This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

National Housing Bank (NHB), a wholly-owned subsidiary of the Reserve Bank of India (RBI) and the regulator of the housing finance companies (HFCs) in India, will be coming out with its issue of tax free bonds from the coming Monday, 30th of December.

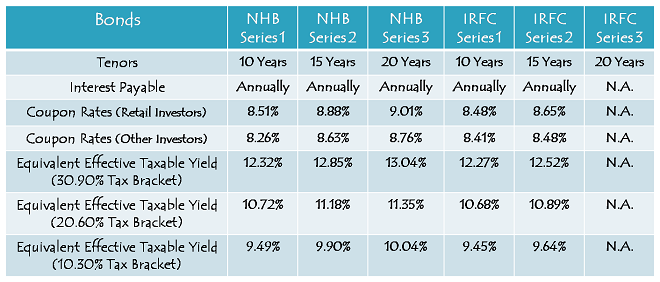

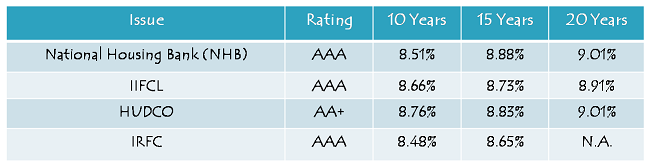

The good news is that the company is going to offer 9.01% per annum for the 20-year option and 8.88% per annum for the 15-year option, which is the highest rate of interest any ‘AAA’ rated issue has carried till date.

Though the issue is scheduled to remain open for the whole of next month to close on January 31st, 2014, the company reserves the right to close it earlier as well in case the issue gets oversubscribed anytime before the due date.

Size of the Issue – NHB is authorised to issue tax free bonds worth Rs. 3,000 crore this financial year, out of which it has already raised Rs. 900 crore through a private placement carried out on August 30th, 2013. NHB plans to raise the remaining Rs. 2,100 crore from this issue, including the green-shoe option to retain oversubscription to the tune of Rs. 1,100 crore.

Rating of the Issue – Being the regulator of the housing finance companies and a wholly-owned subsidiary of the RBI, this issue of NHB has been rated as ‘AAA’ by three credit rating agencies, CRISIL, CARE and ICRA, which is the highest rating by these rating agencies.

Interest Rates on Offer – The company has decided to offer 9.01% p.a. with the 20-year bonds, 8.88% p.a. with the 15-year bonds and 8.51% p.a. with the 10-year bonds. HUDCO is currently offering 9.01% p.a. for 20 years, 8.83% p.a. for 15 years and 8.76% p.a. for 10 years, but that is a ‘AA+’ rated issue. At 9.01% and 8.88%, NHB issue has become the best AAA rated issue for the 20-year and 15-year duration respectively.

If you want to have only AAA rated bonds in your portfolio and do not have more than 10 year investment horizon, then you can still subscribe to the IIFCL bonds which carry 8.66% p.a. interest rate for 10 years.

Investor Categories & Allocation Ratio – The investors have been classified in the following four categories and each category will have certain percentage of the issue size reserved during the allocation process:

Category I – Qualified Institutional Bidders (QIBs) – 10% of the issue i.e. Rs. 210 crore is reserved

Category II – Non-Institutional Investors (NIIs) – 25% of the issue i.e. Rs. 525 crore is reserved

Category III – High Net Worth Individuals including HUFs – 25% of the issue i.e. Rs. 525 crore is reserved

Category IV – Resident Indian Individuals including HUFs – 40% of the issue i.e. Rs. 840 crore is reserved

NRI Investment – Non-Resident Indians (NRIs) and Qualified Foreign Investors (QFIs) are not eligible to invest in this issue.

Allotment on First Come First Served Basis – Subject to the allocation ratio, allotment will be made on a first come first serve (FCFS) basis in each of the investor categories, based on the date of upload of each application into the electronic system of the stock exchanges.

Lock-in Period, Premature Redemption & Listing – There is no lock-in period with these bonds, but at the same time, you cannot redeem these bonds back to the company before their maturity period gets over. In order to encash your investment before maturity, you’ll have to compulsorily sell these bonds on the stock exchange(s) where they have been listed for trading.

The company has decided to get these bonds listed only on the National Stock Exchange (NSE) and has got the necessary in-principle listing approval for the same on December 20, 2013. The company will get these bonds allotted and listed within 12 working days from the closing date of the issue.

Demat/Physical Option – Though it is mandatory to have a demat account to sell/trade these bonds, you can subscribe to them in physical/certificate form as well and keep them till maturity. Interest will still get credited to your respective bank accounts through ECS.

Interest on Application Money & Refund – NHB will pay interest to the successful allottees on their application money, from the date of realization of application money up to one day prior to the deemed date of allotment, at the applicable coupon rates. Unsuccessful allottees will get interest @ 5% per annum on their refund money.

Face Value of the bonds & Minimum Investment – NHB is the first company this financial year to keep the face value of its bonds as Rs. 5,000 instead of Rs. 1,000. Considering its face value and minimum application size of one bond, an investor is required to invest at least Rs. 5,000 in this issue.

Interest Payment Date – NHB has not fixed its interest payment date as yet and the first due interest will be paid exactly one year after the deemed date of allotment. As the deemed date of allotment will be fixed once the issue gets closed and before the bonds get listed, I will update this post as and when it gets announced.

Should you invest in this issue?

I would say that one should definitely invest in this issue and I have many reasons to justify my view. Here are some of those reasons:

First, NHB issue is ‘AAA’ rated.

Second, you are going to get 9.01% p.a. and 8.88% p.a. coupon rates which are the best 20-year and 15-year rates offered by any AAA rated or AA+ rated issuer till date.

Third, NHB is a wholly-owned subsidiary of the RBI and I don’t foresee the RBI to ever let its subsidiary default on any such bond issue. Also, NHB is the regulator of the housing finance companies, like RBI is for the banks and SEBI is for the capital markets. I don’t think any government would allow any regulator to default on its payments.

Fourth, it is almost certain that the CPI inflation will start falling from next month onwards. If that materialises, we might have G-Sec yields falling quite sharply.

Fifth, IRFC is the next company to launch its tax-free bonds from January 6 and its coupon rates are lower than that of NHB at 8.48% p.a. for 10 years and 8.65% p.a. for 15 years. It is not going to issue these bonds for 20 years either.

Sixth, there are very few good companies left now to issue tax-free bonds this financial year. REC, PFC, NHPC and NTPC have already raised their quota of authorised amount from the markets. HUDCO is also very close to reach its targeted amount. Only IIFCL, NHAI, IREDA, Airport Authority of India (AAI), Ennore Port and Cochin Ship Yard are now left to issue these bonds and their issue sizes are also very small, except NHAI and IIFCL.

Seventh, it is still not certain whether tax-free bonds would see the light of the day next financial year onwards or not. Like 80CCF infrastructure bonds got stopped getting issued from FY 2012-13 onwards, it is possible that the next government decides to stop extending this budgetary support to all such companies.

Eighth, NTPC issue got listed a few days back and that too at a premium. If an issue with coupon rates lower than the NHB issue can trade at a premium, then it is almost certain that these NHB bonds would also trade at a premium on listing.

Ninth, NHB has reasonably strong fundamentals. It reported profit after tax (PAT) of Rs. 450 crore with total income of Rs. 3,030 crore for the period ended June 30, 2013 as against Rs. 387 crore and Rs. 2,492 crore respectively for the period ended June 30, 2012. Its net interest margin (NIM) also improved to 2.25% during this period as against 2.20% last year.

NHB’s asset quality has also been remarkable. Gross NPAs and Net NPAs remained quite close to zero for the periods ended June 30, 2011 and June 30, 2012. Though its gross NPAs and Net NPAs have jumped to 0.53% and 0.45% respectively in the latest period ending June 30, 2013, this relative poor performance was due to one large project exposure slipping into the NPA category. This large account was worth Rs. 179.60 crore out of its total NPAs of Rs. 180.62 crore.

Why you should not invest in this issue?

If I myself decide not to invest in this issue, I would have only one valid reason for that, higher expected coupon rates in the forthcoming issues. If any of you think that the rates would be higher with NHAI bonds or IIFCL tranche III bonds, then you can probably skip this issue. Personally, I would invest my family’s money in this issue and would also advise my clients to do that.

Application Form of NHB Tax Free Bonds

NHB Tax-Free Bonds – Bidding Centres

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in NHB tax-free bonds, you can contact me at +919811797407

Day 3 (January 1) subscription figures:

Category I – Rs. 575 crore as against Rs. 210 crore reserved

Category II – Rs. 1,462.86 crore as against Rs. 525 crore reserved

Category III – Rs. 1,198.35 crore as against Rs. 525 crore reserved

Category IV – Rs. 1,231.40 crore as against Rs. 840 crore reserved

Total Subscription – Rs. 4,467.62 crore as against total issue size of Rs. 2,100 crore

NHB issue stands closed today.

Hi Shiv,

Wish you and your family a very happy and prosperous new year !! one of my biggest achievements in 2013 was discovering OneMint and all of these informative and useful articles.

When should we expect to get back the NHB refund ?

Thanks a lot Aditya for your wishes and your kind words !! I too wish you and your family a very Happy, Healthy & Prosperous New Year !! 🙂

You can expect NHB refunds to start pouring in either from January 10th or January 13th.

Hi Shiv

NHAI has filed draft prospectus with SEBI on Dec-26 for TFB . Hopefully they will also come up with their issue around mid Jan. NHB would have refunded unallocated amount by then. Looks like both NHAI and IRFC has decided to not opt for 20 year bonds. Hope NHAI throws some surprise like NHB on interest rates

Regards

Ramadas

Hi,

Yes, NHAI has filed its draft shelf prospectus on December 27th. It is again surprising that NHAI also is not carrying the 20-year option. Let’s see how soon they launch it and what do they have in store for us. Also, let us hope their rates are not as disappointing as IRFC.

Hi,

Should we make the stop payment for the cheque, if the broker failed to bid on the first day and done on the next day? I shall appreciate, if you can suggest, as I do not wish to block money unnecessarily for another 10 days.

Thanks.

Hi Shub,

Yes, if the bidding has not happened on the first day, then it is better not to proceed with your application.

Thanks very much Mr Shiv.

Is there any way to see the status of the application prior to the allotment?

Regards..

No Shub, there is no way you can check that.

Day 2 (December 31) Subscription Figures:

Category I – Rs. 575 crore as against Rs. 210 crore reserved

Category II – Rs. 1,462.61 crore as against Rs. 525 crore reserved

Category III – Rs. 1,198.35 crore as against Rs. 525 crore reserved

Category IV – Rs. 1,206.08 crore as against Rs. 840 crore reserved

Total Subscription – Rs. 4,442.04 crore as against total issue size of Rs. 2,100 crore

BSE site now state that the NHB issue will be closed only on tomorrow (1/1/2014). Why are they keep on postponing it when the issue is already oversubscribed?

Probably they are required to keep it open for at least three days.

Hi Shiv

I see IRFC and NHB filed final prospectus in a span of 4 days and their interest rates vary quite a lot. How was NHB able to offer higher rates than IRFC? I cant figure out such a drastic variaion in govt bonds yields in those 4 days.In fact i was not expecting anything more than 8.71% for 20 years and finally what came was way higher than that at 9.01%

It is also surprising NHB decided to have one month window with such a small issue and IRFC is over confident of closing such a big issue in 2 weeks?

Regards

Ramadas

Even I’ve failed to understand this variation Mr. Ramadas and that is why I am not in a position to comment on this.

All these are board decisions and it depends on what they are targeting. I don’t think IRFC will be able to raise such a big amount till January 20th.

IRFC knows that they won’t be able to collect full amount in Tranche 1 and want to come with Tranche 2 soon (ie may they are hoping for better rates at that time). Anyway, they have to collect this huge sum before March 31 ( ie whatever the number of tranches).

Yes, that’s right.

Hi Shiv,

I’m also one of silent admirer of your impartial advice. Thanks for your good work.

I had also applied in NHB issue submitted through my broker last evening. Per him the application was submitted by him before 5 pm yesterday and will have stamp of yesterday. He says lead manager can’t confirm the allotment of 74%. I’m surprised. Can you throw some light on the process of submission. Will NHB deposit my cheque if the application is not received by 5pm yesterday? My broker says in case cheque is not presented within next 2/3 days, like hood of allotment is remote.

Thanks

Thanks Viks for kind words !!

If the ‘bidding’ of your application on the exchanges happened on 30th of December before 5 p.m., then you’ll get approximately 74% allotment for sure, irrespective of the cheque hitting your bank on Thursday or Friday. Also, your cheque will get presented by the bank for sure, even if your application bid got made by your broker on 30th, 31st or 1st. I think your broker is misguiding you somehow.

Shiv, thanks.

Is there any process to check whether the bid application was applied before 5pm. The acknowledgement slip just the stamp of the broker and no date.

Regards

Viks

Hi Viks,

I have no idea how to check it on the exchanges. When I do the bidding for my clients or other investors, I share the bid timing & date with them. I think you should also ask your broker to share his bidding data with you.

Hi Shiv,

Thanks a lot for the detailed replies. Read on twitter today that NHB issue is over-subscribed, had qs on how much will get alloted etc. Was pleasantly surprised to see all this discussion, which i missed out on yesterday 🙁

So as of now it looks like should get approx. 75% of bonds, and refund by Jan 10th. Now need to check the other issues like IIFCL and HUDCO.

Thanks again 🙂

You are welcome Ayush !! 🙂

Thanks for such quick reply Shiv. Yes, I do have 15 to 20% of my portfolio in equities and equity related mutual funds. TBH I’ve not had best of experience when it comes to equities in last 3-4 years and best returns which I got was from gold (glad I sold most of it in time). Will def decide investing more into equities once political (after gen elections) and macroeconomic picture becomes more clearer.

Smart investors always invest before the event and not after. Forecasting is the key.

hmm..Will try and visit you next time when I’m in and around Delhi and get your personalized advice regarding my portfolio.

Sure, most welcome !!

In last 3 months I have applied for almost all the TFB issues on day 1 and got 100% allocation hence bit disappointed not to get it this time around. Anyway, now time to do some maths again and decide where to invest the refund.

Refund is just 25% Ikjot. As per asset allocation, you should put some money in equities also. 😉

Thanks Shiv. I am fortunate that on Sunday night before going to bed I didn’t miss to read you and could apply for NHB bonds today.

Unfortunate thing is that more and more retail investors are reading your blog. You are solely responsible for such an interest in NHB. (Not to mention that I am kidding :)).

I know my application will get partial allocation. My question is if NHB keeps the bond issue open for tomorrow, should I apply more tomorrow? Is there a chance of getting a little from tomorrows application or is it fully FCFS on a per day basis? I mean even if they keep issue open no one from tomorrows applicants will get any (I guess even with possible technical rejection todays subscription is more than 100%)? Kindly reply today only :).

One more point – I saw exchanges in between Sam and others above, which I feel has lowered the ethos and essence of this forum.

Contributor like Sam should understand that one with contra-view is welcome by you and others because everyone wants to listen and understand counter perspective. Otherwise, you, yourself, wouldn’t have allowed his view to go public. But what is absolutely wrong is wordings and tone of Sam’s comment of trying to abuse. I feel, better will be that, if you don’t make such comments public unless those are written in right spirit (or remove them if you have set auto accept or just ignore them and don’t reply or reply with no emotion). It is wastage of time for others to read such conversations. After first day’s interest among people I don’t need to say who was very much wrong in his prediction. Even if he is right, provided future TBF rates are higher, I feel I have done right thing to invest in NHB bonds considering present context.

But one thing caught my eyes is “But I don’t misguide people like you do just to earn a commission.”. It is a serious (perhaps wild) allegation he has put on you. It raises question of conflict of interest and questions your integrity and my trust on this forum. Shiv, I will request you explain how come is that possible that I apply for TBF using my icicidirect account and you get a commission? And let me know is it possible in this world that a Govt organization pays an eminent financial planner to promote their debt market issue on top of another organization? Others can also add their logic in this conspiracy theory.

Hi Pinaki,

I don’t know why I responded to Sam, as I don’t think it was even worth responding. But now I don’t want to take it any further. I am quite tired after writing seven posts in the last ten days, working around 15-16 hours a day, answering almost all the queries here, servicing my clients for these tax-free bonds and answering many unknown/useless calls. I need a break from all these arguments and counter-arguments.

Healthy counter perspective is most welcome, who minds it, nobody. But, what Sam was trying to do is to unnecessarily blame me for none of my fault. If I had been doing all this just to earn commissions, I would have been promoting all the private NCD issues here. If I am writing posts here and in return I am getting clients for my financial planning, investment planning, tax planning and general investments, then what’s the problem in that? Would you mind it? I have seen people copying our articles, nobody objects to that. Misselling happens in the insurance space and in the investment world, nobody objects to that. If I am earning my bread & butter by blogging and subsequently servicing the clients with my services, what’s the problem in that? Just leave it, no more explanations.

Answering your query, you won’t get any allotment if you submit your additional application tomorrow. It is FCFS on a per day basis. If you want to earn 5% p.a. interest on your refund application, then probably you can do it tomorrow as well. 🙂

Hi Shiv,

Thanks for such prompt reply.

I would not mind at all if you win clients as an effect of your honest and arduous effort. I don’t see anything unfair or unethical here.

I repeat what I wrote earlier, you are doing almost philanthropy on regular basis by helping so many retail investors. Thousands if not lakhs of people like me, who does not have any monetary terms with you till now, are thankful to you. I wish you, prosperity, success in your personal and professional life as well.

Cheer up !!! have another great year of 2014. Happy New Year in advance.

Pinaki

I have been very very honest in all my responses to the best of my knowledge and abilities Pinaki !! I don’t know how much it has helped people, but Manshu’s & my intentions are very clear – to help people learn about the financial world and facilitate them choosing & investing in the best investment options. Rest God is there to help everybody !!

Also, thanks a lot for all your wishes and compliments Pinaki !! You too have a happy, prosperous and wonderful year ahead !! 🙂

May God give us more honest leaders in 2014 and we too become better persons in our day-to-day lives !!

Will the issue open for subscription tomorrow? I applied at 7 PM today

Hi Ishan,

Issue is open for subscription tomorrow, but you won’t get any allotment now.

Hi Shiv,

What is the point in keeping the issue open tomorrow ? Why did NHB not close it today itself ?

Early closure has to be advertised in a leading national daily newspaper before closing it. NTPC also did the same.

Thanks Shiv. I’m new to the bond space and fascinated by your analysis on this website.

Thanks Ishan !! You are most welcome to participate/contribute on this forum!

Hi Shiv!

Will everyone get the allotment on a proportionate basis or will F.C.F.S apply?

Hi Simple,

Allotment will be made on a proportionate basis. FCFS is not applicable as the retail investors category got oversubscribed on the 1st day itself.

That is bad news.

Can you provide the subscription figures for IINSS-C? (Inflation Indexed National Saving Securities-Cumulative)

http://economictimes.indiatimes.com/markets/bonds/rbi-extends-date-of-issue-of-inflation-index-bonds-to-march-31/articleshow/28150119.cms

I think extending this product won’t solve the purpose, it requires some special tax treatment for it to succeed.

I’ve no access to this info Simple, I don’t even know how to check the subscription figures.

Day 1 (December 30th) Subscription Figures:

Category I – Rs. 575 crore as against Rs. 210 crore reserved

Category II – Rs. 1,461.39 crore as against Rs. 525 crore reserved

Category III – Rs. 1,190.70 crore as against Rs. 525 crore reserved

Category IV – Rs. 1,139.35 crore as against Rs. 840 crore reserved

Total Subscription – Rs. 4,366.43 crore as against total issue size of Rs. 2,100 crore

What is the expected percentage of allotment Shiv ?

Rs. 840/ Rs. 1,139.35 = 73.73% 🙂

Some applications will get rejected due to technical rejections, so we can expect approximately 3 bonds for every 4 bonds applied or 150 bonds for every 200 bonds applied.

isn’t there any dark-green shoe option haha so that we can get full allotment

🙂 🙂 It was awesome Aditya !! How greener you want it to be, like a broccoli ??

green enough to give me my full allotment hahaha

🙂

Hey Shiv,

What does technical rejection mean. Does it mean software error, or incorrect details filled while applying for the application?

Hi Prash,

Please check the prospectus language of NHB issue:

“The Registrar to the Issue will undertake technical rejections based on the electronic details and the Depository database. In case of any discrepancy between the electronic data and the Depository records, NHB, in consultation with the Designated Stock Exchange, the Lead Managers and the Registrar to the Issue, reserves the right to proceed as per the Depository records or treat such ASBA Application as rejected.”

Yes, the retail investors subscription figure finally stands at Rs. 1,139.35 crore and it is really amazing that the issue has received bids worth Rs. 4,366.43 crore as against Rs. 2,100 crore total issue size, including the green-shoe option. This is something others haven’t been to do this financial year.

HUDCO issue is also offering 9.01% for 20 years and in fact, its 8.76% for the 10-year option is higher than this NHB issue, still the investors got attracted towards this issue and have opened up their lockers for this issue.

You were dead right Shiv, when you gave detailed reasons why NHB was the best issue so far. Investors, including me, have preferred NHB over HUDCO but the reason for my preference was that I had already got HUDCO bonds in the first tranche. I also understand that investors were flush with funds because of the end of the year bonus. I hope we get the refund quickly so that we can invest in the IRFC bonds.

Huge response for the issue is due to NHB’s first and the only issue this financial year and its attractive interest rates.

I think you’ll get the refund by January 10th or 13th and I am sure by this time IRFC issue will be open.

At the final subscription of Rs 1139 cr today, against the Rs 840 cr, the allotment for retail guys will be around 74% only.

That’s right Raju! Let’s see how many applications remain after technical rejections.

It is really amazing that we will not get 100% allocation inspite of applying on the very first day!

Shiv, can you please explain what is “green-shoe option”?

I read the below in your summary:

“including the green-shoe option to retain oversubscription to the tune of Rs. 1,100 crore.”

Green-Shoe Option – An option which allows the underwriter of a new issue to increase the size of the issue due to high demand for the securities (shares, bonds or NCDs) on offer.

Total retail subscription (BSE + NSE) = 1139 crore.

Thanks Sailesh!

where are u looking these figures ? which url / link ? pl. share

http://www.bseindia.com/markets/publicIssues/DisplayIPO.aspx?id=751&type=DPI&idtype=1&status=L&IPONo=809&startdt=12%2f30%2f2013