India Infoline Finance Limited 12% NCDs Issue – September 2013

This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

So, the next company in line to issue non-convertible debentures (NCDs) is India Infoline Finance Limited (IIFL), a 98.87% subsidiary of India Infoline Limited (IIL). It is the same company which issued 12.75% unsecured NCDs last year in September and 11.90% / 11.70% secured NCDs in August 2011. I will talk about its past issues later in the post, but first let us check out the features of its current issue.

This year the company is offering 12% interest rate, across two maturity periods – 36 months and 60 months. The issue will open next week on September 17th and is scheduled to close on October 4th, but if required, the company may extend the closing date of the issue, depending on the investors’ response.

The company plans to raise Rs. 1,050 crore from this issue, including the green-shoe option of Rs. 525 crore. The issue size looks fairly large to me and the company plans to use these proceeds for its financing activities and business operations and also to repay its existing loans.

Categories of Investors & Basis of Allotment – The investors have been classified in the following three categories and each category will have certain percentage of the issue reserved for the allotment:

Category I – Institutional Investors – 40% of the issue is reserved

Category II – Non-Institutional Investors (NIIs) – 10% of the issue is reserved

Category III – Resident Indian Individuals (RIIs) – 50% of the issue is reserved*

* Out of 50% reserved for Category III, upto 40% of the issue will be allotted to the resident individual investors who apply for these NCDs aggregating to a value not more than Rs. 10 lakhs and upto 10% of the issue will be allotted to those resident individual investors who apply for these NCDs aggregating to a value of more than Rs. 10 lakhs. The first sub-category is called “Reserved Individual Portion” and the second sub-category is called “Unreserved Individual Portion”. In a way, the second sub-category is for HNIs.

Non-resident individuals (NRIs), on repatriation as well as non-repatriation basis, and Qualified Foreign Investors (QFIs) are also eligible to invest in this issue. NCDs will be allotted on a first-come-first-serve basis.

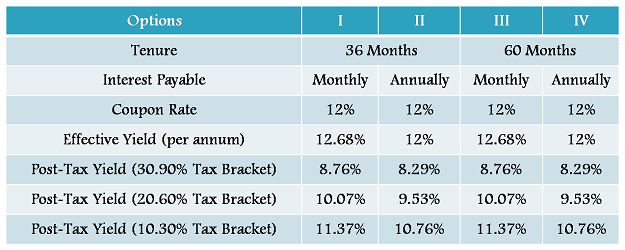

Rate of Interest and Tenors

Unlike Muthoot NCDs issue, which is very complicated due to its XI interest options, IIFL has kept its issue fairly simple. There is only one interest rate to deal with and that is 12% per annum. Also, there is no cumulative interest option this time and the interest will be paid either annually or on the first day of every month.

Like its previous issues, the company has kept equal coupon rate for all the categories of investors – institutional, non-institutional and the retail investors. Also, there are only two maturity periods – 36 months and 60 months.

Minimum Investment – Minimum investment requirement has been kept at Rs. 5,000 i.e. 5 bonds of face value Rs. 1,000 each.

Ratings & Nature of NCDs – CARE has assigned ‘AA’ rating and Brickwork Ratings has given ‘AA/Stable’ rating to this issue. Unlike last year, these NCDs are secured in nature and that ways, the claims of the investors this year will be superior to the claims of those investors who invested in its 12.75% NCDs last year.

Listing, Demat & TDS – These NCDs are proposed to be listed on both the exchanges, National Stock Exchange (NSE) as well as Bombay Stock Exchange (BSE). Resident investors have the option to apply these NCDs in physical form as well as demat form. But, NRIs will compulsorily require demat accounts to apply for these NCDs.

It is a standard statement for the taxable NCDs. The interest earned will be taxable as per the tax slab of the investor and TDS will be applicable if the interest amount exceeds Rs. 5,000. But, NCDs taken in the demat form will not attract any TDS on the interest income.

Profile & Financials of India Infoline Finance Limited

India Infoline Finance Limited is a credit and finance arm of the India Infoline Limited group and provides loan against property, housing loans, gold loans, commercial vehicle loans, loan against securities/margin financing and medical equipment financing to its corporate clients as well as retail clients.

IIFL has a strong network of 1,403 branches all over India and has a total loan portfolio outstanding at Rs. 9,464 crore as on June 30, 2013. The loan book of the company has grown at a CAGR of 79.3% over the last three years.

Total income, on a consolidated basis, registered a growth of 82%, from Rs. 954 crore for the period ended March 31, 2012 to Rs. 1,737 crore for the period ended March 31, 2013. Net profit for the same period registered a growth of 80%, jumping from Rs. 105 crore to Rs. 189 crore. Net interest income (NII) also jumped 81%, from Rs. 429 crore to Rs. 776 crore.

As far as its asset quality is concerned, the company has done a reasonably good job in a difficult economic environment. Gross NPAs of the company as on March 31, 2013 stood at 0.49% as compared to 0.56% as on March 31, 2012, while Net NPAs were at 0.17% as against 0.40%. Net NPAs to net worth ratio improved from 1.84% to 1.03% during the same period.

You can check the financial results of IIFL for FY 2012-13 from this link.

Previous Years’ IIFL NCDs

NCDs issued last year and in 2011 are trading at a yield higher than the coupon rates offered by the company in the current issue, except its N1 NCDs. You can check the yields and their respective prices from the table below:

So, going by the yields of its previous issues, I think it is better to buy IIFL’s NCDs from the secondary markets.

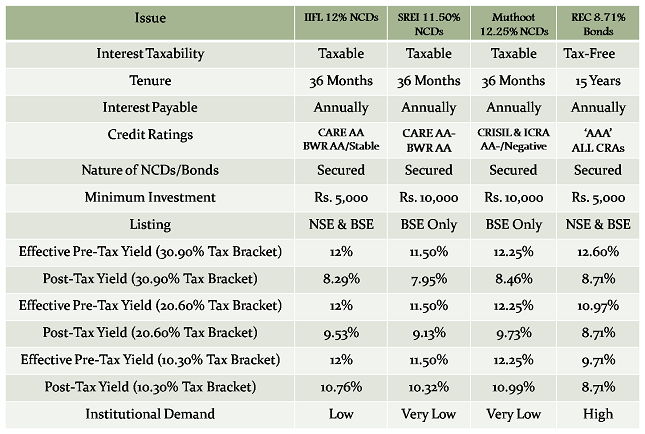

Comparison of NCD/Bond Issues open for subscription

If you want to make some investment in any of the NCDs or bonds which are open for subscription, then here are four such options – IIFL 12% NCDs, SREI 11.50% NCDs, Muthoot 12.25% NCD and REC 8.71% Tax-Free Bonds. The table below has some features which are comparable to these four issues. I have taken 36 month, annual interest options for the first three issues to make them comparable.

Though REC bonds issue is the odd one out, but then it makes the investors think why or why not tax-free bonds. If I were to invest in any of these four options, I would have gone for REC tax-free bonds, due to its safety, liquidity, tradability, tax-free interest, long duration, scope of capital appreciation, high institutional demand etc. Which one would you go for?

Hi Shiv

Even though the yield is higher for NCDs from secondary market, but from taxation perspective, the cost of acquisition would be considered as the Face Value (1000) and not Market Purchase Price (eg. 1038 for N4), so the post tax returns may not necessarily better than those bought in the primary market. Your thoughts on this ?

I am talking about the case where NCDs bought in secondary market are held till maturity.

Hi Ramprakash,

Your cost of acquisition would be the market purchase price and not the face value, if you buy these bonds from the secondary markets.

Hi Shiv,

Thanks for the timely article.

You mentioned, it is better to buy the previous issues of IIFL NCDs form the secondary market instead of current offering. But the ones that you have listed/compared, higher yield (12%plus) is for only unsecured NCDs. I would prefer to go for the Secured.

Also, there could be slight listing gain. I think current lot of “Secured, monthly 12%, getting the same at the face value” is better compared to other offerings of IIFL.

Let me know if I’m missing anything.

Thanks,

Vikas

Hi Vikas,

IIFL NCDs issued during FY 2011-12, N1, N2, N3 & N4, were all ‘Secured’, while those issued last year, N5, N6 & N7 were all ‘Unsecured’.

With the kind of supply, at 12% coupon rate, I dont think there would be listing gains. 12% per annum from IIFL is slightly unattractive to me in the current interest rate environment. Monthly interest option is better.

Thanks Shiv.

After further research, I have decided to go with HUDCO offering..:-)

Vikas

Great !!

Can you illustrate IIFL with some numeric example. I am sure, most of the reader does not understand yield definition very well.

Hi Vijay,

What kind of illustration do you want? I mean what exactly should be there in the example?

Something like.. what would be return if 50000 invested in different options… what is the rupee value of return…. basically inr example instead of only yield

Not a good idea to do it now in the post, probably will do that with upcoming issues.

IIFL has decided to preclose the issue on Monday, September 23.

Thanks Shiv for the analysis. Would be great if you can keep us posted on the listing date of these NCDs – and also the HUDCO ones.

Sure AB, I’ll do that.

IIFL NCDs to list on the NSE and BSE on October 8th i.e. Tuesday. Here are the NSE & BSE codes for the respective Series:

Series I – 36M Monthly Interest Option – NSE Code ‘N8’ — BSE Code – 934911

Series II – 36M Annual Interest Option – NSE Code ‘N9’ — BSE Code – 934912

Series III – 60M Monthly Interest Option – NSE Code ‘NA’ — BSE Code – 934913

Series IV – 60M Annual Interest Option – NSE Code ‘NB’ — BSE Code – 934914

IIFL NCDs got listed at Rs. 1,000 today, hit a high of Rs. 1,002 and a low of Rs. 993.

Dear sir

I have allotted 200 Ncds category -111 reserved on 30/9/2013,

Interest is credited to my bank ac up to April 2016, after April int no credited to my account.

When I will get reduction amount . Conform.My allotment advice no is 251000000422. Pl clarify.

Yours

Netaji

dear sr.

very tedious job to encash 25 alloted ..sbmib series.2012ncd bonds.

tell me hovv to vvithdral..?