IIFL 12% NCDs vs. HUDCO 8.76% Tax-Free Bonds – which one is better to invest?

This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

Two debt issues opened for subscription on September 17 – India Infoline Finance Limited (IIFL) 12% NCDs and HUDCO 8.76% Tax-Free Bonds. Both these issues have seen reasonably good response from the investors. But, still there are many people who have not been able to take a decision and probably require some more help or some detailed research. Let us try to do a comparative analysis of the two.

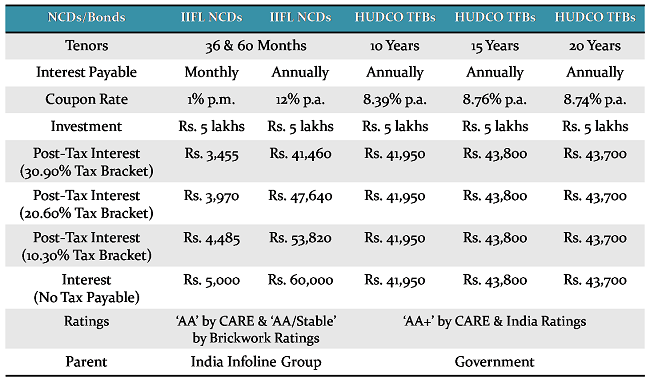

A couple of days ago Vijay asked me to illustrate IIFL NCDs with a numeric example, involving rupee values of return.

Vijay September 17, 2013 at 10:26 am

Can you illustrate IIFL with some numeric example. I am sure, most of the reader does not understand yield definition very well.

As I did not want to edit the original post, I could not fulfill his desire. But, now I can get his request fulfilled by comparing numeric examples of both IIFL NCDs and HUDCO tax-free bonds.

There are many factors which should determine your decision and I am going to state those factors here:

Maturity Period – As interest rates hit troughs, the investors should go for the shortest possible period of investments and when interest rates hit peaks, the investors should go for the longest possible period of investments. Though it is very difficult to determine these troughs and peaks, I think the current period is one of those of higher interest rates in the recent history with the 10-year G-Sec bond yields crossing 9% psychological mark.

IIFL has a maturity period of 36 months & 60 months, whereas HUDCO is available with tenors of 10 years, 15 years and 20 years. So, which one should you invest in? If you think there is still more room for interest rates to rise, you should go for IIFL NCDs and if you agree with my view on the interest rates, then you should go for the HUDCO 20-year or 15-year bonds.

Coupon Rates & Taxability – While HUDCO is offering tax-free interest rates of 8.74%, 8.76% and 8.39% for 20 years, 15 years and 10 years respectively, IIFL has fixed a single taxable rate at 12% for both of its maturity periods, 36 months & 60 months.

Investor’s Tax Bracket – First, you should determine your income tax bracket for the current financial year and try to foresee it for those financial years also till which you are planning to stay invested in these NCDs/bonds. If you fall in one of the higher tax brackets, then I think it is better to invest in HUDCO tax-free bonds as paying tax on 12% interest income from IIFL would make it 8.29% in the 30% tax bracket and 9.53% in the 20% tax bracket.

I would say earning 8.76% with tax-free bonds with safety of a government company and ‘AA+’ rating clearly makes me favour HUDCO bonds. If one is not liable to pay any tax on the interest income earned, then only I think IIFL NCDs would score over HUDCO bonds. It is up to the investors to decide if they fall in the 10% tax bracket.

Frequency of Interest Payments – While IIFL is offering annual as well as monthly interest payment options, HUDCO has only one interest payment option and that is annual. It makes IIFL NCDs attractive for those investors who want monthly interest payment option.

Ratings, Safety & Business Model – IIFL NCDs are rated ‘AA’ while HUDCO bonds are rated ‘AA+’, a difference of just one notch. But, practically there is a lot of difference. IIFL is a private company and a 98.87% subsidiary of India Infoline Group. It is a relatively newer company with business model concentrated in two major segments, mortgage loans and gold loans.

HUDCO is a wholly-owned corporation of the government of India. It has a relatively stable business model with financing of housing and urban infrastructure in many major cities across India. IIFL’s business model is relatively riskier than HUDCO. This factor also goes in HUDCO’s favour.

Issue Size – While HUDCO is planning to raise Rs. 4,809.20 crore from its issue, IIFL wants to raise Rs. 1,050 crore. How the issue size matters? The bigger the issue size, the higher is the liquidity in the secondary markets. Higher liquidity provides easier exit option to its investors. So, I think the issue size is also positive for HUDCO bonds.

Listing – While the issue size of IIFL is smaller than HUDCO’s issue size, it is going to list on both the stock exchanges, Bombay Stock Exchange (BSE) as well as National Stock Exchange (NSE). HUDCO bonds are going to list only on the BSE. Though the issue size of HUDCO is big and there will not be any liquidity problem as such, but still it would have been better if the company could have got it listed on the NSE as well. This augurs well for IIFL NCDs.

While the whole world cheers the US Federal Reserve’s policy decision not to taper QE3 and to keep its bond-buying programme steady at $85 billion per month, I think it presents a perfect platform to the Governor of RBI, Dr. Raghuram Rajan, to bring back the much awaited normalcy in the Indian bond and currency markets. If he succeeds in doing that, I think the bond investors are up for a really good time. They should then be subscribing to these bonds at these really attractive interest rates.

IIFL just lost huge amount of money (its own or its investor’s money) in the NSEL ‘investment’. I wouldn’t hand over my money to them.

Though India Infoline Finance Limited (IIFL) is a subsidiary of India Infoline Group and is not affected directly by such an incidence, but that is what makes private companies riskier than HUDCO – their business model.

Generally I go by trust. For e.g,. we can trust brands like Tata, L and T.

Brands generally get created by good management and good governance, so it is very important to have a good management.

Thanks Shiv for the explnations.

People dont know when is HUDCO issue is opening, let us know if u hav any details on this.

Or Post it as and when you come to know.

Thanks in Advance !!!!!!

I came across a post, though its not related to Bonds, but was an intresting read on Mutual Fund Activities, and would be helpful to equity market readers.

http://www.quantspartner.com/MFInvestments.aspx

•In Aug-13, Indian fund managers perceived Axis Bank & Bharti Airtel at deep discount. They had unanimous consensus, so there was rush among all AMCs to buy these two stocks. Domestic AMC’s collectively bought Axis Bank worth of Rs 617 cr and Bharti Airtel worth of Rs 479 cr from other market participants.

•It seems Reliance AMC, is not positive about the future prospects of Tata Steel and Tata Motors, as they sold-off almost entire holding in these two Tata group companies. Similarly, they reduced significant holding from another index stock, namely ONGC

•Classic activity of Reliance AMC is on Strides Acrolab, where they made quick gains and just moved on. Stock fell by 33% in July-13 and they increased holding significantly. In Aug-13, stock rose by 49%, and they sold a large chunk of holding, even after that they are left with the same holding value which they had as on July 1, 2013.

•In July-13, Reliance AMC and SBI AMC had opposite view on Strides Acrolab, in Aug-13 they had opposite view on Triveni Turbines. Reliance exited from the stock; however SBI significantly increased the holding.

•Franklin Templeton is the only AMC which added new stocks in their portfolios. They bought Asian paints, Cipla, Shree Cement and Hero Motocorp. Incidentally, DSP BlackRock holds opposite view on Shree Cement as they sold equivalent shares. In July-13, Hero Motorcorp was the top pick of most Fund Managers.

•DSP BlackRock exited from Sun Pharma, which is the most preferred and valued stock in pharma space. They also exited from Glenmark, in which they had investment equivalent to Sun Pharma.

•Birla and Reliance are the only two AMC which were holding Financial Technologies as of July-13, however, it seems that FMs at both AMC foresee only dark future ahead for this company, and consequently sold-off shares in Aug-13.

•Yes Bank was another popular counter among 3 AMCs viz. SBI, FT and Birla. All that Birla sold was absorbed by SBI & FT.

•In midcaps, HDFC picked up Amara Raja Batteries and almost doubled their investment from Rs 51 cr to Rs 105 cr.

•UTI holds positive outlook for Technology and especially for I.T., as 6 out of Top 10 buys are Wipro, HCL Tech, Bharti Airtel, TCS, Tech Mahindra and Infosys.

Thanks Lalit!

People and I already know when HUDCO issue is opening, but probably you do not know that I have already covered it. Please check it for your reference.

https://www.onemint.com/2013/09/14/hudco-8-76-tax-free-bonds-issue-september-2013/

Thanks Shiv

I was checking on NSE

http://www.nseindia.com/products/content/equities/ipos/homepage_ipo.htm

its not apperaing there under current issue, but I found it on BSE.

I hav another unique query,

Form should be filled on Name as Appearing on PAN Card or As Apperaing on Bank Statement

Form should be filled as per your the PAN Card.

Ok so Bank will not Reject the cheque citing reson as difference in Name. Bascically, My wife name has changed post marriage. Name on Bank account and Demat account is New Name and Name on PAN Card is her maiden name.

So, I was worried If Bank reject the Cheque and application dont get process.

Someboday said it should be as per Your Demat Account, which is same as Bank Account Name.

The demat account name should be there as per the PAN card name and if somebody is applying these bonds in the demat form, then the application form should be filled as per the demat account name and linked bank account details.

Ok. Thanks a Lot !!!!!

You are welcome!

excellent info Shiv! thanks a lot.

Thanks Kishor!

hi Manish/shiv

Long term bonds provide higher tax free rates. so it is better to go for 15-20 year tenures rather than 10 yr tenure, even if you intend to keep them for 10 years only, because you can always sell them on the secondary market and pay LT Cg tax after 10 years?

now as interest rates are rising still, can we expect Tax free bonds with interest higher than Hudco?

kindly provide expert comments.

Hi Ramesh,

Yes, even I think so that it is better to go for a higher tenure bonds out of the three options available. I think for other bond issues to offer even higher rates, the 10-year G-Sec rate has to cross the 9% mark once again.

Dear Shiv,

India Infoline brokerage was providing finance for leveraging trades in NSEL to its customers. I am not sure whether the financing done by India Infoline or India Infoline Finance. Do you have any information ?

If the financing was done by India Infoline Finance, does it increase risk to the investors of the present issue of NCDs ?

The company has announced that present issue is closing on Monday, 26th Sept which is well before the scheduled closing date. Response from all categories of investors, including QIBs has been better than most of the recent issues of NCDs. What is the reason for such good response ?

QIB portion, which remained under-subscribed for REC Tax-Free Bonds (where they were getting upto 12.6% effective pre-tax yield), may be fully subscribed in India Infoline Finance NCD issue. Why QIBs have favoured India Infoline Finance NCDs over REC tax-free bonds ?

Thanks

TCB

Hi TCB,

As per the prospectus for this issue, none of the companies in the India Infoline Group, including IIFL, has funded any client positions on NSEL.

There has been an improvement in the financials of IIFL over its last years’ performances. All categories of investors, including QIBs, are quite familiar with the working style & business model of India Infoline Group companies. Also, I think IIFL issue has been marketed quite well by the company. Probably these are the reasons why people have shown a good response to this issue over SREI issue or Muthoot issue.

Before its public issue, REC did a private placement of its tax-free bonds worth Rs. 1,500 crore. I think QIBs participated in that placement and that is why they did not invest much in the public issue.

Dear Shiv,

In above post, I have written “Monday, 26th Sept.” by mistake. Please read it as “Monday, 23rd Sept.” which is the issue closing date.

For retail applicants, what is the chance of getting allotment, if applications are submitted on Monday (23rd Sept.) ?

Thanks

TCB

Hi TCB,

As per a SEBI letter issued to IIFL, in case of oversubscription, the allotment to the applicants will be made on a proportionate basis on the date of oversubscription. So, keeping that in mind, I think the retail applicants, submitting applications on Monday, will get 50-100% allotment of their subscription, depending on the quantum of applications submitted.

Approximately Rs. 142.15 crore (Rs. 525 crore – Rs. 382.85 crore) is still left for the retail investors. If they apply for Rs. 142.15 crore or less on Monday, they should get 100% allotment.

Dear Shiv,

Thanks for your reply.

Is there any way to find out which tenure of NCDs are being opted for by how many applicants ? In other words, which tenure has a higher demand ?

Same question for HUDCO bonds also, because in one of your posts you have mentioned to go for the tenure which is has higher demand, so that liquidity would be better.

Thanks

TCB

Dear Shiv,

If it is possible to get the above details, please also tell me, which option – monthly interest or annual interest is having a higher demand ?

Thanks

TCB

Dear TCB,

Please check these links:

http://www.bseindia.com/markets/publicIssues/DisplayIPO.aspx?id=713&type=DPI&idtype=1&status=L&IPONo=770&startdt=9/17/2013

http://www.bseindia.com/markets/publicIssues/DisplayIPO.aspx?id=714&type=DPI&idtype=1&status=L&IPONo=771&startdt=9/17/2013

Click on the “Cumulative Bid Details” and you’ll get your answers.

Dear Shiv,

I have read all the your explanation on the IIFL NCD and HUDCO tax free Bonds. It is so informative that, like a small retail investor like me it is very useful. On the your judgements I can make my decision where I can put my money in safer options.

Thanks

A.V.Sarode

Thanks a lot A.V. for your kind words! It is my pleasure if I could help you in taking such decisions!

I need to invest Rs.1Lac for the children for about 10 years to get more interest, but on net I seen IIFL has closed the NCD issue,is it true? if yes then what abt HUDCO or any good scheme will come in near by.

Hi Mr. Bhagwan,

Yes, IIFL NCDs issue has got closed yesterday. HUDCO issue is open till October 14th. Shriram Transport Finance NCD issue with a similar interest rates is expected to open in the near future. IIFCL & PFC tax free bond issues should also open in the next 5-15 days.

sir, pl. let me infirm where i can collect the required application form for purchase hudco tax free bond

Hi Mr. Sen,

There is no issue open for HUDCO tax-free bonds and that is why you cannot apply for it. If you want to invest in HUDCO tax-free bonds, you need to buy them from the secondary markets.

Your article helped me a lot, is there any more related content? Thanks!