This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

Rashesh Shah promoted Edelweiss Financial Services’ 79.28% subsidiary, ECL Finance Limited is going to launch its public issue of secured, redeemable, non-convertible debentures (NCDs) from January 16th i.e. the coming Thursday. ECL Finance has issued such NCDs earlier also, but only through private placements. So, this is the first such public issue of NCDs by the company.

The issue will remain open for just eight days from January 16 and is scheduled to get closed on January 27, which is a Monday.

Size & Objective of the Issue – ECL Finance plans to raise Rs. 500 crore from this issue, including the green-shoe option of Rs. 250 crore. The company plans to use the proceeds for various financing activities including lending and investments, to repay existing loans, for capital expenditures and other working capital requirements.

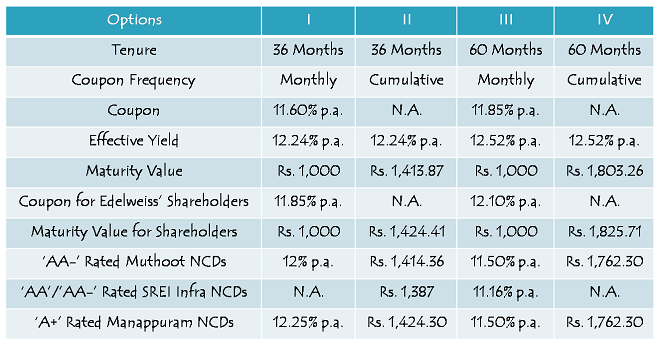

Coupon Rates & Tenors on Offer – The company has decided to issue these NCDs for a duration of 36 months and 60 months. For 36 months, it is offering 11.60% per annum rate of interest, payable either monthly or at the end of this period on a cumulative basis.

For 60 months, it is going to pay 11.85% per annum, again payable either monthly or on a cumulative basis on maturity.

Higher Coupon Rate for Edelweiss Shareholders – ECL finance has decided to offer an additional 0.25% p.a. to the shareholders of Edelweiss Financial Services, its promoter company. So, even if you hold one equity share of Edelweiss, which closed at Rs. 28.80 per share on January 13, you are going to get this additional rate of interest.

But, you need to keep a couple of clauses in mind before you get attracted to this extra rate. One, you need to be a shareholder in the records of Edelweiss, on the deemed date of allotment as well as on the record date(s) i.e. both the dates.

Two, you are going to get this additional interest only on the lower number of NCDs held by you on the deemed date of allotment and the record date(s). So, if you buy some more NCDs from the secondary markets, you are not going to get the additional interest. Also, if you sell some NCDs after you get them in the initial allotment, you are going to lose out on this additional interest on those NCDs.

Interest Payment – With monthly option of interest payment, due interest will be paid on the first day of every month, except Sundays and public holidays on which commercial banks are closed in Mumbai.

Categories of Investors & Allocation Ratio – The investors have been classified in the following three categories and each category will have the below mentioned percentage fixed in the allotment:

Category I – Institutional Investors – 20% of the issue is reserved

Category II – Non-Institutional Investors – 20% of the issue is reserved

Category III – (i) “Unreserved Individual Portion” including HUFs – 20% of the issue is reserved

Category III – (ii) “Reserved Individual Portion” including HUFs – 40% of the issue is reserved

Resident Indian individuals or HUFs, investing Rs. 10 lakhs or less, would fall under the “Reserved Individual Portion” and those who invest more than Rs. 10 lakhs would come under the “Unreserved Individual Portion”.

NCDs will be allotted on a first come first served basis.

NRI not Allowed – Non-Resident Indians (NRIs), foreign nationals and qualified foreign investors (QFIs) among others are not eligible to invest in this issue.

Rating of the Issue – The issue has been rated by CARE and Brickwork Ratings and both have assigned it a ‘AA’ rating. Brickwork Ratings has a ‘Stable’ outlook for the issue.

Demat & TDS – Demat account is not mandatory to invest in these bonds as the investors have the option to apply these NCDs in physical form as well. Also, though the interest income would be taxable with these bonds, NCDs taken in demat form will not attract any TDS.

Listing, Premature Withdrawal & Put/Call Option – The company is going to get its NCDs listed on the Bombay Stock Exchange (BSE) only. The investors will not have the option to redeem these bonds back to the company before the maturity period gets over, but they can always sell these bonds on the BSE anytime they want. Liquidity remains low with these NCD issues though.

There is neither any put option with the investors of these bonds nor there is a call option with the company to pay back early.

Minimum Investment – The investors will be required to apply for at least 10 NCDs in this issue which makes it a minimum investment of Rs. 10,000.

Profile of ECL Finance Limited

ECL Finance is the 79.28% subsidiary of Edelweiss Financial Services Limited. Rest of its shareholders include Edelweiss Commodities Services Limited holding 7.77%, Edelweiss Securities Limited holding 5.15% and Waverly Pte Limited, an affiliate of GIC Singapore, holding 7.80% in the company as on November 30, 2013. It is one of the forty seven (47) subsidiaries of Edelweiss Financial Services Limited.

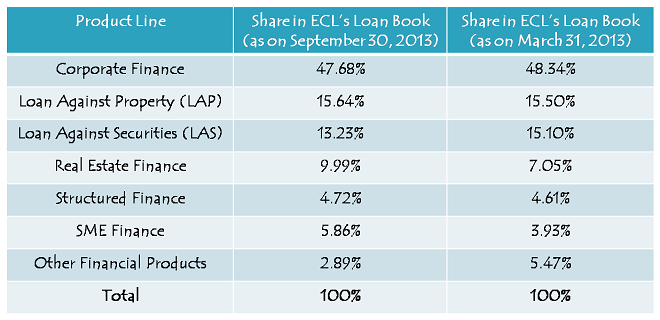

ECL Finance is into the business of lending and has diversified product line, including short-term/long-term finance to the corporates, loan against property & securities, financing to the real estate developers and small & medium enterprises (SMEs), ESOP financing, IPO financing, loan against mutual fund units/bonds etc.

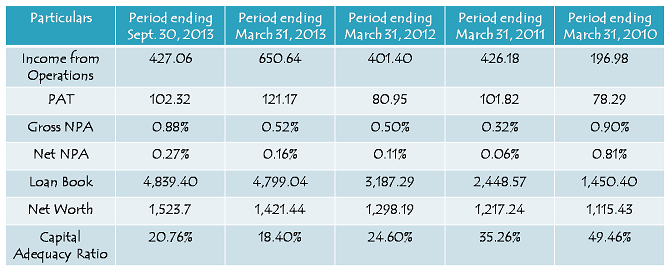

Relatively speaking, I think this issue looks better to me as compared to the other issues of Muthoot Finance, Manappuram Finance, SREI Infra and even India Infoline Housing Finance Limited (IIHFL). ECL Finance has a diversified product portfolio and backing of a reputed promoter group. Its financial position also looks healthy.

But, again I think that the investors in the higher tax bracket are better off investing in tax-free bonds rather than these taxable NCDs. Investors, who are not liable to pay any taxes and who can bear some risk of investing their money with a private company, can consider these NCDs for their investment.

Application Form of ECL Finance NCDs

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in ECL Finance NCDs, you can contact me at +919811797407

Hi Shiv,

is there some new NCDs coming in the market in May as well as June?

Hi,

Thanks for detailed review,Can you please let me know If these NCDs get listed to BSE, What are ISIN numbers of listing?

Hi Chander,

Here are the BSE codes & ISIN for ECL Finance NCDs:

Option I – BSE Code – 934951 – ISIN – INE804I07SG6

Option II – BSE Code – 934952 – ISIN – INE804I07SH4

Option III – BSE Code – 934953 – ISIN – INE804I07SI2

Option IV – BSE Code – 934954 – ISIN – INE804I07SJ0

Link to check the allotment status of ECL Finance:

http://www.linkintime.co.in/newsite/applicationStatus.jsp?comanyIdn=1089

pl.confirm allotment Pan no anjpp5778q

Hi Shubhada,

Website of ECL Finance’s Registrar, Link Intime, is not working. So, you’ll have to contact your agent/service provider for the allotment info.

ECL Finance NCDs to get listed on the BSE on February 3rd i.e. Monday.

Here are the BSE codes for the same:

Option I – 11.60% Monthly Interest – 36 Months – BSE Code – 934951

Option II – 11.60% Cumulative Interest – 36 Months – BSE Code – 934952

Option III – 11.85% Monthly Interest – 60 Months – BSE Code – 934953

Option IV – 11.85% Cumulative Interest – 60 Months – BSE Code – 934954

Deemed date of allotment has been fixed as January 28, 2014. Monthly interest will be paid on the first working day of every month.

I bought ECL shares before ECL ncd allotment for I earned more 0.25% more interest. ECL shares already allotted in my demat account before ECL ncd allotment but when i shown my demat statement ECL ncd interest rate 11.85% . Where is my 0.25% interest?

Hi Maulik,

You’ll be paid this extra 0.25% interest on the interest payment date, given you hold Edelweiss shares on the record date as well and you don’t sell these NCDs before the record date.

Thank you so much.

You are welcome.

Hi Shiv,

When the allotment of this issue is expected?

Hi Namdev,

Allotment should happen sometime next week, I think by Thursday or Friday.

Day 3 (January 20) Subscription Figures:

Category I – Rs. 180.03 crore as against Rs. 100 crore reserved

Category II – Rs. 73.65 crore as against Rs. 100 crore reserved

Category III – Rs. 326.28 crore as against Rs. 300 crore reserved

Total Subscription – Rs. 579.95 crore as against total issue size of Rs. 500 crore

This issue stands closed today. 100% allotment to all Category III investors, even if the application got submitted today.

Edelweiss’ ECL Finance NCD issue closes today. Investors need to get their forms submitted by 5 p.m. today.

With 250 cr as Green shoe option, application made on Monday most probably will get 50% allotment right?

I have no idea what percentage of allotment will be made if application is made on Monday. It all depends on the quantum of investments, allotment can be 100% also.

Day 2 (January 17) Subscription Figures:

Category I – Rs. 180.03 crore as against Rs. 100 crore reserved

Category II – Rs. 71.76 crore as against Rs. 100 crore reserved

Category III – Rs. 264.02 crore as against Rs. 300 crore reserved

Total Subscription – Rs. 515.80 crore as against total issue size of Rs. 500 crore

Hi Shiv,

Few questions.

1) How can we know the break-up subscription numbers within category III for “Reserved Individual portion” and “Unreserved Individual portion”.

2) Do you think, if I apply on Monday for “Reserved Individual portion”, will I get full allotment?

3) On Monday if category III gets oversubscribed, I think they have the first right to allocation in category II under subscription if any? Is my understanding correct?

Hi Sailesh,

1. It is not possible to have the break up of subscription data within Category III. It is known to the company itself.

2. I am not 100% sure about it, but you’ve some fair probability of getting allotment either full or partial.

3. Yes, if Category III gets oversubscribed on Monday, which I doubt it will, then they will have first right in allotment.

thanks for ur post

could pls tell me that if i purchase a share tomorrow from NSE or BSE of Edelweiss, will i get the extra percentage. how they calulate the tax is it while TDS or on the maturity. and how the tax free bond are ?. i am just retired and want to invest 4lks in bonds,mutual fund and some secured investment. i bit can take risk upto 2 lks investment not more than that. how i would go.pls provide a portfolio. further i thought for NHAI bonds but ur post for edelweissis bond seems lucrative what should i go .pls suggest thank for ur goodresearch

Thanks Mr. Anagh for your kind words!

All shareholders on the date of allotment will get the extra interest. TDS gets deducted if you take taxable NCDs in physical form and the annual interest is more than Rs. 5,000. There is no TDS if these bonds are taken in a demat form. Also, I cannot advise you against your personal queries here on this forum.

Will I get allotment if I apply tommorrow for series I …I m resident Individual investor.

Yes, you’ll get it.

Hi Shiv,

Can u post 2day’s subscription figures.

Will I get full allotment if I apply 2moro for category 4.

Day 1 (January 16) Subscription Figures:

Category I – Rs. 180.03 crore as against Rs. 100 crore reserved

Category II – Rs. 70.57 crore as against Rs. 100 crore reserved

Category III – Rs. 177.28 crore as against Rs. 300 crore reserved

Total Subscription – Rs. 427.88 crore as against total issue size of Rs. 500 crore

There is no Category IV with this issue.

The subscription figures is really more than 100% excluding green shoe option in every category, which is an amazing response for first day.

That’s right!

Yeah, probably as ppl are tired with repeating NCDs 🙂 of shriram, muthoot etc, this a good option for diversification

Hi Shiv, few queries.

1. Is it advisable to buy this through investment agent or directly through Demat?

2. Some where I read that agents pass on additional .5% to 1% commission. 3. Is it true for individual investor also?

Thanks in advance.

Hi SUB,

1. As these are not mutual funds and it doesn’t really affect your investment, there is no harm in getting it done through an agent, but then it really depends with which mode you are more comfortable with. I think demat accounts are more comfortable to invest.

2. I don’t want to comment on this point, as it is not legal to pass commission earned with these products.

3. I didn’t get this query.

Hi Shiv,

If I buy one share tomorrow, will I be eligible for additional interest?

Hi Nagendra,

You need to be a shareholder on the deemed date of allotment. Say, if this issue gets closed on January 20th and the deemed date of allotment gets fixed as January 30th, you need to be a shareholder on this date in the books of Edelweiss.

Thanks a lot Anup for your encouraging words !!

Yes, that’s correct, you’ll be eligible for this extra interest rate even if you’ve only one share.

Thanks Shiv for clarifying. Appreciate it.

You are welcome Anup!

Great Article Shiv! One question regarding Shareholders. If I buy one share today (15th) and keep it till tenure ends, I will be liable to get extra interest rate? I think yes but just confirming.

Also – thanks a lot for all your descriptive analysis this time and in past too. 🙂

So this NCDs seems better compared to other recently launched NCDs.

Thanks for the review.

You are welcome Saurabh!

Great Shiv, was waiting for this post 🙂 Thanks for comparing with other NCDs. 2 qns…

1. How do you compare this with Shriram NCD relatively?

2. For investors not liable to pay taxes, which tenure you suggest – 36 or 60 months? (assuming no cashflow reqts constraint)

Thanks Chaitanya!

1. I think Shriram Transport Finance has a long history than this company, so it is more reliable. But, then ECL Finance’s interest rate is higher, its product line is diversified and has a more reputed promoter group. I think one needs to take a call with which company he/she is more comfortable.

2. Personally, if I decide to ever invest in such issues, I would always prefer the shortest possible tenure with NCDs or company FDs.

Thanks again Shiv!!

You are welcome Chaitanya!