This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

National Housing Bank (NHB), a wholly-owned subsidiary of the Reserve Bank of India (RBI) and the regulator of the housing finance companies (HFCs) in India, will be coming out with its issue of tax free bonds from the coming Monday, 30th of December.

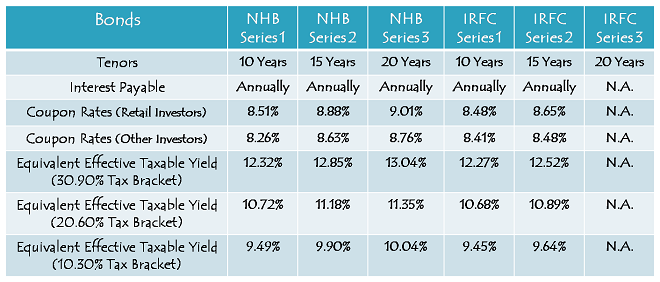

The good news is that the company is going to offer 9.01% per annum for the 20-year option and 8.88% per annum for the 15-year option, which is the highest rate of interest any ‘AAA’ rated issue has carried till date.

Though the issue is scheduled to remain open for the whole of next month to close on January 31st, 2014, the company reserves the right to close it earlier as well in case the issue gets oversubscribed anytime before the due date.

Size of the Issue – NHB is authorised to issue tax free bonds worth Rs. 3,000 crore this financial year, out of which it has already raised Rs. 900 crore through a private placement carried out on August 30th, 2013. NHB plans to raise the remaining Rs. 2,100 crore from this issue, including the green-shoe option to retain oversubscription to the tune of Rs. 1,100 crore.

Rating of the Issue – Being the regulator of the housing finance companies and a wholly-owned subsidiary of the RBI, this issue of NHB has been rated as ‘AAA’ by three credit rating agencies, CRISIL, CARE and ICRA, which is the highest rating by these rating agencies.

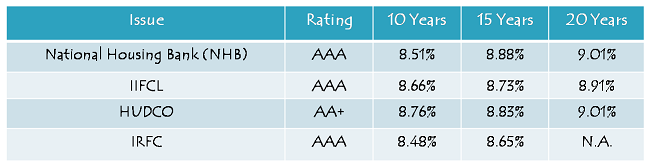

Interest Rates on Offer – The company has decided to offer 9.01% p.a. with the 20-year bonds, 8.88% p.a. with the 15-year bonds and 8.51% p.a. with the 10-year bonds. HUDCO is currently offering 9.01% p.a. for 20 years, 8.83% p.a. for 15 years and 8.76% p.a. for 10 years, but that is a ‘AA+’ rated issue. At 9.01% and 8.88%, NHB issue has become the best AAA rated issue for the 20-year and 15-year duration respectively.

If you want to have only AAA rated bonds in your portfolio and do not have more than 10 year investment horizon, then you can still subscribe to the IIFCL bonds which carry 8.66% p.a. interest rate for 10 years.

Investor Categories & Allocation Ratio – The investors have been classified in the following four categories and each category will have certain percentage of the issue size reserved during the allocation process:

Category I – Qualified Institutional Bidders (QIBs) – 10% of the issue i.e. Rs. 210 crore is reserved

Category II – Non-Institutional Investors (NIIs) – 25% of the issue i.e. Rs. 525 crore is reserved

Category III – High Net Worth Individuals including HUFs – 25% of the issue i.e. Rs. 525 crore is reserved

Category IV – Resident Indian Individuals including HUFs – 40% of the issue i.e. Rs. 840 crore is reserved

NRI Investment – Non-Resident Indians (NRIs) and Qualified Foreign Investors (QFIs) are not eligible to invest in this issue.

Allotment on First Come First Served Basis – Subject to the allocation ratio, allotment will be made on a first come first serve (FCFS) basis in each of the investor categories, based on the date of upload of each application into the electronic system of the stock exchanges.

Lock-in Period, Premature Redemption & Listing – There is no lock-in period with these bonds, but at the same time, you cannot redeem these bonds back to the company before their maturity period gets over. In order to encash your investment before maturity, you’ll have to compulsorily sell these bonds on the stock exchange(s) where they have been listed for trading.

The company has decided to get these bonds listed only on the National Stock Exchange (NSE) and has got the necessary in-principle listing approval for the same on December 20, 2013. The company will get these bonds allotted and listed within 12 working days from the closing date of the issue.

Demat/Physical Option – Though it is mandatory to have a demat account to sell/trade these bonds, you can subscribe to them in physical/certificate form as well and keep them till maturity. Interest will still get credited to your respective bank accounts through ECS.

Interest on Application Money & Refund – NHB will pay interest to the successful allottees on their application money, from the date of realization of application money up to one day prior to the deemed date of allotment, at the applicable coupon rates. Unsuccessful allottees will get interest @ 5% per annum on their refund money.

Face Value of the bonds & Minimum Investment – NHB is the first company this financial year to keep the face value of its bonds as Rs. 5,000 instead of Rs. 1,000. Considering its face value and minimum application size of one bond, an investor is required to invest at least Rs. 5,000 in this issue.

Interest Payment Date – NHB has not fixed its interest payment date as yet and the first due interest will be paid exactly one year after the deemed date of allotment. As the deemed date of allotment will be fixed once the issue gets closed and before the bonds get listed, I will update this post as and when it gets announced.

Should you invest in this issue?

I would say that one should definitely invest in this issue and I have many reasons to justify my view. Here are some of those reasons:

First, NHB issue is ‘AAA’ rated.

Second, you are going to get 9.01% p.a. and 8.88% p.a. coupon rates which are the best 20-year and 15-year rates offered by any AAA rated or AA+ rated issuer till date.

Third, NHB is a wholly-owned subsidiary of the RBI and I don’t foresee the RBI to ever let its subsidiary default on any such bond issue. Also, NHB is the regulator of the housing finance companies, like RBI is for the banks and SEBI is for the capital markets. I don’t think any government would allow any regulator to default on its payments.

Fourth, it is almost certain that the CPI inflation will start falling from next month onwards. If that materialises, we might have G-Sec yields falling quite sharply.

Fifth, IRFC is the next company to launch its tax-free bonds from January 6 and its coupon rates are lower than that of NHB at 8.48% p.a. for 10 years and 8.65% p.a. for 15 years. It is not going to issue these bonds for 20 years either.

Sixth, there are very few good companies left now to issue tax-free bonds this financial year. REC, PFC, NHPC and NTPC have already raised their quota of authorised amount from the markets. HUDCO is also very close to reach its targeted amount. Only IIFCL, NHAI, IREDA, Airport Authority of India (AAI), Ennore Port and Cochin Ship Yard are now left to issue these bonds and their issue sizes are also very small, except NHAI and IIFCL.

Seventh, it is still not certain whether tax-free bonds would see the light of the day next financial year onwards or not. Like 80CCF infrastructure bonds got stopped getting issued from FY 2012-13 onwards, it is possible that the next government decides to stop extending this budgetary support to all such companies.

Eighth, NTPC issue got listed a few days back and that too at a premium. If an issue with coupon rates lower than the NHB issue can trade at a premium, then it is almost certain that these NHB bonds would also trade at a premium on listing.

Ninth, NHB has reasonably strong fundamentals. It reported profit after tax (PAT) of Rs. 450 crore with total income of Rs. 3,030 crore for the period ended June 30, 2013 as against Rs. 387 crore and Rs. 2,492 crore respectively for the period ended June 30, 2012. Its net interest margin (NIM) also improved to 2.25% during this period as against 2.20% last year.

NHB’s asset quality has also been remarkable. Gross NPAs and Net NPAs remained quite close to zero for the periods ended June 30, 2011 and June 30, 2012. Though its gross NPAs and Net NPAs have jumped to 0.53% and 0.45% respectively in the latest period ending June 30, 2013, this relative poor performance was due to one large project exposure slipping into the NPA category. This large account was worth Rs. 179.60 crore out of its total NPAs of Rs. 180.62 crore.

Why you should not invest in this issue?

If I myself decide not to invest in this issue, I would have only one valid reason for that, higher expected coupon rates in the forthcoming issues. If any of you think that the rates would be higher with NHAI bonds or IIFCL tranche III bonds, then you can probably skip this issue. Personally, I would invest my family’s money in this issue and would also advise my clients to do that.

Application Form of NHB Tax Free Bonds

NHB Tax-Free Bonds – Bidding Centres

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in NHB tax-free bonds, you can contact me at +919811797407

Shiv – you’ve said:

* Fourth, it is almost certain that the CPI inflation will start falling from next month onwards. If that materialises, we might have G-Sec yields falling quite sharply.

This would make G-secs attractive, if newer instruments offer smaller coupon rates, older higher-coupon rates demand will go up. Mutual funds with this strategy would make good investment.

But will inflation tame? From Rajan’s Dec 18 speech, it seemed he’d like to wait longer, reviewing results of previous actions, before increasing repo rate.

Can you share more on your view of CPI? Or maybe do a post on it?

Thanks for excellent content.

Yes, you are right about investing in Gilt (G-Sec) mutual funds. Investment in these tax-free bonds also will result in capital appreciation if rates fall anytime in future.

Dr. Rajan expects the inflation to fall in the coming months, that is why he did not increase the rates on December 18. But, if it does not materialise, then we’ll see another rate hike and G-Sec yields move up.

I think the CPI inflation should fall, but how & when, only God knows. I’ll try to do a post on the same sometime next month.

Thanks for your kind words!

Great Article as always. Do you still suggest these bonds for someone who doesn’t have any tax liability?

Yes Anup, that is because it has scope of capital appreciation. Investors who can bear high risk should go for equity mutual funds.

Truely informative and an excellent writeup. You get to know all the details about the issue by reading this post.

Thanks a lot Aditya for your kind words !!

Hi Shiv,

As usual very thoughly researched analsysis. Thank you. Now I have to look around for funds and that too need to get in next 2 days. Quite challenging. I have one question, I have a demat account. In the past. I bought all the tax free bonds using paper/physical certificate. Then I am in the process of converting to electronic form. How can I invest using demat account? I am assuming if I invest thru demat account, then it will be in electronic form instead of physical ; so no need to do the conversion.

Please let me know. Thanks,

Regards,

Sundar.

Thanks Sundar !!

You need to contact your broker to get the required info about the process of applying for these bonds through your online demat account.

Hi Shiv,

I am a regular reader of your posts though this is the first time I need to ask a question.

Currently I have my money lying in at 9% FDs maturing in 2016. It’s been a year since the money is locked in these FDs. I want to get out of these FDs for tax reasons and want to put it in these TFBs. Mainly looking for a 15 year option of NHB. Would you recommend me to do that?

Also, do we need a Demat account to hold these bonds in electronic form? or will the HDFC ISA or ICICI invest@ease platform suffice? Also, if I go for physical bonds for now, will I be able to convert them into demat form once I open a demat account later?

Thanks for advance alert on NHB.

– Sanjiv

Hi Mr. Sanjiv,

Sorry to say, but I won’t be able to take any personal queries here on this forum.

To invest in these bonds, either you need to have a demat account or you’ll subscribe for it in a physical/certificate form. I am not sure how HDFC ISA or ICICI invest@ease platform work and if they provide this service, whether it would go into your demat account or the bonds will be issued in physical form.

Yes, if you go for physical bonds now, you can get them converted into demat form later whenever you open a demat account.

Thanks very much Shiv for a prompt answer.

I do not think that the first of the question is a personal query. I guess there would be so many people like me who may have got their money locked in FDs, so the answer will benefit them all. Anyways, it is your choice to answer it or not. Thanks again.

You are welcome !!

I may add this to your query. I have personally withdrawn my premature FD’s of 9.25% rate to invest in these TFB’s and think they are much better option than FD with no TDS and chances of capital appreciation with no liquidity issues so I think it’s a no brainer.

Thanks Ikjot for your inputs !!

Thanks Ikjot and Shiv, I was inclined for the same. Thanks for making my decision easier.

Sanjiv, While you are taking a decision on breaking the FD, you need to look at your financial position. Do not break all FDs considering that return is tax free and there is opportunity for capital gain. Look at the amount which you can consider blocked long term and break those FDs and invest. The liquidity will be an issue if the price goes down. I definitely would not like to sell the bond below the face value. If I have to sell the TF bonds, I should get my interest for the period and some premium. Probably this is the reason why Shiv also refused to comment. When I took that decision to break my FDs, I consider a percentage of the amount which I can allow blocking unless and otherwise real emergency occurs.

Hi Shiv!

In point 2 of the form, can you kindly confirm the sub-category code for Category IV investors. Usually its 41, but I was reading the prospectus & couldn’t find it. Could you also tell me where exactly is it mentioned?

Also, it has been mentioned in the prospectus in bold letters that “Checks without the nine digit MICR code are liable to be rejected”. My check doesn’t have the code mentioned on it. Neither have I ever come across such an instruction in any prospectus before. Does it mean I cannot apply for this issue? Can you kindly clarify on the same.

Hi Simple,

Sub-category would be ’41’ in this issue as always. Please check this link and type 41, you’ll get the required info – http://www.akstockmart.com/akintra/Upload_DnLoad/72_EXTRA.pdf

I am listening it for the first time that a cheque leaf is not carrying MICR number. I am not doubting what you are saying, but check this link before we discuss it any further.

http://4.bp.blogspot.com/_Ht1_rh8kGYQ/TUqNxRK_eNI/AAAAAAAADcs/zavpCZj3nAk/s1600/IFSC+and+MICR+Code+in+check.PNG

Couldn’t find 41. But I will take your word for it.

Whoops…. o_O

Found it! Thanks for the link. 🙂

You are welcome !!

🙂

Thanks for your excellant report given above.

i want to invest 20 lacs in NHB for long term ( 2 applications )

Where can i find / what is current G sec rates ?

In How many years G-Sec rates expected to fall to 7% ?

what % of gain can be expected in this issue of NHB (9.01 -20 years) if it falls to 7 % ?

where can i get forms to apply ?

Thanks Rohit !!

1. Here is the link to check the G-Sec rates – https://www.ccilindia.com/OMHome.aspx

2. Only God knows how much time it will take G-Sec rates to fall to 7%. It can happen in 3 months time or it might take 5 years for the same.

3. I am not sure exactly what would be the percentage gain if the G-Sec yield falls to 7%, but I think it should be approximately 15-25%.

Also, here is the link to download the forms – http://www.akstockmart.com/akintra/BA/DNLDFORM.aspx?refno=dU6gu20m1nc=

i am your new reader .. very impressive you reply so fast with such an expert guidance

to new investors like us .. i cannot understand where to look for Gsec rates at this link – https://www.ccilindia.com/OMHome.aspx it shows various data between 8.6 & 9.3

so can i assume its 9 % average at present . Am i correct ?

No Rohit, that’s not correct. All these are different securities with different rate of interest (coupon rate) and different maturity periods.

Consider this: 8.83 GS 2023 – It is a 10-year Government Security (G-Sec) maturing in 2023 carrying 8.83% rate of interest payable half-yearly.

Great informative article as always Shiv. Thanks.

Thanks Hemant !!

Apart from the interest rate and credit rate, the 9 reasons, why we should invest, are fascinating.

hmm.. ok

As always, a thorough and structured analysis by Mr. Kukreja. Your site has indeed become indispensable to the many lost wanderers on the net looking for actionable information in the bond space. Thanks once more for your wonderful work.

Thanks a lot Rama for such motivating words !!

Hi Shiv,

I was holding on my last piece of funds for a good TFB, but looking at the IRFC’s rates and noticing that IIFCL was inching towards closure… I applied for IIFCL a couple of days back. But, as a pleasant surprise NHB has come up with great rates, which I would like to invest (even more after reading your 9-point recommendation 🙂 )… Is it possible to withdraw the IIFCL application? I’ve applied thru online trading account of R-Money.

Regards,

CVS

Hi CVS,

Yes, it is possible to withdraw your IIFCL application. You need to approach your broker or the Registrar of the issue to cancel your IIFCL application.

Note that you wont get refund amount immediately if ur broker already filed ur application, it will be refunded after allotment happens (atleast thats what happened to me with Kotak online).

That’s right.

It also depends on how you apply. If the application is using ASBA, the block is released on the same day (ie you can use the same fund for applying somewhere else). I have already done this 2-3 times using my HDFC Sec online system.

Thanks for this info Raju !!

Hi Shiv,

Thanks for your excellent recommendation on NHB bonds.

Wanted to check if you know of any online portfolio manager where you can track the trading volumes and LTP of the tax free bonds listed on the NSE and BSE issued in the last 3 years in one place. While individual prices are available on NSE/BSE, I could not find any portfolio manager for the same. Any suggestions shall be appreciated.

Thanks Pankaj for your kind words !!

Even I haven’t come across any such perfect link. Please check this link of Edelweiss, it has many such bonds and NCDs, but this link also is not 100%.

https://www.edelweiss.in/debt/National-Highway-Authority-of-India/NHAI-N2.html

Have you checked this link of NSE?

http://www.nseindia.com/live_market/dynaContent/live_watch/equities_stock_watch.htm?cat=SEC

You could get some info from the BSE site as well –

http://www.bseindia.com/markets/debt/debt_corporate_EOD.aspx?curPage=1&expandable=0

Thanks Raju for this link!

Great analysis, thanks much.

Quick question. Do you think once G-Sec yield starts sliding down, some of the previous TF bonds can be sold at buy price at least? e.g.

HUDCO 8.39% 10 Y

REC 8.71% 15 Y

IIFCL 8.75% 20 Y

Absolutely, you would be able to even earn capital gains with your current investments. If the G-Sec rates fall to 7% or so, you’ll have great gains in your current portfolio and even greater gains with these NHB bonds.

Subscribing to follow up comments

Thanks Shiv for this. I was searching about this issue for the last 1 week and this is the only analysis I could get.

That’s great to hear !! 🙂

Dear Shiv,

Excellent Analysis as usual. If a person does not want to invest for long term, but only wants to benefit from lowering of interest rates by RBI (due to fall in inflation) in future, which is better option : Long-Term Gilt mutual funds or tax-free bonds ?

Thanks

Thanks TCB !!

I think Gilt mutual funds with high duration portfolio would be a better option. It will have great liquidity also. But, if the fund manager has an opposite view as the investor’s and his/her view turns out to be incorrect, then it will be very painful for the investor.

Thanks Shiv for the wonderful article!

As others, I also enjoyed reading your 9 point positive feedback on this issue.

One feedback – there seems to be a typo in Category I limit – I think it should be 210 instead of 175.

One question – when you say you will invest “family’s money” what do you actually mean? And why you are not planning to invest your own money? 🙂

Thanks Amlan for your kind words and also for pointing out the typo !! I have corrected it now.

I’ll give honest answer to your question. My family means me, my parents, my brother, my sister-in-law and their two kids and my family’s money means our money. I do not earn big money, but whatever I earn, I invest that in my business and riskier investments like equities. I invest my family’s money in safer products as per their risk profile and asset allocation.

I hope it satisfies your query!

There should be a “like” option for replies… Just like FB! 😉

It is not very difficult to write it also “I like your reply/comment” !! 😉

I liked this reply.. 🙂

Sir,

I think the Interest payment date has already been fixed in this case. You may please refer the page 26 of the application form. It is 7th February every year.

May I please request you to clarify?

Thanks very much.

Hi Shub,

Thanks for noticing and pointing it out Shub! But actually February 7 as the interest payment date is just an illustrative example. It as as per the Deemed Date of Allotment which has been assumed to be February 7, 2014. It was perfectly natural for you to get confused.

Good Analysis Shiv! I appreciate your 9 reasons for investing. As a 10th one, I will say this is the only bond from a bank which can further diversify the portfolio. As you rightly pointed out, the chances of interest rate for TF bonds going up is minimum considering the fact that no company can offer interest more than that they can get by lending. Banks already reduce lending rates for housing loans which is in the range of 10-10.5%. If NHB lends to these banks and banks themselves are giving loan at 10.5% , where is the opportunity for further increase. Even if the Government securities goes up, it is not mandatory for the TF bond to be higher. Government tried to control the upper limit of the coupon and not the lower limit. It is quite clear that this will be the best opportunity for TF investors.

Thanks George !! I agree to most of your thoughts George !!

High inflation is a genuine problem and the RBI is doing its best to control it. It is not that the inflation and interest rates cannot move higher from these levels. People in the metro cities & some rural areas are earning good money and are spending it like there is no tomorrow. We are nowhere closer to the western world, but we are better off than earlier.

I think the government is not playing its required role and it has already started seeing the results of it. Now, it is our responsibility to do justice with our money, our economy and our country. I think we should not waste our natural resources and limit our discretionary expenses. I am quite confident that the interest rates would move lower in a few months time.

Hi Shiv, excellent analysis as always.

With your 9-star recommendations, this issue is likely to be fully subscribed soon.

Well how many days maximum, you think it will allow us , to apply and still get full allotment?

Thanks Mr. Ramesh !!

I am not sure how many days it will take for the issue to get oversubscribed, it all depends on the first day subscription by the institutional and corporate investors. I think it should take at least 2 days for the retail investor category to get oversubscribed though.