This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

Shriram Transport Finance Company Limited (STFCL) will be launching its public issue of non-convertible debentures (NCDs) from October 7th i.e. next Monday. The company plans to raise Rs. 500 crore with this issue, including a green-shoe option of Rs. 250 crore.

This is the second such public issue of this financial year from STFC, as the company raised Rs. 750 crore from its first issue in July and the issue got preclosed in just seven days time on July 24th. The current issue will get closed in a couple of weeks time on October 21st, if it does not get preclosed this time again or extended by the company beyond this date.

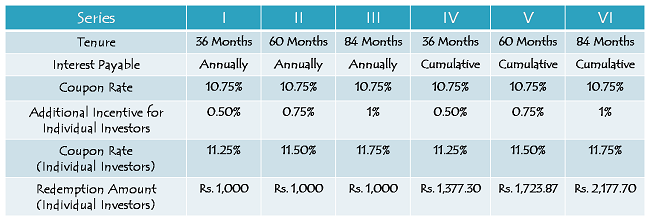

Shriram Transport Finance offered 10.90% per annum for 36 months and 11.15% per annum for 60 months in its last issue to the individual investors. This time the rates are 35 basis points (or 0.35%) higher at 11.25% per annum for 36 months and 11.50% per annum for 60 months. The company did not offer 84 months option in its first issue, which is there in its current issue. But, there is no monthly interest option this time.

Before it starts getting repetitive again, here you have the table having the details about the tenors and the interest rate options.

As you can check from the table above, there is an additional incentive of 0.50% p.a. with 36 months option, 0.75% p.a. with 60 months option and 1% p.a. with 84 months option. Unlike tax-free bonds, this additional incentive is available to the individual investors irrespective of the size of their investment amount.

The company is offering its highest rate of interest @ 11.75% p.a. for an investment period of 84 months, which is a very long period for me to stay invested with a private company. Personally, I would avoid 84 months option.

Categories of Investors – The investors have been classified in the following four categories and the individual investors fall in Category III as well as Category IV.

- Category I – Institutional Investors

- Category II – Non-Institutional Investors

- Category III – High Net-Worth Individuals, including Hindu Undivided Families (HUFs)

- Category IV – Retail Individual Investors, including Hindu Undivided Families (HUFs)

Non-Resident Indians (NRIs), foreign nationals and qualified foreign investors (QFIs) among others are not eligible to invest in this issue.

Allocation Ratio – 50% of the issue is reserved for the Retail Individual Investors (RIIs) i.e. the individual investors investing up to Rs. 5 lakhs and 30% of the issue is reserved for the High Net-Worth Individual Investors (HNIs) i.e. the individual investors investing above Rs. 5 lakhs. 10% of the issue is reserved for the Institutional Investors and the remaining 10% is for the Non-Institutional Investors (NIIs). The allotment will be made on a “first come first serve” basis.

Minimum Investment – Like last time, the company has decided to keep the minimum investment requirement at Rs. 10,000 again i.e. 10 bonds of face value Rs. 1,000 each.

Listing – STFC will get these bonds listed on the National Stock Exchange (NSE) as well as the Bombay Stock Exchange (BSE). Investors can apply for these bonds either in physical form or in demat form, at their own discretion.

Allotment and subsequent listing both are happening super fast these days as we have seen it in the case of REC tax-free bonds. The company will get the NCDs allotted and listed within 9 working days from the date of closure of the issue.

Rating & Nature of the NCDs – CRISIL has rated these NCDs as ‘AA/Stable’ and CARE has assigned a rating of ‘AA+’ to this issue. Moreover, these NCDs are ‘Secured’ by a first charge on an identified immovable property and specified future receivables of the company.

Taxability & TDS – The interest earned on these NCDs will be taxable as per the tax slab of the investors. TDS will be applicable if the NCDs are taken in the physical form and the interest amount exceeds Rs. 5,000 in a financial year. But, if you take these NCDs in your demat account, the company will not deduct any TDS from the interest income.

Interest on Application Money & Refund – Investors will get interest on their application money @ 9% p.a., from the date of investment till the deemed date of allotment, and @ 4% p.a. on the amount liable to be refunded.

Interest Payment Date & Record Date – STFC will make its first interest payment on April 1, 2014 and then on April 1st every year. The record date will be 15 days prior to every interest payment date.

Performance of NCDs issued in July – It is not surprising for me to see all of the NCDs, issued in its first issue in July, to trade below the face value of Rs. 1,000. The reason being the interest rates have risen since then.

STFC-NV, 36 months annual interest option, last traded at Rs. 985 and STFC-NW, 60 months annual interest option, last traded at Rs. 980.10 as on September 27, 2013. Allotment date of these NCDs was August 1, 2013 and it has been almost two months since then. So, the yield on these NCDs must be ruling around the coupon rates offered by the company in the current issue.

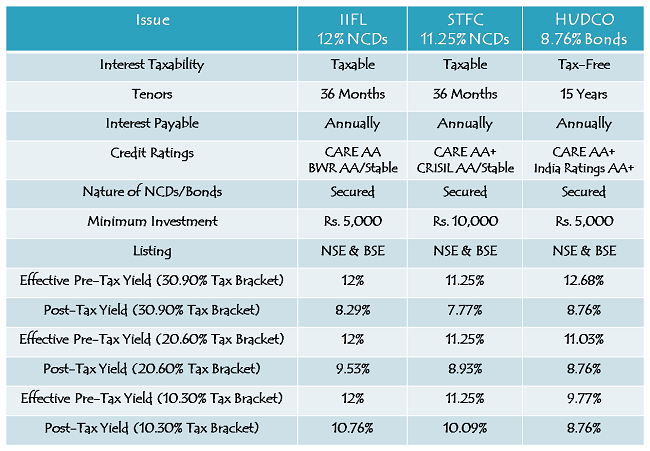

IIFL NCDs Issue vs. STFC NCDs Issue vs. HUDCO Tax-Free Bonds

If some of the investors were comfortable investing with the just concluded IIFL NCDs but somehow missed it, then I think they can consider investing in this issue. My personal opinion is that the business model of Shriram Transport Finance is better than the business model of India Infoline Finance Limited (IIFL) and probably its credit rating also suggests that.

But, I would still say that one should explore the already listed NCDs yielding 13-14% with a maturity period of 1-2 years. I think, with fixed deposits (FDs) or NCDs issued by private companies, the shorter the tenure of your investment is, the better it is.

As explained many times earlier, I think the investors falling in the higher tax brackets should opt for tax-free bonds rather than these taxable NCDs. So, personally I would go for HUDCO tax-free bonds or the upcoming IIFCL tax-free bonds rather than these STFC NCDs.

If you are thinking that I have missed to quote the financial of the company in this post, then you are right, but it is intentional. I did that exercise in my July STFC NCDs post and I don’t want to do that again as those were its latest annual results.

Link to Download the Application Form of Shriram Transport Finance NCDs

SSIR MY PARTY HAS NOT RECEIVED MATURITY AMOUNT OF NCD 2013 OF SHRIRAM TRANSPORT FINANCE CO LTD THE DETAILS ARE AS UNDER

NAME MEHTA KALPANABEN JAYVADAN FOLIO NO NCD6-11507

NO OF BONDS 25 DATE OF MATURITY 24.10.2016

2) NAME MEHTA JAYVADAN RAMANLAL FOLIO NO NCD6-11506

NO OF BONDS 25 D O MATURITY 24.10.2016

PLEASE LOOK INTO THE MATTER URGENTLY

SIR MY PARTY HAS NOT RECEIVED MATURITY AMOUNT OF NCD 2013 OF SHRIRAM TRANSPORT FINANCE CO LTD THE DETAILS ARE AS UNDER

NAME MEHTA KALPANABEN JAYVADAN FOLIO NO NCD6-11507

NO OF BONDS 25 DATE OF MATURITY 24.10.2016

2) NAME MEHTA JAYVADAN RAMANLAL FOLIO NO NCD6-11506

NO OF BONDS 25 D O MATURITY 24.10.2016

PLEASE LOOK INTO THE MATTER URGENTLY

I HAD INVESTED IN STFC in ncd in july 2011 .138ncd ,dpid1203330000307916 & my daughter ,,Shah Amruta pradip ,dpid ,in30051314836596, 138NCD,allotted in july2011,till date not received amount at maturity .

Why is YTM in page for shriram Transport NCD is @17.054 though the stock is trading @ slightly above 1030 ; facevalue 1000.

http://www.nseindia.com/live_market/dynaContent/live_watch/get_quote/GetQuote.jsp?symbol=SRTRANSFIN&series=NQ

As per the NSE’s calculation, this is the annualised yield you’ll earn if you buy this bond at Rs. 1,030 and hold it till its maturity on July 11, 2014. You are going to get full year’s interest of Rs. 110 on April 1, 2014 and also the interest for 102 days on maturity.

What is the tax implication of buying and holding it till maturity?

Interest and Short-Term Capital Gain will be taxed as per your tax slab. No tax on short-term capital loss. In this case, there is no scope of any Long-Term Capital Gain/Loss.

Shriram Transport NCDs got listed today on the NSE & BSE. 11.25% 36-months bonds hit a high of Rs. 1,005, low of Rs. 995 and closed at Rs. 1,005. Total NCDs traded on the BSE were 1.50 lakhs.

Shriram Transport NCDs to get listed on the stock exchanges on October 29th i.e. Tuesday.

Here are the BSE codes for the same:

Series I – BSE Code – 934915

Series II – BSE Code – 934916

Series III – BSE Code – 934917

Series IV – BSE Code – 934918

Series V – BSE Code – 934919

Series VI – BSE Code – 934920

Dear-Shiv,

plz,let me confirm and communicate the forthcoming NCD issue or leading companies with Minimun investment.

Dear Arun,

At present, I do not have any info about any forthcoming NCD. We cover all NCDs and Tax-Free Bonds as & when they come. You can subscribe to our newsletter above and you’ll get a mail when any such issue hits the market.

Dear Shiv,

Will you please inform us through your post, when listing date of these NCDs is published ?

Thanks.

Sure, I’ll do that.

Your table showing Hudco bonds yield as 12.68 % is blatantly misleading. While the actual cash flow is just 8.76 %, the remaining 3.92 % is just a notional income; you will not get it whatever maybe the circumstance.

Kindly remove that.

plz,provide/send me the latest Corporate Fixed Deposits rates till now with ncd etc in my mail-id,ASAP

Sorry Mr. Arun, we do not provide these kind of personalized services.

Dear Shiv,

In contrast to the India Infoline NCD issue, subscription by Non-individual categories (Category 1& 2) is very low (almost zero), in this issue. Other than interest rate (10.75%(annually) in this issue against 12%(monthly) in India Infoline), is there any other reason for less subscription by non-individual investors ?

Also, the portion reserved for Non-individual categories is just 20% in this issue against 50% in India Infoline NCD issue. Looking at lower coupan offered to non-individual investors and smaller portion reserved for them, it seems Shriram Transport Finance is less interested in issuing its NCDs to non-individuals. What could be the reason for this bias being shown towards individual category ?

Do you think less allotment and lower coupan for non-individual categories will result in poor liquidity compared to India Infoline NCDs after listing ?

Thanks

TCB

Dear TCB,

1. I don’t think there is any other reason for the non-institutional investors to show such a poor interest in these NCDs other than the low coupon rates being offered. I think STFC is a better company than IIFL fundamentally.

2. Yes, I agree with your observation that STFC is more interested in issuing its NCDs to the individual investors. STFC gives this explanation for its motive behind higher rates for individual investors – “The objective of this offering is to diversify our lenders base and to provide an opportunity to the retail -investors to participate in our growth”.

3. Yes, I think so that it will result in a lower liquidity for the STFC NCDs than the IIFL NCDs. Also, STFC NCDs issue size is smaller than IIFL NCDs issue, it will also result in a lower liquidity.

Like last time, this STFC NCDs issue is getting closed early this time also and that too in just 7 days again. The issue is getting closed on October 14th i.e. Monday. The company has already raised Rs. 527.20 crore till yesterday.

Hi Shiv,

At the outset a sensible analysis, often not found that many!,

The final verdict you had sounded with HUDCO, do you reckon it is good prospect as the net effective IT adjusted return seems to be lower than the FD rates of some of the banks. Further, considering the low liquidity, wouldn’t the FD more appropriate.

Thanks,

Hi Ram,

FDs are probably better only for the investors who are not required to pay any taxes. FDs are yielding between 8.75% to 9.5%, only for shorter tenures. HUDCO bonds are yielding 8.75% tax-free for 20 years. There is a scope of capital appreciation also. Suppose, HUDCO bonds give you a capital appreciation of 10%, anytime during the next 5 years, its annual returns would surpass 10-11% very easily. There are many benefits tax-free bonds carry over bank FDs or company FDs.

Hi,Shiv

Can you pls check these ncds

L&T N2—YTM is showing 22.82% https://www.edelweiss.in/debt/L-And-T-Finance-Ltd/L_TFINANCE-N2.html

Similarly IIFL-N5 showing YTM as 16.45%

Are these rates given correctly or anything wrong in the figures?These kind of rate even beat equities Am I missing something?

Hi Saurabh,

Not sure about IIFL N5 YTM @ 16.45%, but L&T N2 YTM @ 22.82% is definitely incorrect. Don’t bank on these YTMs blindly, these are calculated incorrectly.

Thanks for reply.

Yes the information provided about YTM seems to be wrong in many of the NCDs.

I wonder how edelweiss can be so careless about the data provided,they are taking customers for granted.Better not provide data instead of putting wrong data.

It is the case with most of the service providers in the financial services industry these days. This industry has become agents’ industry as you’ll hardly find high service standards and no misselling.

I totally agree with you that they should provide no data instead of providing incorrect data.

I realised one should be careful of YTM mentioned in Edelweiss after the interest cutoff date during year end (March) and half yearly (Sep) (based on whether coupon payment is annual or semi annual), as the site assumes dividend is payable even if you transact just before dividend due date (end of month).

Hope this helps.

This problem exists everywhere, even on the NSE platform. Some YTMs on the NSE platform are also incorrect. I am yet to see a site which has this YTM data all perfect.

Hi Shiv,

thanks for detailed post and info about IIFCL tax-free bonds issue date. I always look forward for your posts. thanks again.

–Kishor

Thanks Kishor! This is what keeps us going that extra mile!

IIFCL tax-free bonds issue opens October 3rd. Tentative coupon rates are 8.26% p.a. for 10 years, 8.63% p.a. for 15 years and 8.75% p.a. for 20 years. The issue is rated ‘AAA’ as compared to ‘AA+’ for the HUDCO issue & ‘AAA’ for the REC issue.

Hi Shiv

Always look forward to your posts. Can you advise on existing NCDs which can be considered? Some of us dont know how to calculate the 13-14% yield?

Thanks

Hi Harineem, I am glad you enjoy our posts & these are useful to you !!

As far as YTM calculation is concerned, you can check this post. I hope it helps somewhat!

http://www.onemint.com/2012/07/25/how-to-calculate-yield-to-maturity-of-a-bond-or-ncd/

Though it doesn’t make me comfortable advising securities here, but still, one can check N4 of IIFL Finance, trading at Rs. 1,025, N1 of IIFL Finance, trading at Rs. 1,040, NL of Shriram Transport, trading at Rs. 1,040. Though some of the NCDs of Religare, Muthoot, Shriram City etc. must be yielding more than the above mentioned NCDs, but I would stick to the better ones.

what is the news on IIFCL TAX free bond issue ?

No news out yet, at least I don’t have it.

Can you please suggest web sites which provide exhaustive quotes for NCD,s in Secondary Market?

Here you have it Mr. Ramamurthy:

http://www.nseindia.com/live_market/dynaContent/live_watch/equities_stock_watch.htm?cat=SEC

https://www.edelweiss.in/debt/State-Bank-of-India/SBIN-N5.html

Thank You

You are welcome Mr. Ramamurthy!