This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

Two power sector companies are inviting your applications for their tax-free bonds – PFC 8.92% bond issue is already open, the issue size is Rs. 3,875.90 crore and has received an extremely good response from the investors by getting subscribed to the tune of Rs. 2,639.30 crore in just two days time. NHPC is entering the field for a competitive fight from October 18th with a smaller issue size of Rs. 1,000 crore.

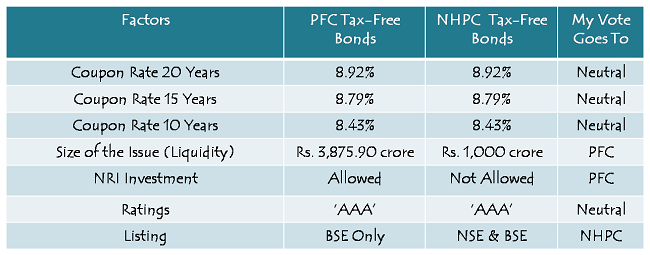

As far as the features of these two issues are concerned, the fight is so close that it has become extremely difficult for retail investors to make a decision. There are so many features which are absolutely same in both the issues and there are other features which are similar, but do not have much relevance to be considered. Just have a look at the features which are same and which are mildly different:

With interest rates exactly the same, both being PSUs and with features so similar, it becomes extremely difficult to make a choice based on just the features of these two issues. So, I thought of doing a fundamental comparative analysis between the two companies.

Profile of PFC & NHPC

PFC got incorporated in 1986 as a financial institution to finance, facilitate and promote India’s power sector development. It is a Central Public Sector Enterprise (CPSE) and got declared a Mini-Ratna enterprise in 1988 and entitled Navratna status in 2007.

PFC provides loans for various power-sector activities, including power generation, power distribution, power transmission and plant renovation and maintenance. PFC finances state electricity boards (SEBs), power generating companies of states and independent power producers (IPPs).

NHPC got established in 1975 to execute all aspects of hydroelectric power project development, from concept to commissioning. It was declared a Mini-Ratna Category-I CPSE in 2008 and has recently sought Navratna status from the government.

To be eligible for ‘Navratna’ status, a company needs to have a score of 60 out of 100, based on certain parameters which include net profit, net worth, total manpower cost, total cost of production, cost of services, Profit Before Depreciation, Interest and Taxes (PBDIT), capital employed etc.

As a Mini-Ratna Category-I entity, NHPC has been granted autonomy to undertake new projects. NHPC has developed and constructed 17 hydroelectric power stations and has current total generating capacity of 5,676.2 MW which is approximately 14.4% of the total hydel generating capacity in India.

It has power stations and hydroelectric projects located predominantly in the North and North East of India, in the states of Jammu & Kashmir, Himachal Pradesh, Uttrakhand, Arunachal Pradesh, Assam, Manipur, Sikkim. and West Bengal.

Credit Ratings of PFC & NHPC

International credit rating agencies Moody’s, Fitch and Standard & Poor’s (S&P) have granted PFC long-term foreign currency issuer ratings of “Baa3”, “BBB-” and “BBB-“, respectively, which are at par with the sovereign ratings for India.

NHPC has also been assigned “BBB-” rating by Fitch. S&P had also given “BBB-” rating to NHPC and removed it from ‘CreditWatch’ in September 2009, based on its assessment of NHPC’s “very strong” link with the government. S&P expressed its opinion that “there is a high likelihood that the government of India would provide extraordinary support for the company in the event of any financial distress”.

S&P also said that the ongoing support from the government is reflected in a tripartite agreement between NHPC, state electricity boards and the government, which largely mitigates the risk of any delay in payments from NHPC’s customers – the state electricity boards (SEBs) that have weak credit profiles.

Financials & other factors to consider

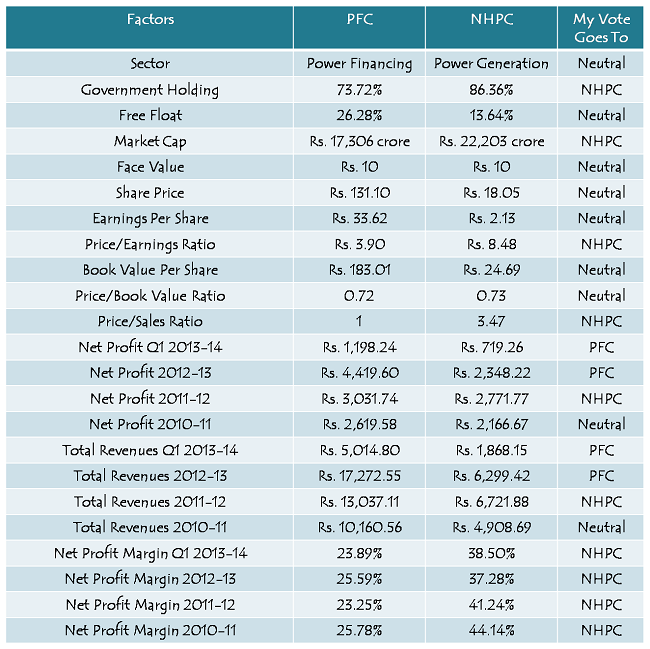

NHPC is a bigger company with a market cap of Rs. 22,203 crore based on its 15th October’s closing share price of Rs. 18.05. On the other hand, market cap of PFC is Rs. 17,306 crore with its share price being Rs. 131.10.

NHPC is also a less riskier company and it gets reflected in its PE ratio. The market is ready to pay NHPC a higher price for buying its shares based on its earnings, as compared to PFC. NHPC is trading at a P/E Ratio of 8.48 times as compared to PFC which is trading at 3.90 times.

PFC’s P/E Ratio of 3.90X is too low and it makes me feel that the market either believes PFC’s earnings to decline considerably at some point in future or some of the borrowers to default on their loan/interest payments.

Final Opinion

I am not a power sector expert. But, as a retail investor, I think NHPC is a better company to invest your money in the power sector. As a common consumer of electricity, this is what I understand – I buy electricity from a private power distribution company in Delhi, which in turn buys it from a power generation company like NHPC etc. Power generation business is a capital intensive business, for which companies like NHPC get capital infusion from the governments, loans from the power financiers like PFC, REC etc. and carry internal accruals by generating profits.

For NHPC, it is better to take money directly from us, the retail investors, rather than we giving money to PFC and then PFC lending it to NHPC at a higher rate. PFC’s fortunes hinge on the power producers like NHPC. If power producers are doing well, PFC would do better, but, if they are not doing good, PFC cannot do anything about it. This relationship is somewhat similar to real estate developers and project finance companies.

The fortunes of these power producers also depend on its cost of the factors of production, like labour, raw materials, technology, machinery etc. Most power plants here in India are coal-based, for whom it becomes a problem if coal supply gets interrupted or they have to import expensive coal due to its scarcity or falling value of rupee. For NHPC, the raw material cost is minimal.

My views might reflect very basic understanding because I don’t know how exactly things get carried out. I could have done some deep research on the functionalities & technicalities of the power sector companies, but then it would have become too complicated for me as well you to understand. So, personally & marginally, I prefer NHPC tax-free bonds over PFC tax-free bonds. Which one is your preference? Please share it share.

Hi shiv

I have been following your blog past 2months. your articles are very informative and extraordinary .thanks a lot for your time and dedication .

Thanks Shiv for the quick reply. Will the listing will be at a premium like NHPC? Or will it be at a discount due to the recent jump in 10 year yield?

Ideally it should be similar to the NHPC bonds. But, PFC bonds will have a higher supply than NHPC bonds, so I think it should give somewhat lower premium than NHPC.

Got the PFC Bonds allotment. Any idea when it will be listed?

Most likely it will get listed on the BSE tomorrow or maximum on Thursday.

Hi Shiv,

10 year yield now over 9 . Do you see further upside in it ?

Hi,

Macroeconomic data released today points out that there is more pain still in store for us. IIP growth came in at 2%, whereas CPI inflation has crossed 10% mark once again. Also, the picture is getting murkier for our fiscal deficit. So, as of now, there is only dim light at the end of this long tunnel.