PFC 8.92% Tax-Free Bonds – October 2013 Issue

This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

‘AAA’ rated REC issue offered 8.71% to its investors, ‘AA+’ rated HUDCO issue fixed it at 8.76% and then ‘AAA’ rated IIFCL issue managed to cross REC’s peak rate of interest with 8.75%, but now it is the turn of Power Finance Corporation (PFC) to surpass all previous rates to set this year’s highest interest rate on its tax-free bonds by offering 8.92% for a 20-year duration.

PFC would be the fourth company to launch its public issue of tax free bonds this year from Monday i.e. October 14th. The issue would run till fifth Monday i.e. November 11th. But, the company may extend it or preclose it, depending on the investors’ response to the issue.

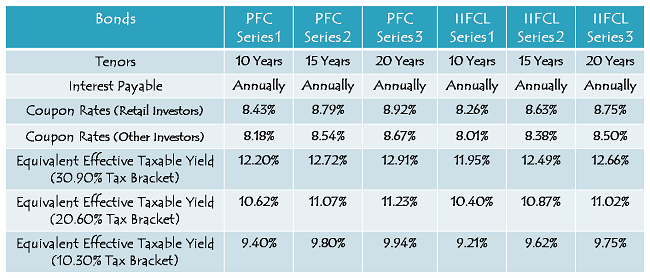

Interest rates offered by PFC are the highest rates for all three tenors. PFC has set its coupon rates at 8.92% per annum for 20 years, 8.79% per annum for 15 years and 8.43% per annum for 10 years. This jump is due to a rise in the benchmark G-Sec rates in the last 10-15 trading days, after the Repo Rate hike by the RBI.

Size of the Issue – PFC has been authorised to raise Rs. 5,000 crore from tax-free bonds this financial year, out of which it has already raised Rs. 1,124.10 crore through a private placement on August 30th. The company plans to raise the remaining 3,875.90 crore from this issue, with the base issue size of Rs. 750 crore and the green-shoe option of Rs. 3,125.90 crore.

Like REC, if this issue gets subscribed to the tune of Rs. 3,875.90 crore, it will be the last issue of PFC this financial year.

Green Signal for NRIs – After IIFCL not allowing NRIs and QFIs to invest in its issue, PFC has decided not to do that. NRIs, on repatriation basis and on non-repatriation basis, are eligible to invest in this issue. Qualified Foreign Investors (QFIs) are also eligible to participate in this issue.

No Lock-in Period – Many people have been asking me about the lock-in period of these tax-free bond issues, but I don’t know how I missed to mention it here in all my previous posts that there is no lock-in period with these tax-free bonds. If you subscribe to these bonds in demat form, you can sell them anytime you want after their listing on the stock exchange.

These are not tax saving bonds, like 80CCF Infrastructure Bonds or 54EC Capital Gain Tax Saving Bonds, which carry a lock-in period of five years and three years respectively.

Listing – PFC will get these bonds listed only on the Bombay Stock Exchange (BSE). Investors can apply for these bonds either in demat form or in physical form, as per their choice. The company will get the bonds allotted and listed within 12 working days from the issue closing date.

Rating of the issue – Three credit rating agencies, CRISIL, ICRA and CARE have rated this issue and all of them have rated it as ‘AAA’, which is their highest rating to any debt issue. Also, these bonds are ‘Secured’ in nature against certain assets of the company.

Categories of Investors & Allocation Ratio – The investors again have been classified in the following four categories and each category has certain percentage of the issue reserved for the allotment:

- Category I – Qualified Institutional Bidders – 15% of the issue is reserved

- Category II – Non-Institutional Investors – 20% of the issue is reserved

- Category III – High Networth Individuals including HUFs, NRIs & QFIs – 25% of the issue reserved

- Category IV – Resident Indian Individuals including HUFs, NRIs & QFIs – 40% of the issue reserved

Minimum & Maximum Investment – There is no change in the minimum investment requirement of Rs. 5,000 i.e. at least 5 bonds of Rs. 1,000 face value each. Retail Investors’ investment limit stands at Rs. 10 lakhs, beyond which they will be considered as HNIs and will get a lower rate of interest.

Interest on Application Money & Refund – PFC will pay interest to the successful allottees on their application money at the applicable coupon rates, from the date of realization of application money up to one day prior to the deemed date of allotment. Unsuccessful allottees will get interest @ 5% per annum on their refund money.

Factors favouring investment in this PFC Issue…

* Highest Coupon Rates – Thanks to a sudden spike in the G-Sec yields in the last 10-12 trading days since the RBI raised the Repo Rate in its monetary policy of September 20th, PFC has been to offer the highest interest rates of the current financial year. I think with 8.92% or 8.79% tax-free rates, investors in the 30% or 20% tax brackets would not even think of going for a bank FD @ 9%.

* RBI cutting the MSF Rate – RBI has cut the MSF Rate by 50 basis points to 9% a couple of days back. The idea was to reduce liquidity crunch in the banking system and help banks in reducing their cost of overnight (very short-term) borrowings and also normalize the yield curve. This move makes market participants believe that the RBI will try to cap the rise in overall interest rates as much as possible.

* Fall in G-Sec Yield – As a result of the RBI’s move to cut the MSF Rate, the 10-year G-Sec yield has fallen from 8.68% to 8.46% in the last couple of days. If this fall is not temporary and continues for a little longer time, you would see a fall in the coupon rates of the upcoming tax-free bond issues.

* Postponement of QE3 Tapering & US Shutdown – US Federal Reserve’s decision to postpone QE3 tapering and a partial shutdown in the US have resulted in a fall in the 10-year bond yield there from 3%+ to 2.64% today. This should also keep the sentiment somewhat healthy here in the Indian bond market.

* Steep fall in September Trade Deficit – With a fall in gold & oil imports and a surge in exports, the Ministry of Commerce today announced a steep fall in our September trade deficit. The problem, which was becoming too burdensome for our economy, is finally getting controlled. This should strengthen the value of Indian rupee against the US dollar in the coming days and the bond yield should also move lower.

Factors against this PFC Issue – Though there are not many factors which come to my mind against this issue, but overall things are not very bright for the power financing sector here in India. PFC, REC and PTC India Financial Services are some of the companies which have been struggling to get their money back which they have been lending to the state electricity boards (SEBs) over the years.

These kind of events have resulted in its share price falling from Rs. 350+ during 2010-11 to below Rs. 100 this year and I think stock price performance is a good barometer to check a company’s current financial health and future prospects. So, this is one thing which you should consider before investing your money in this issue.

With PFC offering relatively higher interest rates and NHPC issue hitting the market only in the third week, I would prefer to invest my money in this issue as compared to HUDCO and IIFCL issues. With so many positives and a possible fall in inflation & interest rates, I think PFC’s rates would be the highest coupon rates offered by any ‘AAA’ rated issuer this financial year.

Application Form of PFC Tax Free Bonds

As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in PFC tax-free bonds, you can contact me at +919811797407

Thanks for quick update Shiv.

I was about to buy IIFCL bonds but now, I will buy PFC bonds as interest is high.

You are welcome Amit! I am glad it helped you in making a better choice.

Same here! Thanks Shiv

Roberto

You are also welcome Roberto! 🙂

Same here too ! Thanks Shiv

Just one question on PFC vs NHPC. Do you think the retail portion of NHPC will get subscribed on day 1 itself ? Though I doubt it, do you have any past data on 1st day subscription figures to justify my intuitive feel.

Naga

You are welcome Nagarajan!

Very interesting point. I think you are asking me this because of super Day 1 response to the PFC issue. Am I right?

I think your intuitive feeling is not totally unjustified, but I too have a big doubt about it getting materialised. Past data suggests retail investors follow the institutional investors and do not invest on Day 1. But, looking at the institutional, corporate investment figures for the PFC issue, NHPC too will have a bumper opening day. It would be interesting to see the retail response on Day 1. I think I’ll make my family’s first tax-free bond investment this year in NHPC on Day 1.

Thanks Shiv for sharing this. Interest rate really looks good for 20Yrs tenure.

One question, hope you can help. I have already submitted bid for IIFCL 20 yr bond via hdfcsec. Can I cancel that bid, and if I can, will I get my amount back in few days so I can invest in PFC bonds. OR is it like after canceling the IIFCL bid, i need to wait until IIFCL allotment is done to get the amount back.

You should get the money back in a day or two.I have withdrawn from IIFCl is shows unblocking. I havent invested through HDFC though.

Hi Prajju,

Yes, you can withdraw your IIFCL application through online HDFC Securities account, after which it is the responsibility of HDFC Securities to cancel your bid. But, I am not sure how soon will you have access to your invested money. In this case, you’ll not get any interest on your application money though.

Thanks Shiv for sharing the details.

The sector specific risk that you have mentioned under “Factors against this PFC Issue” section – will it be applicable for NHPC also?

My NHPC stock portfolio is in red for last 3 years!

Hi Amlan,

The whole Power Sector has been under pressure for quite some time now, due to one reason or the other. There were problems everywhere in the past, with the producers as well as the financiers.

But, in the last 2-3 months things are getting somewhat better. India is a power scarce country and whatever gets produced there are buyers ready to absorb it. Unlike coal dependent power producers, thankfully there is no shortage of raw materials for NHPC and it is a free source also. So, that ways I would say NHPC stands better than PFC.

But, then it is all about good management and mismanagement. How can you expect good managements in a country where there is no culture of efficiency and hard work in government organisations. So, I would say one should pray to the God to bring back Mr. Suresh Prabhu like Power Minister at the helm in order to ensure things get managed in a better way.

Can anybody tell me how can i withdraw my bid for IIFCL . I have ordered with ICICI DIRECT and cant see option to withdraw bid.

Hi Raj,

Just call the customer care department of ICICI Direct or write a mail to them asking them to withdraw your application and they should respond back to your request.

Thanks Shiv for reply, Called customer service and was told we cannot withdraw speak to bond issuer. Had an heated argument with customer supervisor as well who said unable to cancel or withdraw your bid. Very unhappy with their service.

Mail them this link having the prospectus of IIFCL:

http://www.akcapindia.com//WebSiteDocuments/IIFCL_Shelf_Prospectus.pdf

“Withdrawal of Direct Online Applications

Direct Online Applications may be withdrawn in accordance with the procedure prescribed by the Stock Exchanges.”

or write a mail to the Registrar directly quoting your Unique Application Number (UAN):

“Applicants applying through the Direct Online Application facility must preserve their UAN and quote their UAN in: (a) any cancellation/withdrawal of their Application; (b) in queries in connection with Allotment of Bonds and/or refund(s); and/or (c) in all investor grievances/complaints in connection with the Issue.”

It is the duty of ICICI Direct or any broking company/Registrar through which you are applying for these bonds to let you know the procedure to withdraw your application.

Raj is my brother who applied for this and I had to speak with ICICI DIRECT on his behalf. What pathetic customer service they provide..unbelievable !!

I knew that would be the outcome in 99 out of 100 times you call or mail the customer care centers of any of these broking companies.

Is it possible that interest rates drop drastically in future and the company chose to cancel these bonds and return the principal amount because it becomes no longer viable for the company to pay the interest at these high rates. Is this a risk?

I think it has happened before.

Sardar sarovar bonds 17% p.a

http://articles.economictimes.indiatimes.com/2004-05-22/news/27393796_1_deep-discount-bonds-bond-issue-sardar-sarovar-dam-project

Not sure if there were rating agencies then but even then rating is good only for today not 20 yrs from now. PFC and REC are good companies though, future is unknown.

Hi Johnny,

There is no “Call Option” with PFC or “Put Option” with the investors of these bonds. So, there is no such risk. Like an investor cannot redeem these bonds back to PFC in case they want their money back in some kind of emergency, similarly PFC also cannot return your investment back to you even if there is a drop in interest rates dramatically.

Dear Shri Kukreja,

I retired recently with a corpus of Rs 70 lacs which I intend to invest for the long term. I do not want to take any risks with this money and therefore have decided to invest this money in tax free bonds. I have already invested 10 lacs each in HUDCO and IIFCL (the 20 year option in both). I would like to invest the rest of the money in two parts of 25 lacs each in PFC and NHPC. I am likely to be in the 30% tax bracket because of other income which is around 8 lacs a year (and derived mainly through rent income and NCD income). In light of your comments on the risks related to the principal vested with these companies, can you please let me know if this is what I should be doing? Many thanks in anticipation for your inputs and guidance.

Ramachandran

Looking forward to response from Shiv !

Ramchandran sir, I think it is good that you are diversifying into various issues.

Personally, I thought no future issues would be able to match REC coupon rates and hence I invested fully into REC. Now sadly I am missing out on the recent issues !

I have similar goals as you ; however I am also reserving 30% for equity, and rest into fixed income. Overall this type of combination should yield about 12 %.

Hi Ramachandran,

Since you are in 30% bracket, you are having a sound Financial background after retirement. Since 70 L you have received from retirement can serve you better , TF bonds are good option. In reality no return is 100% risk free. I will suggest you to not rush 25L each and it will be better to invest another 10 L each. Keep the remaining in FD. Some times liquidity can become a concern. It is not advisable to have all eggs in one basket. I am sure Shiv will give more balanced views. This is my take on this and I would have done the same. Diversification of portfolio always helps in meeting eventualities unknown.

Great & valuable comments from Sagar, George and Jitendra (below).

I would like add another dimension to diversification across Companies.

Different companies have different interest payout date (Some in Oct, Some in July, some in Jan). So the yearly interest may work as continuous and regular source of income!

Thanks Amlan for your inputs! If somebody requires regular income, then your suggestion is really a good idea.

Thanks George for your inputs! They are of great help!

I think Mr. Ramachandran doesn’t have liquidity as his top requirement, as he is having enough rental income and other sources of income. I never recommend company FDs. Bank FDs come last in my list in this case, as he is in 30% tax bracket. As far as liquidity is concerned, though bank FDs are liquid, their system of calculating interest in case of premature withdrawal is not investor-friendly. I think there will be enough liquidity with these bonds for an investor to cash out in case of an emergency. I would have invested some portion of my investment in debt MFs for liquidity purposes rather than FDs.

Hi Mr. Ramachandran,

Risk Profiling & Asset Allocation are two key things for Financial Planning. Diversification within an asset class is also key to minimize the risk. As you don’t want to take any risk with your investments, you are left with only fixed income options.

Within fixed income options, I think the current tax-free bond issues, with high interest rates & improved terms & conditions as compared to last year, truly score high over other options like bank FDs, company FDs, Post Office schemes (except PPF) and certain debt mutual funds.

FMPs and certain open ended debt mutual funds have their own advantages, but then FMPs are not liquid and debt funds also have their own risks. So, at present, tax-free bonds are the flavour of the season. In the last decade or so, I haven’t seen such an attractive fixed income option for the investors in the higher tax brackets.

Though I would not like to give any personal advice here, but if I were to invest my money, I would have invested only Rs. 10 lakhs each in PFC & NHPC and rest I would have invested in diversified equity mutual funds. If you don’t want to invest in equities, then you should invest in PFC & NHPC and then wait till their closing dates for other issues to hit. If the rates of other issues are higher than the rates for non-retail investors of PFC & NHPC, then you should go for those issues and diversify your investments. If not, you can top-up your investments in PFC & NHPC. I hope it helps!

Hi Shiv,

Thanks for doing a post on PFC tax free bonds. Your post lands up in the top result on google when I search for “PFC tax free bonds 2013” !!!

I have been reading comments / views given by you and other readers / investors to Mr. Ramachandran. Iam an investor who fall in 30% tax bracket and would like diversify into fixed income options. I feel I have enough exposure in equity as currently > 50% of my net worth is in equity and I am planning to book some profits in some of the stocks.

I have been reading that FMP’s (1 to 3 years) are attractive and offer good post-tax returns due to Long term capital gains tax accorded to FMP’s. I am planning to reserve some portion of fixed income to FMP’s as well instead of investing completely in tax free bonds.

1) What is your view on FMP as compared to the current tax free bonds?

2) In the current high interest rate scenario what kind of likely post tax returns can one expect from FMP’s (1 year to 3 years)? Can FMP deliver better post-tax returns than tax free bonds?

3) You present some risks associated with power financing sector in this post. What kind of risks are associated with FMP’s?

Are there any other issuers of tax free bonds expected in near future (1-2 months) apart from PFC and NHPC.

Awaiting your reply.

Thanks,

Sailesh

I would recommend invest in NHAI, NHB and IRFC too. On an investment of 10 lacs, bottom line impact of .5% is 5000/-. with such a big investment base I don’t think this should cause any concern to the investor, rather utility derived in terms of better diversification far exceeds the shortfall due to lower interest rates. I always keep suggesting (though a personal opinion) – never think for maximizing your returns, rather plan for optimizing your returns!

Thanks Jitendra for your inputs!

You are absolutely right in your approach and it is always wise to diversify even if the returns are somewhat lower. That is why I recommend tax-free bonds over company NCDs. I think it is better to invest with good PSUs rather than private companies offering high rate of risky returns.

But, I would say don’t wait too long for NHAI, IRFC etc. to come up with their issues. Probably they won’t raise money from these bonds at all, like last year NHAI did not show up with its bonds issue. Even if they do come, the rates might go down till that time.

Also, there is no guarantee that a PSU offering lower interest rate would never default. So, it is better to have a balanced view and take the opportunity of current high rates.

Hi Shri. Kukreja,

Many thanks for the quick response. Your inputs are most helpful. I have one problem, though, in doing this: ICICIDIRECT says that “Only one application is allowed per Match Account”. Therefore I may not be able to modify (or, in other words, submit more than one application for the same issue) the order. Strangely, most of these service providers and intermediaries seem to be totally impervious to either customer needs or the fact that technology has made service easier to provide, to win their loyalty. But of course, these are really extraneous to the concerns of this forum.

Thanks again to you and the other folks who were kind enough to provide their perspectives too.

~ Ramachandran

You are welcome Mr. Ramachandran! In case ICICI Direct doesn’t allow you to modify it or submit more than one application, you can contact me on my number or email id and I’ll try to help you out in whichever way I can.

Could u advice us if these bonds are beneficial to invest for NRI’s since NRE Bank F.D’s do offer the same range of interest rates?

Also could u do a post on FCNR(B) deposits which are now being issued for NRI’s and the pros and cons of investing in it?

Hi NKN,

One thing which is a major positive for me with these tax-free bonds over any kind of FDs is that there is a scope of capital appreciation also. So, if there is a capital appreciation, then these bonds will give bumper returns.

Even if there is no capital appreciation, an NRI should be happy with their interest rates and liquidity as compared to NRE deposits.

I’ll try to do a post on FCNR(B) deposits sometime in future, whenever I get enough time to do it.

NHPC issue is expected to open on October 18th.

Dear Shiv,

I am currently in the non income tax bracket as my income is less then 2 lakes a year. I have 11 lakh of savings which I want to invest in these bonds. Do you think it’s the right thing to do or should I go for bank fd’s.

Thanks

Hi,

It is very difficult to give such an ad hoc advice here. There are many more things to analyse and plan before giving advice in your case. But, I would say NCDs are better than Bank FDs & Company FDs from your perspective.

The rates for 20 yr tenure for retail investors are really attrActive. but I have a time frame of 10 yes tenure in mind.

I wonder if it will be OK to go for a 20 year tenure, earn attractive interest @8.9% for 10 years and then sell in secondary market and pay LTG at 10%. Earning additional capital gain of 90% after paying LTCG tax as and when possible or needed. or there are some other pitfalls?

Hi Ramesh,

That is exactly what I would be doing myself & advising most of my clients. The only pitfall is – what if the interest rates are higher 10 years down the line? In that case, it will result in a capital loss.

But, I think the probability of that happening is quite low and therefore one should go for the highest coupon rate & highest tenure, if he/she applies for it in a demat form.

Hi shiv

I regularly follow one mint and It helped me a lot in making a informed decision when it comes to investments

I have a few queries. Pls answer and help me

1. How much capital appreciation in the bond price can i expect at the end of 20 yr tenure?

2. It is taxed 10% based on the indexation or 20% without indexation? correct?

3. Is there a chance that coupon rate fixed at the start of the tenure can change as bond prices change?

4. Is there a chance for default?

I am considering this as a constant yearly income for my father and mother instead of going for the annuity option which will come under the taxable income and gives the very less interest rate also.

Pls share me a link on Senior citizen savings scheme! so that i can just do a comparision.

Pls answer my queries.

Thanks nce again

Hi Vignesh,

1) You cannot expect any capital appreciation in the bonds after twenty years. These bonds gives an investor yearly interest and at the end of the twenty year period the bonds are auto-redeemed and the initial investment amount returned to the investor. So after twenty years, you will not find any buyers to buy the bonds simply because the redemption is due and there is no interest to be gained if one purchases the bonds then sine the maximum tenure of the bond is twenty years.

2) Under section 2 (29A) & 2 (42A) of the Income Tax Act, the Bonds are treated as a long term capital asset if the same is held for more than 12 months where they are subject to the tax at the rate of 20% of capital gains with indexation or 10% of capital gains without indexation.

3) No, interest rate is fixed throughout the tenure of the bond. The yearly interest rate will not change.

4) Technically yes a company offering tax free bonds can default. PFC has been given the highest safety rating of AAA by CRISIL and CARE.

You can view details of the senior citizen saving scheme at http://www.indiapost.gov.in/scss.aspx or just Google for the same and you will have plenty of reliable sites such as MoneyControl.com offering further insights and details into the senior citizen saving scheme

Thanks a lot Sanjay for your inputs! Only point no. 2 is incorrect, otherwise your explanations are of great help.

Hi Vignesh, I am glad that OneMint’s efforts have contributed in making your financial life better!

Here is my response to your queries:

1. Zero capital appreciation on the date of maturity, even if the interest rates fall to the Japanese levels 20 years from now.

2. LTCG tax is calculated at a single rate of 10% in case of listed bonds/NCDs.

3. There is no chance of any coupon rate cut, it will remain the same throughout the tenure. Only the market price of the bond and its yield (YTM) will change.

4. Yes, there is chance of default, if the financial condition of the company deteriorates so badly to make it unviable for the company to meet its obligations. But, that is highly unlikely with PSUs and it gets reflected in the credit ratings of all these companies.

At present, I think tax-free bond investment is either the best or at least one of the best fixed income investment option.

http://www.indiapost.gov.in/scss.aspx

Hi Shiv!

It is nice reading your analysis on various financial issues.

Regarding your analysis on PFC Bonds 2013, I have following views to express:

1. It is good that such Bonds do not carry any holding period like the 80C Bonds. But there is a catch for investment decision. In the market (BSE) the quote for these Bonds would be quite low and it would go up (cetris paribus) as the period approaches the maturity date. Thus there would be reduced effective yield, if one decides to sell these Bonds early.

2. When rupee appreciates, foreign investors would have to bring in more amount of foreign exchange to buy same unit of investment. Thus, their effective yield would come down in dollar terms. So they would prefer India’s depreciating rupee scenario when they invest; and they would prefer rupee appreciation when they dis-invest or leave. Hence this aspect has to be analyzed from two different angles. Further, in the total gamut it has to be seen what is the total share of foreign investment in a particular investment so as to conclude whether falling or rising rupee really has any impact over the effective yield rate on bonds.

Bye and best wishes for Puja festivals.

Thanks Jagdish for kind words!

1. I completely disagree with your 1st point. NHAI tax-free bonds got issued in January 2012. Since listing, these bonds were trading at a premium to their face value (or face value + accrued interest). This month, for the first time since listing, its price has fallen below its face value, due to rising G-Sec yields and higher coupon rates this year’s tax-free bonds are offering.

So, my point is – Initially, it is not the “Time to Maturity” primarily, on which the market price of these bonds will depend, rather it is the overall interest rate environment and the government’s taxation policies on which the returns of these bonds hinge on. As the time to maturity recedes and reaches near to the maturity period, market price of a bond will slowly merge to its face value.

2. Your 2nd point is valid, but I think less than 5% foreign money pours into these tax-free bonds (though I am not sure about it). Also, nobody can ever catch the rupee movement with certainty. Nobody ever imagined early this year for rupee to have such a steep fall to 68-69 levels and when it was 68-69, nobody had an idea that it will recover to 61-62 in such a short span of time. So, nobody can be sure about these things and therefore, should be ignored, at least at the level of this forum.

Many thanks for your wishes Jagdish and you too have a wonderful festive season !!

I agree with Shiv. There is very low exposure of Foreign investors in Tax free bonds. NHAI issued bonds for 15 years fetched me Rs 1170 per bond when I sold few 6 months back. At the same time the bonds issued last year are trading at around Rs 950 because of high yield offered currently. The price of bond is very much related to yield of GSec and RBI rate. The interest rate also reflects the mood of the economy. We will not have the current situation for ever and once the environment improves the interest rate will come down and the bond price will pickup. If one is having enough money and have the stomach for long term investments, this is the right time for investment in TF bonds.

NHPC tax-free bond issue opens on October 18th. Coupon Rates are as under:

8.92% for 20 Years

8.79% for 15 Years

8.43% for 10 Years

The rates offered are absolutely same as the PFC rates. It is also rated ‘AAA’. The issue closes on the same date i.e. November 11th. You can check the application form from the link pasted above in this post.

I think, 8.71 vs 8.92 makes a difference of only 2100 rupees a year for a Rs. 10 lakh investment. So I guess if you have invested in REC, I suggest giving PFC the miss as they are both financiers to power sector and I guess it is better to diversify in that respect. HUDCO, IIFCL, upcoming NHPC, NHAI, will be better diversification bets. Although all are quasi sovereign bonds, it is better to not put too much in one sector type of company. Thats what I feel. Comments welcome. I think NHPC will also come out soon to take advantage of rise in bond yields. Also with another repo rate hike in the offing I dont rule out subsequent tax free issuers even offering higher than PFC rates.

Thanks Vivek for your views, your points are valid to a great extent!

One point I want to add here is that it is not just Rs. 2,100 difference in the annual interest which matters, the tax-free bonds like 8.92% PFC bonds will have a greater capital appreciation vis-a-vis 8.71% REC bonds, this also matters to a bond investor. If interest rates fall by 1-2% in the next 2-3 years, the capital appreciation will be much more than just Rs. 2,100 on a Rs. 10 lakh investment.

Also, it is not another Repo Rate hike which is bothering the market participants right now, it is the weak government policies, high inflation and poor economic growth for which the markets are getting jittery.

Dear Shiv,

What would be the implications on the company’s financials, credit rating and prices of these bonds, if the company is privatized by the government ?

Thanks

TCB

Dear TCB,

It is a good query. Though it would be an achievement to remember for any Indian Prime Minister to successfully privatize any of such big organizations, I think the financials would improve in 99.99% cases and credit ratings/prices of these bonds would decline to some extent initially.

Dear Shiv,

Last NDA government had privatized Maruti and IPCL through stretegic stake sale. If NDA comes to power again, to improve country’s economic condition, disinvestment / privatisation may again happen. As the duration of these bonds is very long, in case of fall in bond prices due to privatisation, investors can get stuck for a long time or would have to book loss. As I am planning to invest a good amount in these bonds, I need your valueable comments about my concern.

Thanks

TCB

Dear TCB,

I would be really really happy if that becomes a reality & I would definitely hold on to my investments in these bonds even in that situation. Trust me, you’ll see Sensex jumping at least 1,000 points the day this kind of announcement is made. You know what, India is the only big country which is facing the problems of low GDP growth, high inflation & high interest rates. Rest all countries don’t have all these problems together. G-Sec yields are higher here in India as we are considered a riskier economy to invest in.

It is a country in which the Finance Minister visits various countries to invite foreign investors to invest in the country, tries to convince them that we are taking various steps to improve situation at the ground level and the same government tries to introduce an ordinance to make convict people become our national leaders.

I think privatization alone, if done properly & transparently, can take India’s GDP growth beyond 10% and I can bet on that. Your concern is probably genuine, but disinvestment will be a big positive for the financials & valuations of these companies.

To completely buyout any of these big organisations, the private company itself is required to be quite big. There isn’t any sovereign guarantee to these bonds at present and there won’t be any in the future also. But, with privatization, I think overall interest rates would come down dramatically and there won’t be any requirement for any government support.

Support is required by weak people and weak entities. Strong people and strong entities support others.

Shiv,

Not sure if you have seen the below comment. …

Hi Shiv,

Thanks for doing a post on PFC tax free bonds. Your post lands up in the top result on google when I search for “PFC tax free bonds 2013? !!!

I have been reading comments / views given by you and other readers / investors to Mr. Ramachandran. Iam an investor who fall in 30% tax bracket and would like diversify into fixed income options. I feel I have enough exposure in equity as currently > 50% of my net worth is in equity and I am planning to book some profits in some of the stocks.

I have been reading that FMP’s (1 to 3 years) are attractive and offer good post-tax returns due to Long term capital gains tax accorded to FMP’s. I am planning to reserve some portion of fixed income to FMP’s as well instead of investing completely in tax free bonds.

1) What is your view on FMP as compared to the current tax free bonds?

2) In the current high interest rate scenario what kind of likely post tax returns can one expect from FMP’s (1 year to 3 years)? Can FMP deliver better post-tax returns than tax free bonds?

3) You present some risks associated with power financing sector in this post. What kind of risks are associated with FMP’s?

Are there any other issuers of tax free bonds expected in near future (1-2 months) apart from PFC and NHPC.

Awaiting your reply.

Thanks,

Sailesh

Hi Sailesh,

I missed your comment earlier. Here are my responses to your points:

1. FMPs have their own set of advantages and disadvantages over tax-free bonds. You can check this post having my views about it – https://www.onemint.com/2013/09/10/fixed-maturity-plans-aka-fmps-favourable-factors-checklist-for-the-investors/

2. I think one can expect 8.5-10% post-tax returns from your investment in FMPs made from 1-3 years perspective.

3. Just check the FMP post, I think you’ll get to know what risks are there with FMPs.

Overall, personally I prefer tax-free bonds over FMPs, but then certain things are in favour of FMPs over tax-free bonds from short-term perspective.

Hi Shiv,

Thanks a lot. The post on FMP’s is very informative. I agree with you. FMP’s are good from short term perspective. Currently it looks attractive due to high yields in debt instruments. Since the interest rates are relatively high, why not lock them from a long term perspective using Tax free bonds. If short term need arises, we can always sell them on stock exchange.

I will go ahead and invest in PFC tax free bonds. Looks like the issue is in good demand (already subscribed 1.98 times of base issue)

Thanks,

Sailesh

That’s great! You are bang on with your views Sailesh!

PFC subscription is largely driven by the institutional, corporate and HNI demand. Retail investors are still sleeping and should wake up in a day or two after reading subscription news online or in newspapers.

Day 1 (October 14th) subscription figures:

Category I – Rs. 320 crore as against Rs. 581.38 crore reserved

Category II – Rs. 1,202.67 crore as against Rs. 775.18 crore reserved

Category III – Rs. 619.45 crore as against Rs. 968.98 crore reserved

Category IV – Rs. 189.90 crore as against Rs. 1,550.36 crore reserved

Total Subscription – Rs. 2,332.02 crore as against total issue size of Rs. 3,875.90 crore

Super opening on Day 1 due to huge investments by the Category II & Category III investors.

Hi Shiv,

Thanks for the Day 1 update. What is the status for Day 2?

PS: Where do you get the category breakdown from? I am unable to find it at http://www.bseindia.com/markets/publicIssues/DisplayIPO.aspx?id=728&type=DPI&idtype=1&status=L&IPONo=783&startdt=10%2f14%2f2013

Day 2 (October 15th) subscription figures:

Category I – Rs. 320 crore as against Rs. 581.38 crore reserved

Category II – Rs. 1,217.90 crore as against Rs. 775.18 crore reserved

Category III – Rs. 731.65 crore as against Rs. 968.98 crore reserved

Category IV – Rs. 369.75 crore as against Rs. 1,550.36 crore reserved

Total Subscription – Rs. 2,639.30 crore as against total issue size of Rs. 3,875.90 crore

Click on “Cumulative Demand Schedule” and you’ll get the category breakdown.

Dear Sir

I was looking at the subscription figure of PFC Tax Free Bond Day 2 – October 15 th and it shows in Category II. Rs. 1,217.90. Crore as against Rs. 775.18. Crore. Reserved.

Now I am expecting fund of Rs. 10 Lac.on 23. rd October. And the Category. II. Is oversubscribed by 442. Crore on the 2 nd day.

So my question is if I apply for 10 Lac on 23 rd , can I get the Bond of full amount ( Rs. 10 Lac )

Or I will receive the partial ? And if will get the Bond of partial amount ,when I will get my money back to invest in other bonds.

If there is a oversubscribed how they make the allotment ?

Dear Paresh,

You want to invest in these bonds in some company’s name ?? I think there is some confusion you have. Category II is for corporates or non-institutional investors. For individual investors, Category III or Category IV is applicable. Category III is for investments above Rs. 10 lakhs & Category IV is for investments below Rs. 10 lakhs.

Day 3 (October 17th) subscription figures:

Category I – Rs. 320 crore as against Rs. 581.38 crore reserved

Category II – Rs. 1,221.64 crore as against Rs. 775.18 crore reserved

Category III – Rs. 937.53 crore as against Rs. 968.98 crore reserved

Category IV – Rs. 541.68 crore as against Rs. 1,550.36 crore reserved

Total Subscription – Rs. 3,020.85 crore as against total issue size of Rs. 3,875.90 crore

Hi Shiv

I want to invest from my AOP [ Association of Person ] Trust a/c. So in y ind AOP – Trust go in to Category II.

So please tell me AOP is in which category

Yes , you are right, AOP falls under Category II.

I would like to know suppose Category II is oversubscribed and by the end of issue closing date in any other category which is not fully subscribed , they can give [ transfer ] that Bond quantity to the category II applicant

in PFC bond as on to-day Category II is oversucribed. and in category I and IV not fully subscribed.

In this Bond issues they consider first come base or after completing the issue they will allot after dividing the no. of Bonds applied.

Now I got your query Paresh, but I think it is too early to do all these calculations based on such permutations & combinations. You please put the same query here either on the day of your investment or when PFC announces early closure of this issue.

But still in the current scenario and based on expected subscription numbers, I think the chances of getting allotment in Category II by making investment on 23rd are not very bright. I think the company would like to close this issue on Tuesday or Wednesday or maximum by the end of next week.

Thanks for replying instantly.

You know why i am asking you about the over subscribed Bond , if Category II is over subcribed in PFC Bond , and there are chances of not getting the full Bonds of amount which I applied , then I will apply in NHPC Bond which start from 18 th October

Earliest I can apply on Tuesday and latest by Wednesday

I am expecting NHPC issue to get fully subscribed in all the categories tomorrow itself and the issue to get closed either on Monday or Tuesday. Let’s see what happens tomorrow.

Day 4 (October 18th) subscription figures:

Category I – Rs. 360 crore as against Rs. 581.38 crore reserved

Category II – Rs. 1,223.30 crore as against Rs. 775.18 crore reserved

Category III – Rs. 977.84 crore as against Rs. 968.98 crore reserved

Category IV – Rs. 665.81 crore as against Rs. 1,550.36 crore reserved

Total Subscription – Rs. 3,226.95 crore as against total issue size of Rs. 3,875.90 crore

I am based in mumbai. Is there any way I can apply for nhpc tax free bonds online ??

Hi Harshad,

You can apply for it online with your online trading A/c. if you have any or else you’ll have to fill the physical application form. For the 2nd option, I can assist you in applying for these bonds. If you want, let me know.

i am applying on Saturday morning.. can i expect full allotment..?

As i prefer PFC over NHPC.

pls advise.

thanks..

Yes, if you are applying for it as a retail investor, you’ll get the full allotment.

As per your information both PFC and NHPC Tax free Bonds will close early latest by Tuesday.

And I think in PFC Category II I will not get the full Bond of Rs. 10 Lac. And also in NHPC also because of oversubscribing in Category II [ AOP Trust ]

So i would like to know is there and other good Tax Free Bonds are coming in near future.

Not sure about PFC, but I think NHPC should get closed latest by Tuesday or Wednesday. As you must be knowing by now, 13 companies have been allowed to raise money through these tax-free bonds, out of which 5 companies have done it so far. So, the remaining 8 companies would do that in the coming 5 months.

I think National Housing Bank (NHB) is up next in the queue, but it has not even filed its Draft Shelf Prospectus as yet. So, I expect next issue to hit only after Diwali holidays.

Day 5 (October 21st) subscription figures:

Category I – Rs. 360 crore as against Rs. 581.38 crore reserved

Category II – Rs. 1,223.69 crore as against Rs. 775.18 crore reserved

Category III – Rs. 988.72 crore as against Rs. 968.98 crore reserved

Category IV – Rs. 821.27 crore as against Rs. 1,550.36 crore reserved

Total Subscription – Rs. 3,393.68 crore as against total issue size of Rs. 3,875.90 crore

Day 6 (October 22nd) subscription figures:

Category I – Rs. 385 crore as against Rs. 581.38 crore reserved

Category II – Rs. 1,230.86 crore as against Rs. 775.18 crore reserved

Category III – Rs. 1,002.81 crore as against Rs. 968.98 crore reserved

Category IV – Rs. 926.59 crore as against Rs. 1,550.36 crore reserved

Total Subscription – Rs. 3,545.26 crore as against total issue size of Rs. 3,875.90 crore

What is the status of PFC Bond and NHPC BOnds issue ?

I would like to know whether they are still open or close ?

NHPC issue has got closed today but PFC issue is still open. Retail investors category is subscribed to the tune of Rs. 1,018.74 crore as against Rs. 1,550.36 crore reserved. I think PFC will not close the issue till the time it gets fully subscribed in the retail investors category.

Day 7 (October 23rd) subscription figures:

Category I – Rs. 385 crore as against Rs. 581.38 crore reserved

Category II – Rs. 1,240.81 crore as against Rs. 775.18 crore reserved

Category III – Rs. 1,011.53 crore as against Rs. 968.98 crore reserved

Category IV – Rs. 1,018.74 crore as against Rs. 1,550.36 crore reserved

Total Subscription – Rs. 3,656.09 crore as against total issue size of Rs. 3,875.90 crore

Shiv Sir,

I have applied for 46 number of PFC tax free bonds amounting 46,000/- on 22-Oct 2013 as I have only that much of money that day. Now I have arranged 40,000/= more on 23-Oct 2013. When I apply through ICICIDIRECT I am not able to invest as the message shows one application per account.

Please tell me whether it is possible to top up or not. If yes, how to proceed.

NR Bhatta

Hi Nawraj,

Yes, it is possible to put multiple applications in the same name under same PAN no. If you’ve another demat account, then you can apply for it online. Otherwise, you can apply for it in physical form. If you require any assistance in applying for it in physical form, just let me know.

is interest on application money taxable

Yes, interest on application money is taxable.

Dear Shiv,

In this year I have purchased REC and IIFCL bonds (2 Lakh each). I have 6 Lakh more which would like to invest in other tax free bonds. Is PFC still open for purchase? Also let me know whether PFC would be a good option or not (as REC is also from same field). Or I should wait for IRFC or others? Can you please let me know who else are likely to offer tax free bonds in this financial year?

Debasis

Dear Debasis,

Yes, PFC is still open for purchase. Till date it has got subscription worth Rs. 1,105.57 in the retail investors category out of Rs. 1,550.36 reserved.

Though it is better to avoid exposure to two companies in the same sector, it is totally your call whether you want to wait for other companies’ issues or not. There are 8 more companies which have been allowed to raise money from TFBs this financial year. Please check this link to know all those companies:

https://www.onemint.com/2013/08/16/tax-free-bonds-notification-fy-2013-14/

Day 8 (October 24th) subscription figures:

Category I – Rs. 455 crore as against Rs. 581.38 crore reserved

Category II – Rs. 1,241.02 crore as against Rs. 775.18 crore reserved

Category III – Rs. 1,021.60 crore as against Rs. 968.98 crore reserved

Category IV – Rs. 1,105.57 crore as against Rs. 1,550.36 crore reserved

Total Subscription – Rs. 3,823.19 crore as against total issue size of Rs. 3,875.90 crore

Day 9 (October 25th) subscription figures:

Category I – Rs. 455 crore as against Rs. 581.38 crore reserved

Category II – Rs. 1,241.07 crore as against Rs. 775.18 crore reserved

Category III – Rs. 1,026.31 crore as against Rs. 968.98 crore reserved

Category IV – Rs. 1,188.06 crore as against Rs. 1,550.36 crore reserved

Total Subscription – Rs. 3,910.45 crore as against total issue size of Rs. 3,875.90 crore

Dear Shiv,

Do you think there will be any listing gains in PFC bonds ? If yes, what is your estimate ?

Thanks

Dear TCB,

Listing is too far for PFC bonds, let the RBI announce its credit policy & let the CAD & inflation numbers pour in next month. In the current situation, it should not be more than Rs. 10 per bond.

The total subscription has crossed the limit but I see Category IV is still undersubscribed.

Can I invest in Category IV on Monday 28-Oct and expect an allotment? Checking if it is worth breaking my FD to subscribe to the issue.

Yes Deepak, as the retail investors category is still not fully subscribed, you’ll get 100% allotment if you apply for it on Monday.

Thanks for all your help, Shiv.

I don’t think there is any site as comprehensive as this one for the Tax Free bonds being issued in India

You are welcome Deepak and thanks for your kind words!

Hi shiv. What is the Record Date for these bonds? I read the prospectus, i was unable to find it

Hi Simple,

For PFC, the interest payment date will be exactly 1 year from the deemed date of allotment and the record date will be 15 days prior to the interest payment date. e.g. if the first interest payment date is November 15, 2014, then the record date will be November 1, 2014.

Thanks for the prompt reply. I have 1 follow up question:- The deemed date of allotment will be the day these bonds list, or 1 day prior to listing? Or will the deemed date be the date these bonds get credited in the demat a/c of individual retail investors? Usually, bonds get credited over a period of 2-3 days to different retail investors and I am assuming that there can be only one record date for the entire issue

Let me answer this question with an example – Deemed date of allotment is always fixed prior to the date of listing. In the case of REC issue, the bonds got credited in the demat accounts on September 27th, got listed on September 30th, whereas the deemed date of allotment is September 24th.

Ok got it! Thank you 🙂

You are welcome Simple! 🙂

Hi Shiv, (I have given the same suggestion to Manshu. Please speak to him as well)

There are a number of tax free bonds in the market every year, for the past 3 years.

The interest rates are different for each bond in each year!

What makes it more complicated is that the interest rates are different for the same bond if you have got a direct allotment or bought it from the stock market.

Each one comes with a different date of interest payment.

With all this, it has become really difficult to track the interest payment. I also find it difficult to link the bonds to their Scrip ID and Code because of the long list of bonds in my statement.

I also don’t know in which month will I receive the interest of the bonds that I purchased last year.

Would it be possible for you to have a table with the following details as one of your articles?

Company

Year of Issue

ISIN

Scrip Id

Scrip Code

Rate of Interest (Direct Allotment)

Rate of Interest (If purchased later)

Due date of interest

And anything else that you find appropriate…

I’m certain it would benefit a lot of people.

Regards,

Deepak

Hi Deepak, I’ll definitely try to do such a post and provide all information in a single post. You want me to do it right away or wait for this financial year to end & then do it sometime in April? If I do it now, there will be a lot many issues which will get left out. Just let me know.

Thanks a lot for considering this in the first place, Shiv.

The financial year end is 5 months away 🙁

Is it possible for you to create a list, and then keep updating the same as and when new issues hit the market?

You might get some more suggestions when you publish the first draft.

One more thing that I note down for my investments is the Maturity Date – which I don’t know for many of these tax free bonds that I own 🙁

Thanks again…

Regards,

Deepak

ok, let me check if it is feasible or not. I’ll do that once PFC & IIFCL bonds get listed. If it skips my mind, just remind me once.

Would it be possible for you to work on this now?

Trust me, you will have an enviable bible when you complete the same…

Sure Deepak, I’ll work on it after covering HUDCO Tranche II and NTPC bond issues.

Day 10 (October 28th) subscription figures:

Category I – Rs. 515 crore as against Rs. 581.38 crore reserved

Category II – Rs. 1,242.32 crore as against Rs. 775.18 crore reserved

Category III – Rs. 1,029.76 crore as against Rs. 968.98 crore reserved

Category IV – Rs. 1,293.24 crore as against Rs. 1,550.36 crore reserved

Total Subscription – Rs. 4,080.32 crore as against total issue size of Rs. 3,875.90 crore

Hi Shiv,

I had applied this afternoon at 2.30pm under Cat 4. Is it safe to assume that the nos published for 28th presumably includes my application money too?

Thanks,

Subbu

Hi Subbu,

I don’t know which is the mode through which you’ve applied for it, but most likely it is included in today’s subscription figures.

Dear Shiv,

Based on RBI’s credit policy announced today, can you please share your views about possibility of future rate hikes and possibility of future bonds being issued with higher coupan rates ?

Thanks

Hi TCB,

As I had mentioned earlier also, 0.25% hike in Repo Rate & 0.25% cut in MSF Rate was already factored in by the markets. After the policy actions by the RBI, stock markets have risen & G-Sec rates have fallen slightly.

Further policy actions by the RBI will depend on inflation, fiscal deficit, policy actions by the govt, growth in industrial production, international oil prices, QE tapering etc.

We know by now that Coupon Rates of Tax-Free Bonds are linked to the benchmark G-Sec rates. As of now, I don’t think that the coupon rates will be higher with the upcoming tax-free bonds.

Day 11 (October 29th) subscription figures:

Category I – Rs. 515 crore as against Rs. 581.38 crore reserved

Category II – Rs. 1,242.42 crore as against Rs. 775.18 crore reserved

Category III – Rs. 1,029.46 crore as against Rs. 968.98 crore reserved

Category IV – Rs. 1,357.85 crore as against Rs. 1,550.36 crore reserved

Total Subscription – Rs. 4,144.74 crore as against total issue size of Rs. 3,875.90 crore

Any update on today’s figures?

Hi Shiv,

Could you please share today’s figures, or let me know where I can get them? They don’t turn up on a Google search…

Regards,

Deepak

I would like to know if someone like to invest in tax free bond after 10 th November , he should wait for the another Tax Free Bonds which are coming in next 5 months [ Before 31 st March ] for more coupon rate [ Interest ] or if you think that coupon rates will not be higher than this PFC Bond / NHPC Bond then he should buy from the market.

I have some funds in the month of November , what should i do ?

Should i buy from the market [ NSE / BSE ]

What will be the coupon rate [ approximate ] for the next issues of coming Bonds you think ?

Hi Paresh,

As of now, it is not possible to guesstimate the coupon rates on the upcoming tax-free bond issues. You just need to compare the yields of listed bonds with the coupon rates these bonds are offering. Whichever is higher after deducting your brokerage charges, you should go with that.

Day 12 (October 30th) subscription figures:

Category I – Rs. 565 crore as against Rs. 581.38 crore reserved

Category II – Rs. 1,242.43 crore as against Rs. 775.18 crore reserved

Category III – Rs. 1,037.16 crore as against Rs. 968.98 crore reserved

Category IV – Rs. 1,417.72 crore as against Rs. 1,550.36 crore reserved

Total Subscription – Rs. 4,262.32 crore as against total issue size of Rs. 3,875.90 crore

Hi Shiv,

From the figures, it seems that the category IV (i assume this is retail) is not fully subscribed as yet. What are the chances of getting full allotment tomorrow (1st Nov) ?

Also is a brokerage charged if i buy through my trading account ?

Thanks in Advance

Hi Aditya,

As of today, Category IV has got subscribed to the tune of Rs. 1,508.11 crore. If you invest in it tomorrow, I think you’ll get approximately 50% allotment.

Yes, brokerage is charged if you buy it through your trading account. In fact, ICICI Direct charges 1% for NCDs/Bonds.

Hi Aditya,

Brokerage is charged if you buy it from the secondary markets through your trading account. If applied during the offer period, no brokerage is charged.

Day 13 (October 31st) subscription figures:

Category I – Rs. 581 crore as against Rs. 581.38 crore reserved

Category II – Rs. 1,245.73 crore as against Rs. 775.18 crore reserved

Category III – Rs. 1,039.56 crore as against Rs. 968.98 crore reserved

Category IV – Rs. 1,508.11 crore as against Rs. 1,550.36 crore reserved

Total Subscription – Rs. 4,374.40 crore as against total issue size of Rs. 3,875.90 crore

The issue should get closed on November 5th i.e. Tuesday. November 4th is an exchange holiday.

Shiv – I guess ICICI Direct charges brokerage only when you buy / sell in secondary market. Not at the time of initial offer?

Mr. Jitendra is right. My experience with ICICIDIRECT is that they don’t charge any brokerage for IPO’s – guess they get their cut from the issue managers (0.75% of bid is a figure I am told is involved in IPO collections).

On the other hand, my experience is that for secondary market bond transactions, they charge a hefty 1.2% brokerage (for transaction value > 10,000 rupees). This I feel is rather high; and therefore have taken Shiv’s sensible suggestion to avoid the secondary market.

Yes Mr. Ramachandran, Jitendra is right. Thanks!

Hi Jitendra,

That is exactly what I meant when I mentioned about 1% charges. These charges are levied only when you buy these bonds/NCDs from the secondary markets and not when you apply in the initial offer.

When I answered Aditya’s query, I thought he was asking about buying these bonds from the secondary markets. My apologies if my answer (due to misunderstanding Aditya’s query) created some kind of confusion.

When the market price of these PFC bonds changes e..g reduces then the face value. Say at the end of 10th year when the auto redemption is to happen if the market price for these bonds is 900 what will be the return of principal to the investor during the auto redemption.. will the investor get 1000 RS as that was the face value of the bond or will the investor get 900 as the market value on the 10th year was.

Hi Uma,

First of all, what you are saying is not possible. On or a few days before the maturity date, the market price cannot be significantly below the Face Value. Nobody would be willing to sell you his/her holdings at Rs. 900 just a few days before the maturity date.

Moreover, you’ll get Rs. 1,000 back at the end of maturity period irrespective of its market price. PFC will pay you back your principal investment of Rs. 1,000.

Day 14 (November 1st) subscription figures:

Category I – Rs. 581 crore as against Rs. 581.38 crore reserved

Category II – Rs. 1,245.73 crore as against Rs. 775.18 crore reserved

Category III – Rs. 1,042.16 crore as against Rs. 968.98 crore reserved

Category IV – Rs. 1,551.57 crore as against Rs. 1,550.36 crore reserved

Total Subscription – Rs. 4,420.46 crore as against total issue size of Rs. 3,875.90 crore

Hi Shiv,

Wish you and all the readers onemint a happy Diwali!!

Just curious to know now that the Cat 4 is fully subscribed and in fact oversubscribed by about 1 crore how would the allotment happen? Would they do proportionate or the last 1 crore investments will be refunded or prioritized over other Categories?

Hi Subbu,

Thank you and wish you too a very Happy & Prosperous Diwali !!

As you mentioned, in such a situation, only those investors who have applied for it on November 1st will get allotment on a proportionate basis. I mean only Rs. 42.25 crore worth of bonds were left for subscription till Friday morning, but Rs. 43.46 crore worth of bids got submitted during the day. So, the investors will get allotment in the ratio of 42.25:43.46.

Remaining investors will get 100% allotment for their investment to the tune of Rs. 1,508.11 crore.

The issue should get closed as soon as PFC decides to do that. If Category I investors decide not to go for the remaining 0.38 crore bonds reserved for them, then it would be given to the Category IV investors first.

PFC 8.92% tax-free bonds issue is getting closed today i.e. November 5th.

Hi Shiv,

Interestingly there are further Cat 4 bids today and wonder how this’ll be handled since in the previous trading session itself the oversubscription limit has been crossed. Will everyone will start getting a cut or these new monies will be returned?

Hi Subbu,

Bids made today will get their money refunded without any allotment. They’ll only get interest on their money @ 5% p.a. till the deemed date of allotment.

Hi Shiv,

Looks like the Cat 1 has not bid for the 0.38 crore balance and that should flow on to the Cat 4. So the revised equation for those who applied on 1st Nov, if I understood it right, should get 9.8 bonds per 10 applied and for those prior to 1st Nov should get 10 out 10 applied. Is that right?

Hi Subbu,

If Category I investors apply for the remaining 0.38 crore bonds today, then the retail investors won’t get this pie.

Thanks shiv for the continuous updates.

When will I be able to know whether units allotted or not ?

Thanks

Thanks Vignesh,

I think by November 15th or November 18th you’ll get to know the allotment status.

Hi shiv – any idea on nhb / IRFC issues?? Probable issue opening date??

Hi Jitendra,

No issue lined up as of now. None of these companies, including NHB, IRFC, NTPC, NHAI etc., has even filed its draft shelf prospectus. NHB, NTPC & NHAI have announced their plans to raise money, but most likely they’ll launch their issues either in the last week of November or sometime in December.

Day 15 (November 5th) subscription figures:

Category I – Rs. 581 crore as against Rs. 581.38 crore reserved

Category II – Rs. 1,246.74 crore as against Rs. 775.18 crore reserved

Category III – Rs. 1,044.24 crore as against Rs. 968.98 crore reserved

Category IV – Rs. 1,596.84 crore as against Rs. 1,550.36 crore reserved

Total Subscription – Rs. 4,468.32 crore as against total issue size of Rs. 3,875.90 crore

This issue stands closed now.

Hi Shiv. I have 2 fundamental questions.

The 10 year Bond yield today was at 8.82 and yet the price of the recently issued REC 8.72% 10 year bonds was at a 13 rupee premium despite offering a 10 basis points lower yield.

10 days ago, when the NHPC and the PFC issues were open, the 10 year yield was between 8.57-8.68 and the price of the REC 8.72 bonds was below 1000/-

What is the explanation for this? Aren’t bond prices and yield supposed to be inversely proportional?

Secondly, the NHAI 8.20% bonds issued last year are trading only 2 rupees below their issue price despite the difference between yields being 60 basis points. Shouldn’t those bonds trade much lower?

Hi Simple,

Nothing can change the law of finance. Bond prices and yields are always inversely related. But, you cannot relate yield of one security (G-Secs here) with the price of the other security (TFBs).

1. I think one of the reasons behind this upmove is – Interest is getting accrued on the principal investment of Rs. 1,000. REC bonds got allotted one & a half months back and I think the price reflects some accrued interest also.

Secondly, I think immediate sellers/speculators are slowly going away by selling off their holdings. So, when the supply gets absorbed in by the market, you are bound to see upsurge in its price.

Thirdly, NHPC got listed today and closed at around Rs. 1,016 on the NSE. So, probably the difference between 8.62% REC bonds & 8.92% NHPC bonds is getting reflected here.

Listing of REC bonds at Par & NHPC bonds at a premium gives me a feeling that these tax-free bond issues are really attractive for Category I/II/III investors due to the terms set for these issues this financial year.

There might be some other factors also, probably I am not aware of those factors.

2. Anybody, who buys NHAI 8.20% bonds from the secondary markets, gets 8.20% rate of interest, even if it is an institutional investor. So, I think you should compare 8.20% with REC’s 8.01% for 10 years. Also, interest payment date of NHAI bonds is October 1, so its price should also reflect some accrued interest.

These explanations do not mean that there can never be mismatches between the intrinsic values of these bonds and their market prices. Opportunities are always there in all kind of markets.

Thank You for the detailed and prompt reply! 🙂

You are welcome!

Hi,

Are there any future bonds in the pipeline, which are safe to invest( government type bonds) and also which can give good returns?. I am looking for a horizon of 5-10 years of lock-in investment .

When I say secure, for e.g if I invest in some bond, and if it gets defaulter list, then also we get our money back. Unlike the private organizations, where if it is defaulted, the money is lost ( for .eg UTI bonds issue few years ago)

Hi Prash,

There is no such govt. guaranteed bond in which you get your money back even if the issuer company defaults on its payments. Post Office schemes are the safest to invest from that point of view.

Thanks Shiv for confirmation and sharing your knowledge. You are doing an awesome job educating people on the web. Keep it up!!!

Please share whenever you hear about any good upcoming bonds , whenever you have that info.

Take care,

Prash

Thanks Prash!

We keep on writing on various topics of personal finance. You just need to subscribe to our newsletter, its free & doesn’t involve any kind of selling tactics. Whenever any such investment opportunity comes, I am sure we’ll write about it and that ways you’ll get to know about it.

Hi Shiv,

The bond yields have soared up this week and have reached levels of 8.90-8.95. How will this affect the coupon rate of the upcoming tax-free bonds issues by NHAI and IRFC ?

Hi Aditya,

Looking at a steady upmove in the govt. bond yields, it seems to me that there will be an increase in the coupon rates of the upcoming bonds. But, then it depends on their timings also. WPI & CPI inflation figures next week will be quite important.

Hi Shiv,

Read about the draft prospectus of IRFC Tax Free Bonds..Any news when the subscription will start ?

Hi Aditya,

IRFC issue will take at least 15-20 days to hit the streets. IIFCL is planning to launch its Tranche 2 before that.

Thanks Shiv…As ususal very very prompt reply.

Does IRFC have a better rating than IIFCL ? Thanks in advance.

It cannot be higher than ‘AAA’ Aditya and both these companies are entitled to ‘AAA’ rating.

🙂 … sorry i confused it with the Hudco ratings !!

HUDCO is the only company which has issued its tax-free bonds this financial year with AA+ rating. Rest all have AAA ratings so far.

Hi Shiv

Why do bond prices fall just prior to the record date? Shouldn’t prices rise so as to deter people from buying them for a very very short term just to get the interest? Isn’t it detrimental to long term holders?

Sorry Simple, I haven’t closely observed such a price fall before every record date. If you’ve any such data, please share it with me.

I have read it very often in the pink papers that bond prices fall just before a record date as the interest money is factored in. Eg, today the price of REC bonds fell by 13 rupees (its record date is on the 15th). Yesterday, when the G-sec yields was at 9.20%, the same bond had touched an intra-day high of 1023. Today the G-sec yield was below 9% and yet the bond price fell

All these bonds become “Ex-Interest” 2 working days prior to their “Record Dates”. That is why you see a fall in their prices the day they become ex-interest. All the bondholders whose names appear in the books of the Registrar on the record date are entitled to this interest. I’ll try do a post on the same with your REC example.

How can a bond become ex-interest “2 days prior” to the record date? You are entitled to interest if the Bonds are in your Demat a/c on the day of the record date. So shouldn’t the bonds become ex-interest 1 day prior to the record date? (since it takes 2 days for the bonds to reflect in your a/c)

For example, if the record date for a bond is 15th, and I buy them on 13th, wouldn’t I be be entitled to get the interest?

Yes, it is as per T+2 settlement. If you buy a bond on the “ex-interest” date, you won’t be entitled to the interest due. As November 15th is a trading holiday, that is why REC bonds became ex-interest on 13th itself.

Got it! thank you 🙂

I will be looking forward to your post on record dates and ex-interest price movements of bonds

Do you advise selling these REC bonds now that they are ex interest and freeing up funds for the upcoming IRFC/IIFCL issues? Do you think the yields offered will be better for these bonds now that both CPI (10.09%) & WPI (7%) nos are out?

Also, will you be informing us about the deemed date of allotment for PFC bonds along with the BSE code?

Yes Simple, I’ll update the BSE codes and other relevant data once PFC bonds get listed.

Also, both CPI inflation as well as WPI inflation figures are disturbing. Yes, I do expect coupon rates to be higher with the IIFCL & IRFC issues, but then it depends on their timings also.

There are many factors which I analyse before I take final call on holding or selling these bonds. That is why I won’t be able to advise you as an individual here whether to sell or hold your REC bonds. I sold some of my NHPC bond holdings today after the WPI inflation data, as I expect rates to be higher in the upcoming issues.

Thank You Shiv. You have been of great help!

You are welcome Simple! 🙂

I have invested in REC N 2 Tax Free Bonds in April 2013. I have total 2025 Bonds purchased @ Rs. 1005/00 from the market and coupon rate on this Bond is 7.38 %.

I need your advise…….Should I sell this Bonds at current price between Rs. 925 to Rs. 935 .. and then invest in coming new Tax Free BOndsdirectly which give higher Coupon Rate.

My status for Income Tax purpose is A O P [ Association Of Person…Tax rate is 30 % from the 1 st rupee income. ] like in PFC Tax Free Bonds [ for 20 years ] i can get only 8.67 % coupon rate. Not higher then this.

Kindly guide me what should I do. I am waiting for the next issue and i hope the coupon rate will be 8. 67% or higher then this.

Sorry Paresh, but I cannot take such personalized queries here on this forum.

When is PFC getting listed? Are there any new bonds coming up?

Hi Vivek,

PFC should get listed in the next 2-3 working days. IIFCL and IRFC are planning to launch their issues in the near future.

I don’t know how exactly it works, but I felt by reading your article that it is worth an investment. So I applied for it via my axisdirect account. However, I don’t see any updates on it though you say that it is closed now. Does it take some time for the results to come out? Money has been deducted from my linked account, but it is not showing in my axisdirect account that it has been allocated to me. Nor has money come back to my account in case it has not been allotted.

Please clarify.

Hi Mukesh,

It takes up to 12 working days for these companies to allot these bonds & get them listed. You can expect PFC to allot you the bonds & pay the interest due on your application money within next 2 working days.

Thanks for the clarification, Shiv.

When I contacted AxisDirect with same query, they simply asked me to contact Karvy. When I said them I don’t know who to contact and what to ask, and it is their duty to update me, they just repeated themselves asking me to contact Karvy.

As compared to them, your reply was informative and to the point. Appreciate it.

Thanks Mr. Mukesh! Most of the companies dealing in financial products here in India are sales-oriented. Their after-sales service levels are very poor. There are many factors behind it, some are genuine & acceptable, but some are really unacceptable. That is the way we get things here.

I’ve got the PFC tax-free bonds credited to my demat account today. I think the bonds will get listed on the BSE on Wednesday.

Thanks Shiv for confirmation.

I applied for 2 set of Pfc bonds one early and one very late. I recieved confirmation for 1st set , however for the second one looks like I didn’t get d allotment

You must have applied for it on November 5th Prash for you not to get any allotment in the 2nd set.

Hi Shiv

Do you know when next tax free bond issue will hit the market? I see IRFC has already filed prospectus with SEBI. NTPC and NHB are in the news. Any confirmed dates when next tax free bonds will be issued? What is your guess on interest rates for future TFB. Thanks a lot for your response in advance

Regards

Ramadas

Hi Ramadas,

IIFCL, IRFC, NTPC & NHB are lined up to be issue these tax-free bonds, but dates are yet to be announced. I think at least a couple of them should hit the market in the last week of November. Not 100% sure, but I think coupon rate should cross 9% this time for the 20 year option.

I also got confirmation today. Thanks for the update.

You are welcome Mukesh!

Hi Shiv!

Could you give the link to check the allotment status, BSE code for these bonds, the deemed date of allotment & the record date?

Hi Simple,

At present, these links are not uploaded. I’ll share them once I’ve have them.

I sold half of my IIFCL Bonds at 1015 on icicdirect. after 1% brokerage i will get 1000 only. But I think better rates will come in coming months. Will sell rest tomorrow. Anyone with good reason not to exit.

ICICI Direct’s 1% brokerage is too much for NCDs. If I were at your place, I would have got one more demat account opened.

I think it is a good idea to sell at least half of your holdings.

PFC tax-free bonds to get listed on the BSE on November 20th i.e. Wednesday.

Here are the BSE codes for the same:

8.43% 10-year bonds – BSE Code – 961802

8.79% 15-year bonds – BSE Code – 961803

8.92% 20-year bonds – BSE Code – 961804

Deemed date of allotment has been fixed as November 16, 2013. Interest will be paid on November 16th every year.

Source: http://www.bseindia.com/markets/MarketInfo/DispNewNoticesCirculars.aspx?page=20131119-17

What is the Record Date? It is not mentioned in the circular

Record Date is there in the prospectus – It is 15 days prior to the Interest Payment Date.

Can you confirm if it is 1st or 2nd November?

Sorry Vivek, I am not sure whether it would be November 1st or November 2nd or October 31st every year. It is decided every year by the board of the company and then a filing is made with the exchange. Here is an example:

http://nseindia.com/corporates/corpInfo/equities/AnnouncementDetail.jsp?symbol=NHAI&desc=Record+Date&tstamp=300820131249&

PFC bonds got listed today on the BSE. 8.92% 20-year bonds hit a high of Rs. 1,008, a low of Rs. 1,001.01 and closed at Rs. 1,006.50 with total 22,172 bonds traded during the day.

RBI is bringing new benchmark Bond, how it would affect yields and upcoming bond’s coupon rate?

Hi Shashwat, I’m not sure how it would affect bond yields and the coupon rates of upcoming tax-free bond issues. Don’t want to make wild guesses either.

curently they are tagged to benchmark average for last 2 weeks so after the new benchmark will bonds be tagged to new one?

Yes, it will be like that only.

Hi Shashwat,

Please check this link – http://www.business-standard.com/article/finance/bond-spread-set-to-widen-with-new-10-year-benchmark-113112300133_1.html

It is a nice read to understand what’s happening in the bond market with 10-year benchmark govt bond.

Below link still shows yield 9.10%.

http://www.bloomberg.com/quote/GIND10YR:IND

The new 10 year benchmark yield is 8.78% and expected to fall as per this article. So no hope of 9%+ bonds now from IRFC and IIFCL ?

OR

till the time old g-sec remains benchmark we can expect higher rates on upcoming TFBs

PLEASE ANSWER THE QUESTION

Yes Shashwat, till the time 7.16% G-Sec is there, it’ll remain the benchmark and the 10-year coupon rate will be linked to it.

Hi Shiv,

Any news on the opening dates for IIFCL , IRFC and NTPC bond issues ? 10-year bond yields have crossed 9% , so expecting a good coupon rate for these issues.

Hi Aditya, no news on the opening date of any of the issues as yet.

hi shiv

I have applied for PFC on day 2 itself in retail category. very initial days of opening. but today I received back my amount. I applied online via Fundsindia.

what could be the reason shiv ?

Hi Vignesh,

Though it is very strange that it has happened, I think this is due to some mistake/error by FundsIndia in submitting/bidding your application. You should write a mail to Karvy Computershare asking the reason for your application getting rejected.

how much commission do u give to the retail cutomer if one submits an application for a bond issue through you?

Nothing Sandy. We deserve what we earn for our services/efforts. Also, as per SEBI, it is illegal to share your incentives.

IRFC bonds to come in December. http://www.deccanherald.com/content/370457/railways-tax-free-bonds-likely.html

Yes, IRFC issue is expected in the first week of December.

Drastic fall in yield today. Prospectus has to filed this week as last two weeks average yield was 9%+. Any updates?

7.16% G-Sec yield is still trading at 9.04%. It is the new 8.83% G-Sec which has a yield of 8.74% and that is why the Bloomberg chart is showing a steep decline in 10-year Indian G-Sec.