden on the borrowers.

With a huge difference between the 10-year interest rate and the 20-year or 15-year rates, I used to prefer the 20-year or 15-year options earlier. But, as the difference has narrowed down considerably, the 10-year option has also become quite attractive now. However, I still prefer the longer duration options as I think it is better to stay invested with longer duration bonds when the interest rates get higher.

Though the issue is scheduled to get closed on January 10, 2014, I really doubt that it would continue that long. I expect it to get closed earlier than that given other companies don’t offer a similar or higher rate of interest.

With coupon rate crossing 9% now on these tax free bonds, there is no reason for the investors to ignore such high rate of interest and keep investing their fresh money into fixed deposits or keep their money invested in it.

Application Form of HUDCO Tax Free Bonds

HUDCO Tax-Free Bonds – Bidding Centres

HUDCO Tax Free Bonds – Banking Matrix

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in HUDCO tax-free bonds, you can contact me at +919811797407

Hi Shiv!

This issue is rated AA & NTPC is rated AAA. What difference do you expect in the price of these 2 bonds post listing?

Will the 10bps higher interest rate being offered by HUDCO get evened out by its lower listing price compared to NTPC because the former is AA & the latter is AAA? For someone looking to hold these bonds till term, there is no difference since they are both secured. But I am asking from the perspective of short term traders

In general, what is the price difference, post listing (if any), between AA & AAA? Could you please elaborate the same with some examples?

Hi Simple,

HUDCO issue is ‘AA+’ rated and NTPC issue is ‘AAA’ rated. I think both issues are equally good for the long term. It is difficult to conclude which issue stands superior. I think NTPC issue is slightly better for listing gains. I’ll try to compare both these issues soon.

Hi Shiv – Sorry this might be a silly question , but what is the probability of getting full allotment in both cases if online application is made on the 2nd-3rd day of the issue ?

Hi Aditya,

I cannot be 100% sure about it. But, I think you should easily get full allotment with both the issues on the 2nd/3rd day of your bidding. I think there will be a better demand for the NTPC issue as the issue size is smaller as compared to the HUDCO issue, it is ‘AAA’ rated and the company is fundamentally better. It is better to bid for the NTPC issue first. If you want to ensure full allotment on the 2nd/3rd day of your bidding, just let me know.

Excellent analysis as always!

it is great that NRIs can also subscribe to this issue.

I wonder why would they? They keep their surplus funds in NRE accounts which gives them more than 9.5% tax free in India. Why would they try to earn only 9% tax free here.

I also understand that NRIs in USA have to pay taxes on their global income. both interest income in NRE accounts and in tax free bonds though tax free in India is taxable In USA. This is a gray area.

Do you have any references for taxation in USA For parents who got recently migrated, obtained a GC, have nil income in USA, but are paying taxes in India for their pensions, interest incomes etc. I also presume that dividends in India, and profit from sale of mutual funds are also treated differently in USA. if you have done any blog on the subject or planning to take up this topic, that would be great. there must be some tax consultants who specialize in filing taxes in USA for such NRIs to avoid double taxation. Actually if you are not earning in USA and are paying taxes in India regularly, you should be OK. But they want us to file return in USA also from the date we become permanent residents there. this is a daunting task for elderly.

Thanks Mr. Ramesh for your kind words !!

Yes, you are right that NRE deposits are also tax free and they are also giving good returns. But, I think it is a short term measure by the Indian government to keep them tax free in order to boost dollar inflows and keep the value of Indian Rupee somewhat stronger.

As these bonds are tax-free right from the beginning, they will remain tax free throughout this long tenors.

Also, I am not sure whether Manshu has done any post on NRI taxation or not, I’ll ask him to cover it, if possible. Personally, I handle these issues for my NRI clients.

Can you give the info on interest dates for ALL the tax free bonds in the last 2 months?

I’ll do a post on the same very soon.

Hi,

I have already invested 10 lac in Hudco in Sep-2013. If I invest another 10 lac, do I get the interest rate for category 4 ? I guess their document says if the investment is over 10 lac across all series then the category will change to HNI. Please clarify this?

Hi Hemant,

Even if you invest Rs. 10 lac in this issue as well, you’ll get the higher rate of interest. The investment should not exceed Rs. 10 lac across all ‘Series’ of the same issue, but it can exceed Rs. 10 lac across different issues or different tranches.

Thanks for the reply.

Thanks for the clarification.

You are welcome!

Hi,

I have already invested 10 lac in Hudco in Sep-2013. If I invest another 10 lac, do I get the interest rate for category 4 ? I guess their document says if the investment is over 10 lac across all series then the category will change to HNI. Please clarify this?

Already replied.

Day 1 (December 2) subscription figures:

Category I – Rs. 2 crore as against Rs. 243.92 crore reserved

Category II – Rs. 163.85 crore as against Rs. 487.84 crore reserved

Category III – Rs. 165.27 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 167.46 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 498.58 crore as against total issue size of Rs. 2,439.20 crore

Hi Shiv,

What do you make of these subscription figures ? Only 2 crores in Cat 1 and about 15-16% subscription in Cat 4 !!

I would call it a wait & watch stance by the Category I investors as they are the smartest investors, whereas Category IV investors’ response always remain like that. Even with the NHPC issue, it was only Rs. 171.82 crore on the first day.

Hi,

Is there a call/put option for this HUDCO series bonds? Also, is it possible to pls clarify if there are other “guaranteed” (or relatively safer) investment options for NRI investors without market risk – other than Bank FD’s, NCDs and tax free bonds – in repatriation mode? I know of NSC’s but there are not repatriable and company FD’s would not fit the above criteria. Pls advise.

Hi,

There is no call/put option with these bonds. Also, there aren’t many fixed income instruments which offer high guaranteed returns without market risk. Even tax-free bonds carry market risk & interest rate risk, if you want to cash out sometime before maturity.

Hi Shiv,

Can you please shed some light on how these bonds and their rates move with passing time.

For Eg i have bonds worth 5 lac and want to sell bonds worth 1 lac every year. Does the interest accumulate and is paid at the end of the tenure or it reflects in the value of the bonds after the interest payment date and the bonds can be sold at that rate.

Lastly are there any previously issued bonds which are available at discounted rates and can give good returns over a few years.

Hi,

With tax-free bonds, interest amount gets annually paid on the interest payment date and credited into your bank account, after which their market price becomes “Ex-Interest”. In between two “ex-interest dates”, the interest amount gets accrued and gets reflected in the market price of the bonds.

As far as I know, the coupon rates the current bonds are offering are the highest. These are higher than the YTMs last years’ bonds are trading at. So, it is better to subscribe to the current year’s bonds.

Day 2 (December 3) subscription figures:

Category I – Rs. 2 crore as against Rs. 243.92 crore reserved

Category II – Rs. 184.09 crore as against Rs. 487.84 crore reserved

Category III – Rs. 229.38 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 311.63 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 727.10 crore as against total issue size of Rs. 2,439.20 crore

Thanks for replying. The interest on these bonds is paid on a monthly/quarterly/half yearly/yearly basis?

And do we have bonds where the interest also gets compounded with the principal?

You are welcome!

1. The interest gets paid annually on a fixed date.

2. No tax free bond issue offers interest to be compounded.

Hi Shiv,

I applied for HUDCO bonds today for some portion of my investment. Just wanted to double-check that i will get full allotment right ?

The issue seems to be losing steam !!

Yes Aditya, you’ll get full allotment in HUDCO bonds if the investment is made today.

Can a retail investor invest Rs. 10 lakhs, or does it have to be less than that (i.e. 9.99 lakhs)?

Yes Deepak, a retail investor can invest Rs. 10 lakhs in a single issue and get higher interest. It is Rs. 10 lakhs or less. The category will change above Rs. 10 lakh investment.

Day 3 (December 4) subscription figures:

Category I – Rs. 12.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 229.39 crore as against Rs. 487.84 crore reserved

Category III – Rs. 291.65 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 488.61 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 1,021.68 crore as against total issue size of Rs. 2,439.20 crore

Please notify me of follow up

Hi Shiv,

I have heard from people that one shoould invest in Bonds only with a sizeable investment amount like 4-5 Lakhs. Is it correct?

How much sense does it make for a small investor with investment amount of say 15000-20000 to invest in Bonds like HUDCO or NTPC? Would it be better to invest in Power Grid FPO with this much of investment amount?

This is kind of dilemma which I am sure many small investors with limited investable amount face always. Since for small investors its always a either-or situation between various investment options.

your take on this please.

Thanks,

Pratyush

Hi,

While Shiv is responding, I would like to add some perspectives of Tax free bond. It depends on the purpose of investment. Long term gain, short term gain, regular income etc. Which tax bracket the investor is in. It makes sense for someone in 20% or 30% tax brackets to chose the Tax free bonds, since return is better considering the return from other investments after the deduction of tax. If one is looking for investing 10-50 K and planning to sell on appreciation , the gain is not so high and it will be better to look at equity market. If there is a chance to save on tax from interest income, Tax free bond is better.

Thanks George for your valuable inputs !! Your thoughts are very clear.

Hi Pratyush,

I am not sure how to answer this question. I think for a small investor, small investment of Rs. 15,000-20,000 is a big investment. To me, the amount of investment doesn’t matter. What matters is the purpose of investment, how much after-tax return I earn from my investment(s) and how favourable is the risk-return ratio.

With tax-free bonds, there are a lot of things which attract me – tax-free fixed returns, PSUs issuing these bonds, scope of capital appreciation, easy liquidity etc.

For higher returns, I always advise equity investments. But, then equity investments are riskier and there is no free lunch in the equity markets. Power Grid FPO is attractively valued. It was attractive in November 2010 as well. But, since then, in 3 years’ time, it has given very poor returns. So, you need to consider all these things while investing.

If Rs. 15,000-20,000 is a big investment for you and you don’t want to lose this money, then equity investment is not for you. Though I expect Power Grid to give 30-50% returns in the next 1-2 years time. I also expect equity markets to give good returns in the next 1-3 years time frame.

Day 4 (December 5) subscription figures:

Category I – Rs. 12.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 268.18 crore as against Rs. 487.84 crore reserved

Category III – Rs. 321.01 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 647.41 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 1,248.63 crore as against total issue size of Rs. 2,439.20 crore

Hi Shiv – Are you going to do a writeup on IIFCL bond issue ?

Since there are number of Adityas 🙂 , posting with full name

Hi Aditya,

I’ll cover it in a day or two.

Hi Shiv,

Are there any more TF bonds expected in December, other than IIFCL?

Thanks in advance…

Hi Deepak,

I am expecting IRFC, NHB & NHAI issues to get launched during December.

Dear Mr Shiv

If aperson does not need regular income and is in the highest tax bracket, does it make sense to invest in these bonds. Or else if a person decides to go for the bonds , where does he invest the annual interest so as to retain the benefit of no taxation.

would debt mutual funds be the right scheme to invest the annual interest received?

Dear NKN,

You can invest the interest amount in PPF, debt mutual funds, tax-free bonds or any other instrument which offers you a good investment opportunity.

Dear Shiv,

I heard that Tata Sons is going to come out with 300 Crore debt issue soon – do you have any update if NRI’s can invest and if there will be cumulative option?

Dear Jayaram,

Most of these deals happen through private placement. So, general public cannot participate in these issues.

You have not posted Day 5 (December 6) subscription figures.

When will PGCIL fix the price? How many shares can I get for 2L application if issue is subscribed 2.17 time? I will get 6 lots minimum- how much more?

Thanks Vivek for reminding me !! I’ll do it right away. I was under the impression that I did that yesterday.

Basis of Allotment system has been changed for the IPOs/FPOs Vivek. Though I analysed it last year, I don’t remember how exactly it works. But, one thing is for sure – every valid application will get at least one lot of 150 shares allotted. I am working on a post with many such queries about Power Grid FPO.

Day 5 (December 6) subscription figures:

Category I – Rs. 22.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 288.48 crore as against Rs. 487.84 crore reserved

Category III – Rs. 341.81 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 770.70 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 1,423.03 crore as against total issue size of Rs. 2,439.20 crore

Category IV should get oversubscribed in a couple of days time.

Dear Mr. Shiv

I have applied online today under category IV ( <10 lakhs). I believe that I will get full allotment. Kindly advise on subscription figures for today Day 6. Kindly also advise as to how to check allotment status online and when would the allotment take place.

Many thanks for your support and co-operation.

Hi NKN,

Though it is quite close to getting fully subscribed in the retail investors’ category, it doesn’t look like that it will get fully subscribed today itself. I think you’ll get the full allotment.

Hi Shiv,

Will HUDCO wait for all categories to get subscribed fully ? Or they might call an early close to the issue ? considering this is tranche 2 of their bond issue and those who have already invested in Tranche 1 may not be interested here.

Hi Aditya,

As the retail investor category (Category IV) is already close to getting fully subscribed, HUDCO will now wait for only the issue to get fully subscribed and not each category. As soon as the subscription figures cross Rs. 2,439.20 crore mark or reach very close to it, HUDCO should decide to close the issue the very next day.

Here is the link to check the allotment status:

http://www.bseindia.com/markets/publicIssues/BSEcumu_demand.aspx?ID=740

Allotment will take place within 12 working days from the issue closing date. If the issue gets closed on say 18th December, you’ll get allotment within 12 working days from December 18th.

Dear Mr Shiv

Thanks for your quick response. By allotment status I meant a website where I could feed my application number and demat details & know if indeed I have got full allotment.

As of now it is not possible. It will be declared only once the Basis of Allotment gets finalised.

You’ll get to check it on this link: http://mis.karvycomputershare.com/ipo/#

Day 6 (December 9) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 301.97 crore as against Rs. 487.84 crore reserved

Category III – Rs. 464.52 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 934.37 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 1,747.89 crore as against total issue size of Rs. 2,439.20 crore

Category IV should get oversubscribed tomorrow.

Hi,

By saying “Category IV should get oversubscribed tomorrow.” , is that I cannot invest in this Bond after its over subscribed ?

Thanks & Regards

Devan.

It is not like that Devan. You can very well invest in Category IV even after it gets oversubscribed. But, as it is on a “first come first served” basis, there is no guarantee of allotment if you invest after its over-subscription.

Seems that HUDCO is oversubscribed now in the Retail category

That’s correct, it has got oversubscribed in the retail category.

Day 7 (December 10) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 312.13 crore as against Rs. 487.84 crore reserved

Category III – Rs. 485.05 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 1,004.64 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 1,848.85 crore as against total issue size of Rs. 2,439.20 crore

Hi Shiv

I have one question for HUDCO 9.01 % Bond. On day 7 [ Dec 10 ] Category II – Rs. 321.13 crore as against 487.84 crore.

So now if apply on day 8 [ Dec 11 ] and category II is not fully subscribed up to 487.84 crore there are chances of full allotment what i apply.

What i understand is that in Category II i can apply up to the day it fully subscribe up to 487.84 crore and in that case i will get the full allotment what I apply.

Please explain me. Because i am gettimg some fund on 13 th December.

That is correct Paresh. If you apply for it today and if it does not get oversubscribed by 5 p.m., you’ll get full allotment.

Hi Shiv

That doesn’t sound right to me. First come first serve basis is applicable to respective category in my view. If a Cat II investor applies for their quota any day before HUDCO decides to close the offer so long they have the limit availability they should get their allotment. How can a Cat 4 investor who’s applying over their reserved limit get an allotment from Cat 2 reserved limit in such a case?

Hi Subbu,

Paresh wants to apply in Category II itself (not in Category IV) and you are absolutely right that each category is going to get its own allocation. If Category II remains unsubscribed, then whatever portion remains unsubscribed will go to the Category IV investors first.

Hi Shiv,

Excellent coverage and you do take pains to respond to each and every query.

I have also subscribed to hudco bonds under retail category. The advantage with this issue is that the interest rate is very high and it is unlikely that any other issue will be offering this high an interest, at least in the near future. And as the interest rates start falling in the future, one can get handsome listing gains. However, the disadvantage with this issue, as with other tax free bonds is the virtual absence of liquidity in the secondary market. Some bonds such as NHAI get traded frequently, while most other do not get that heavily traded. However, looking at the size of this issue, I am hopeful that there is a good liquidity when the bonds get listed on the BSE. My suggestion is that the financial intermediaries should trade in these bonds more frequently so as to provide the desired liquidity to the small investors.

Ram Mohan

Thanks Mr. Ram Mohan for your inputs !!

There are many factors which affect liquidity for a specific issue and you are right NHAI has liquidity which is good enough for a bond. I too hope this issue will have a better liquidity than the previous issue by HUDCO.

Financial intermediaries don’t find any profitable opportunities in trading unnecessarily in the bond market. That is why they don’t do that.

Thanks Shiv for your comments. I have actually made a model for calculating the effect of yields on the capital values of long term bonds. The longer the tenure the greater is the impact due to changes in yields. For instance, for a 20 year bond, which is the longest available now, a 1% change in yield affects the price by 10%. This provides the greatest leverage. Naturally, the leverage decreases with decrease in tenure. Thus, with the HUDCO bond which is available at 9% yield, the price would increase by 10% if the yield goes down to 8%. This change in yield may not happen overnight, but even if it happens over a 2 year period, this effectively translates into a capital appreciation of 10% over 2 years, or 5% per year. This is in addition to the 9% interest that one gets from the bonds, which means one can get a 14% virtually risk-free return per year. And one can exit after the 2 years.

Hi Mr. Ram Mohan,

Your model is called the duration effect. The higher the duration (volatility), the higher is the change in the bond prices. I am sure 1% fall in the YTM (yield) of a 20-year tax-free bond would result in a more than 5-10% increase in its prices.

Hi Shiv,

Do you expect RBI to hike repo rate this time and if it does will the coupon for future bonds increase?

Hi Jay,

Personally, I think Dr. Rajan would like to surprise the markets by not raising the Repo Rate this time. But, if the Repo Rate gets increased, then I think G-Sec yields will rise and future coupon rates would get fixed higher.

I also think Raghuram Rajan (who incidentally also happens to be my classmate) likes to surprise the markets and he may not change the rates contrary to the 25 bps hike that the market is expecting.

That is great to know Mr. Ram Mohan !! So, if we want to meet Dr. Rajan some day, I hope we can always contact you ??

Also, even I would like Dr. Rajan to give Repo Rate hike a miss this time and give growth a chance to revive. In fact, it is the government’s duty to take steps to control inflation.

Mr. Ram Mohan, your classmate has actually left the markets pleasantly surprised. 🙂

Yes he has Shiv. Even when he was the CEA before becoming the RBI Guv, ie when he was on the other side of the fence, so to speak, and voicing views of the Finance Ministry, he used to say that the RBI needs to surprise the markets at least once in a while. This would put all the speculators on guard. Raghuram Rajan has been a good event for the markets ever since he took over in September. Since then on, his exemplary achievement has been to bring the Rupee back to stability and that singular achievement has brought in confidence in the markets especially for the overseas markets, who were worried whether they would earn far less when the time actually comes to withdraw the money. His other achievement has been to reverse the inverted yield curve. When he took over the short term debt yields were higher than long term yields, a sure recipe for economy stagnation. Now the yield curve has straightened and that is good.

Yes, you are absolutely right! He has been smarter and fortunate also. He has been successfully able to reverse the measures taken by the RBI earlier and correct the yield curve.

But, at the same time, I would fully support the ex-Governor of RBI, Dr. Subbarao. Whatever he did, it was done under finance ministry’s undue pressure. I think the rupee got stabilized due to deferment of QE tapering and improvement in the market sentiment.

Whatever wrong is there in the economy, it is due to the government’s incorrect policies and unreasonable arrogance.

Day 8 (December 11) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 328.77 crore as against Rs. 487.84 crore reserved

Category III – Rs. 494.95 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 1,039.73 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 1,910.48 crore as against total issue size of Rs. 2,439.20 crore

Hi Shiv,

Is it possible to check allotment status for a physical application for hudco bonds? If so, pls could you advise how and when it can be tracked? Thanks in advance.

Hi Jayaram,

You can check the allotment status from the below pasted link after the bonds get allotted:

http://mis.karvycomputershare.com/ipo/

Hi Shiv,

Nov CPI data is 11.24 percent – do you think that RBI governor would still “surprise” markets by keeping status quo on repo rate? Thanks

No, not now. CPI Inflation is on a higher side and deeply disappointing. 25 basis points Repo Rate hike is a done deal now. If Dr. Rajan does not hike it, then it would be difficult for us to understand his reasons behind it. This again puts the government in an extremely difficult position now. Its a wake up call for Mr. Chidambaram !!

Hi Shiv,

So higher coupon rates in the offering – for forthcoming bonds ?

Yes, it seems so.

Hi Shiv,

Any news at all on IRFC\NHAI\NHB ? Possibly higher g-sec yields now makes these issues interesting with higher coupon rates possible as you stated

Hi Aditya,

I’ve been told that IRFC is getting ready to launch its issue anytime on or after December 23rd. NHB has also filed its Draft Shelf Prospectus on December 13th, so you can expect its issue to hit in the last week of December or 1st week of January.

Thanks Shiv – useful info

Day 9 (December 12) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 330.08 crore as against Rs. 487.84 crore reserved

Category III – Rs. 504.25 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 1,064.30 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 1,945.67 crore as against total issue size of Rs. 2,439.20 crore

Please advise why there is difference in your subscription figures vs bse website figures like in cat III bse website shows 3.24 times subscription whereas above figures are different.

3.24 times is as per the base issue size of Rs. 150 crore applicable to Category III.

Day 10 (December 13) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 338.58 crore as against Rs. 487.84 crore reserved

Category III – Rs. 508.86 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 1,083.12 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 1,977.59 crore as against total issue size of Rs. 2,439.20 crore

Hi Shiv

I am not sure this is the time to ask you.

I want to know is there any Tax Free Bonds coming in the month between May 2014 to August 2014.

Hi Paresh,

As of now, it is not possible for anybody to tell you anything about it. The quantum of tax-free bond issues get announced only in Budget every year. Next year there is no certainty that these bonds would get issued or not.

Day 11 (December 16) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 342.13 crore as against Rs. 487.84 crore reserved

Category III – Rs. 521.01 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 1,107.33 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 2,017.51 crore as against total issue size of Rs. 2,439.20 crore

today’s subscription numbers ?

Day 12 (December 17) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 342.63 crore as against Rs. 487.84 crore reserved

Category III – Rs. 526.79 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 1,121.26 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 2,037.71 crore as against total issue size of Rs. 2,439.20 crore

Hi Shiv,

what happens to accrued interest if bonds are sold before payout? say payout date is month away and I sell my holdings, the accrued interest goes to buyer?

Hi Binish,

Yes, that’s right. The person who holds the bonds on a day before the “Ex-Interest” date or whose name appears in the books of the Registrar on the “Record Date”, gets the interest paid on the “Interest Payment Date”.

thanks Shiv,

I have some HUDCO TFBs, which will receive payment on Feb’16 2013. I guess I will sell them and invest again hopefully in newer bonds after payout. Lets see.

hmm… just share your actions when you take a decision.

In a great news, Dr. Rajan has left the Repo Rate and the CRR unchanged. The RBI wants to read more data before hiking rates from these levels.

Hi Shiv,

So where does that leave us now with the coupon rates for upcoming issues 🙂

Ok I guess you answered it on the other post

Day 13 (December 18) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 347.33 crore as against Rs. 487.84 crore reserved

Category III – Rs. 533.41 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 1,134.40 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 2,062.18 crore as against total issue size of Rs. 2,439.20 crore

Hi Shiv

I have already invested Rs. 1,40,000 before a week and now I would like to invest Rs. 7,60,000 more to-day. I think I will get the full allotment of total investment of Rs. 9,00,000 because total is less then ten lacs.

As on December 18 Category II – Rs. 347.33 crore as against Rs. 487.84 crore reserved.

My status is A O P Trust which fall in to category II.

I applied both applications in category II

I hope there should be no problem to apply 2 times in the same name and hope will get the full allotment because category II is still open by 140 crore

Hi Paresh,

Category II investors need not worry about Rs. 10 lakh limit. You can submit multiple applications under the same name (with same PAN) and your application won’t get rejected.

Day 14 (December 19) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 350.85 crore as against Rs. 487.84 crore reserved

Category III – Rs. 540.82 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 1,143.14 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 2,081.84 crore as against total issue size of Rs. 2,439.20 crore

NHAI to launch its tax-free bonds issue sometime around mid-January.

http://www.thehindubusinessline.com/markets/nhais-taxfree-bond-issue-to-hit-market-in-midjan/article5478623.ece

Hi AGAIN Shiv!

If I apply for these, will I get 100% allotment since other Categories have not been subscribed for as yet?

Hi Simple,

In this case, if the application is submitted now, there is no guarantee that the retail investors will get 100% allotment. If other investors put in money any day before the issue gets closed, then they will be allotted bonds as per their reserved portion first. But, still there is a high probability that other categories won’t bid for a high amount now.

Thank you

You are welcome Simple!

Hi Shiv

On December 19 , 2013 against one of my question you have replied me :

CATEGORY II INVESTORS NEED NOT WORRY ABOUT RS. 10 LAC LIMIT…

so i have already submitted a application for Rs. 10 Lac in category II before a week. And if now i submit another application for another 10 Lac in category II , i will get the full allotment of Rs. 20 Lac.

Yes, that’s right Paresh.

Today’s subscription numbers ?

Thanks for the reminder Aditya! 🙂

Day 15 (December 20) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 360.73 crore as against Rs. 487.84 crore reserved

Category III – Rs. 542.22 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 1,154.75 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 2,104.73 crore as against total issue size of Rs. 2,439.20 crore

IRFC issue to get launched on January 6th. Coupon Rates are 8.48% p.a. for 10 years and 8.65% p.a. for 15 years. 20 years option is not available. The issue closes on January 20th.

Hi Shiv,

Is this coupon rate for cat IV i.e. retail investors?

Yes Debasis, it is for the retail investors.

The unenthusiastic subscriptions for Category I,Ii and Iii are trying to give a message to retail investors!

Or is it just an excellent opportunity for Retail investors to grab some high interest bearing TFB even on Monday.

In view of falling interest rates now, is it advisable to subscribe for Hudco now? what are chances of full allotment on Monday?

Hi Mr. Ramesh,

With HUDCO application now, there is a complete uncertainty whether you’ll get allotment or not. It depends on the response from other categories of investors and how soon the issue gets closed. If you want to ensure full allotment, then you should subscribe to the IIFCL bonds.

Hi Shiv

As on Dec 20 in Category II – Rs. 360.73 crore against Rs. 487.84 crore reserved.

SO what you think if i apply for 10 Lac on Monday , will i get the full allotent ?

Sorry Paresh, I would not like to answer such personalized queries on a regular basis. You can avail my advisory services if you want me to answer such queries and more like that on a regular basis. Please don’t mind.

Hi Shiv

Thanks for responding me.

But I think my question was not personalized query , I was just ask you if I apply on Monday what you think I will get the full allotment if it will not fully subscribe and if fully subscribe can they allot partial . I was asking you your view about this.

I hope you can understand me.

Thanks

Day 16 (December 23) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 372.68 crore as against Rs. 487.84 crore reserved

Category III – Rs. 548.98 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 1,172.72 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 2,141.41 crore as against total issue size of Rs. 2,439.20 crore

Hi Shiv

When do you think HUDCO will close their TFB? From extrapolating retail subscription , most likely by next monday , retail subscription will ensure total issue size is achieved. Do you think HUDCO will wait till Jan-10 or will announce closure once issue size is reached? I understand in the past companies have kept TFB issue open till retail gets fully subscribed even though issue size is reached, here the situation is completely reverse and not seen yet.

This site has become so informative that it has become a must visit for me every day to get latest info. Thanks for all the hard work you are putting in to post and respond to every query

Regards

Ramadas

Thanks Mr. Ramadas for your kind words !!

I think HUDCO issue should take at least 5-7 working days to get closed. HUDCO will not wait till January 10th to close the issue as the retail category has already got oversubscribed.

Companies wait for the retail category to get subscribed first and then the whole issue to get subscribed. They don’t close it until the retail category gets fully subscribed, like NHPC, NTPC etc.

Now, HUDCO is waiting for the whole issue to get fully subscribed, whereas IIFCL is waiting for the retail category to get fully subscribed. 🙂

NHB Tax-Free Bonds issue opens on December 30th. Coupon Rates – 8.51% for 10 years, 8.88% for 15 years and 9.01% for 20 years. It is a ‘AAA’ rated issue and closes on January 31, 2014. I am pleasantly surprised with the coupon rates.

Day 17 (December 24) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 374.23 crore as against Rs. 487.84 crore reserved

Category III – Rs. 550.54 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 1,182.46 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 2,154.27 crore as against total issue size of Rs. 2,439.20 crore

Hi,

I was wondering if you or anyone else would kindly consider clearing the following query:

Pls kindly clarify all the implications of the flowing article titled “RBI allows foreign retail investments in tax-free rupee bonds”

http://articles.economictimes.indiatimes.com/2013-12-25/news/45561782_1_ashutosh-khajuria-investor-base-fixed-deposits

What bonds are being referred to here? I see NHB has not allowed NRIs to invest in the recent tranche – would this RBI clarification imply NRI can invest?

Thanks in advance.

Hi Jayaram,

No, it does not mean that NRIs can invest in the current issue of NHB. I think this RBI decision needs to be notified before the foreign retail investors would be able to invest in these issues.

Day 18 (December 26) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 374.74 crore as against Rs. 487.84 crore reserved

Category III – Rs. 553.74 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 1,190.36 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 2,165.87 crore as against total issue size of Rs. 2,439.20 crore

Think HUDCO will fall just short even if it keeps the issue open till 10th Jan

🙂

Hi Shiv

In IRFC Bond coupon rate for 15 years is 8.65 % , but my investment is in Category II , so what will be the coupon rate for that.

It will be same or less ?

8.65 is for retail , category II rate would be 8.40 %/

Subscription numbers please 🙂

Thanks for the reminder! 🙂

Day 19 (December 27) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 374.74 crore as against Rs. 487.84 crore reserved

Category III – Rs. 558.04 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 1,197.90 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 2,177.72 crore as against total issue size of Rs. 2,439.20 crore

Day 20 (December 30th) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 375.09 crore as against Rs. 487.84 crore reserved

Category III – Rs. 560.89 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 1,208.43 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 2,191.44 crore as against total issue size of Rs. 2,439.20 crore

Day 21 (December 31st) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 376.29 crore as against Rs. 487.84 crore reserved

Category III – Rs. 572.84 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 1,218.28 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 2,214.44 crore as against total issue size of Rs. 2,439.20 crore

Day 22 (January 1) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 376.39 crore as against Rs. 487.84 crore reserved

Category III – Rs. 574.89 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 1,228.53 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 2,226.84 crore as against total issue size of Rs. 2,439.20 crore

Also, HUDCO tax-free bonds issue is getting closed on Friday i.e. January 3rd, as against its scheduled closing date of January 10th.

But the issue is not yet subscribed, are they expecting it to be subscribed in next 2 days or is there something else?

As a retail investor, shall I apply to the issue even though the retail category is oversubscribed?

Probably they don’t want all the money to be raised in this public issue. They have the option to raise it through a private placement as well.

If you apply as a retail investor either today or tomorrow, you’ll get 100% allotment, in case other investor categories don’t put bulk money.

thanks.

You are welcome!

Please post today’s subscription numbers…

Day 23 (January 2) subscription figures:

Category I – Rs. 47.28 crore as against Rs. 243.92 crore reserved

Category II – Rs. 378.84 crore as against Rs. 487.84 crore reserved

Category III – Rs. 480.15 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 1,244.82 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 2,151.09 crore as against total issue size of Rs. 2,439.20 crore

Hi Shiv

Interesting trend in subscription . HNI’s started to withdraw bids. 94 crore withdrawn compared to yesterday. Dont understand why someone will withdraw a day before closure. I didnt understand why hudco is pre closing this issue with 300 crore lesser than target either. Is there any interest rate restriction for private placement of TFB?

Regards

Ramadas

Hi Ramadas,

Yes, it is interesting. HUDCO is closing the issue as it doesn’t want to drag it anymore. Most of the investors have already invested whatever amount they wanted to. Whatever amount is left, HUDCO will try to cover it through private placement(s), if required. Almost similar rules apply to private placements as well what they are for the public issues.

Hi Shiv,

Total subscription is less than from 1st Jan. Cat-III lot of withdrawals happened, is there any specific reason?

Hi Ravi,

I don’t have any idea about the reasons for this withdrawal.

Please post final subscription numbers.

Day 24 (January 3) subscription figures:

Category I – Rs. 47.03 crore as against Rs. 243.92 crore reserved

Category II – Rs. 379.62 crore as against Rs. 487.84 crore reserved

Category III – Rs. 491.03 crore as against Rs. 731.76 crore reserved

Category IV – Rs. 1,267.15 crore as against Rs. 975.68 crore reserved

Total Subscription – Rs. 2,184.83 crore as against total issue size of Rs. 2,439.20 crore

The issue stands closed today.

Hi Shiv

I would like to know whether HUDCO TFB is closed on Friday or not , because I would like to invest on Monday

It has closed on Friday Paresh.

Hi Shiv,

I have applied for these HUDCO TFBs on the first day in Cat 4 and its been a week since the issue closure. I do not have a demat account so I applied for paper bonds. Is there a way I can track my application ?

Thanks !!

Hi Gaurav,

I think you need not worry about it. It doesn’t really matter whether you applied for it on the 1st day or the last day, the allotment process starts only after the issue gets closed. I don’t think there is any way you can track the status of your application till the time the allotment gets started. Just wait for 4-5 days more and you’ll get to know the allotment status.

Thanks for the reply Shiv… much appreciated !!!

You are welcome!

Hi Shiv, my demat account shows an allocation of the HUDCO bonds tonight, as of 10 PM.

Hi Rama, thanks for this info!

HUDCO allotment was really quick, faster than how I expected it to be.

Got Hudco and NHB bonds credited in my demat account !!! Only thing remaining is the interest money from HUDCO application.

Hi Shiv, I had applied for these HUDCO bonds in physical form.. pls could you advise where I can check my allotment status? Thanks

Hi Jayaram,

You cannot check the allotment status of your application as of now, but here is the link to check it whenever it gets uploaded by the Registrar:

http://mis.karvycomputershare.com/ipo/#

You can check your bank account though for the credit of interest payment.

Has anyone got the HUDCO application interest amount ?

Hi Shiv – Any news on the deemed date of allotment for HUDCO ?

Oh sorry, I just forgot to update it. Just give me a few minutes.

HUDCO tax-free bonds to get listed on the BSE on January 17th i.e. Friday.

Here are the BSE codes for the same:

8.76% 10-year bonds – BSE Code – 961814

8.83% 15-year bonds – BSE Code – 961815

9.01% 20-year bonds – BSE Code – 961816

Deemed date of allotment has been fixed as January 13, 2014. Interest will be paid on January 13th every year.

Hi Shiv,

Thanks very much for this.. Do you know on what date application amount interest will be credited to bank a/c?

Hi Jayaram,

Ideally they should have done it by now, but I don’t know why they’ve delayed it. But, 12 working days is the deadline from the closing date of the issue, which is January 21st.

Hi Shiv, Jayram – I got the HUDCO application money interest credited to my bank account late evening today

That’s great, thanks for sharing it Aditya!

Okay .. then will interest on the application amount be paid till date of credit or only till date of allotment?

Obviously, only till the date of allotment.

Thats good shiv..

Dear Mr. Shiv

My demat account shows that units have been credited.But the link u had posted does not show the allotment status?

Dear NKN,

Please let me know your application no. or PAN no. You can do so on my email id either, if you don’t want to share it here.

Sorry, please don’t do that. HUDCO Tranche II allotment data is yet to get uploaded by Karvy Computershare.

Hudco bonds listed on BSE today..Is trading now at Rs 1018

Thanks Raju for this info!

HUDCO bonds got listed today on the BSE. 9.01% 20-year bonds opened at Rs. 1,019, touched a high of Rs. 1,022, a low of Rs. 1,007.01 and finally closed at Rs. 1,009.08.

http://www.bseindia.com/NewStockReach/StockReach_Debt.aspx?scripcode=961816

Hi Shiv,

I got the allotment letter from HUDCO yesterday and it says that TDS is deducted from the interest payment of 37 days. Do you think it is correct if the TDS is deducted given that these are tax free bonds ?

Thanks,

Gaurav

Hi Gaurav,

Interest earned on the application money is taxable and that is why the company is right in deducting TDS on the interest earned by the investors. Actually, the tax-free interest period starts from the date of allotment and ends on the date of maturity.

They have correctly deducted TDS on this interest. however they have not mentioned the TAN number. We need that while filing tax returns. Somewhat unprofessional company, I would say.

Don’t worry, it would be there in your Form 26AS.

Hi Shiv

I got letter of allotment for HUDCO tranche II bonds, the letter says that i need to send the letter to registrar of companies to get bond certificates. Can you please throw some light on process of what to do after getting letter of allotment, if i have subscribed for bonds in physical form.

That’s correct Kunal, you need to send the letter of allotment to the Registrar, Karvy Computershare, and they’ll send you the bond certificate to your registered address.

I applied for HUDCO Transche II Bonds in Jan but haven’t yet got the allotment. I applied via ICICI Direct site and while the transaction shows as executed I am yet to get the bonds allotment and the ICICI Direct site does not show it in my portfolio as seemingly they have not got the info from HUDCO.

What all can I do?

Hi Manish,

Just check from the following link whether you’ve been allotted HUDCO tranche II bonds or not – http://mis.karvycomputershare.com/ipo/#

If it doesn’t show any allotment in your name, then you should either contact the Registrar (Karvy Computershare) or the ICICI Direct team to know why it is not showing there and why no allotment has been made.

Hi Shiv,

I have applied for HUDCO tax free bonds Tranche II in Dec 2013 and received the allotment letter for the bonds. I got a letter dated 18.3.2014 asking me to return the letter of allotment to Karvy by 04.04.2014. However, since I was traveling, I was not able to send the letter of allotment back to them by the due date. Will they nevertheless send me the bond certificates or can I still send the letter of allotment to them even after the deadline of 04.04.2014?

Regards

Rajan

Hi Rajan,

I think you should send the letter of allotment to Karvy as soon as possible. This would set you free with your responsibility.

Hi Shiv, My brother is an NRI and had got the allotment letters for the above Dec 2013 series of HUDCO bonds in Physical Form. Is it compulsory that he should do any other thing such as applying for physical certificates of bond to receive annual interest in NRE a/c or it will just happen automatically every year without any further step? Thanks in advance.

Hi Jay,

Your brother will get interest amount credited directly to his NRE A/c. He must have got the interest on the application money credited to the same account when the bond allotment happened.

Dear Shiv, It was very nice to talk to you today. Thanks for your time. Reg these HUDCO bonds,Is there a possibility to pls let me know where I can find details reg TDS info on short and long term capital gains for NRI’s – if it is sold in demat form. I had already checked the HUDCO prospectus and did a google search but not able to get info any specific info reg NRI applicants. Thanks in advance.

You are welcome Dr. Subramanian !!

Here is the link to check the TDS rates applicable to NRIs:

http://www.incometaxindiapr.gov.in/incometaxindiacr/contents/forms2010/pamphets/tdsrates_2013_14.htm

dear sir

I applied for the HUDCO TAX FRRE BOND Tranche II Duirng december.I did not recive the bond allottment letter nor credit of interst to my bank account . I contacted the Axix bank where i had deposited the appplication and cheque . The Axix Bank had debited my account on 5.12.13 .They contacted KARVEY , and informed that i shall be getting allottement shortly . Then they informed during mid july 14 ,that allotment has not made and for refund I have to contact , Karvey Hyderabad. I contacted karvey hyderabd and their “Corporate registry investment cell ” informed that refund is bieng processed. Finally they refunded the principal only .On further enquiry they no interst for delay is payable and I can complain to any authority like SEBI etc. May i request you to inform the legal position , and how to get back my interst for delay period and if I have to complain to which authority to complain.I am an old lady and this amount was my life saving. This loss of intesr of about 10 month Which is about Rs 50000/- has really broken me.

Regards

Mrs Nirmala Pandey

Dear Mrs. Pandey,

Sorry to know about such a painful experience you had. SEBI is the regulatory authority for all such complaints, you’ll have to register your complaint with SEBI only.

Hi Shiv,

The first interest payout has happened on 13th January and the bond is now trading at around 1200 level. Do you have any idea whether it will go up further or will be it wise to book profit at these levels?

Thanks,

Amit

Hi Amit,

With falling interest rates, I think the value should further go up. But, I think the pace of capital appreciation should be slow and volatile going forward.

Hi Shiv,

This may sound a little silly but I thought I ask you to be doubly sure.

In all the public issues of Tax Free Bonds during 20012-13, 2013-14 & 2014-14, the limit for retail investors was Rs. 10 L i.e. 1000 Bonds which fetched a slightly higher coupon rate than the non retail category.

If I buy more than 1000 bonds from the market now, what will be applicable interest rate – the one applicable to retail category or the lower rate ?

Hi Shiv,

I have query related to Tax Free Bonds in general.

In the IPOs for these bonds, the differential rates of interest were offered to the retail investors (investment up to 10 Lacs = 1000 Bonds) and general category investors i.e. the retail investors got marginally higher interest.

What about the TFBs bought from the stock market ? Whether the lower interest rate will be applicable irrespective of the no. of Bonds purchased or higher interest rate will be applicable up to 1000 Bonds and if one exceeds ceiling of 1000 Bonds, lower interest rate becomes applicable on the total holding ?

Thanks.