National Housing Bank (NHB) 8.93% Tax Free Bonds – March 2014 Issue

This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

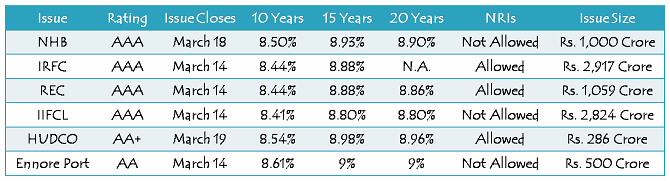

With the current financial year coming closer to an end, the investors, waiting to deploy their cash surplus or maturity proceeds from their other investments into tax free bonds, are currently spoilt for choice. There are as many as five tax free bond issues currently open and the much awaited NHB issue is getting open for subscription tomorrow i.e. March 7.

As expected, it is carrying the highest rate of interest among the ‘AAA’ rated issues which are currently open – 8.93% p.a. for 15 years, 8.90% p.a. for 20 years and 8.50% p.a. for 10 years.

Size & Closing Date of the Issue – NHB’s first issue in December was of Rs. 2,100 crore and it got subscription to the tune of Rs. 4,366.43 crore on the first day itself. Though the current issue is scheduled to close on March 18, going by the issue size of Rs. 1,000 crore, I think it too should get oversubscribed on the first day itself.

So, in order to avoid rejection of their applications, I would advise the interested investors to apply for these NHB bonds on the first day itself. In case of oversubscription on the first day, the applicants will get allotment on a pro rata basis.

NRI/Foreign Portfolio Investment – Foreign Institutional Investors (FIIs), Non-Resident Indians (NRIs) and Qualified Foreign Investors (QFIs) are not eligible to invest in this issue.

Investor Categories & Allocation Ratio – Once again the investors have been classified in the following four categories and each category will have certain percentage of the issue size reserved during the allocation process:

Category I – Qualified Institutional Bidders (QIBs) – 10% of the issue i.e. Rs. 100 crore is reserved

Category II – Non-Institutional Investors (NIIs) – 25% of the issue i.e. Rs. 250 crore is reserved

Category III – High Net Worth Individuals including HUFs – 25% of the issue i.e. Rs. 250 crore is reserved

Category IV – Resident Indian Individuals including HUFs – 40% of the issue i.e. Rs. 400 crore is reserved

Allotment on First Come First Served Basis – Subject to the allocation ratio, allotment will be made on a first come first serve (FCFS) basis in each of the investor categories, based on the date of upload of each application into the electronic system of the stock exchanges. As mentioned above, allotment will be made on a pro rata basis for that day on which the concerned category gets oversubscribed.

Rating of the Issue – Investors seeking safety of their capital give high importance to the credit rating of an issue. This issue has been rated ‘AAA’ by CRISIL, ICRA and CARE. Instruments with ‘AAA’ rating are considered to have highest degree of safety regarding timely servicing of financial obligations.

Lock-in Period & Premature Redemption – There is no lock-in period with these bonds, but at the same time, you cannot redeem these bonds back to the company before their maturity period gets over. In order to encash your investment before maturity, you’ll have to compulsorily sell these bonds on the National Stock Exchange (NSE) where these bonds will get listed for trading.

Demat/Physical Option – Though it is mandatory to have a demat account to sell/trade these bonds, you can subscribe to them in physical/certificate form as well. Interest payment will still get credited to your bank account through ECS.

Interest on Application Money & Refund – As always, NHB will pay interest to the successful allottees on their application money, from the date of realization of application money up to one day prior to the deemed date of allotment, at the applicable coupon rates. Unsuccessful allottees will get interest @ 5% per annum on their refund money.

Minimum Investment – As NHB has kept the face value of its bonds unchanged at Rs. 5,000, an investor is required to apply at least one bond in this issue i.e. minimum investment of Rs. 5,000.

Interest Payment Date – NHB has not fixed its interest payment date this time as well and its first due interest will be paid exactly one year after the deemed date of allotment.

Which issue should I invest in?

When I covered NHB’s first issue in December, I mentioned certain points to express my views. Let me mention those points again and express my current views regarding those points:

First, NHB issue is ‘AAA’ rated.

Current View: There is no change in NHB’s credit rating for this issue as well. So, I think it remains a good issue to invest rating wise.

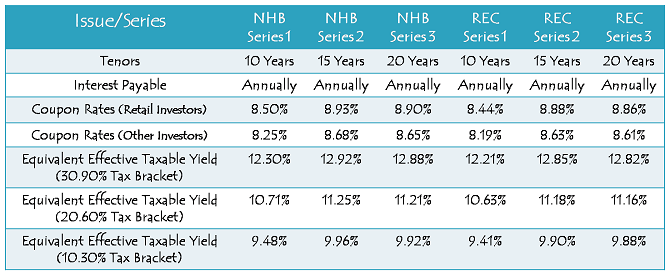

Second, you are going to get 9.01% p.a. and 8.88% p.a. coupon rates which are the best 20-year and 15-year rates offered by any AAA rated or AA+ rated issuer till date.

Current View: NHB offered 9.01% p.a., 8.88% p.a. and 8.51% p.a. for the 20-year, 15-year and 10-year options respectively. These respective rates stand as 8.90% p.a., 8.93% p.a. and 8.50% p.a. this time around, which makes the 15-year option to be the most attractive for a retail investor.

Third, NHB is a wholly-owned subsidiary of the RBI and I don’t foresee the RBI to ever let its subsidiary default on any such bond issue. Also, NHB is the regulator of the housing finance companies, like RBI is for the banks and SEBI is for the capital markets. I don’t think any government would allow any regulator to default on its payments.

Current View: I think there is no need to change my earlier view as far as this point is concerned.

Fourth, it is almost certain that the CPI inflation will start falling from next month onwards. If that materialises, we might have G-Sec yields falling quite sharply.

Current View: Though there has been a sharp fall in the CPI as well as the WPI inflation January onwards, but unfortunately, G-Sec yields have not fallen in line with the inflation numbers. There have been many factors behind it – high fiscal deficit, high debt levels of the government, unexpected Repo Rate hike & start of inflation targeting by the RBI in its January policy, uncertain political & economic policy environment in the short term and the government’s unrealistic fiscal deficit target for the next fiscal year.

I think the G-Sec yields should move in a broad range till the time we have a stable government at the centre. If we have a sharp fall in the inflation numbers and controlled government expenditure in the next few months, we can expect G-Sec yield to fall sharply if we get a strong and stable government in May.

Fifth, IRFC is the next company to launch its tax-free bonds from January 6 and its coupon rates are lower than that of NHB at 8.48% p.a. for 10 years and 8.65% p.a. for 15 years. It is not going to issue these bonds for 20 years either.

Current View: There are five issues currently open, out of which three issues are ‘AAA’ rated, one is ‘AA+’ and one is ‘AA’ rated. As this ‘AAA’ rated NHB issue is offering the highest rate of return as compared to the other ‘AAA’ rated issues, I expect a very good response from the institutional as well as the retail investors.

Sixth, there are very few good companies left now to issue tax-free bonds this financial year. REC, PFC, NHPC and NTPC have already raised their quota of authorised amount from the markets. HUDCO is also very close to reach its targeted amount. Only IIFCL, NHAI, IREDA, Airport Authority of India (AAI), Ennore Port and Cochin Ship Yard are now left to issue these bonds and their issue sizes are also very small, except NHAI and IIFCL.

Current View: IRFC today extended the closing date of its current issue from March 7th to March 14th. Also, as AAI issue is not expected in the current financial year and Cochin Ship Yard is yet to file the prospectus for its issue, I think this NHB issue should be the last public issue of the current financial year.

Seventh, it is still not certain whether tax-free bonds would see the light of the day next financial year onwards or not. Like 80CCF infrastructure bonds got stopped getting issued from FY 2012-13 onwards, it is possible that the next government decides to stop extending this budgetary support to all such companies.

Current View: I think there is no need to change this view as well. You might not have tax free bonds available for subscription next financial year, in which case you will see a good demand for these bonds in the secondary markets.

Eighth, NTPC issue got listed a few days back and that too at a premium. If an issue with coupon rates lower than the NHB issue can trade at a premium, then it is almost certain that these NHB bonds would also trade at a premium on listing.

Current View: It has been the case with most of these issues in the current financial year. Most of these bonds have been trading at a premium and I expect NHB bonds also to list at a premium in the current interest rate scenario.

Ninth, NHB has reasonably strong fundamentals. It reported profit after tax (PAT) of Rs. 450 crore with total income of Rs. 3,030 crore for the period ended June 30, 2013 as against Rs. 387 crore and Rs. 2,492 crore respectively for the period ended June 30, 2012. Its net interest margin (NIM) also improved to 2.25% during this period as against 2.20% last year.

NHB’s asset quality has also been remarkable. Gross NPAs and Net NPAs remained quite close to zero for the periods ended June 30, 2011 and June 30, 2012. Though its gross NPAs and Net NPAs have jumped to 0.53% and 0.45% respectively in the latest period ending June 30, 2013, this relative poor performance was due to one large project exposure slipping into the NPA category. This large account was worth Rs. 179.60 crore out of its total NPAs of Rs. 180.62 crore.

Current View: There is no change in my view as far as NHB’s fundamentals are concerned.

Why you should not invest in this issue?

If I myself decide not to invest in this issue, I would have only one valid reason for that, higher expected coupon rates in the forthcoming issues. If any of you think that the rates would be higher with NHAI bonds or IIFCL tranche III bonds, then you can probably skip this issue. Personally, I would invest my family’s money in this issue and would also advise my clients to do that.

Current View: Last time I had only one reason. This time I don’t have any reason for me not to invest in this issue, except that I don’t have enough money for me to fully utilise Rs. 10 lakh limit applicable for a retail investor.

Application Form of NHB Tax Free Bonds

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in NHB tax-free bonds, you can contact me at +919811797407

Last good opportunity for the TFB investors… thanks for the update Shiv !!!

You are welcome Gaurav !! Yes, it seems to be the last good opportunity for this financial year.

Better to invest in other TFB as this will get oversubscribed and money gets blocked. 🙁

Better to invest in other TFB as this will get oversubscribed and money gets blocked 🙁

Very important and interesting observation. It is a call the investors need to take. I’ll still go for this NHB issue only.

Thanks Shiv, for adding the NRI column in the table… 🙂

You are welcome Ketki !!

What happened to NTPC issue? Is it still expected?

NTPC has raised the additional quota of tax free bonds through private placement, so no public issue is expected now.

sir,

can you please share the score i.e subscription numbers

Hi Shiv!

What happened to NTPC issue? Is it still expected?

Dear Shiv,

If an investor has applied for only one bond and if the issue gets more than 1 times subscribed on the day of application, will the investor get confirmed allotment (as in case of equity ipos wherein minimum one lot is alloted to all applicants before alloting higher quantities to bigger applicants) ?

Thanks

yes. Last time I had applied for 1 bond of NHB got one alloted.

Yes, that’s right. All of the investors, who apply for 1 bond, will get 1 bond allotted.

What is the subscription status? Any idea??

i feel people who apply for 1st day could get 100% allotment 😉

Bidding Update @ 12 o’clock:

Total Bidding – Rs. 218.62 Crore

Category IV Bidding – Rs. 50.96 Crore

Hi Shiv,

Any thoughts on some good avenues to invest proceeds of the yearly interest payout of tax free bonds?

Hi SKb,

I’ll try to cover those investment options with a separate post. At present, you can reinvest your annual interest in these bonds.

Shiv, Looks like for cat4 (400 cr) people who will apply on day1 should get 100% allotment – correct?

Hi RS,

It is difficult to predict the final retail subscription figure at the end of the day, but it seems to me that it should be between Rs. 300 to Rs. 500 crore.

Its going fast. @2PM its close to 500 Cr total bid!

Another 3 hrs to go.. do we get 100% in Cat 4.. looks likely though with less than 200% subscription levels yet..

That is not good news 🙁

Where u guys check the bidding update?

Its close to 620 Crore @ 2.58 PM

Source: http://www.bseindia.com/markets/publicIssues/BSEcumu_demand.aspx?ID=784

It is approximately Rs. 143.50 crore in the retail category by 3 p.m.

Sorry, it is Rs. 230.88 crore in the retail category.

In retail category @ 3:42 the total bond subscribed is 341320 – which translates to 170Cr versus 400 Cr ear marked for the category – so we have another 230Cr left – so guess we should see 100% allocation in retail category…

Hi Prashant,

You need to check the “Cumulative Bid Details”. At 4 p.m., it stands at 564,606 bonds * Rs. 5,000 = Rs. 282.30 Crore in the retail category.

Usually one sees hughe jump in the evening. I guess it will cross 400 cr.

Its 157 crore only in retail category.

Check the “Cumulative Bid Details”. It is 464,033 bonds * Rs. 5,000 = Rs. 232.02 Crore.

230 or 157 ?

230 means 400 cr will be crossed EOD. 🙁

Sorry. May be.. I could not understand. There are 6 series. which belongs to retail category.

Series 4, 5 and 6 belong to the retail category.

Thanks Shiv.

You are welcome Rohit!

Retail subscription stands close to Rs. 430.34 crore at the end of the day.

Ok then it looks like we’ll have marginal haircut in the 100% allotment. Anyway just curios, BSE records the timestamp of application and can they not use it as a mechanism to adjudge the allotment even when oversubscribed on Day 1?

Probably they don’t want to make it more controversial/complicated.

sir,

will there be so much rejections that amount will come down to 400 cr

?

Not sure if it would come down to Rs. 400 Crore, but it would definitely be lower than Rs. 430 crore.

we dont want to be like queue for tatkal and parents standing for nursery application forms for kids 😉

Final Figure: Retail Category: 430.34 crore.

All Cat 4 applied today should get 100% allotment going by less than 400% subscription status. Is that right Shiv?

After technical rejection of certain applications, retail category allotment should be very close to 100%, if not 100%.

How much will we get?

Very close to 100% allotment.

what is the overall subscription ? i mean in each category

Thanks sir for the info on NHB bonds. The info on this issue was not available in any sites that I visit or in newspapers. It is because of you that I have applied and hope to get some bonds 🙂

You are welcome Pradeep!

Day 1 (March 7th) Subscription Figures:

Category I – Rs. 195 crore as against Rs. 100 crore reserved

Category II – Rs. 391.59 crore as against Rs. 250 crore reserved

Category III – Rs. 235.07 crore as against Rs. 250 crore reserved

Category IV – Rs. 430.34 crore as against Rs. 400 crore reserved

Total Subscription – Rs. 1,252 crore as against total issue size of Rs. 1,000 crore

So technically they should close the issue tomorrow. What about Cat 3 under subscription will that differential given to Cat 4 or will they take whatever comes tomorrow in Cat 3 and fill it out?

The issue is yet to get closed officially. Such oversubscribed issues did not get closed even on the 2nd day in the past. Normally, these companies close such issues on the 3rd day. I think this issue will remain open at least till Monday on which the category III will definitely get subscribed. So, no scope of category IV getting any cut from category III reserved portion.

Thanks Shiv. You are always prompt with your responses!

Thanks Mr. Subbu for these kind words! 🙂

Hardly it matters since all retail investors will get 93-95% allotment.

Shiv can you pls elaborate the taxation of income received from these bonds….and also is it worth to subscribe these bonds those who falls under 10% bracket

Hi Namdev,

Interest income earned on these bonds is tax free, which is why these bonds are called tax-free bonds. Long term capital gain (LTCG) is taxed at 10% and short term capital gain (STCG) is taxed as per the tax slab of the investor.

If an investor, in the 10% tax bracket, can earn more than 10% elsewhere with this kind of safety & flexibility, only then these bonds are not worth it for investment. However, I find these bonds to be quite attractive for a retail investor.

And also IIHFL bonds will be open for subscription on 12March…can you pls also evaluate that issue…thank u

I’ve already started working on that. I’ll try to complete it by tomorrow.

Hi Shiv,

I would really appreciate if you could include a few lines on comparison with IRFC and REC – the other bonds which people can subscribe to currently.

Regards,

Deepak

Hi Deepak,

Here you have the link to their comparison:

https://www.onemint.com/2014/02/27/8-88-irfc-vs-8-88-rec-tax-free-bonds-february-2014/

IIHFL monthly 11.52% Secured Redeemable NCD can buy @ 970

i.e 3% discount on market & this one coming out Un-Secured ??

mr shiv , pl. cover this point if possible ..

Shiv, I have applied for this issue for 20 years today, looks like will get ‘almost’ 100% allotment (around 95% maybe).

Now if I apply again for 15 years tomorrow day2 (the sum of both subscription is below the cap on retail investment I.e 10 lakhs).

How will the allotment happen Tomm?

Chances of allotment against Monday’s application are very very bleak.

retail (cat 4) is oversubscribed 2.67 times. Do not try to Subscribe for the bonds any more .In case you have already subscribed and have cash in hand might make sense to apply for the rec/ irfc bonds based on the part refund expected from nhb

I understand from Mr Shiv’s subscription figure that, the Category IV (Retail) is oversubscribed by 1.08 times. (430.34/400).

How you arrived the figure of “2.67 times”?

My bad shubh,,i followed the link pasted above which still gives 2.67 (For base issue size of rs 250 cr).

Shiv is correct.. the retail category is just about oversubscribed

http://www.bseindia.com/markets/publicIssues/EODCumlativeShedule.aspx?ID=784

NHB has decided to close this issue tomorrow i.e. on tuesday, March 11th.

http://epaper.financialexpress.com/240639/Indian-Express/10-March-2014#page/5/2

Hi Shiv

I am not sure if this time also people will get close to 100% allotment. Definetly better than last issue for sure. I feel NHB allotment will be complicated this time especially for those who applied for more than 1Lakh. Technically , 93% allotment is feasible. Note that NHB has a bond value of 5000. Mostly likely people who have applied upto 50000 will get full allotment. For those applied above that 85%-90% is what i feel allotment will be. I am expecting 10% refund from NHB. Let me know if you have different view

Regards

Ramadas

Hi Ramadas,

I agree with most of your points and I think a minimum of 95% allotment will be made to each applicant after technical rejections.

Shiv, what does technical rejection imply?

By the way your articles and advice is very timely and helpful. keep up your good work.

Some kind of discrepancy in the application form or mismatch between the bidding info and application info/supporting documents fall under technical rejections.

Also, thanks a lot for your encouraging words !!

Shiv, Cat 3 has no application today!! I guess one more day to go and that small gap may be then given to the Cat 4 which means 100% allotment possibility – keeping fingers crossed 🙂 What do you think?

Rs. 8.82 crore additional investment in Category III today. Either no or very small portion of Category III would get allotted to Category IV.

Hi

Have one doubt. A local cooperative bank is offering 9.25 on FD which they claim is tax-free for members. I am not sure whats the rules on FD interest taxation for cooperatives. Reason am asking is wouldnt this be a better option than tax-free bonds interest wise if you ignore the lock-in. Seek your advise. Thanks

Co-ooperative bank FD interest is fully taxable. Only difference is they are not subject to TDS. Co-operative banks are always more risky than AAA rated tax free bonds or scheduled bank fixed deposits. 9.25% is not a tempting offer either. For debt , i would prefer low risk high return avenues like tax free bonds only. If someone would like to take high risk , better to invest in equity which offers higher risk reward ratio

Regards

Ramadas

Sorry when u say taxable. Taxable in what sense? If no TDS whats the tax? Thanks

Hi Harineem,

Bank/corporate fixed deposits are always taxable. An investor is required to pay tax on its interest income as per his/her tax slab. I think these deposits are liable to TDS as well. I don’t know how they are claiming it to be tax-free. Is it some kind of charitable organisation or they have some special provision under which the interest income is tax-free ??

Co-operative banks do not deduct TDS for sure. Even charitable institutions does not have any provision to offer tax free interest. Charitable institutions at best help claim tax deduction on donations given. Looks like mis-selling from the part of co-operative bank

TDS is tax deducted at source which is 10% when you have PAN. You are supposed to add interest income with your total income and pay tax accordingly. TDS covers only part of the tax unless you are in 10% tax bracket. Looks like co-operative bank officials is using no TDS provision to tell it is tax free.

Regards

Ramadas

Hi Ramadas,

Though I am not 100% sure, but I think co-operative banks do deduct TDS. Please check – http://www.rbi.org.in/scripts/NotificationUser.aspx?Id=8620&Mode=0

Interesting. I didnt know they deduct TDS. Then i have no idea how cop-operative bank can claim no tax. Thanks shiv for the data.

Regards

Ramadas

Thanks Ramadas!

Dear Shiv,

I m keen follower of your posts on onemint.

I have two questions pertaining to Tax Free bonds

1) How are TFBs better than 5 year FMPs. Please consider following

5 Yr FMP is on offer from Stable/reputed MF house. FMP is having strong Portfolio. My Investment horizon is 5 years.

2) There are some issues of TFBs, where NRIs can invest.

If at all NRI is not in india currently, but has given POA to his father, can father sign the form and invest on NRI’s behalf? The investment should be in NRIs name.

The payment can be made from NRO acct of NRI where-in father is mandate holder in the acct or

can father give cheque from his own savings acct from the funds sent by his NRI son

Thanks

Vijesh

Hi Vijesh, I am glad that you follow OneMint regularly !!

1. I think FMPs are great when an investor has a shorter investment horizon than 10/15/20 years, when FMPs provide double indexation benefit, when the investor doesn’t have any liquidity requirements for this investment period and also when the interest rates are ruling higher. The month of March is a great time to invest in FMPs to get double indexation benefit.

Personally, I prefer tax free bonds as they offer reasonable liquidity and scope of capital appreciation. I think interest rates should fall with a stable & strong government at the centre. Also, FMPs invest in securities like these tax free bonds and other corporate debt instruments like NCDs. Why not to invest in bonds/NCDs directly?

2. I am not sure what is the exact procedure for an NRI investment in such a situation. You can mail me your query in detail and let me check if I can help you in this matter.

Thanks a lot Shiv

You are welcome!

Day 2 (March 10th) Subscription Figures:

Category I – Rs. 195 crore as against Rs. 100 crore reserved

Category II – Rs. 391.81 crore as against Rs. 250 crore reserved

Category III – Rs. 243.89 crore as against Rs. 250 crore reserved

Category IV – Rs. 469.48 crore as against Rs. 400 crore reserved

Total Subscription – Rs. 1,300.18 crore as against total issue size of Rs. 1,000 crore

Shiv

It looks like this is missed opportunity for me. If I subscribe IRFC, any chance of allottment there?

Thanks

Yes, you’ll get 100% allotment with IRFC, IIFCL and REC issues.

Thankd shiv.

You are welcome KS!

Dear Shiv, Great work.

I have one query. I had applied for Tranche-I in Physical mode. I have got the Allotment Letter quite some time back, but Certificates have not arrived yet. Can you please provide some input and help me? Thanks.

Thanks Anjan!

I think you should contact the Registrar (Karvy Computershare) to inquire about the same. Contact details of Karvy will be there in the allotment advice. I think they will be able to help you in this matter.

Day 3 (March 11) Subscription Figures:

Category I – Rs. 195 crore as against Rs. 100 crore reserved

Category II – Rs. 391.81 crore as against Rs. 250 crore reserved

Category III – Rs. 247.66 crore as against Rs. 250 crore reserved

Category IV – Rs. 481.94 crore as against Rs. 400 crore reserved

Total Subscription – Rs. 1,316.41 crore as against total issue size of Rs. 1,000 crore

The issue stands closed today. Undersubscription of Rs. 2.34 crore in Category III will get allotted to Category IV investors.

I wantd to know if there is any good tax free bonds that i can invest into now. i hv never invested in TFB before.

Hi Ankur,

You can consider IRFC or REC tax free bonds. Both these issues are offering 8.88% interest for 15 years.

https://www.onemint.com/2014/02/27/8-88-irfc-vs-8-88-rec-tax-free-bonds-february-2014/

Hi Shiv,

If a company buys TFBs from secondary market, will it get the higher coupon rate which was reserved for retail investors?

Thanks

Hi AB,

The company will get a lower rate of interest as the Registrar will pay interest based on the investors’ PAN details.

any news on ratio of allotement?

No news as yet.

Hi Shiv,

I have some tax free bonds which has a step down clause (higher rates for original investor and lower rates if they are transferred.).

I want to close the demat account and transfer the same to some other demat account in my name.

How to ensure that I get the same higher rate even after this transfer?

Also, any clue as to what is the process for closure cum transfer of the demat account as the IndiaBulls is asking for a strange process where I have to submit multiple copies of the client master for each of the bond type.

Rgds,

Anuj

Hi Anuj,

You’ll be paid the due interest tracking your PAN card. If the PAN card remains the same, the allottee is considered to be the first allottee. You need to ensure that your name is exactly the same in both the demat accounts.

I have no idea about the procedure IndiaBulls follows during the transfer process.

Thanks Shiv

You are welcome Anuj!

NHB listing for these bonds expected on which date ??

Listing info is yet to get announced.

Looks like 95 % allotment. Today I see a ASBA debit in my bank acount against NHB.

Thanks SB for this info !!

Yeah got about 4.25% refund, so yes about 95+% allotment. Had applied on day 1 itself.

Thanks RS for this info !! 0.25% is the interest on application money. Allotment is 96%.

people who have invested small amount like 2-3 bonds have got 100% allotment. 😀

Thanks Pradeep for this info !! I think people who applied for up to 9-10 bonds have got 100% allotment.

Gov is doing good job by small investor like me who invest 5-10k happy. 🙂 😀 😉

The bonds have been credited to my demat account.

Are tax free infrastructure bonds ,under 80ccf , still availabe? if so, what are those?

Hi Neelam,

80CCF exemption was available till FY 2011-12 only, after which it got discontinued. So, no infra bonds are available now.

Hi All,

Today I got the NHB Bonds credited to my demat account. Allotment is 90%.

Hi Amlan,

I think it should be more than 90%. How many did you apply for and how many have you got?

Hi Shiv,

It is 10 out of 11.

Hi,

I didn’t get any NHB allotment yet. I had submitted the application very early on the first day itself. No refund either.

Thanks

Hi Ash,

Allotment has started today itself, so you’ll get your allotment in a day or two.

Hi Shiv,

Just received 90% allotment despite applying within the early hour of opening. I am not sure if there is any pattern of allotment.

Thanks

Hi Ash,

Allotment has happened only to those investors who had applied for it on the first day itself. It doesn’t really matter whether you applied for it early in the morning or just before the closing hours of bidding, you would have got allotment in this pattern only. There is a Basis of Allotment for all the equity/debt IPOs, which every company is required to announce. NHB will also announce that very soon.

Hi,

I didn’t mean about morning or evening of the first day. I understand all that. What I meant is within the first day of allotment is varied. So lets see what they come out with.

Thanks

Ya sure, lets see how it goes. I’ll share the allotment basis info once I have it.

Strange that Amlan got 10 out of 11. I have applied and got 24 out of 24 which shows that allocation is at 96%.

But, your allotment makes it 100% George !! Isn’t it ?? I think Amlan’s allotment ratio makes sense to me. My father has also got 96% allotment.

Yes Shiv. I meant 96% allotment. Since 96 % of Rs 120,000 is having balance of less than Rs 5000. If some one applied for 25 bonds , he would have got 24 only. Until 24 it is 100% based on my allotment.

I got 95% allotment whereas my father got only 90% ( 9 out of 10)

Regards

Ramadas

Thanks Ramadas for sharing this info !! I think up to an application for 9 bonds, the investors have been given 100% allotment.

I got 192 out of 200 bonds. I applied on first day. Remaining amount is not yet credited.

Thanks for sharing this info Rita !! Have you checked your bank account, the refunds have got credited yesterday into the bank accounts.

Hi Shiv, I’ve got 96% allotment. Thanks for maintaining a lively blog..

Hi Subbu,

It is because of active participation by you people that this blog has been lively, otherwise I would have been talking to myself the whole time. 🙂

Received 95% allotment. Applied AM on first day

Regards

That’s great, thanks for sharing this info !!

NHB tax-free bonds to get listed on the NSE tomorrow i.e. March 26th, Wednesday.

Here are the NSE codes for the same:

8.50% 10-year bonds – NSE Code – N5

8.93% 15-year bonds – NSE Code – N6

8.90% 20-year bonds – NSE Code – N7

Deemed date of allotment has been fixed as March 24, 2014. Interest will be paid on March 24th every year.

NHB 8.93% tax free bonds got listed on the NSE today. Most traded 15-year option bonds opened at Rs. 5,069, touched a low of Rs. 5,064.50 and a high of Rs. 5,079.99 and finally closed at Rs. 5,073.84.

16,170 bonds got traded on the stock exchange, worth Rs. 8.20 crore.

NHB N6 is showing 9.01% interest bonds @ 5270

how to load it correctly at NSE & BSE

http://www.nseindia.com/live_market/dynaContent/live_watch/get_quote/GetQuote.jsp?symbol=NHBTF2023&series=N6

Mr Shiv ,

thanks so much for being so helpful to all of us.

b/regards .Dr S.K. Agarwal

Thanks Dr. Agarwal !!

It gives me immense pleasure to be helpful to OneMint readers to the best of my knowledge/abilities.

Yes, there is every reason to agree with Dr. Agarwal. Mr. Shiv Kukreja do take pain in R & D and the most important is that he believes in knowledge sharing. Highly appreciated.

Thanks

Regards

Thanks Anand !! It is a big honour for me to get such an appreciation.

Hi Mr kukreja ,

a) NHB – Have received allotment letter,etc. Dec 2013 issue.

b) IRFC – =======Do===========, Jan 2014 issue

Have not yet recvd ‘intimation letters’ with regards to the above. I would like to know whether the cos have sent the ‘Int letters or Bonds’ to the allotment letter holders.

thanks and regards,

F.Rodrigues.

I believe only allotment Advice is sent.That gives allotment Advice No. Appl. No.DP ID No.bonds appled & alloted,ISIN No.dt.of allotment, series of bonds,No. of bonds, amount paid etc.

FYI & regrds

Anand

Hi Francis,

Some companies have sent the allotment letters first, then intimation letters and finally the bond certificates, while others have sent the allotment letters & then the bond certificates (without sending the intimation letters).

I want to know tax free bonds issue to come now by June 2014 on wards.

Hi Subhash,

No issue has been announced by any of the companies which were authorised to issue these bonds in the last few years. In fact, the finance minister Arun Jaitley would announce in his July Budget whether there will be more tax-free bond issues or not.

I am interested to purchase tax free bonds.Please intimate if any are available.

Hi,

No public issue is open as of today, you’ll have to buy these bonds from the secondary markets or privately from an interested seller.

Dear Mr. Shiv

I have bough NHAI tax free bonds- 8.30% two years before. The interest payment is due on 25th june, but still not yet credited. Should I wait or should I take up with them and how.

thanks,

Dear Mr. Srikrishnan,

Interest Payment Date of NHAI 8.30% tax-free bonds is October 1st every year. Please check this link – https://www.onemint.com/2013/07/04/interest-payment-dates-of-tax-free-bonds-issued-during-fy-2011-12-2012-13/

For confirmation of this date, you can contact MCS Limited, the Registrar for NHAI 8.30% tax-free bonds.

Thank you very much. you are correct.

Regards,

Srikrishnan

That’s great, thanks !!

Hi Manshu,

Are there any updates for TFB 2014-15?

what are the current and future prospects for sale of existing TFB in secondary market.

I WISH TO INVEST AROUND RS 15 LAKHS IN TAX FREE BONDS. IS IT BETTER TO WAIT FOR NEW ISSUES OR CAN I GO FOR SECONDARY MARKET.

Hi,

You won’t have any new issue of tax-free bonds this financial year, so you should go ahead and buy these bonds from the secondary markets.

We are senior citizens ( me and my wife).

We need your guidance for investment in tax free high yielding bonds with minimum risk and lowest risk and reasonable liquidity and regular interest payments.

Is there any upper limit for individuals.

Thanks

Dear Shiv,

To arrange money for investing in NHB Tax Free Bonds issue, I had sold some old Tax Free Bonds, in which I had invested more than 2 years ago. In doing so, I had incurred Net Long Term Capital Loss. While filing my Income Tax Return, I have come across the following querries :

1) Like other Long Term Capital Losses, can I carry forward this loss, so that it can be set-off against future Long Term Capital Gains ?

2) While calculating Long Term Capital Loss, can I index the purchase price of bonds ?

3) Which section of Income-Tax is applicable for calculating Long Term Capital Gain Tax on Tax Free Bonds ?

Please guide me.

Thanks

TCB

Dear TCB,

Please don’t mind, but you should consult your tax advisor for such queries as he would be able to study your case in detail and suggest accordingly. You may also avail our tax advisory services for such queries.

Shiv

Considering the rates at which tax-free bonds are quoting, is it a good time to sell? I know you cant predict the future but just wanted your viewpoint on what to consider for making such a decision

Hi Harinee,

I think it depends where you want to reinvest the sale proceeds. If it is fixed deposits or gold, then I think it is not the right time to sell. If it is equities or long-term debt funds, then probably it is a good time to book your profits. Also, I think one should definitely wait for holding period to complete one full year before taking such a decision.

yes mr shiv , hudco9.01 & nhb9.01 trading 25-30 % above issue price

should we sell them huge profit or wait for 1-2-3 year .. how to know

good timing about exit ??

thank you.

S.K.Agarwal

Book profits if you want to invest the proceeds in equities for long term wealth creation, otherwise stay invested for at least 1-2 years more.

Hi Shiv,

What are the good equity avenues that one can pursue at this juncture for long term wealth creating (considering that market is at all time high), some possibilities are 1) Mutual fund NFO- equity oriented (close ended) 2) Mutual fund NFO- equity oriented (open) 3) Existing equity mutual fund with good track record. 4) Direct investment in share market (perhaps not good for average retail investor who is not used to it). What would you suggest?

Regards,

SB

Hi SB,

I think 3rd option is the best & 2nd option is the worst for a retail investor.

I am planning to buy tax free bonds in secondary market. I understand that the current price is more than the face value of Rs 10. But how to calculate or what will be the effective interest rate that one will get if it is bought now?

I read YTM is the key. How to calculate YTM? For some bonds, BSE website shows YTM for other it is not.

Assume if YTM is 7.00 for any tax free bonds (the original interest was 8.71%). If one invests Rs 10 lakhs in that now, does that mean, one will get only Rs 70,000 every year instead of Rs 87100?

Can you let me know? Thanks,

Please check this link – https://www.onemint.com/2012/07/25/how-to-calculate-yield-to-maturity-of-a-bond-or-ncd/

YTM of 7% means your investment of Rs. 10 lakh will ultimately earn 7% for you annually, if it is held till maturity. You’ll continue to get Rs. 87,100 every year as the interest, but on maturity you’ll get Rs. 10 lakh only and not the premium which these bonds are carrying in the secondary markets now and which you’ll be paying if you buy these bonds from the secondary markets. Premium paid for these bonds now will be your loss on maturity.

Thanks. It helps to understand the calculation of YTM. But I am still have a question on interest.

For example, the tax free bond from power finance corp (interest rate is 8.92%) YTM 7.23, the current price is Rs 1192.

If one invests Rs 11.92 lakhs, I assume that this will buy 11.92 lakh/1192 = 1000 bonds. Is it correct?

Then one would get Rs 89200 interest rate on annual basis for the remaining 19 years (based on maturity year 2033). Is it correct?

At the date of maturity (assume one holds until maturity), one will get only Rs10 lakhs back instead of Rs11.92 lakhs. Is it correct?

Can you let me know? Thanks

1. Correct

2. Correct

3. Correct

Thank you Shiv. It is really helpful to understand YTM and secondary market for these bonds.

Comparing this YTM, the new Jeevan Shagun policy from LIC seems better as it offers approx. 8% tax free return. What is your view on this Shiv?

I think insurance should never be compared to a pure investment. LIC Jeevan Shagun will also invest in securities like these tax-free bonds or NCDs or bond funds or other debt securities, will offer high commission to its agents and then pass on the remaining returns to its investors. High commissions always affect insurance returns badly, so it is better to invest in products which carry low management charges and have highly efficient professionals managing them.

Thanks very much for your views.

Regards,

SB

I have sold the bond in the middle of the interest tenure, will I get any pro-rata of annual interest.

Please advise.

No Servesh, you’ll not get any interest.

has interest been received by any one ??

I have not received yet. I wonder if anyone else received it yet. I am hoping should have received by now.

I too have not received. Trust it was due to long Bank holidays

Interest on NHB Tax-Free Bonds will get credited today in your bank accounts.

Thank you. It got credited.

That’s great!

I want bse scirpt code of NHBTF2023 8.90% & NHBTF2014 9.01% bonds please shiv

I want to know BSE script code of NHBTF2023 8.90% & NHBTF2014 9.01% please shiv

Hi Nitesh,

NHB Tax Free Bonds issued in FY 2013-14 are not listed on the BSE.