This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

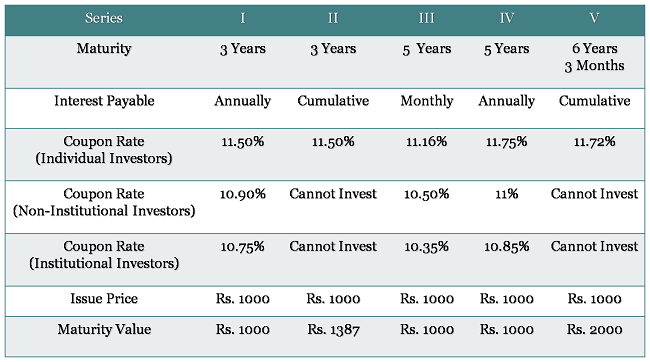

SREI Infrastructure Finance Limited is going to launch its second public issue of non-convertible debentures (NCDs) of the current financial year 2013-14 from Monday, August 24th. It is going to offer a maximum of 11.75% per annum to the individual investors for 5 years tenor and a minimum of 10.35% per annum to the institutional investors for 3 years tenor.

SREI Infra plans to raise Rs. 200 crore from this issue, including the green-shoe option of Rs. 100 crore. The issue is scheduled to close on September 17th or earlier, depending on the response for the issue. NCDs will be allotted on a first-come-first-serve basis.

Categories of Investors & Basis of Allotment – The investors would be classified in the following three categories and each category will have certain percentage fixed for the allotment:

Category I – Institutional Investors – 20% of the overall issue size

Category II – Non-Institutional Investors (NIIs) including corporates – 20% of the issue

Category III – Individual Investors including Hindu Undivided Families (HUFs) – Rest 60% of the issue

NRIs and foreign nationals among others are not eligible to invest in this issue.

Tenors and Rate of Interest

SREI came up with its first issue in April this year and as compared to that issue, the second issue looks attractive from the retail investors’ point of view. As compared to 10.75% for 3 years and 11% for 5 years in its last issue, this time the company is offering 11.50% and 11.75% respectively.

The bonds will be issued for a tenor of 3 years, 5 years and 75 months (6 years and 3 months) with monthly interest, annual interest and cumulative interest options. The monthly interest option is available only with 5 years period and will carry coupon rate of 11.16%, which effectively is 11.50% per annum.

“Double Your Money” Option – Series V NCDs offer to double your money in a period of 6 years and 3 months and effectively yield 11.72% per annum. Though it is quite attractive to hear doubling of money, I think it is better to go for shorter tenors in case of company NCDs.

Ratings & Nature of NCDs – CARE has assigned ‘AA-’ rating and Brickwork Ratings has given ‘AA’ rating to this issue. Moreover, these NCDs are secured in nature and the claims of its investors will be superior to the claims of any unsecured creditors of the company.

Listing, Demat & TDS – These NCDs are proposed to be listed on the Bombay Stock Exchange (BSE) only. Investors have the option to apply these NCDs in physical form as well as demat form, except for Series III NCDs, which carry monthly interest and will be allotted compulsorily in the demat form.

The interest earned will be taxable as per the tax slab of the investor and TDS will be applicable if the interest amount exceeds Rs. 5,000. But, NCDs taken in the demat form will not attract any TDS on the interest income.

Minimum Investment – There is a minimum investment requirement of Rs. 10,000 i.e. at least 10 bonds of face value Rs. 1,000.

Profile & Financials of SREI Infrastructure Finance Limited – SREI was initially registered with the RBI as a deposit taking non-banking financial company (NBFC). Effective March 31, 2011, SREI got converted into non-deposit taking NBFC and the RBI classified it as an Infrastructure Finance Company (IFC). Later, SREI got notified as a Public Financial Institution (PFI) by the Ministry of Corporate Affairs.

The company provides financial services to its customers engaged in infrastructure development and construction, with particular focus on power, road, telecom, port, oil and gas and special economic zone (SEZ) sectors in India with a medium to long term perspective.

SREI has a national presence with a network of 198 offices all over India and over Rs. 33,330 crore of consolidated assets under management (AUM). SREI’s loan disbursements have grown at a CAGR of approximately 44% in the last four years, with consolidated disbursements of Rs. 15,667 crore for the period ended March 31, 2013 and Rs. 18,600 crore for the year ended March 31, 2012.

Total income on a standalone basis for the period ended March 31, 2013 and March 31, 2012 stood at Rs. 1,666 crore and Rs. 1,181 crore respectively. Net profit for the same periods was registered at Rs. 94.96 crore and Rs. 57.96 crore respectively.

The grey area, with which the whole of the infrastructure finance industry is suffering, has also affected SREI Infra badly. Gross NPAs of the company as on March 31, 2013 stood at 2.77% as against 1.58% as on March 31, 2012, while Net NPAs were at 2.30% as against 1.18%.

SREI Infra NCDs are definitely better than some of the riskier company FDs like Unitech, Gitanjali Gems, Jaiprakash Associates or other lesser known companies. Investors, who are willing to take low to moderate risk and looking for higher returns than bank FDs or comparable company FDs, can think of investing in these NCDs. But, I think it should not be more than 5 to 10% of your total debt portfolio. Investors in the 30% tax bracket should definitely wait for the tax-free bonds or go for the tax-efficient debt funds or FMPs, as these investments should result in higher effective yields for them.

This is an interesting topic and is something that I’ve given some thought to myself. I won’t restrict myself to the question about the second stream of income, but share some things about this topic that people who have taken this course have told me about, and I feel are important as well.

You need to save to invest

Let’s start with the basics, which I find is hard for a lot of people to do. If you have credit card payments due or have a big car loan or home loan that has an installment due every month then you are probably not saving very much money. If you aren’t saving a lot of money then you can’t invest anything to create a second stream of income in the first place.

You can only save money when your expenses are low, so I believe low expenses are the foundation of this attempt.

Not all earned money is equal

Since we are so used to paying taxes, often we don’t realize how big of a piece the government actually takes. So when you save money that’s actually worth a lot more than making that much extra money in salary because you don’t pay taxes on savings.

Similarly taxes on mutual fund capital gains and FMPs are less than the marginal rate so any income you get from that source is worth a lot more than your salary.

Lastly, when you do a calculation of how much your startup income should be to replace your salary income, consider your take home pay, and not your gross salary. From your take home pay deduct your savings, and usually this should be a comforting number because it is a lot less than simply dividing your gross salary by 12 and hoping your new enterprise makes that much in the very first year itself.

Be prepared to dip into your savings

I don’t think it is practical to think that you can save enough to completely replace your salary at such a young age so if you want to take a sabbatical of sorts to try out your hand in a new venture then be prepared to dip in your savings.

This means that some part (a significant one I would imagine) of your money is invested in assets that you can liquidate easily. If you are invested in FMPs, infrastructure bonds, PPF, NSCs or any other investment which has a long gestation period then you have to ensure that you have other assets that allow you to liquidate them if you need money. Here, you have to remember what instruments truly have a lock in period. Most tax free bonds have a 10 or 15 year time frame for redemption but they trade on the market so if you needed the money you could sell them off fairly easily.

Tax free and tax saving instruments

Don’t invest a lot in tax free or tax saving instruments. For example, tax free bonds are a great source of tax free income when you are in the 30% tax bracket but you don’t need that if you aren’t going to be hitting that level every year, so you don’t need to give up compounding for that (tax free bonds pay out yearly interest that you can’t reinvest in the same thing). A fixed deposit that compounds and reinvests might be a much better option.

Equity investments

Due to the volatile nature of Indian equities, they can make for a great investment if you take advantage of the crashes and stick to an investment plan. Although your first instinct would be to avoid such a volatile investment option since you need money in a medium to short run, I think it is best to have exposure to equities even with this type of a need.

Work part time before you quit completely

I have a few friends who have taken the entrepreneurial route and it is a mix of people who just left their jobs as well as people who worked part time, made some money on the side and then quit their jobs. It’s not always possible to work part time on the side but wherever possible that is definitely the better option. You get to experiment with what you are doing without risking a lot and you get a fair sense of whether it will work or not and then the plunge full time is a lot less stressful. That you already have cash coming in is a tremendously huge plus.

Conclusion

I feel a good strategy to approach this situation is to save a lot of money, make sure your credit cards are zero and you don’t have any other big EMIs due every month and then invest the rest in medium term instruments that have good liquidity and generate a decent return. There are not many instruments that fit this bill and a mix of dynamic bond funds, equity mutual funds and the good old fixed deposits will help you go a long way in achieving this.

Finally, I know a lot of readers fit this bill as well, and I would request them to leave comments here and share their insights on how they managed money when they switched from full time employment to their own venture.