RBI Monetary Policy Review – Leaves Repo Rate, MSF Rate, CRR Unchanged

This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

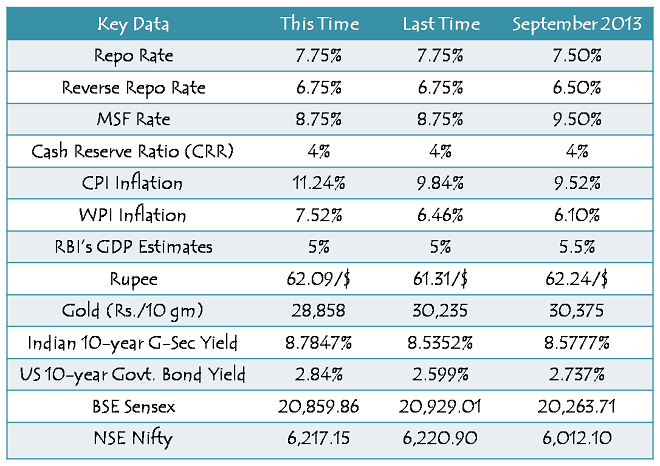

It was again a day of monetary policy announcement and with CPI inflation rising to 11.24% and WPI inflation rising to 7.52%, most of the analysts on the dalal street had already factored in at least 25 basis points or 0.25% rate hike to be a done deal.

But, contrary to market expectations, Dr. Raghuram Rajan today surprised most of us and decided not to hike the policy rates, including the Repo Rate, Marginal Standing Facility (MSF) Rate and the Cash Reserve Ratio (CRR).

He left the Repo Rate unchanged at 7.75% and the MSF Rate at 8.75% and also assured the markets about its commitment to keep the difference between these two rates at 100 basis points or 1%. It was really a pleasant surprise and gave both the equity markets as well as the debt market a much needed relief.

Why he did not hike the rates despite high inflation?

Dr. Rajan has a view that the recent unusual spike in inflation, due to unseasonal upturn in vegetable prices, is temporary in nature and the prices have already started declining in some of the metro cities, as swiftly as they had increased.

Also, as most analysts believe, a rate hike has not been a successful tool so far to anchor inflationary trends, Dr. Rajan wants to wait for more macroeconomic data to pour in before he takes his call next month.

This is what the RBI did and had to say today:

Repo Rate left unchanged at 7.75% – RBI has left the Repo Rate unchanged at 7.75%. This is the rate at which the commercial banks borrow money from the RBI for a short period of time.

Though it has been left unchanged for now, the governor has made it very clear that the central bank will not stop itself in hiking these rates quickly if the inflationary situation doesn’t improve as expected.

Reverse Repo Rate unchanged at 6.75% – As the Reverse Repo Rate is linked to the Repo Rate, it has also remained unchanged at 6.75%. This is the rate at which the banks deposit their excess money with the RBI for a short period of time.

MSF Rate unchanged at 8.75% – Marginal Standing Facility (MSF) Rate is also linked to the Repo Rate and though people were speculating that it will also be hiked by 0.25% along with the Repo Rate, the RBI has left this rate also untouched at 8.75%. This is the rate which the RBI charges to the scheduled commercial banks for the money borrowed for their overnight liquidity requirements.

Cash Reserve Ratio (CRR) unchanged at 4% – Along expected lines as always, RBI has left the CRR unchanged at 4%. After Pratip Chaudhuri, the former Chairman of SBI, now nobody asks the RBI to cut CRR from its current levels.

Note: If you want to know more about RBI’s monetary policy tools & their intended impact in detail, please visit this post – RBI’s Monetary Policy – Tools & Expected Outcomes

Impact of the Monetary Policy

Impact on stock markets – After ending in the red for six straight sessions, the stock markets today rejoiced the RBI’s decision and called it a pre-Christmas surprise gift by Dr. Rajan. Markets opened on a positive note and had a sharp spike immediately after the RBI announcement at around 11 a.m. BSE Sensex closed up 247.72 points (or 1.20%) at 20,860 and NSE Nifty closed up 78.10 points (or 1.27%) at 6,217.

Impact on debt markets – 10-year benchmark 8.83% G-Sec yield closed at 8.78%, 13 basis points lower than Tuesday’s close of 8.91%. It was again a good news for the debt fund investors as most of these schemes ended the day on a positive note.

Impact on currency – Despite a strong upmove in the markets, the rupee declined 8 paise to close at 62.09 against yesterday’s close of 62.01. Market participants were cautious to deal in the currencies markets ahead of the US FOMC meeting today.

So, after RBI’s policy decisions and market closing, this is where we stand as of today:

Though we are still facing higher and higher growth in consumer inflation in the last few months, today’s so-called ‘brave’ decision by Dr. Rajan has brought much required welcome relief for the markets. What I have been able to make out of Dr. Rajan’s policy decisions and the RBI’s commentary is that they want to give India’s economic growth a chance to recover and probably one more opportunity to the government also to take measures to curb speculative inflation.

As I finish writing this post, the US Federal Reserve has decided to start tapering quantitative easing (QE) by cutting down its bond purchases to $75 billion a month as compared to $85 billion earlier. It would be the first such step towards unwinding the stimulus that has been in place for quite a long time now.

After the Indian markets rejoiced on its central bank’s Rate hike decision, now it is the turn of the US markets to rejoice on its central bank’s QE3 tapering decision. Dow is already up 237 points in today’s trade and we should also have a rally in the Indian markets tomorrow.

As always- on time, crisp and comprehensive enough. Thanks.

Thanks Mayur for your kind words !!

Hi Shiv,

Does the unchanged rates mean that the Tax Free Bonds coming up in near future will have same interst rates as the current ones (HUDCO & IIFCL) or is there still a probability that they may offer lower/higher interest rates?

Regards,

CVS

Hi CVS,

The coupon rates of tax-free bonds are not linked to the policy rates directly, rather they are linked to the G-Sec yields (YTMs). G-Sec yields change every single day as trading happens in the bond markets. In the past 2-3 days, G-Sec yields have fallen slightly from 8.93% to 8.74%. So, if the same trend continues, upcoming bond issues will have lower coupon rates.

After the RBI decision, the market yields for the 10 / 15 / 20 year papers are falling, so will the new tax free bond issues come with lower yield?

Hi Raju,

If the market yields continue falling in the same manner in the next 5-10 days, upcoming bond issues will carry lower coupon rates.

Can a Demat a/c be opened for a minor? Can one apply for IPO/FPO/TFB in the name of a minor? Can one trade in equities in the name of a minor?

Yes Simple.

Thank You!

Can you tell the dates when the following data will be released in January- IIP, CPI, WPI, RBI Monetary policy?

NHAI Bonds will open in mid-January, yields offered will be well below 8.91%- your thoughts?

Can you also explain the relation between the US 10 yr yield and our own?

Inflation Indexed Bonds are opening from Monday, a word on that would also be welcome

Hi Simple,

RBI’s next monetary policy is due on January 28th. IIP, CPI & WPI inflation figures will get released sometime between 13th & 15th January.

I really cannot comment on NHAI coupon rates as of now.

It is not possible for me to explain the relationship between Indian bond yield and US bond yield here on this forum.

I’ll cover the Inflation Indexed Bonds with a post today.

Thanks for the answer!

Can you tell why is it not possible for you to do a post to explain the relationship between Indian bond yield and US bond yield?

Bcoz the relationship is not always directly linked. I think it is very complicated to fully understand & explain it. Most of the times they move due to certain events based on various other kind of domestic factors.

Hi Shiv!

Strides arcolab had declared a special dividend of 500/- with the record date set as 20th December. Can you explain why the stock went ex-dividend on 20th itself (Its share price fell by 60%)? Would the people who sold the share on 20th still be eligible to get the dividend? If yes, Why? If no, then why did they sell it & the stock crashed?

PS: This is not a stock specific or a personal query. This is just a general question to better understand record dates

Hi Simple,

This is due to the “T+2” settlement system that is being followed by the stock exchanges. Strides Arcolab went “Ex-Dividend” on Thursday, December 19th and its Record Date was December 20th. If you held these bonds till the end of trading hours on December 18th, then your name will be there in the records of the Registrar on December 20th i.e. the Record Date. If you sold these bonds on December 18th, you’ll not get the dividend. But, if you sold these bonds on December 19th, then you’ll get the dividend.

I have understood the T+2 part. So “Record date” is different from “Ex-dividend” date?

But then if one would still get the dividend by selling on 19th, then why didn’t the stock correct on 19th itself? Why wait till 20th & wait for the stock to go ex-dividend?

This link of NSE shows that Strides Arcolab closed up on Friday at Rs. 382.05 as against Thursday’s closing price of Rs. 373.75

http://www.nseindia.com/live_market/dynaContent/live_watch/get_quote/GetQuote.jsp?symbol=STAR&illiquid=0

It corrected on 19th itself.

Dear Mr. Kukreja, if it is possible for you to integrate a search box on to this site, it would be extremely beneficial to all visitors; and also possibly reduce the burden on you in having to answer the same question many times.

Thanks for all the work you are doing to enable investor education.

Thanks Mr. Rama for your kind words !!

Also, I’ll discuss your suggestion with Manshu once and let’s see if we can do something about it. Thanks for such an input!

Could you cover an article/ comments on EIL FPO opening tomorrow?

Hi SB,

It has been posted now, please check:

https://www.onemint.com/2014/02/06/engineers-india-limited-eil-fpo-rs-145-150-february-2014/