This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

With rising inflation and high fiscal deficit here in India, yields on government securities are also rising and high G-Sec yields bring along some good investment opportunities for the prospective tax-free bond investors. Many of the investors, who could not invest in the previous five tax-free bond issues of REC, HUDCO, IIFCL, PFC and NHPC, have been eagerly waiting for the new issues to get launched.

A few days back Ramadas asked me if I know when the next tax free bond issue will hit the market. Here is what he had to say:

Ramadas November 19, 2013 at 7:16 am

Hi Shiv

Do you know when next tax free bond issue will hit the market? I see IRFC has already filed prospectus with SEBI. NTPC and NHB are in the news. Any confirmed dates when next tax free bonds will be issued?

I have received many such queries in the past 15-20 days as many people have been asking this question on different posts.

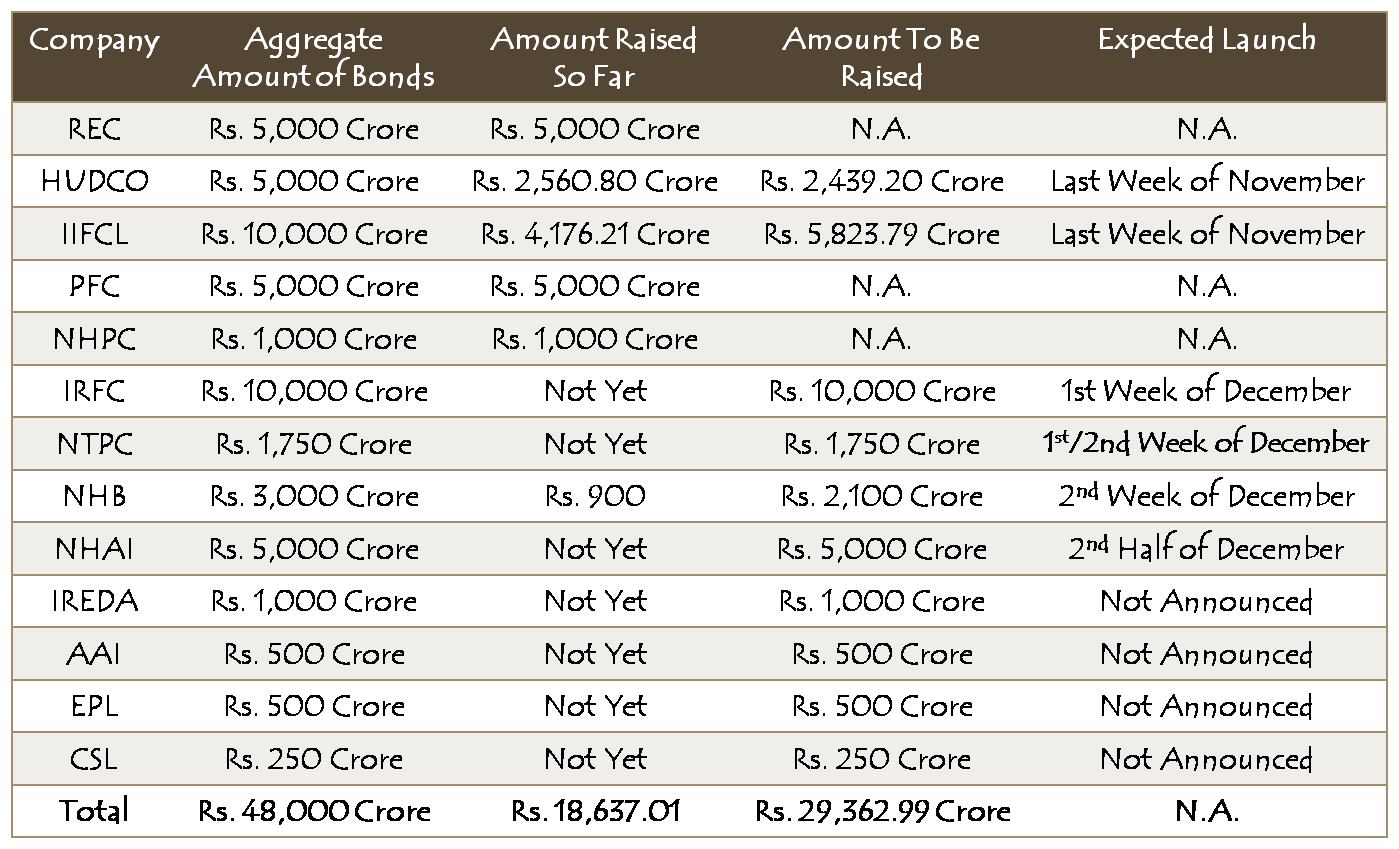

As none of the companies has filed the final prospectus for its issue, nobody knows the exact opening dates of the upcoming tax free bond issues. But, with whatever information I have and based on the dates of filing of their draft shelf prospectus, here is the list of tax free bond issues which are going to hit the streets in the next one month or so.

IIFCL Issue – Last week of November – IIFCL announced earlier this month that it would launch the second tranche of its tax free bonds in the third or the fourth week of November. IIFCL has already raised around Rs. 4,200 crore out of Rs. 10,000 crore it has been allowed to raise from tax-free bonds this financial year.

HUDCO Issue – Last week of November – I have been told by a close associate that HUDCO is also planning to launch the second tranche of its tax-free bonds issue in the next 3-5 days time. The company could raise around Rs. 2,400 crore in the first tranche which got closed on October 14. HUDCO still has the authority to raise another Rs. 2,400 crore.

IRFC Issue – First week of December – IRFC filed the draft shelf prospectus with SEBI to raise Rs. 10,000 crore from its tax-free bonds issues on November 11. As observed in the past, it takes around 15-20 days for a company to launch its public issue from the date it files the draft shelf prospectus.

Also, as Shashwat shared it yesterday, an official of IRFC has told Deccan Herald that it is planning to launch its public issue in December. Taking a cue from it, I think IRFC issue should hit the streets in the first week of December.

NTPC Issue – First week of December – Just a few days after IRFC did it, NTPC also filed the draft shelf prospectus on November 15 to raise Rs. 1,750 crore from tax-free bonds. So, I expect NTPC issue also to hit either in the first week or the second week of December.

NHB Issue – Second week of December – Though NHB raised Rs. 900 crore from these bonds through private placement in August this year, it has taken more than usual time to do it through its public issue. But, now they have officially announced to launch its issue in the second week of December. I hope they do not delay it further.

NHAI Issue – Second half of December – Last month, NHAI announced its plan to raise funds through these bonds sometime in December. But, as the company has still not filed its draft shelf prospectus as yet, I do not see the issue hitting the streets before second half of December.

November was a dry month as far as tax free bond issues are concerned. But, if all these issues get launched sometime next month, it would really create a glut for these bonds in the market.

Thanks to the high interest rates scenario, these companies would find it less difficult to attract investors’ money to get invested in these bonds.

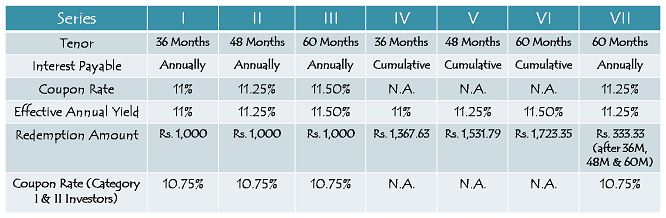

I’ll update this post as and when I have any information about any new issue getting launched and the coupon rates it is going to carry. If any of you get any kind of information, please share it here so that all of us benefit out of it.

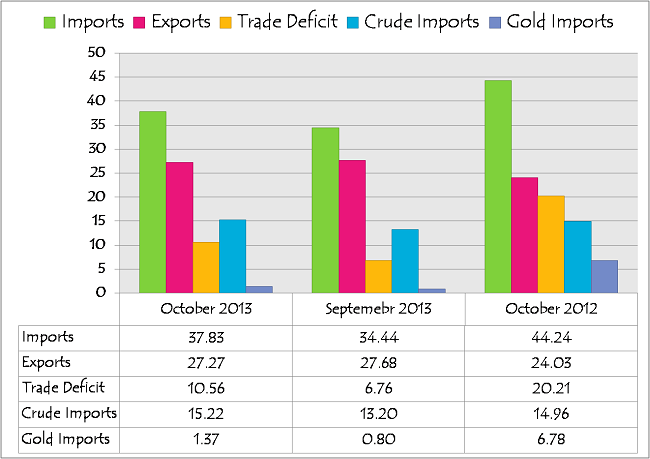

(Note: Figures are in US $ billion)

(Note: Figures are in US $ billion)

My screening technique is very simple and inspired by Peter Lynch’s One Up On Wall Street where he talks about using the power of your common knowledge, and investing in companies you deal with every day.

Following these techniques has been profitable and fun for me. I believe it’s important for this to be fun because if you’re not a professional, you won’t be able to practice these techniques if they aren’t fun.

Who makes this great product?

I watched “Thor: Dark World” in 3D yesterday, and enjoyed it quite a bit. I have seen the last Thor movie as well, but at that time I didn’t notice Thor is a Marvel character. Before the movie, they played trailers of other upcoming movies with Marvel characters, and I made a mental note to look at Marvel to see if it may be a good buy.

Two other companies that caught my eye were IMAX, and I have bought and sold IMAX at a profit in the past, and RealD, which is the company that makes the 3D glasses for these movies. I have screened RealD earlier and avoided it because of the competition they face, and also the emphasis on re-use of 3D glasses.

Earlier in the day I spent a long time in the snaking queues of Banana Republic, and window shopped a Prada store because I can’t afford anything there. Both these companies seem to be excellent stock picks, and just keeping an eye out for popular products is a great way to screen companies.

You also read about trends like 3D printing and drones, and it is a good idea to see if there are any good companies operating in those areas. When I first learned about 3D printing, I thought it was a very new field, and it would be difficult to find any profitable companies operating in this area but then I discovered 3D Systems which has also been a very profitable stock for me.

Another way to screen companies is to see what enterprise software you use, and if there are any good companies operating in that field.

I was a regular reader of Business India and Business World, and they feature a lot of good companies that you can analyze further. I remember reading a glowing review of Jain Irrigation Systems in Business India many years ago and thinking about buying the stock — I never did, and the stock was a multi-bagger in the years to follow.

Reading about investments from others is also a good way to identify stocks. You can do this easier than ever before by using Twitter, and following people who are interested in investments.

Good ideas are all around you when you are actively seeking them.

Is it listed?

That’s the question I ask myself often. Yesterday I learned that Marvel is owned by Disney, and both Banana Republic and Prada are private companies that you can’t invest in.

That will be the case with a lot of companies but you have to go through them to find the ones that are listed and could be potential buys. If it is listed then you can go to the “Investor Relations” section on their website and read more about the company, if not, you move to the next idea.

Currently, I own seven stocks and one ETF. I’m a customer of six out of the seven companies, the only one that I don’t knowingly use the products of is Huntsman Corporation, which I bought a couple of years ago because it had a dividend yield of 4%, and steady financials. This stock is over 100% of my purchase price today, and I felt like this would be a good buy when I chanced upon it.

You obviously make mistakes in this process as well, and one good example is Primo Water that I sold at a 50% loss sometime last year. This is a company that sells water, and they ran into financial troubles last year.

Evaluating a company

Not every company that makes a good product will be a profitable company, and not every profitable company will result in a profitable stock. HLL and Infosys are good examples of these. These two stocks were the darlings of investors some years ago, but after a while they lost their favor with investors and were never able to give the returns they once did. They are still good companies that own great brands, and provide great service, but due to other factors they haven’t been great stocks for the past few years.

This is an important thing to understand because it is not very intuitive. My own understanding of this concept became very clear in running OneMint. OneMint is a good product that has benefited a lot of people, but at the same time it has a non existent business model and if it were a stock I wouldn’t invest in it. Just providing value to people is not enough, there has to be a good business model and a way to monetize that value or else the business will never be profitable.

Even if a business is profitable, you have to look at its valuation to see if that justifies the current price, and leaves room for growth.I’m going to do a follow up post on this sometime this week, and share some of my ideas on how to measure this.