This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

Gateway Distriparks’ 54.04% owned subsidiary, Snowman Logistics Limited, is coming out with its initial public offer (IPO) from tomorrow i.e. August 26. The company has floated the issue with a price band between Rs. 44-47 per share and is offering 4.20 crore shares during the offer period. The offer will remain open for three days to close on August 28.

At Rs. 47 per share, the company plans to raise Rs. 197.40 crore in the IPO. The face value of its shares is Rs. 10 and thus, the issue commands a premium of Rs. 34-37 to its face value. As the company’s average pre-tax profits in 3 of the preceding 5 years was less than Rs. 15 crore, only 10% of the issue size is reserved for the retail individual investors.

About Snowman and its Operations

Gateway Distriparks owns majority of Snowman Logistics outstanding shares as its shareholding stands at 54.04%. Snowman’s other large shareholders include Norwest Venture Partners VII-A Mauritius (13.78%), Mitsubishi Corporation (12.57%), International Finance Corporation (12.40%), Mitsubishi Logistics Corporation (2.92%) and Laguna International Pte. Ltd. (1.57%).

Snowman is engaged in offering integrated temperature controlled logistics (TCL) services including warehousing and distribution of frozen and chilled products like dairy products including butter and cheese, ice-cream, poultry and meat, seafood, ready-to-eat/ready-to-cook food products, confectioneries including chocolates and baked products, fruits and vegetables, healthcare and pharmaceutical products and industrial products such as x-ray and photo imaging films.

As of March 31, 2014, Snowman carried out its operations having 23 temperature controlled warehouses across 14 locations in India including Serampore (near Kolkata), Taloja (near Mumbai), Palwal (near Delhi), Mevalurkuppam, (near Chennai) and Bengaluru capable of warehousing 58,543 pallets and 3,000 ambient pallets. Further, it had 370 Reefer vehicles consisting of 307 leased and 63 owned vehicles with a total workforce of 1,490 including 383 permanent employees and 1,107 on a contract labour basis.

Snowman has a diversified customer base with top 20 customers contributing approximately 44.10% of its total revenues during FY 2013-14. Its top 20 customers include Hindustan Unilever Limited (HUL), Al-Karim Exports Private Limited, McCain Foods India Pvt. Ltd., Novozyme South Asia Pvt. Ltd., Ferrero India Pvt. Ltd. and Graviss Foods Private Limited.

Objectives of the Issue – Out of Rs. 197.40 crore it targets to raise in this issue, Snowman plans to use approximately Rs. 128.28 crore to set up 6 temperature controlled warehouses and 2 ambient warehouses in various cities including Taloja (near Mumbai), Cuttack, Pune, Mevalurkuppam (near Chennai), Visakhapatnam, Pune and Surat.

IPO Grading – The issue has been graded by CRISIL as 4 out of 5, indicating that the issue is fundamentally above average relative to other listed equity securities. However, this grading is neither a recommendation to subscribe or not to subscribe to the issue nor an opinion of CRISIL whether the issue price is appropriate in relation to the fundamentals of the company.

Minimum/Maximum Subscription – Market lot of the issue is 300 shares and thus the investors would be required to bid for at least 300 equity shares in the IPO i.e. a minimum investment of Rs. 14,100. Retail investors would be able to apply for a maximum of 4,200 shares at the ‘Cut-Off’ price.

Listing – The company will get its shares listed for trading on the National Stock Exchange (NSE) and Bombay Stock Exchange (BSE) within 12 working days from the closing date of the issue.

Risks

* The company is yet to obtain certain approvals/licenses for warehouses for which the funds are being raised through the issue.

* Profitability of the company is quite sensitive to power and fuel costs. Any significant increase in these costs or any continuous or chronic interruption in power supply to the warehousing facilities will have a material adverse impact on its operations.

* The company operates 307 of its 370 reefer vehicles and 13 of its 23 temperature controlled warehouses on lease. For these operations to run smoothly, the company is dependent on third party service providers. Any disruption in operations due to any unforeseen reason might result in below par operating performance.

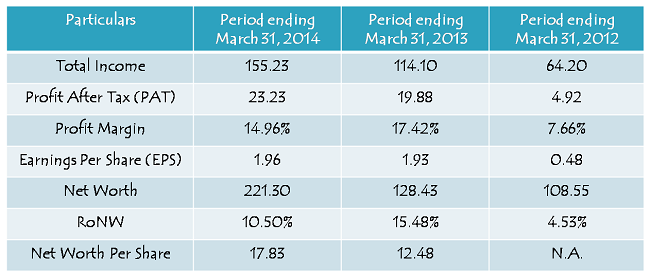

Financials of the Company

(Figures are in Rs. Crore, except per share data & percentage figures)

Anchor Investment – Three Anchor Investors, IDFC, ICICI Prudential and Faering Capital, have been allotted 94.50 lakh shares of the company today at Rs. 47 i.e. the upper end of the price band. IDFC has been allotted approximately 26.6 lakh shares for IDFC Sterling Equity Fund and 3.19 lakh shares for IDFC Infrastructure Fund, whereas ICICI Prudential has been allotted 21.28 lakh shares for ICICI Prudential Growth Fund – Series 2 and 8.51 lakh shares for ICICI Prudential Value Fund – Series 4.

Valuations

Snowman reported a growth of 16.85% in its profit after tax during the last financial year. Assuming a similar growth this financial year as well, the price band of Rs. 44-47 values the company at around 27 times to 29 times on an expanded equity base post-IPO. Considering a short to medium term operating history, these valuations seem to be on a higher side to me.

But, at the same time, considering the cold storage to be a sunrise industry with infrastructure status tag, there is an immense potential of growth and thus, the issue looks attractive with a little risk involved. Though the issue looks attractive from the listing gains perspective, I think the investors should invest in this issue from a long-term perspective. If things pan out well, I expect the issue to generate good returns for the investors over a period of 2-3 years.

Investors would do well to keep a close eye on the company’s operating performance on a regular basis. Any significant deviation from its expected operating performance should be analysed thoroughly.

Same thing happened with me…no shares allotted…

with such euphoria, dont think the stock will list less than 65

but will wait for some correction to enter in it…lets see how it goes?

will it be a next wonderla or just dial..time will tell…

Yes, the mood is upbeat for this issue to list stronger.

Another unlucky applicant receiving mail from Snowman 🙁

I had applied for the least amount of shares 1 lot, i.e. 300 with price 47/- on 28th around 1 pm. Does it make sense to apply for more than 1 lot so that at least you are allotted few shares?

Hoping to get few Sharda Cropchem shares now.

Hi Ketan,

The answer to your question lies in the number of times the issue gets subscribed. With huge subscription, it all depends on the lottery system. Had this IPO got subscribed less than 13-14 times, then you would have got at least some shares. But, I think you’ll get Sharda Cropchem shares for sure, as it got subscribed only 5.85 times in the retail category.

Snowman Logistics will get listed on both the exchanges NSE and BSE w.e.f. tomorrow i.e. September 12, 2014.

Hi Shiv,

Few general query on IPO application.

1. I have only one demat account. Can i apply 2 different application from different bank account ASBA with same DP/client details ? 2lac from one bank and another 2 lac from another bank. Will it get cancelled ?

2. Can I submit ASBA request from my wife’s bank account pointing to my PAN and DP details ?

Thanks.

Hi SD,

IPO allotment happens based on the investors’ PAN. So, it is not possible to apply for more than Rs. 2 lakhs and still remain a retail investor. Moreover, in an equity IPO, you should not submit more than one application as doing that will make your applications invalid and you’ll not be allotted any share.

Thanks for the reply.

I had submitted 3 applications (of course using 3 different PAN numbers of my family members) via maximum possible amount. All 3 applications had 0 shares allotted. Surprised – as this has never ever happened before…in any IPOs of any size 🙁 🙁 🙁

Yes, it is very disappointing when you apply for a good IPO and don’t get even a single share allotted. The new system of allotment is the reason behind it.

I applied for the IPO on the first day itself online via my bank for maximum possible amount (Rs. 1,97,400) and selected cut-off price.

I just got an email from Snowman 3 hours ago on amount allotted and it says 0 shares allotted! Is that possible?

Nothing wrong in the application. Application ha not been rejected.

Hi Sanjay,

Yes, it is possible! With the new method of allotment, the size of the application is irrelevant in an issue with such a huge subscription. The allotment must have been made through a lottery system and you were one of those unlucky applicants who could not get any shares.

Hi Shiv, what’s the probability of allotment of shares v/s numbers applied for at the cut off price?

Hi Shiv,

Did you invest in this IPO?

Last Day (August 28) subscription figures:

Category I – Qualified Institutional Buyers (QIBs) – 16.98 times

Category II – Non Institutional Investors (NIIs) – 221.79 times

Category III – Retail Individual Investors (RIIs) – 41.26 times

Total Subscription – 59.75 times

Hi,

Can you please tell me about allotment and listing date for this IPO ?

Thanks.

Hi SD,

Snowman shares are expected to get allotted and listed on or before 15th September.

Will it be possible to get at ?50 from listed date

Hi Zamir,

This is something which at least I won’t be able to guesstimate.

Day 2 (August 27) subscription figures:

Category I – Qualified Institutional Buyers (QIBs) – 1.49 times

Category II – Non Institutional Investors (NIIs) – 0.82 times

Category III – Retail Individual Investors (RIIs) – 12.94 times

Total Subscription – 2.84 times

What r 2nd day subscribtions

What is 2nd day response

Shall we apply for listing gains

It is widely expected to provide listing gains to its investors, but its not assured.

Day 1 (August 26) subscription figures:

Category I – Qualified Institutional Buyers (QIBs) – 0.62 times

Category II – Non Institutional Investors (NIIs) – 0.34 times

Category III – Retail Individual Investors (RIIs) – 2.70 times

Total Subscription – 0.83 times

Hi Shiv,

How about the criminal proceedings and legal issues with the promoters, and group companies?

Gateway distriparks has a contigency liability in the tune of around 3400 crore against all the total legal issues.

Dont you think its a red flag for the company?

Also how about the competition in the this niche/nascent industry.

It looks Snowman leads this industry space. The other big players are Gati Kausar, coldex, kelvin cold chain, CONCOR subsidiary Fresh and hygine entreprises ltd, and some other logistics company. Out of the above gati and FHEL posted losses in last couple of years. remaining are really very small scale companies, of which financial data is not available.

So investors should take their call based on the above risk and positive future…

Hi Yogesh,

There is no denying that the involvement of promoters and other companies in certain legal matters could affect the operating performance of Snowman adversely, but then I left out this risk bcoz such risks are there with many of the companies and I think this is more of a qualitative risk.

Also, there are very few comparable professional companies in this sector, so, for an investor, what matters most is how well Snowman gets managed.