This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

We keep reading all these days RBI has done this to save rupee from falling further against the dollar or RBI has done that to contain inflation from rising further. Many of us must be wondering all the time what the heck these policy measures are and how do they actually affect our common day-to-day life.

What is RBI’s Monetary Policy? What exactly is the role of RBI in managing money supply in the country? What are RBI’s different tools through which it controls the money supply and other related factors. Through this post, I will try to throw some light on RBI’s monetary policy tools and impact of those tools on the factors which they are targeted on.

Open Market Operations (OMOs) involve sale and purchase of Government securities (G-Secs) by the RBI to adjust the liquidity conditions in the system. RBI conducts such selling operations to suck liquidity whenever it feels there is excess liquidity in the system. Similarly, when the liquidity conditions are tight, RBI goes for such buying operations in the open market, thereby releasing liquidity into the system.

Liquidity Adjustment Facility (LAF) is a policy tool which allows banks to borrow money from the RBI through repurchase agreements, popularly called repo transactions. As the name itself suggests, LAF has been provided to aid the banks in adjusting their day-to-day liquidity mismatches. LAF consists of repo and reverse repo operations. Repo transactions inject liquidity into the system, while reverse repo transactions result in absorption of excess liquidity.

Repo Rate is the rate at which commercial banks borrow money from the RBI for a short period of time. Banks sell their securities or financial assets to the RBI with an agreement to repurchase them at a predetermined price at some future date.

Expected Outcome: A high Repo Rate deters the banks to raise funds from the RBI, forces banks to keep their own lending and deposit rates high and thereby, keeps money supply in check. This is what RBI tried to do on July 16th, which caused panic among the market participants and banks/corporates scrambled to shore up their cash holdings.

Higher interest rates normally curtail investments, as a result of which the overall consumption and aggregate demand start falling. Lower demand results in lower resource utilization. When resource utilization is low, prices and wages usually rise at a more modest rate. On the other hand, RBI purposefully reduces Repo Rate as and when it wants to encourage banks to borrow money for further lending to spur investments.

Reverse Repo Rate is the rate at which banks deposit their excess money with the RBI for a short period of time. RBI lowers the Reverse Repo Rate whenever it wants banks not to deposit incremental cash with it, thereby raise liquidity in the banking system for further lending and to raise overall investment levels and hence the aggregate demand. It also makes banks to offer lower rate of interest on the deposits made by the general public. But, at the same time, it allows banks to lend at a lower rate. Reverse Repo Rate remains fixed these days at 100 basis points (or 1%) below the Repo Rate.

Cash Reserve Ratio (CRR) is the percentage of a bank’s total deposits, which the bank is required to maintain with the RBI. Banks are mandated to deposit this amount with the RBI on a fortnightly basis. CRR is a tool used by the RBI to control the liquidity in the system.

Expected Outcome: So, when there is excess money floating around in the system, RBI will raise the CRR to suck out the excess money. On the other hand, if there is a credit crunch, RBI cuts the CRR to release money into the system. Normally, CRR cut increases liquidity in the system to a marginal extent only.

Statutory Liquidity ratio (SLR) is the proportion of deposits that banks are required to maintain in cash or gold or government approved securities.

Expected Outcome: Similar to CRR, a reduction in SLR also increases some money supply in the financial system. After keeping the required amount for CRR & SLR, the banks are free to use the remaining deposits for their lending purposes.

Marginal Standing Facility (MSF) is a facility provided only to the scheduled commercial banks under which they can borrow funds from the RBI for their overnight liquidity requirements. Banks can do this borrowing only against their SLR holdings, up to 2% of their net demand and time liabilities (NDTL). MSF rate is the rate at which banks can do this borrowing.

Expected Outcome: A hike in the MSF rate can raise banks’ cost of borrowing for their overnight liquidity requirements under the MSF window. At the same time, a cut in the percentage of NDTL, up to which the banks can borrow funds from the RBI, can squeeze liquidity for these banks. So, these two simultaneous steps mean a double trouble for the banks.

Till July 16th, MSF rate was fixed at 1% above the Repo Rate i.e. at 8.25% (7.25%+1%). At present it has been hiked to 3% above the Repo Rate i.e. 10.25%. Also, the RBI has cut the borrowing limit under MSF on two occasions in July, once from 2% to 1% and then from 1% to 0.5%, in order to squeeze liquidity from the markets and curb speculative trades in the currency market.

Impact on Your Investments

Equity Investments like Stocks, Equity Mutual Funds – A cut in the interest rates by RBI is always cheered by the stock markets and equity investors as this step reduces interest expense burden of the companies listed on various stock exchanges and thereby increases their profitability.

Financial Sector including Banks, Housing Finance Companies (HFCs) & NBFCs: Again, a cut in the interest rates boosts the business growth, profitability and net interest margins (NIMs) of the financial sector companies. Banks, HFCs, auto loan companies etc. get benefitted as it increases loan demand from its borrowers and also increases their margins.

Auto Sector, Real Estate Sector & Consumer Durable Sector Companies: Companies, which are in the businesses of auto or auto ancillary, real estate and consumer durables, get benefitted with a fall in interest rates as it reduces the borrowers’ overall cost of taking a loan and thus increases the demand for these companies’ products used by their customers.

Market-linked Fixed Income investments like Gilt Funds, Income Funds, Tax-Free Bonds or NCDs – There is an inverse relationship between interest rates and bond prices. When interest rates go up, bond prices fall and when interest rates fall, bond prices rise. RBI’s policy measures influence movement of bond yields, both government as well as corporate. Your market-linked investments like debt mutual funds, NCDs and tax-free bonds also get affected due to these measures. The value (or market price) of these investments goes up with a cut in the policy rates and vice-versa. The higher the quantum of rate cut and the more unexpected it is, the more will be the jump in the value of your investments.

Investments in gilt funds, which in turn invest in government securities (G-Secs) primarily, and investments in income funds, which invest in corporate bonds primarily, could give higher returns to the investors as the interest rates decline and their prices go up. Your direct investments in tax-free bonds or corporate NCDs also appreciate in value due to a cut in the RBI’s policy rates and a subsequent fall in their yield to maturity (YTM). This results in a gain in your overall bond portfolio.

Fixed Income Investments like Bank FDs, Company FDs or Post Office Schemes – A reduction in RBI’s policy rates does not affect your existing investments in FDs or Post Office schemes at all because these investments are not market linked and the interest rates, you are eligible to get, do not change. But, at the same time, it signals a likely fall in the interest rates on these FDs in the times to come.

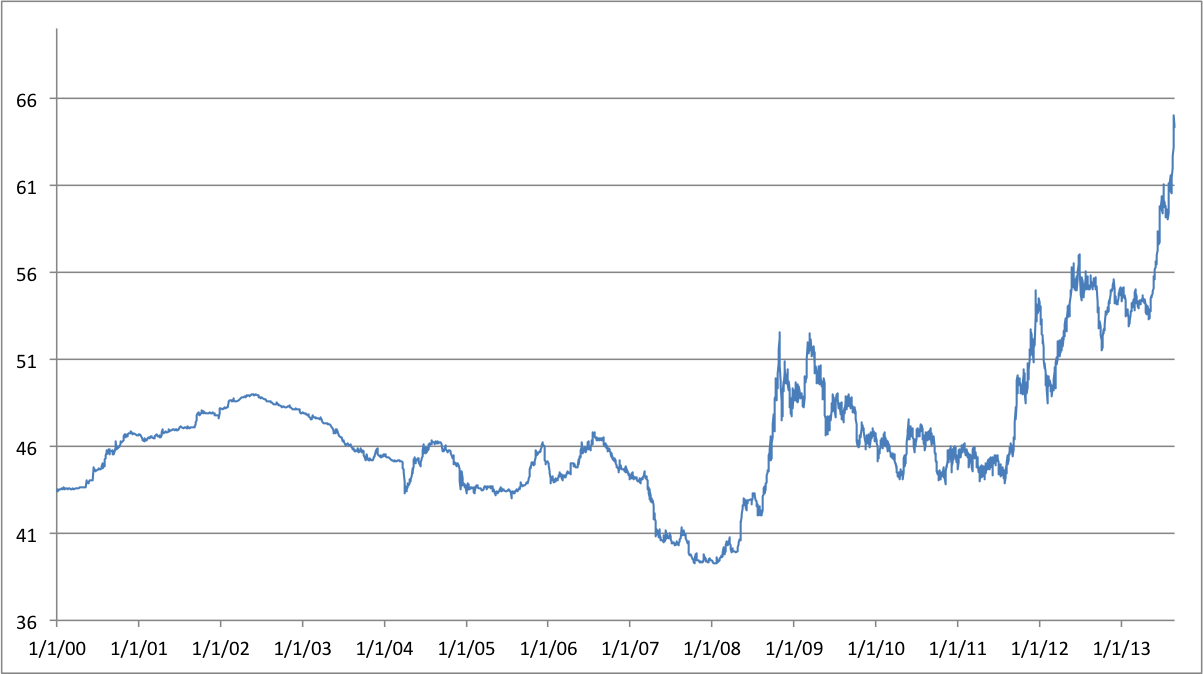

Indian Currency (Rupee) – All those measures, which the RBI takes to absorb liquidity in the system, result in reduced supply of rupee in the markets as compared to the other global currencies. This reduced supply of rupee should ideally result in higher value (or appreciation) of Indian currency against other global currencies.

So, if the present situation is tough, if it is making the interest rates go higher, share prices and NAVs of your investments in mutual funds go down, then it should be taken as part of a cycle which keeps on changing with moving times. With a change in the decision-making authority at the RBI, people are again expecting something dramatic to happen for their bleeding portfolio values. Lets see what Mr. Raghuram Rajan has in store for us during his tenure as the Governor of RBI.