This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

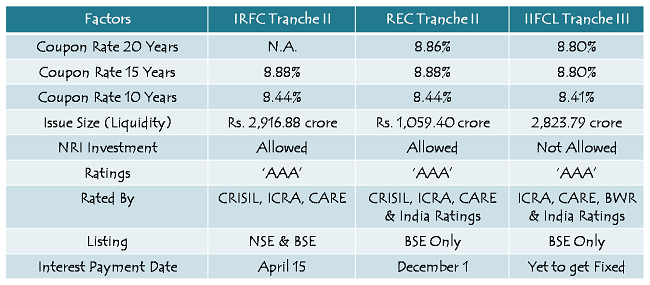

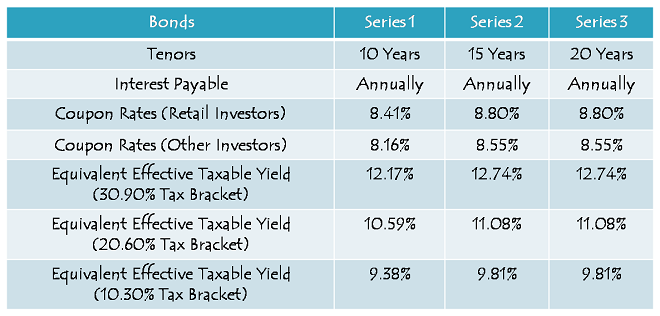

Three tax free bond issues are getting launched from the coming Friday i.e. 28th of this month. These are from IRFC, REC and HUDCO. While IRFC and REC issues are ‘AAA’ rated, HUDCO issue is ‘AA+’ rated. As most of you are aware by now, issues which carry higher ratings also carry lower coupon rates. So, it is natural for the IRFC and REC issues to offer lower rate of interest.

While HUDCO has been able to offer 8.98% as its highest annual interest rate, the same stands at 8.88% for the other two issues. As the HUDCO issue is of Rs. 285 crore only, which is very small by its standards, I expect the issue to get oversubscribed on the first day itself. This makes me feel like that the investors would be more interested in a comparison between the IRFC and the REC issues. So, I would like to cover such a comparison in this post.

Size of the Issues – IRFC issue is bigger in size with the company planning to raise approximately Rs. 2,916.88 crore this time around, whereas REC has recently got the authorization to raise another Rs. 1,059.40 crore. Both the companies have reserved 40% of their respective issue sizes for the retail investors.

Closing Dates of the Issues – REC issue is scheduled to close on March 14, whereas IRFC has decided to keep it extremely short to close it on March 7.

20-Year Option – REC will offer 8.86% per annum for the 20-year option, whereas the IRFC issue will not carry the 20-year option. For the other two durations, both companies are offering the same coupon rates.

Ratings of the Issues – As mentioned above also, both these issues are ‘AAA’ rated. While the IRFC issue is rated by CRISIL, ICRA and CARE, the REC issue is also rated by these three rating agencies in addition to India Ratings as well.

Investor Categories & Allocation Ratio – As always, the investors have been classified in the following four categories and each category will have certain percentage of the issue sizes reserved during the allocation process:

Category I – Qualified Institutional Bidders (QIBs) – IRFC – 10% of the issue i.e. Rs. 291.69 crore is reserved; REC – 10% of the issue i.e. Rs. 105.94 crore

Category II – Non-Institutional Investors (NIIs) – IRFC – 30% of the issue i.e. Rs. 875.06 crore is reserved; REC – 25% of the issue i.e. 264.85 crore is reserved

Category III – High Net Worth Individuals including HUFs – IRFC – 20% of the issue i.e. Rs. 583.38 crore is reserved; REC – 25% of the issue i.e. 264.85 crore is reserved

Category IV – Retail Individual Investors (RIIs) – IRFC – 40% of the issue i.e. Rs. 1,166.75 crore is reserved; REC – 40% of the issue i.e. Rs. 423.76 crore is reserved

As always, allotment will be made on a first come first serve (FCFS) basis in each of the investor categories.

NRI/FPI/QFI Investment – Both the companies have allowed Non-Resident Indians (NRIs) to participate in their respective issues, on a repatriation basis as well as on a non-repatriation basis. Qualified Foreign Investors (QFIs) category has been recently merged with the FIIs category to form a new category termed as Foreign Portfolio Investors (FPIs). FPIs have also been allowed to invest in these bonds now.

Listing – IRFC has decided to get its bonds listed both on the National Stock Exchange (NSE) as well as on the Bombay Stock Exchange (BSE), whereas REC bonds will get listed only on the BSE.

Interest on Application Money & Refund – Both the companies will pay interest to the successful allottees on their application money at the applicable coupon rates. Unsuccessful allottees will get interest @ 5% per annum on their refund money.

Interest Payment Dates – IRFC will pay the due interest on April 15th every year, whereas REC has fixed its interest payment date to be December 1st every year.

Though it is very difficult to make out which issue is superior between the two, I would personally prefer the IRFC issue due to its business fundamentals, bigger issue size and listing of its bonds on both the stock exchanges. But, if you have already invested with either of these companies earlier, then I think it would be better to go for the other company’s bonds in order to diversify your bond portfolio.

I would also like to wait for the NHB issue to declare its coupon rates sometime early next week. If NHB’s interest rates are higher, then I would rather prefer to go with the subsidiary of the central bank rather than these public sector enterprises.

{kind=link}