Double Your Money in 6 Years with Muthoot Finance NCDs – November 2013 Issue

This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

Muthoot Finance has again come out with a public issue of its secured and unsecured non-convertible debentures (NCDs) and it has been launched from today. This would be the second issue from Muthoot Finance this financial year after it raised Rs. 300 crore in September from its first issue.

The issue will remain open for two weeks to get closed on December 2nd i.e. first Monday of December. The company may extend the closing date of the issue or preclose it, depending on the response for the issue.

Most of the features of the current issue, including its coupon rates for the retail investors, are same as they were in the first issue. Let us first have a look at all of its features.

Size of the issue – The company plans to raise Rs. 300 crore from this issue as well, including the green shoe option of Rs. 150 crore.

Coupon Rates – Like Muthoot offered in its earlier issue as well, the company promises to double your investment amount in 6 years’ time i.e. 72 months with an effective yield of 12.25% per annum. But, NCDs issued under this option are ‘Unsecured’ in nature.

Apart from this option, it is offering coupon rates ranging from 11% to 12.25% with different maturity periods and different interest payment options as you can very well check from the table below.

Coupon Rates for Institutional Investors – This is one significant change Muthoot has made as compared to its first issue. Muthoot has decided to offer a lower rate of interest to the institutional investors and the difference is of 75 basis points (or 0.75%) across all the options, except option VII. The difference is of 0.25% only with option VII.

Categories of Investors & Allocation Ratio – The investors have been classified in the following three categories and as always, each category will have certain percentage fixed for the allotment:

Category I – Institutional Investors – 15% of the issue is reserved

Category II – Non-Institutional Investors & Corporates – 35% of the issue is reserved

Category III – Retail Individual Investors including HUFs – 50% of the issue is reserved

NCDs will be allotted on a first come first served basis in all these categories.

NRI Investment – Like its first issue, non-resident Indians (NRIs) are not allowed to invest in this issue as well.

Ratings & Nature of NCDs – There are two rating agencies involved in this issue – CRISIL and ICRA and both have assigned ‘AA-/Negative’ rating to this issue. All these NCDs are ‘Secured’ in nature, except NCDs issued under option XI which offer to double your money.

Listing, Demat & TDS – Muthoot has proposed to list its NCDs only on the Bombay Stock Exchange (BSE). Investors will again have the option to apply these NCDs in physical form as well as demat form under options I to VI. Applicants cannot apply for allotment of these NCDs in physical form under options VII to XI i.e. these NCDs will be allotted only in dematerialised form under options VII to XI.

Again, the interest earned will be taxable as per the tax slab of the investor and TDS will be applicable if the interest amount exceeds Rs. 5,000. But, NCDs taken in the demat form will not attract any TDS on the interest income.

Minimum Investment – Minimum investment in this issue as well has been fixed as Rs. 10,000 i.e. 10 bonds of face value Rs. 1,000.

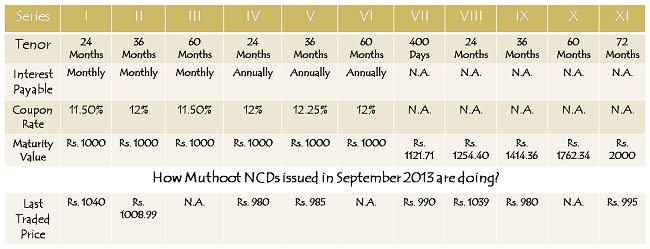

Muthoot NCDs, issued in the first issue this year, have allotment date of September 25th i.e. they were issued around two months back. As you can check from the table above, most of these NCDs are still trading below their face value.

Also, liquidity is very poor with these NCDs, especially under unpopular options like cumulative interest & annual interest options and also with longer duration options of 60 months & more.

Interest rates have also risen since then. So, if I need to invest my money in Muthoot NCDs, I would go for already listed NCDs rather than buying them from the company in this issue.

Also, gold financing sector overall is not doing that great, but Muthoot is a key player in this sector. Investors need to factor in all these variables before applying for these NCDs.

Application Form of Muthoot NCDs

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in Muthoot NCDs, you can contact me at +919811797407

Dear Mr. Kukreja,

I have an amateurish question. If I am ready to ignore the risk factor involved, wouldn’t it be a good idea to invest in the 36 month period (both monthly or annually don’t look bad to my eyes) or even the 72 month doubling your money option?

Dear Mr. Mayur,

If you are ready to ignore the risk factors and if your taxable income is below Rs. 2 lakhs, then probably it is not a bad idea to invest in these taxable NCDs. But, I won’t invest my own money in these NCDs, even if my taxable income is below Rs. 2 lakhs, due to certain risk factors.

Hi Mayur,

I am planning to purchase Muthoot current issue for 36 months monthly basis interest so just wanted to know from you have you got any interest from monthly NCD in December or January ?

For secured Ncd what might be the risk?

If the issuer defaults and there is not enough value of the assets which have been mortgaged against the loan amount, then it would be troublesome for the investors to get their money back.

Also, NCDs issued under Option XI (double your money option) are Unsecured in nature.

Dear,

regulator does not permit any company to bring NCDs size more then its assets size…..so its partially safe to invest yeah risk is there but need to identify that is companies profile and all.

Hi

Do you have any idea when the next tax free bond could come up for issue from any of the public sector undertakings

Hi Shrini,

None of the issuers has announced the date of its tax free bonds issue, but you’ll get to see at least two issues in the next 10 working days.

Hi Shiv

First of all I need to thank you for the wonderful insight you are providing to your readers on personal finance. Keep up the good work !

I would appreciate your insight on the following

Given the fact that most professional currently running on top IT bracket in related to taxes, what other options are available to them to earn a return of at least 9% after taxes except for Tax free bonds that are fairly safe. The stock markets over the last 5 years have turned out to be a dud !

Given the shake up in the bond funds most of us are left with no option but to chase fixed return instruments such as FD’s which never beats inflation

What would be your options to invest with minimal risk

Would be glad to hear from you !

Thanks a lot Shrini for your kind words !!

First of all, I would repeat this – “Risk and Reward go hand in hand”. The lower the risk, the lower the potential return. Apart from tax-free bonds, I think FMPs provide very good short-term tax-adjusted returns at present. Gilt/Income funds are also good, but then they are risky in nature.

Stock markets or equity mutual funds give excellent long-term returns, but they are the riskiest to invest. Personally, I invest in tax-free bonds, gilt funds & stocks primarily.

Hi

Gilt funds I understand are GOI bond investments? Would like a post on same unless you have already done one.

Also on above wouldnt Fed tapering bring down gold rates and directly impact companies like Muthoot.

Hi Harineem,

Please check these two links:

https://www.onemint.com/2010/12/01/what-are-the-different-types-of-debt-funds-in-india/

https://www.onemint.com/2012/11/06/how-to-choose-a-debt-fund-factors-to-consider-while-investing/

These two posts have some basic info about Gilt funds or debt funds in general. Let me know if you need any specific info about them.

Fed would taper if the US economy improves. Improvement in the US economy would result in stronger dollar & weaker Gold prices. A steep fall in the gold prices in India would result in some major defaults for gold financing companies, including Muthoot, Manappuram etc.

But, weaker rupee & high import duties are keeping gold prices artificially higher here in India. Lower CAD & stronger rupee will make Indian govt. reduce import duties on gold and this would trigger a fall in the gold prices here in India too. This is a big risk.

Hi Shiv and thank for in depth information. Considering the financials and assets of the company Would you still not recommend to invest in these NCD’s (in secured options) even if someone wants to invest less then 5% of their total fixed income investment?

Hi Ikjot,

As I replied to Mayur above – I won’t invest my own money in these NCDs, even if my taxable income is below Rs. 2 lakhs, due to certain risk factors. I would say there are better investment options available other than Muthoot NCDs. Even Muthoot’s own NCDs, issued in previous year(s) would be yielding higher than the current NCDs.

Rest it depends from individual to individual. If you are ready to ignore the risk factors and if your taxable income is below Rs. 2 lakhs, then probably it is not a bad idea to invest in these taxable NCDs.

Thanks for your reply Shiv.

You are welcome!

Hi Shiv,

Thanks for enlightening about pitfalls of certain NCDs.

I had invested in Religare NCD in Sep 2011 at 12.5% for 60 months and also in Muthhot Finance NCD in Dec 2011 at 13.43% for 66m cumulative (doubling in July 2017. At that time Tax free bonds were not that attractive.

I am a senior citizen in 30% tax bracket with lesser risk appetite.

Is it advisable to buy Tax Free Bonds now at around 9% after selling any or both of the above?

Hello Mr. Ramesh,

In my view, tax free bonds are very attractive at this point of time. But, whether you should sell any or both of your holdings and invest those proceeds in tax-free bonds require analysis of these holdings (Religare & Muthoot) and also your personal portfolio analysis. For that, either you can a call yourself or avail our advisory services or contact some other unbiased financial advisor.

Hi Shiv,

Nice post and very on dot response to all questions asked.

regards,

–Kishor

Thanks Kishor !!

hi

What is your view on the preference share launched by L and T. Is the dividend taxable and is it worth investing

Thanks

Hi Shrini,

I’ve not analysed L&T preference shares issue completely. I think it was a PP transaction. Let me check if I can have more info on that.

Hi Shiv,

When can we have your report/analysis on Shri ram city union finance issue opening on 25th November?

Thanks

Hi Ikjot,

I’ve started working on that and hopefully you’ll get it posted by today itself.

Muthoot has decided to preclose its NCD Issue on Monday, Nov 25th, 2013.

Very useful views and analysis on the NCD issues and thanks for the same. Why Muthoot has decided to preclose its NCD issue on 25th Nov. 2013 and also let me have your views on Shriram city union finance NCD issue opening on 25th Nov.2013.

Regards

Vinod

Thanks Vinod for your kind words !!

Muthoot issue is getting preclosed on November 25th, as it has got subscribed to the tune of Rs. 283.46 crore till Friday. It targets to collect Rs. 300 crore in this issue which it expects to easily surpass by Monday.

Here is the link to have all the details about SCUF NCD:

https://www.onemint.com/2013/11/24/shriram-city-union-finance-ncds-issue-november-2013/

Thank you very much loving Shiv Kukreja for giving notifications about Bonds and Debentures. Really I am proud to say that the used language is very simple and subjective to understand and invest. I hope that you will keep the same spirit in guiding me through mails.

Thanks Shivakumar for your kind and motivating words !!

Hi ,

My question is to all who might have purchased this bond. Do any one has got any interest from muthoot since allotment for this Tranche.

Hi,

Even I invested in this issue and yet to receive any interest.

Hi Shiv,

I am new in this bond world so not sure how it works. On one side they(Muthoot) say it is secure bonds and on another side they haven’t given interest for 2 months on monthly payable bonds. What’s the guarantee they would ever pay interest and if they pay interest in future for any month then what about all the months for which they haven’t paid any interest.

Muthoot is selling its NCDs to the general public, whether you want to subscribe to it or not, it is totally up to you as an investor. Caveat Emptor i.e. let the buyer beware, is applicable here also. You need to do your own research about the company before investing.

Most of these NCD issues are not bought by the investors, they are mostly get sold by either the agents or the advertisements. Listing at a discount to its face value and lack of volumes for liquidity purposes are two factors which suggest that these are not NCDs worth investing. Manappuram NCD issue also got oversubscribed, even before the official closing date, despite of the fact the financial condition of the company is worse than Muthoot. Investors get greedy with 1-2% higher interest rates and then later blame the government or the RBI when any of these companies default on payments.

Thanks Shiv for your reply. So that means “secure” word as such does not have any meaning in case of private NCDS.

No, it is very much relevant as long as the financial condition of the issuer doesn’t become very bad/junk. I don’t know why Muthoot is not paying its due monthly interest, but I don’t think its financial condition is that bad.

http://www.bseindia.com/corporates/ann.aspx?scrip=934922&dur=A&expandable=0

the above is the link for all the payment dates of muthoot finance NCD of december 2013 series. They have made all interest payments as of today. The first interest payment was on 1st Feb which was for the month of January plus the days between allotment date (04/12/2013) till 31/12/2013. Additionally, there is also interest on successful allotment of NCDs from date of subscription by the investor (actually date of funds clearing) to the date of allotment.

Hi Shiv,

Sorry if my question is silly but i am new in this bond world. On one side they(Muthoot) say that these are secure bonds and on another side they don’t pay interest amount for last two months on monthly payable bonds. Whats the guarantee that they would ever pay interest in any month, if they pay in any month what about interest for all the previous months of which they haven’t paid.

i am a retail investor and i have recently bought monthly 3 year option of december 2013 series (BSE Code: 934922, BSE Id: 1125MFL16B). As you must be aware that the coupon rate is 11.25% for institutional investors but there is 0.75% incentive for retail investors. Suppose, the seller of these NCDs was an institutional investor who had subscribed these NCDs through public issue then what coupon rate will i get for these NCDs (i.e. 11.25% or 12%)? Thank you.

I want to invest in muthoot finance for monthly interest plan please send details

I want to INVEST in muthoot finance for monthly interest planand dp and 72 month scheme please send details

I want to invest in muthoot finance for monthly interest plan please send details

kindly inform me about the NRE fixed deposit interest details transferable to SB account on monthly basis.

Dear sir, MAIN OMAN MEIN KAAM KARTA HOON OUR MAIN BELGAUM KARNATAKA MEIN RAHTA HOON OUR MAIN AAP KE BRANCH BELGAUM MEIN ( MUTHOOT GOLD LOAN)MEIN 500000/- LAK.RS. F.D. KARNA CHAHTA HOON PLE. SIR AAP IS KA JAWAB JALD DE.

dear sir,

I would like to invest in your FD which is doubling in 6 years.

do you have any scheme which is of recurring nature?

please send the details.

Is there any scheme for NRE

rEGARDS

SANAL

Hi

I am an NRI.

i would like to know if i put some amount as FD in muthoot.

What rate will i get?

Will it be monthly or annually??

What will be more preferable mothly or annually???

Please give me a good advice.