This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

National Housing Bank (NHB), a wholly-owned subsidiary of the Reserve Bank of India (RBI) and the regulator of the housing finance companies (HFCs) in India, will be coming out with its issue of tax free bonds from the coming Monday, 30th of December.

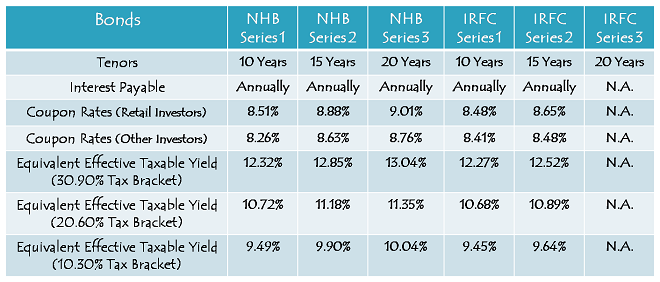

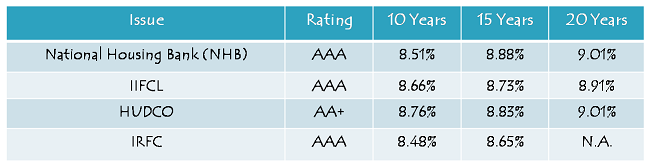

The good news is that the company is going to offer 9.01% per annum for the 20-year option and 8.88% per annum for the 15-year option, which is the highest rate of interest any ‘AAA’ rated issue has carried till date.

Though the issue is scheduled to remain open for the whole of next month to close on January 31st, 2014, the company reserves the right to close it earlier as well in case the issue gets oversubscribed anytime before the due date.

Size of the Issue – NHB is authorised to issue tax free bonds worth Rs. 3,000 crore this financial year, out of which it has already raised Rs. 900 crore through a private placement carried out on August 30th, 2013. NHB plans to raise the remaining Rs. 2,100 crore from this issue, including the green-shoe option to retain oversubscription to the tune of Rs. 1,100 crore.

Rating of the Issue – Being the regulator of the housing finance companies and a wholly-owned subsidiary of the RBI, this issue of NHB has been rated as ‘AAA’ by three credit rating agencies, CRISIL, CARE and ICRA, which is the highest rating by these rating agencies.

Interest Rates on Offer – The company has decided to offer 9.01% p.a. with the 20-year bonds, 8.88% p.a. with the 15-year bonds and 8.51% p.a. with the 10-year bonds. HUDCO is currently offering 9.01% p.a. for 20 years, 8.83% p.a. for 15 years and 8.76% p.a. for 10 years, but that is a ‘AA+’ rated issue. At 9.01% and 8.88%, NHB issue has become the best AAA rated issue for the 20-year and 15-year duration respectively.

If you want to have only AAA rated bonds in your portfolio and do not have more than 10 year investment horizon, then you can still subscribe to the IIFCL bonds which carry 8.66% p.a. interest rate for 10 years.

Investor Categories & Allocation Ratio – The investors have been classified in the following four categories and each category will have certain percentage of the issue size reserved during the allocation process:

Category I – Qualified Institutional Bidders (QIBs) – 10% of the issue i.e. Rs. 210 crore is reserved

Category II – Non-Institutional Investors (NIIs) – 25% of the issue i.e. Rs. 525 crore is reserved

Category III – High Net Worth Individuals including HUFs – 25% of the issue i.e. Rs. 525 crore is reserved

Category IV – Resident Indian Individuals including HUFs – 40% of the issue i.e. Rs. 840 crore is reserved

NRI Investment – Non-Resident Indians (NRIs) and Qualified Foreign Investors (QFIs) are not eligible to invest in this issue.

Allotment on First Come First Served Basis – Subject to the allocation ratio, allotment will be made on a first come first serve (FCFS) basis in each of the investor categories, based on the date of upload of each application into the electronic system of the stock exchanges.

Lock-in Period, Premature Redemption & Listing – There is no lock-in period with these bonds, but at the same time, you cannot redeem these bonds back to the company before their maturity period gets over. In order to encash your investment before maturity, you’ll have to compulsorily sell these bonds on the stock exchange(s) where they have been listed for trading.

The company has decided to get these bonds listed only on the National Stock Exchange (NSE) and has got the necessary in-principle listing approval for the same on December 20, 2013. The company will get these bonds allotted and listed within 12 working days from the closing date of the issue.

Demat/Physical Option – Though it is mandatory to have a demat account to sell/trade these bonds, you can subscribe to them in physical/certificate form as well and keep them till maturity. Interest will still get credited to your respective bank accounts through ECS.

Interest on Application Money & Refund – NHB will pay interest to the successful allottees on their application money, from the date of realization of application money up to one day prior to the deemed date of allotment, at the applicable coupon rates. Unsuccessful allottees will get interest @ 5% per annum on their refund money.

Face Value of the bonds & Minimum Investment – NHB is the first company this financial year to keep the face value of its bonds as Rs. 5,000 instead of Rs. 1,000. Considering its face value and minimum application size of one bond, an investor is required to invest at least Rs. 5,000 in this issue.

Interest Payment Date – NHB has not fixed its interest payment date as yet and the first due interest will be paid exactly one year after the deemed date of allotment. As the deemed date of allotment will be fixed once the issue gets closed and before the bonds get listed, I will update this post as and when it gets announced.

Should you invest in this issue?

I would say that one should definitely invest in this issue and I have many reasons to justify my view. Here are some of those reasons:

First, NHB issue is ‘AAA’ rated.

Second, you are going to get 9.01% p.a. and 8.88% p.a. coupon rates which are the best 20-year and 15-year rates offered by any AAA rated or AA+ rated issuer till date.

Third, NHB is a wholly-owned subsidiary of the RBI and I don’t foresee the RBI to ever let its subsidiary default on any such bond issue. Also, NHB is the regulator of the housing finance companies, like RBI is for the banks and SEBI is for the capital markets. I don’t think any government would allow any regulator to default on its payments.

Fourth, it is almost certain that the CPI inflation will start falling from next month onwards. If that materialises, we might have G-Sec yields falling quite sharply.

Fifth, IRFC is the next company to launch its tax-free bonds from January 6 and its coupon rates are lower than that of NHB at 8.48% p.a. for 10 years and 8.65% p.a. for 15 years. It is not going to issue these bonds for 20 years either.

Sixth, there are very few good companies left now to issue tax-free bonds this financial year. REC, PFC, NHPC and NTPC have already raised their quota of authorised amount from the markets. HUDCO is also very close to reach its targeted amount. Only IIFCL, NHAI, IREDA, Airport Authority of India (AAI), Ennore Port and Cochin Ship Yard are now left to issue these bonds and their issue sizes are also very small, except NHAI and IIFCL.

Seventh, it is still not certain whether tax-free bonds would see the light of the day next financial year onwards or not. Like 80CCF infrastructure bonds got stopped getting issued from FY 2012-13 onwards, it is possible that the next government decides to stop extending this budgetary support to all such companies.

Eighth, NTPC issue got listed a few days back and that too at a premium. If an issue with coupon rates lower than the NHB issue can trade at a premium, then it is almost certain that these NHB bonds would also trade at a premium on listing.

Ninth, NHB has reasonably strong fundamentals. It reported profit after tax (PAT) of Rs. 450 crore with total income of Rs. 3,030 crore for the period ended June 30, 2013 as against Rs. 387 crore and Rs. 2,492 crore respectively for the period ended June 30, 2012. Its net interest margin (NIM) also improved to 2.25% during this period as against 2.20% last year.

NHB’s asset quality has also been remarkable. Gross NPAs and Net NPAs remained quite close to zero for the periods ended June 30, 2011 and June 30, 2012. Though its gross NPAs and Net NPAs have jumped to 0.53% and 0.45% respectively in the latest period ending June 30, 2013, this relative poor performance was due to one large project exposure slipping into the NPA category. This large account was worth Rs. 179.60 crore out of its total NPAs of Rs. 180.62 crore.

Why you should not invest in this issue?

If I myself decide not to invest in this issue, I would have only one valid reason for that, higher expected coupon rates in the forthcoming issues. If any of you think that the rates would be higher with NHAI bonds or IIFCL tranche III bonds, then you can probably skip this issue. Personally, I would invest my family’s money in this issue and would also advise my clients to do that.

Application Form of NHB Tax Free Bonds

NHB Tax-Free Bonds – Bidding Centres

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in NHB tax-free bonds, you can contact me at +919811797407

Whats the latest on retail subscription guys ? 🙂

It is already crossed Rs 934 cr and still climbing (ie more time left).

1.16 times as of 4:00 p.m. 975 crores against 840 crores

To be precise, it is Rs 981 cr at 4 pm.

This must be some sort of history that this TFB issue is creating !!!!

Shiv – just to get a perspective, if retail is say 1000 Cr today EOD, approximately what % allotment can we expect ?

The retail subscription crossed 900 crores. By 5 O clock it is likely to touch 1000 crore as Shiv mentioned.

At 3:30 p.m., issue has been subscribed thrice the base limit and fully subscribed in individual categories as well and that too upto the proportionate shelf limit in each (total=2100 crores). It seems sure that none will get the full allotment of application.However, feeling good for the time being that let go very prompting issues such as PFC, then NHPC and NTPC. Finally have put in good share of portfolio in this issue under retail for 20 years.

That’s great Jasbir !!

Retail will be oversubscribed today itself. It is already 95% subscribed. It should end up 105%-110% oversubscription for retail going by the pace of subscription by end of today. I cant believe 800 crore of retail money is available to be raised in a day. This is no doubt the best TFB till date.

For those who applied today will have to settle for 90-95% allotment. Let us wait for final subscription numbers by end of the day

Regards

Ramadas

It should be more than Rs. 1000 crore in the retail category.

Shiv, I would expect it to be 900 crore. If Sam is still having a look at this forum. I want him to know that all the comments here are based on better understanding of TF market and merit of bonds issued. The forum helps in getting info in time and not losing opportunities. You can always have 2 opinions on one subject. But the one who invests will have to take final call based on the opportunity available and what he is comfortable with. No one takes financial decisions based on one recommendation. Continue to debate for and against without finger pointing.

It is already crossed Rs 934 cr and still climbing (ie more time left).

Crossed 1000 crore. Expect 70-75% allotment in retail.

I agree with you George !!

Retail Investors Category is subscribed by Rs. 729 crore by 2:30 p.m. Only Rs. 111 crore left.

Hi George,

Allotment will be made on a proportionate basis if the issue gets oversubscribed on the 1st day itself.

Oversubscribed as in the whole issue or the category-wise ? Meaning if the other categories and the issue is oversubscribed today but retail is not subscribed 100 % , then all the retails applications today get 100% allotment right ?

Yes, that’s right. But, it looks like that the retail investors category will also get oversubscribed today itself.

Right now it crossed 100% for over all subscription. Retail is at 1.1 Million bonds and it can go upto 1.68 Million. Considering that we have another 3 hours , this should be achieved and I think all those retail investors applying today will get 100%. Once again the issue is getting closed on merit and not because of the publicity. Shiv and this forum was correct in assuming that the issue will have high interest. Getting 2100 crore investment in a day is not a joke.

That is right.

May be the retail guys who has already put money here should do some prayers so that the retail portion doesn’t get oversubscribed by today itself 🙂

Even if it gets oversubscribed, it will be few percentage above subscription level. Retail investor will still get anywhere between 95 & 100%. Let more people participate , even if we get few bonds less.

Thanks for the clarification. The retail subscription is currently at 1.3 Million bonds and the maximum retail is 1.68 Million. We have another 2.5 hours and I feel 100% subscription today itself and all those applied today is likely to get 100%. Though it reached 100%, issue might close tomorrow.

Thank you all for sharing the info.

I will join the prayer for 100% allocation for those applied on the 1st day (today)!

Is there a way to know what is the distribution amongst 10/15/20 year bonds under retail category?

Here is the link to check the distribution Amlan:

http://www.nseindia.com/marketinfo/ipochart/debt_ipochart.jsp?issue=NHBTF14&ir=I&cn=c&sd=D&cnlink=N

Hi, I am just curious to know, how this information will be useful.

Those who wanted higher coupons and waiting for future issues, the NHB issue will mostly close before the end of day. It already surpassed the maximum limit and retail investors still have a chance in next 1 hour for 100% allotment.

The issue is getting huge response and is already oversubscribed. The retail portion is still open (ie Rs 500 cr collected compared to the reserved value of Rs 840 cr), but the same may also get over by today itself.

Thanks Raju for the info !!

Thanks Shiv for the excellent article. NHB interest rates was a very pleasant surprise for me especially when IRFC rates were known. I do think this will be the best interest rate for AAA TFB paper in this FY.

This issue should get fully subscribed by tomorrow evening. It will be interesting to see if withdrawals are seen in IIFCL and HUDCO susbscription to apply for NHB.

Regards

Ramadas

Ya, let’s see how this issue goes. I have observed that the investors normally don’t withdraw their applications in a large number after they submit it. It would be interesting to see what happens with these issues.

Hi Shiv,

For tax free bonds, what is the criteria for High Net Worth Individuals ? If I invest 1 lakh will I be treated as HNI and get lower returns? I am new to this investing world.. Sorry if my question sounds silly.

Hi Praveen,

Individual investors who invest more than Rs. 10 lakhs in tax free bonds are categorised as High Net Worth Individuals (HNIs). Nothing silly here, we all learn like that only.

Dear Shiv,

Tax-free bonds of NTPC are quoting below those of NHPC & even PFC. Is it due to later allotment date of NTPC (and therefore lower interest component in the price) or due to some other reason ?

Is it advisable sell NTPC, NHPC & PFC bonds to invest in NHB, considering long-term investment ?

Thanks

Dear Shiv,

Please consider fundamentals of the issuer also, in addition to other relevant points, while answering my second question above.

Thanks

Dear TCB,

Yes, it is due to the accrued interest which is attached to their prices. Also, demand is more for the NHPC & NTPC bonds as compared to the PFC bonds. So, that is also one more reason.

I would not like to take a call on your second query. Personally, I sold my family’s NHPC bonds within 5-10 days after they got listed between Rs. 1,016 & Rs. 1,028. I am going to invest that money in the NHB Bonds now.

Hey Shiv,

I have a question. If a person applies for this bond, and within few months becomes an NRI. Then can he still redeem this bond upto maturity, or sell in secondary markets.

I understand that once a person becomes NRI, he may at his will later, need to convert his bank accounts to NRI accounts, so how will the demat portfolio be affected?

The reason I am asking above is, this bond is not for NRIs, however I may be an NRI in future, and get my demat account modified with NRI option.

Suggestions/Comments welcome

Hi Prash,

Even I am not sure about it. The government allows PPF accountholders, who subsequently become NRIs, to continue their investments till it matures. But no such guidelines are there for these bonds.

But, one thing is for sure, it is mandatory to convert your bank account(s) to NRO bank accounts and your resident demat account has to be mandatorily closed and a new demat account has to be opened with NRI status. If somebody is expecting to become NRI in the near future, then I think it is probably better to apply for these bonds in physical form.

If somebody has any more info, please share it share.

Please check on this. You need not close the Resident Demat account. The same need to be linked to NRO account.

You need to close it George and open a fresh NRO demat account. You also need to open a PINS account for your investments from abroad.

http://www.moneycontrol.com/news/nri-experts/you-cannot-transfer-sharesyour-old-demat-tonew_215441.html

Hi Shiv,

Exactly a similar question here. What are the problems expected if one applies through a resident demat account and later the status of the applicant changes to NRI (and assuming the demat account continues to be domestic and not converted to non-resident)?

Do you expect any problems in the interim or at the time of redemption?

Shiv

Keep up the good work irrespective of way ward comments from smart alecs

Sure Brian, thanks !!

My first exposure and very informative indeed. Certainly facilitates decision – making.

Personally I was happy to read the dissenting views as well . Only if we can avoid getting personal please.

You are welcome Abhay to visit this site regularly and subscribe to our free newsletter !!

@Sam. Sam , as Rohit said, we all here have one goal as how to make our money work harder. So, let us all benefit each other by our collective views and info. We wouldn’t like an informed reader/contributor leaving this blog and I guess Shiv too won’t mind you staying here. So let us all use our time wisely and keep making this blog more valuable, and please keep posting.

I apply for the bonds jointly with my wife who is 64 years old. Keeping our age in view, we have so far only applied for bonds with 10 years duration. We are now tempted to apply for NHB bonds for a duration of 15 years. There is a view that one can apply for a longer duration because one can always liquidate the bonds in the market. My experience is that the liquidity is very limited and it may be difficult to sell the bonds in the open market. Should we therefore stick with 10 years or go in for 15 years this time.

Hello Mr. Vinod,

I think NHB bonds will have higher liquidity for either 20 years duration or 15 years duration. So, I would say you should go for one of these options.

Thank you very much for your prompt reply.

I urge all readers to appreciate the fact that Shiv is doing a great job in providing us with valuable inputs . I have had the opportunity to interact with many wealth managers and I can say that Shiv is any day more knowledgeable than then. We are all mature people and it is for us to take or leave his advice.

Thanks a lot Sir for your kind and motivating words !!

Hi Shiv,

Very good detailed analysis.

If you were to choose either of 15 yr or 20 yr, for capital gain + liquidity (after waiting for interest rates to fall ), which one is better ?

Thanks Inder for your kind words!

Personally, I would opt for the 20 year option, rest its your personal choice which one suits you better.

will interest be more in upcoming bonds ? and why do you say liquidity is more for 20 yrs bonds.

I have no idea what would be the rates in the upcoming bond issues Pradeep. Also, I never said that I am sure liquidity would be higher with the 20 year bonds. I just said I would prefer the 20 year bonds overall.

thanks sir. happy new year to you and family 🙂 😀

Thanks and same to you Pradeep !!

i am not a genius like you Sam , nothing close to Shiv , but still i can make out

why i should not buy REC 8.71% on monday even if it trade at 990 … reason behind if i am getting 9.01 i.e 0.30 % per year higher then 8.71 = 6 % lesser in 20 years. i can buy REC at 940 to match up with NHB . instead of arguments & blaming each other why not help each

other with own views … there is no compulsion to accept views of any reader or views of Shiv. we are all on same boat and want best returns on our hard earned money … so instead of fighting start thanking each other for encouragement of one & all.

Absolutely, there is no compulsion to accept my views or any reader’s views out here. In fact, I avoid giving advice here and would like to provide only general info.

I agree with you Rohit that there is no point going for bonds trading in the secondary markets until the yield is far superior than the new bonds on offer.

hello sam .

can you guide the viewers which bonds are already listed at prices far lower than their issue price. ? i want to buy on monday instead of applying to NHB 9.1 %

You , the Viewers and Mr Shiv all on same boat & want to find our best options available in mkt

REC 8.71%. Its interest is paid on 1st Dec. Its trading at 996. Assuming a 10 lac application, interest cost is 238/- per day. It should trade at 1006. That is a 10 rupee discount per bond. You can get it at 990, just be patient

Can you please let Rohit and all of us know what is its current yield to maturity at Rs. 996 Mr. Sam ??

YTM % at LTP of REC is 8.8. No need to act smart, both the exchanges do the job of informing the investors perfectly well. Do you want the link to those as well?

But I don’t misguide people like you do just to earn a commission. Nothing wrong with earning money, but the way you do it is reprehensible

Grow up Mr. Shiv Kukreja and learn a little humility as well. I will not indulge in these puerile exchanges with you any further

hahaha… I have all the links Sam and probably more than you. I just wanted to check how much you know. So, you want people to go for 8.8% yield and pay 1% brokerage on that ??

I am not acting smart and I am what I am, you need not tell me what to learn and what not. I don’t need to learn anything from you. It is bcoz of people like you, this advisory business has become a mess.

I still didn’t get it. Why are you suggesting to buy REC 8.71% whose YTM is 8.8% v/s buying NHB whose coupon is 9.01%.

Sam – Please just state facts and not opinions on someone you don’t know fully.

Try buying 1 lakh worth of bonds from the markets. The price will shoot off immediately. I agree Shiv and all of us infact have been wrong and that interest rates have gone up. But I don’t regret my investments made in tax free bond last year. With hindsight I could have waited for 9% but who knew that two or one year back. I will continue to invest in tax-free bonds.

Stop bragging that your father holds a “high post”. The US Fed “high post” economists could not see the subprime housing meltdown. Economy is not a complete science.

Leave it Bhaskar, there is no point arguing with such people. They come to destroy a beautiful world and then just vanish. He advises people to buy a bond which is yielding 8.8% and pay brokerage of 0.5-1% and blames others to misguide investors here.

I agree with you that we have been wrong in predicting the interest rates, inflation, CAD & Fiscal Deficit but nobody has been able to either, neither our Finance Minister nor the RBI Governors. We are nothing in front of them. We can only hope it falls as soon as possible. How can Sam or anybody else in this world predict what would be the inflation or G-Sec yield 3 months, 6 months, 2 years, 5 years down the line.

These people have nothing to do but to mentally disturb others.

You have been consistently wrong in predicting the yields of the various tax free bonds. When REC launched its issue with the 20yr yield @ 8.71%, you proudly claimed that this will be the highest this year (you can read your own posts for reference, in case you have forgotten).

Then PFC issued its 20yr @ 8.91% and again you said it will be the highest. You were proved wrong again as NTPC came out with its issue. Although the yield was the same, yet the company was far superior as evidenced from the fact that the bond got fully subscribed in less than 2 days.

Now again you have gone to town claiming that this is the best ever & have even gone to the extent of giving it a 9 star recommendation!

Point 4 mentioned by you is completely wrong & very misguiding to viewers. While it is a given that CPI will fall, but by how much do you expect it to fall? Even the most optimistic person wont expect it to fall by more than 100-150bps. The G-sec is at 8.88. That is a very very big difference between the CPI & G-sec. Don’t forget that this fall in CPI will be just a temporary phenomenon just as the spike was temporary (due to cyclones hitting the east coast). CPI has shown no signs of relenting otherwise.

Point 7 is again fear mongering and very very presumptuous. With GDP well below 5%, it would take a very brave govt to ban tax free bonds. Some may argue that banning the 80 CCF, is also a contributing factor to the mess we find ourselves in

While I don’t have a problem with you being repeatedly wrong, my only advice to you will be to stop making wildly inaccurate guesses and assumptions. A lot of people must have blindly followed your advice and got trapped in the above mentioned issues. Thankfully I am not one of them. All the bonds mentioned above are trading in the red (even after factoring in the interest premium that builds up over time).

You owe an apology to all the viewers of this forum

The US yields have touched 3 & as QE tapering intensifies, you will see a flight of capital from the debt market. It is inevitable. You will see higher yields on upcoming bond issues, you can mark my words. The bond issues will not stop, neither will CPI soften.

I am not going to apply in these bonds either, as I expect better yields & will look to buy the bonds which have already listed at prices far lower than their issue price.

To anyone interested, my father is an economist and holds a very high post. Most of the above are his views and I fully agree. Sound counter arguments and criticism is welcome

Hi Sam,

You are talking rubbish here as I never claimed that REC 8.71% rates would be the highest this year. Here is the link, you can very well check it: http://www.onemint.com/2013/08/28/rec-8-71-tax-free-bonds-issue-august-2013/

I claimed it for PFC 8.92% and the rate were higher than NTPC’s 8.91%, despite of the fact I was actually wrong in my assessment. As incorrectly stated by you, how can you claim that NTPC issue was far superior than PFC? Just go and check the market prices of these bonds – PFC 8.92% bonds closed today at Rs. 1009.75 and NTPC 8.91% bonds closed at Rs. 1,005. So, which is better?? There was huge demand for NTPC bonds bcoz it was the first such issue from NTPC and the issue size was smaller.

I did not come to your place and claimed that NHB issue is the best one and I never claimed that I am giving it 9-stars. I just used 9 points to express my views.

Can you tell me precisely what would be the CPI inflation next month or two years later ??? If you think that CPI inflation will go higher & higher, then why don’t you invest in IINSS ?? All your thoughts above are laughable. I don’t know why I’m responding to you, but I don’t want to listen to your rubbish claims. I am writing to the best of my abilities and very very honestly. I don’t care who you are, I’ll do what I want and you’ve no right to stop me from that.

Have nothing but pity for people like you. “I don’t care who you are, I’ll do what I want and you’ve no right to stop me from that”… you sound like a teenager going through puberty rather than a sensible analyst.

I will respond to 1 point only in the utter trash that you have just posted, PFC listed on 16th November, and if you factor in the interest cost of 244/- per day (8.92% for 10 lacs), it should trade at 1010. That is a loss of 5 rupees per bond.

hahaha… ok.. this makes NTPC issue “far superior” and NTPC issue does not earn any interest which should be added to its price ?? That’s great, thanks for your inputs Sam, I am really grateful to you that you enlightened me !!

I would advice you to read the balance sheets of PFC & NTPC before commenting. NTPC is the biggest power producer of this country. Or do you think since PFC share price is at 163 & NTPC share price is 137, that makes PFC superior

I reviewed PFC and NHPC bonds and had a view that NHPC bonds were better. Then, I had a view, between NHPC and NTPC, NTPC is a bigger and fundamentally better company. It automatically means NTPC is a better company to invest. I know how to analyse balance sheets and income statements and don’t require your inputs to understand which company is better.

Sam, you yourself mentioned that these are not your opinion and belongs to your father holding a big position. As you know , the PM , FM , RBI Governor, PC Chairman all are renowned economists and not able to predict the economic situation properly. You have commented on the recommendation points by Shiv in this forum which is managed by him. As I understand , Shiv is not an economist and came up with opinion based on his experience and past data as a financial advisor for small investors. Last year this bond were sold initially at 7.5 and Shiv’s blog mentioned that is the best rate offered in the given condition. Some came with further high coupon rates and later on there was bonds which came with less than 7% coupon rates. All of them listed with premium later though the retail bonds had 50 basis points higher. Until August this year also the bond market was at 7 % level and suddenly based on situation of Inflation, fiscal deficit and CAD the rupee went down and the bond coupon rates went higher. Even if the bond goes to 10% or 11% , there is no guarantee that TF bonds will come with high interest rates. You can ignore the recommendations of Shiv and I do not see any reason why he should apologize. I have also learnt economics and track the global economic situation closely. No one is denying the situation of Fed tapering , US Bonds interest rate going up etc. Much will depend on how Indian economic situation and Inflation is going to be. No one can fully and correctly predict the future. Those who are looking for long term benefit from TF bonds, based on current IT rules in India. This is good opportunity. There is no reasons to believe any good TF bonds coming this year other than NHAI which did not reveal the interest rate. We do not know what stand the next government will have on having new TF bonds. There is no free lunch available, all investments carry their own risk. There is nothing wrong in having a contrary view as you have mentioned and I appreciate your view. But , time will tell how the economic plays out. If your view holds Good, investors will have to wait for investing in equity also.

Thank you for your reply & understanding. I will just like to clarify regarding your free lunch comment. These bonds are not issued for us retail guys, for our benefit. These are offered as tax breaks by the govt to these companies to spur the economy. We are the unintended beneficiaries of this process

To your point regarding the Govt initiating the TF bonds is well known to everyone. It gives opportunity for people to save on tax. Taking the benefit of the situation and helping in nation building both are part of the citizen. There are many investments sites and in this forum Shiv is trying to bring info to those who are not well updated about the opportunities. He is not charging for all this service. Please do not discourage him and the people who are in this forum. All are matured enough to understand the basic finance. Have constructive criticism rather than indulging in I know better attitude and pushing some one who is only trying to share info to an audience who is interested in it.

Absolutely, I agree with all your points George !!

You have mentioned some very interesting points Sam. Hope you stay on this forum.

Hi Shiv,

Leave this Sam alone. It seems he is here just to get some free publicity (ie see his boasting that his “father is an economist and holds a very high post”).

Regards,

Which form I should download NHB 13-14 (23/12196 – 36) or 13-14(01/121) ? I am in Bangalore, where can I submit the form for bidding in south Bangalore Jayanagar/JP Nagar? What documents do we need to attach with the form?

You can download any form, it doesn’t make any difference. You can mail me the duly filled form for bidding on my email id – skukreja@investitude.co.in

You need to attach the following documents for submission:

* Self-attested PAN card copy

* Self-attested Address Proof copy

* 2 Cheques – 1 Investment Cheque and 1 Cancelled Cheque

Hi Shiv!

My broker has never asked me to submit these documents with my form. Can you kindly clarify?

Hi Simple,

If you applied for these bonds in physical form, then these docs are mandatory to be submitted along with your application form.