NTPC 8.91% Tax Free Bonds – December 2013 Issue

This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

NTPC (BSE:532355), the country’s largest power generator and a ‘Maharatna’ company, is set to enter the battlefield of tax-free bond issues from Tuesday, December 3rd. It would become the sixth company to do so this financial year after REC, HUDCO, IIFCL, PFC and NHPC.

The issue will remain open for just ten working days to get closed on December 16th i.e. Monday.

Size of the Issue – NTPC has been authorized to raise Rs. 1,750 crore from tax free bonds this financial year. The company plans to mop up the whole of Rs. 1,750 crore from this issue itself, including the green shoe option of Rs. 750 crore, as the base issue size is Rs. 1,000 crore.

Rating of the Issue – NTPC is a big company with market capitalization of Rs. 121,497 crore as compared to REC’s market cap of Rs. 22,376 crore, NHPC’s market cap of Rs. 22,326 crore and PFC’s market cap of Rs. 20,956 crore. Considering its big size and strong fundamentals, CRISIL and ICRA have assigned ‘AAA’ rating to the issue.

Like all other tax free bond issues, these bonds are also ‘Secured’ in nature and certain fixed assets of the company will be charged equivalent to the outstanding amount of the bonds.

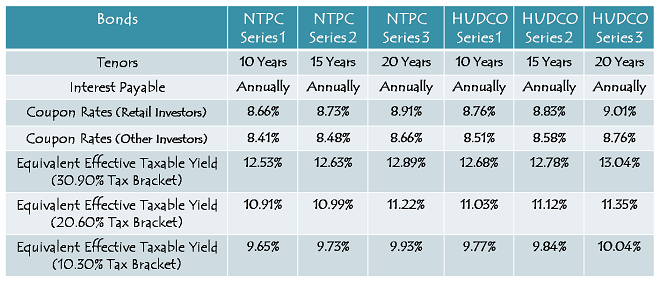

Coupon Rates on Offer – As the issue is rated AAA, the coupon rates are lower by 10 basis points or 0.10% lower than that of HUDCO. NTPC is offering 8.66% per annum for its 10-year option, 8.73% per annum for the 15-year option and 8.91% per annum for the 20-year option to the retail investors investing less than or equal to Rs. 10 lakh.

As always, these rates would be lower by 25 basis points (or 0.25%) for the non-retail investors.

NRI Investment – Repatriation Not Allowed – Non-Resident Indians (NRIs) are also eligible to invest in this issue, but only on a non-repatriation basis. NRI investors will not be allowed to repatriate its interest amount or maturity proceeds outside India.

QFI Investment – Also, unlike HUDCO tax free bonds, Qualified Foreign Investors (QFIs) are not allowed to invest in this issue.

Investor Categories & Allocation Ratio – As always, the investors have been classified in the following four categories and each category will have certain percentage of the issue size reserved during the allocation process:

Category I – Qualified Institutional Bidders (QIBs) – 10% of the issue is reserved i.e. Rs. 175 crore

Category II – Non-Institutional Investors (NIIs) – 25% of the issue is reserved i.e. Rs. 437.50 crore

Category III – High Net Worth Individuals including HUFs & NRIs – 25% of the issue is reserved i.e. Rs. 437.50 crore

Category IV – Resident Indian Individuals including HUFs & NRIs – 40% of the issue is reserved i.e. Rs. 700 crore

Allotment on First Come First Served Basis – Subject to the allocation ratio, allotment will be made on a first come first serve (FCFS) basis in each of the investor categories, based on the date of upload of each application into the electronic system of the stock exchanges.

Listing – NTPC has decided to get these bonds listed on both the stock exchanges i.e. National Stock Exchange (NSE) as well as the Bombay Stock Exchange (BSE) and has successfully got the necessary in-principle listing approval also from these exchanges. The bonds will get allotted and listed within 12 working days from the closing date of the issue.

Demat/Physical Option – Investors have the choice to apply for these bonds either in physical form or in demat form, whichever they like.

No Lock-In Period – These tax-free bonds are freely tradable and do not carry any lock-in period. An investor may sell them at the market price whenever he/she wants after these bonds get listed on the NSE or BSE.

Interest on Application Money & Refund – NTPC will pay interest to the successful allottees on their application money at the applicable coupon rates, from the date of realization of application money up to one day prior to the deemed date of allotment. Unsuccessful allottees will get interest @ 5% per annum on their refund money.

Minimum & Maximum Investment – Investors are required to put in a minimum investment of Rs. 5,000 in this issue i.e. at least 5 bonds of Rs. 1,000 face value each. Though there is no upper limit for the investors to invest in this issue, an investor investing more than Rs. 10 lakhs will be categorized as an HNI and will get a lower rate of interest.

Interest Payment Date – NTPC will make its first interest payment exactly one year after the deemed date of allotment. As the deemed date of allotment will be announced just before the listing date, I will update this post as and when it gets announced.

NTPC is ranked fourteenth among the top Indian companies by market capitalization. Also, at present, there are only seven central public sector enterprises (CPSEs) which have been conferred the status of Maharatna and NTPC is one of them.

Among thirteen companies, which have been authorized to issue tax free bonds this financial year, NTPC is the only company which has this Maharatna status. In fact, the company this year in March got awarded as the most efficient Maharatna in manufacturing for the year 2012.

As NTPC is fundamentally a better company, the issue is rated ‘AAA’ and the issue size is relatively smaller at Rs. 1,750 crore, I think its coupon rates are attractive enough for the issue to get oversubscribed in the first week itself. I expect the investors’ response to be even better than that for NHPC and the company to get it preclosed much before its official closing date of December 16th.

Also, I expect the issue to provide some listing gains also, like it has been the case with NHPC bonds and PFC bonds. Let us see if it meets my expectations or not.

Application Form of NTPC Tax Free Bonds

NTPC Tax-Free Bonds – Bidding Centres

NTPC Tax-Free Bonds – Banking Matrix

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in NTPC tax-free bonds, you can contact me at +919811797407

Dear Shiv,

It would be timely and helpful for investors, if you could post an an article on “Indexed National Saving Securities- Cumulative (IINSS-C)” due to be launched in Dec 2013.

Their comparison with other instruments like Tax Free Bonds, Bank FD’s etc with regard to returns, tax treatment, liquidity, safety, portfolio allocation etc may be considered.

The RBI Notification in this regards is reproduced below:

“Inflation Indexed National Saving Securities- Cumulative (IINSS-C)

The Reserve Bank of India, in consultation with Government of India, has decided to launch Inflation Indexed National Savings Securities-Cumulative (IINSS-C) for retail investors in the second half of December 2013.

These securities are being launched in the backdrop of announcement made in the Union Budget 2013-14 to introduce instruments that will protect savings from inflation, especially the savings of the poor and middle classes.

The distribution/sale of IINSS-C would be through banks. Interest rate on these securities would be linked to final combined Consumer Price Index [CPI (Base: 2010=100)]. Interest rate would comprise two parts – fixed rate (1.5%) and inflation rate based on CPI and the same will be compounded in the principal on half-yearly basis and paid at the time of maturity. Early redemptions will be allowed after one year from the date of issue for senior citizens (i.e. above 65 years of age) and 3 years for all others, subject to penalty charges at the rate of 50% of the last coupon payable for early redemption. Early redemptions, however, will be made only on coupon dates.

The date of issuance for subscription would be announced shortly. The details of the product design and other operational issues are furnished in the Annex. The issuance of non-cumulative Inflation Indexed National Saving Securities for retail investors will be examined in due course.

Alpana Killawala

Principal Chief General Manager

Press Release : 2013-2014/1101”

best wishes

S S Bakshi

Sure Sir, I’ll try to cover it as soon as possible.

Thanks Shiv.

Though the interest rate is 0.10% lower than HUDCO, since it is a very long term investment (I am not eyeing for listing gain), I would go for NTPC since it is AAA rated. 🙂

Ya, probably it makes sense. I’ll make equal investment in both as I’ve never invested in HUDCO bonds before.

Very informative article. Thanks.

Thanks Hemant!

Hi Shiv, Many thanks for this very informative post again. After careful consideration decided to split my investment 60-40 in NTPC and HUDCO respectively as I have HUDCO bonds from earlier issue as well. Also I have applied for number of bonds this year it would be great if you could share a post detailing annual interest payment dates of bonds issued in last few months.

Regards

Ikjot

Sure Ikjot, I’ll do that very soon.

Hi Shiv, The interest that NTPC would pay to successful candidates on allotment, would that also be taxfree?

It would be taxable Ramprakash.

hi Shiv,

The current NtPC and Hudco tax free bonds are reasonably good offers.

Are you expecting any better or even equivalent offers in the current FY? It is difficult to predict the future. But still, what are the chances?

Hi,

IIFCL is coming out with its issue from 9th December and the coupon rates are absolutely same as that of NTPC. As interest rate movement is volatile and difficult to predict, nobody can be sure of better coupon rates in future.

High fiscal deficit and uncontrollable inflation is keeping G-Sec yields higher. Still I have a high hope that interest rates will fall in future and I’m investing my family’s money in these current issues.

what is rating for upcoming issues. we know IIFCL IS AAA. what about others like NHAI, NHB and so on.

IRFC, NHB and NHAI are also ‘AAA’ rated.

As usual great post Shiv.

Have couple of questions on bonds. If the market rate of the bond is less than issue price on maturity date(after 20 years) will the company pay the market rate or the issue price to the redeemer.Also does a buyer on listing have to pay for the accrued interest along with market price if bought from the secondary market.

Hi,

I would like to answer this query . 1) The FV and accrued interest will be paid on maturity and market price is not considered for settling on maturity. The market price will adjust to face value+ Interest accrued at the time of maturity. 2) When buying from market unlike Government securities, one will have to pay only market value for buying Tax free bonds from secondary market. The market price will have the accrued interest also factored in it. Hope I have answered your query and Shiv will help you with further if anything missed.

Thanks George for your inputs !! I would like to just reframe your answers.

Harineem, the market price of a bond must converge to its face value (or maturity value) at the time of maturity. There cannot be any difference between the two. The logic is simple – nobody would like to sell his/her bond holdings a day before the maturity date at a price of say Rs. 950, when he/she is going to get Rs. 1,000 on the maturity date.

Bondholder whose name appears in the books of the company on the Record Date gets the whole of the interest payment on the Interest Payment Date. Between two record dates, interest amount actually gets accrued and gets reflected in the market price.

Hi Shiv,

What chances of getting full allotment tomorrow ?

Hi Aditya,

I would say very very bleak chances, next to impossible.

Day 1 (December 3) subscription figures:

Category I – Rs. 423 crore as against Rs. 175 crore reserved

Category II – Rs. 1,398.83 crore as against Rs. 437.50 crore reserved

Category III – Rs. 852.85 crore as against Rs. 437.50 crore reserved

Category IV – Rs. 669.75 crore as against Rs. 700 crore reserved

Total Subscription – Rs. 3,344.43 crore as against total issue size of Rs. 1,750 crore

Bumper opening subscription for the NTPC issue, even better than the NHPC issue. No point applying for the bonds tomorrow onwards, if you want to get full allotment. It is better to apply for the HUDCO bonds now or wait for the IIFCL issue to open on 9th.

so bad ..i was about to apply.

IIFCL is opening from 9th, you can go for that.

Dear Shiv,

Applications for NTPC today (4/12/13) would get allotment of less than 5% correct ?

What are the coupan rates expected for IIFCL issue ? Is it a better company to invest for long term compared to NTPC ?

Thanks

Dear TCB,

Nobody can be sure of the percentage of allotment against today’s bidding, but it’ll not be 100% for sure.

With IIFCL, the coupon rates are absolutely same as they are with NTPC. I am not able to measure how good a company IIFCL is vis-a-vis NTPC, but it is a very good company in my view.

I read your posts with great interest. I applied for the NTPC Bonds today under the retail option. What are my chances of getting full allottment. Does the FCFS counts from the day in which the application was lodged irrespective of the time at it was lodged or from the time it was lodged on a particular day.

Hi Vinod, I am glad you find these articles interesting !!

Also, you’ll get 100% allotment as you applied for it today. Allotment on FCFS basis has nothing to do with the time the application gets submitted. The day on which the retail category gets oversubscribed matters. Like it got subscribed to the tune of Rs. 669.75 crore out of Rs. 700 crore today. Now, only Rs. 30.25 crore is left for the retail investors. Tomorrow it will get oversubscribed. If Rs. 200 crore gets invested tomorrow, then every investor will get allotment in the ratio of 30.25:200 (or 121/800).

Thank you very much for your reply, Shiv.

You are welcome Vinod !!

Hi Shiv,

I applied today under retail category.Will I get 100% allocation?

Thanks

My apologies Its Category IV not retail.

There is no difference between the retail category and Category IV.

Yes Ikjot, you’ll get 100% allotment.

Any news on when the issue closes?

OK, just read this news that it is closing tomorrow.

http://economictimes.indiatimes.com/markets/bonds/ntpcs-tax-free-bond-issue-oversubscribed-3-3-times/articleshow/26805001.cms

That’s great !!

thanks for you valuable insights! i have been following them for a while now. just missed the opportunity in ntpc and may go for the iifcl bond issue as you suggest.

was also thinking of redeeming my holding in rec bonds invested earlier at around 8.12% albeit at a small loss and increasing my investment now. what are your thoughts?? am in the 10% tax bracket.

Hi Shiv,

I also have a similar query. I am thinking about selling my HUDCO 8.39% 10 Y bonds bought few months back. I am in 30% tax bracket. Please suggest.

Hi Vipreetha and Hi DPP,

It is difficult for me to give random advice in this matter. I would require to analyse your holdings before I suggest you anything and it would fall under our paid services.

I have applied just now, hopefully I get the bonds?

I too hope so, All the Best !!

I was super confident of my allocation but after reading your comments I am…. dukhi 🙁

I applied on 3rd’Dec @ 15:48PM, what do you think my chances are?

I started reading articles on this weblog only last year, they are great, and you put in lot of stats as well. But one of your stat has disappointed me!!

I was confident of 100% allocation, but as per your stats, it seems I might not

I applied yesterday, at 15:48PM via ICICI Direct

Hi Binish,

If you are a retail investor (Category IV), then you are unnecessarily disappointed and :-(. All retail investors, who applied for it yesterday, will get 100% allotment.

yes am Retail investor, thanks for your kind words.

You are welcome!

Day 2 (December 4) subscription figures:

Category I – Rs. 423 crore as against Rs. 175 crore reserved

Category II – Rs. 1,401.66 crore as against Rs. 437.50 crore reserved

Category III – Rs. 868.38 crore as against Rs. 437.50 crore reserved

Category IV – Rs. 902.35 crore as against Rs. 700 crore reserved

Total Subscription – Rs. 3,595.39 crore as against total issue size of Rs. 1,750 crore

Retail Investors, who have applied for NTPC bonds today, should get allotment in the ratio of approximately 30.25 / 232.60 (or 1 bond for every 8 bonds applied), approximately 13% of the bonds applied.

Thanks for the information Shiv. Does the allotment process start today since the issue got closed?

Hi Hemant,

NTPC has committed to allot and list these bonds within 12 working days from the closure of the issue. So, you can expect the bonds to get allotted between December 17th to December 20th.

Hi Shiv,

I’ve applied on 4/Dec/13 and after reading your posts and comments, understand that it oversubscribed (retail category) on 4/Dec/13 and hence all the applicants on 4/Dec/13 would get partial allotment in approx. 1:8 ratio. When would I get the refund amount for non-alloted portion back into my account? Will it be only after the allocation happens (e.g. after Dec 17 – Dec 20)?

thanks,

CVS

Hi CVS,

You’ll get the refund between this period itself i.e between December 17 to December 20.

Please notify me of the followup

NTPC tax-free bonds issue is getting closed today, December 5th.

that is great, does this imply beginning of allocation process? or wait till 16thDec?

Hi Binish,

NTPC will allot and list these bonds within 12 working days from the closure of the issue. So, you can expect the bonds to get allotted between December 17th to December 20th.

thank you Shiv, I am learning every time you respond.

That’s great !! You are welcome Binish !!

Day 3 (December 5) subscription figures:

Category I – Rs. 423 crore as against Rs. 175 crore reserved

Category II – Rs. 1,403.67 crore as against Rs. 437.50 crore reserved

Category III – Rs. 895.64 crore as against Rs. 437.50 crore reserved

Category IV – Rs. 947.26 crore as against Rs. 700 crore reserved

Total Subscription – Rs. 3,669.56 crore as against total issue size of Rs. 1,750 crore

NTPC tax-free bonds issue stands closed today.

Hi Shiv

I have a question a bit unrelated to this post. I was trying to look up IFCI Infra bonds issued 2011(Manshu had done a post on same). My demat acct showed up market rate as double which is definitely wrong. When I tried to find the listing in BSE and Moneycontrol the rates are completely different(code: 972655).

Please advise how to find the market rate and are we allowed to sell these? Thanks

Hi Harineem,

Please ignore all these market prices shown by all these portals. You just cannot redeem/sell your Infra Bond investments till the lock-in period gets over i.e. 5 years from the date of allotment.

Hi Shiv,

The interest that is paid for the period between application date and allotment date, is that also tax free?

Thanks,

DPP

No DPP, it is taxable.

Hi Shiv,

I applied for NTPC bonds on 5th Dec. Any chances of getting allotment? What % allotment is likely?

In case full allotment is not possible by when can i expect the balance money to be refunded back in my account (i appliled through my Demat account)?

Thanks.

Hi SSG,

You won’t get any allotment as the NTPC issue got oversubscribed in the retail category on December 4th itself. You can expect refund amount to get credited to your bank account between December 16th and December 20th.

Thanks Shiv.

Any more good tax free bond issues expected to hit the market after 16th – 20th Dec where the refund could be invested?

IRFC, NHB and NHAI issues are expected to hit the markets in the 2nd half of December.

Hi Shiv

NTPC TFB are credited to my demat account this afternoon. That was pretty fast in 7 working days

Regards

Ramadas

That has been the case with these bonds this financial year Mr. Ramadas !! Great to know that bonds have started getting credited. I am yet to get any message from my DP.

The bonds are showing 261223 and 261233 which suggests maturity on 26th Dec. I am not sure how the interest will be paid till 26th?

hmm.. let’s see!

I just received an SMS confirming my allotment.

I’ve got my allotment as well…Very quick service from NTPC by Indian standards.

That’s Great! NTPC has no role in the allotment process, this work is handled by the Registrar, Karvy Computershare.

Thanks Shiv for the info.

You are welcome!

Congrats to all above, I know the excitement!! I too was when I received the SMS.

My only worry is RBI raising repo rate again, though am not looking for capital gains, it is disappointing to see you investment less than principle. I use TFBs to park my miniscule fund for eventual buying of house, thus I might loose some portion of my principle if they depreciate from their face value.

Dear Binish,

Your concern is valid. At the same time what is the solution? Wait for the highest rate coupon? In reality , no body can guess the bottom of the market and top as well. The one who invested in TF bonds last year are already seeing 10% loss in principal. But if you do not look at the price , you should be fine. When market interest rate was lower, you are satisfied by the rate offered by the bonds. I have started investing from the very TF bond of NHAI. I have sold few of them for gain also. I have continued subscribing to following issues also in small quantities based on fund availability. Today I have average 8.5% coupon return. If I am not planning for short term gain or urgent liquidity, this should be fine. If I need urgent money , then I have to factor the risk and sell. Basically , my personal advise is be happy where we are and no point in worrying about interest rate going up. There is also a chance for interest rate to go down in 1 year time.

Hello George,

I agree with you in letter. I had invested some amount in HUDCO TFBs last year, coupon rate is 8.51% for 20 yrs, but for those who buy them in secondary market it is 1% less, that is 7.51%. Its face value is 936 as of today, while I bought it at 1000.

Even I feel interest rates are quite high and will start falling in following year.

I got my SMS but cant see anything in demat acct .Also says 7 which is pathetic. Had better luck with Power grid got more than 50% applied.

You mean you got only 7 bonds Harineem ??

Thats what I understand from the SMS.

I think you must have applied for 50 bonds on December 4th then. Is that right ??

Absolutely right!

Great !! Allotment has been made approximately 13-14% to all the applications made on December 4th. You must have also received your refund/interest money back into your bank account.

When will these bonds get listed? It would be helpful if you could share the BSE/NSE code for the same. Also have you heard any rumors about any upcoming TFB’s?

NTPC tax-free bonds to get listed on the BSE & the NSE on December 19th i.e. Thursday.

Here are the BSE and the NSE codes for the same:

8.66% 10-year bonds – BSE Code – 961808, NSE Code – N4

8.73% 15-year bonds – BSE Code – 961809, NSE Code – N5

8.91% 20-year bonds – BSE Code – 961810, NSE Code – N6

Deemed date of allotment has been fixed as December 16, 2013. Interest will be paid on December 16th every year.

I got 137 bonds and refund.????

Sorry Hemant, I didn’t get your query.

Hi Shiv,

My query was about basis of allotment as I was not sure about it.

You already answered the same, thanks.

Hemant

Sure… Great !!

NTPC Basis of Allotment:

Category I (QIBs) – 41.37% of their 1st day subscription

Category II (NIIs) – 31.66% of their 1st day subscription

Category III (HNIs) – 56.15% of their 1st day subscription

Category IV (Retail Investors) – 100% of their 1st day subscription and 13.69% of their 2nd day subscription

Hi Shiv – If I buy these bonds from the secondary market, do I still get the tax free interest benefit? or is there some condition somewhere which reduces the post tax interest eanring to people buying NTPC bonds (or other tax free bonds) in the secondary market?

Hi Ranjit,

The interest you’ll get with NTPC bonds will remain tax free. There are no conditions attached except that your investment amount should not be more than Rs. 10 lakhs.