Muthoot Finance NCDs Issue – September 2013

This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

Muthoot Finance has also launched its issue of non-convertible debentures (NCDs) from September 2nd, with its plan to raise Rs. 300 crore, including the green-shoe option of Rs. 150 crore. The issue will remain open for two weeks and will get closed on September 16th. However, if required, the company may extend the closing date of the issue, depending on the response for the issue.

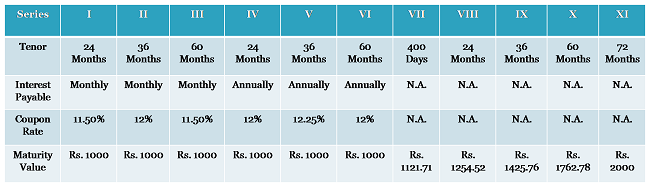

The company offers to double your money in 72 months (or 6 years) with an effective yield of 12.25% per annum. This is just one of the eleven options that the company is offering to the investors, with different maturities and different interest payments.

Interest rates have been left equal for all the categories of investors and there is no differentiation among institutional, non-institutional, HNIs and the retail investors categories. The bonds will be issued for a tenor of 400 days, 24 months, 36 months, 60 months and 72 months, with monthly interest, annual interest and cumulative interest options.

I don’t know why the company is giving so many options and making it too complicated for the investors to take a decision, but it does not give me any confidence to know that the bonds, which are offering to double the money in 72 months, are actually ‘unsecured’ in nature.

Categories of Investors & Basis of Allotment – The investors have been classified in the following three categories and as always, each category will have certain percentage fixed for the allotment:

Category I – Institutional Investors – 15% of the issue is reserved

Category II – Non-Institutional Investors, corporates & HNIs – 35% of the issue is reserved

Category III – Retail Individual Investors including HUFs – 50% of the issue is reserved

NCDs will be allotted on a “first-come-first-served” basis.

Ratings & Nature of NCDs – There are two rating agencies involved in this issue – CRISIL and ICRA and both have assigned ‘AA-/Negative’ rating to this issue. Except the XIth option, all other options are ‘secured’ in nature.

Listing, Demat & TDS – These NCDs are proposed to be listed only on the Bombay Stock Exchange (BSE). Investors have the option to apply these NCDs in physical form as well as demat form for the first six options out of total eleven. NCDs applied under option VII, VIII, IX, X and XI will be allotted compulsorily in the demat form.

Again, the interest earned will be taxable as per the tax slab of the investor and TDS will be applicable if the interest amount exceeds Rs. 5,000. But, NCDs taken in the demat form will not attract any TDS on the interest income.

Minimum Investment – As with SREI Infra NCDs issue, this issue as well requires an investor to put in a minimum investment of Rs. 10,000 i.e. at least 10 bonds of face value Rs. 1,000. I don’t know why these private companies want it to be Rs. 10,000, when PSUs, like REC etc., are keeping their minimum investment requirement at Rs. 5,000.

With the gold prices rising, then falling and then artificially pushed up higher again due to higher import duty and falling value of the Indian currency, I think it is very difficult to analyse the future of gold prices and the growth pattern of the gold finance companies like Muthoot Finance, Manappuram Finance etc.

Though the interest rates are somewhat attractive, I would stay away from such NCD offerings for my personal investments and put my money either in tax-free bonds or tax efficient debt mutual funds including fixed maturity plans (FMPs).

Thanks for information.

What does term ‘secured’ mean here?

I think these NCDs might not be affected by gold prices.

These may not be as safe as fixed deposits but better than stock market (short term, with this volatility) with decent returns IMO.

Hi Harsh,

Secured means in case the company gets into some kind of financial trouble & it is unable to carry its business operations anymore and goes into some kind of bankruptcy or liquidation, then there are certain assets of the company which can be liquidated to get investors’ money back.

There wont be any direct impact on these NCDs, but if gold prices fall sharply and there are loan defaults, then it is somewhat troublesome for companies like Muthoot Finance.

There is nothing as volatile as stock markets, so no comparison between equities and NCDs.

Muthoot comes out with NCD’s very frequently. One may wonder is to pay out to investors who invested in past NCD’s. Is there a regulatory authority which checks this?

Won’t be surprised to hear Muthoot defaulted.

Hi Rakesh,

Companies issuing these NCDs need to state the objectives of their fund raising and utilization of these funds in the prospectus of their respective issues. I think it is SEBI’s responsibility to regulate these issues and fund utilization. But, I think the investors should go through the prospectus once before investing.

Actually I have invested earlier with muthoot finance and have got 12% interest. Not NCDs but gold bonds, similar to FD. I am happy to say that they have paid me back every single time, in time. Now they only accept deposits over 25 Lac. So I can’t invest.

Hence, thinking on NCDs.

I think at present there are better opportunities available than these Muthoot NCDs.

can you plz name them?

I think tax-free bonds, FMPs, other debt funds, already listed NCDs etc. are all better than this issue.

Whats wrong with that? Even your neighbourhood bank does that when they issue home loans for 15-20 years and have deposits for 3-5 years which are revolved. Businesses and banks are going entities. There’s nothing wrong in revolving your debt. Don’t treat them like ponzi pyramid schemes where new money is used to pay off old investors. And FYI, Muthoot & Manappuram have been in their businesses for more than 40-50 years. Only the general public outside Kerala have started hearing of them recently. They give short term secured loans which are actually less risky than banks which give long term unsecured loans to the KFAs & Deccan Chronicles of the world. Heard of the NPAs at PSU banks recently?? u will be shocked!!

HOW MUCH TIME DO YOU NEED TO PUBLISH COMMENTS?????

Hi Shiv,

Thanks for elaborate view. Wanted to check how can I invest in bonds in the secondary market. I checked with my broker and he was clueless. In fact all of them are pushing these primary issues. I want to put say 50k in already trading NCD. How do I go about that as a retail investor? Also, is it possible to trade in them as we do in equity. I guess there isn’t any liquidity in the segment.

Hi Ravi,

Yes, liquidity is a problem in those NCDs/bonds in which the institutional interest is low. Sometimes no trading happens in a bond or an NCD for a few days or months. So, it is a difficult job to find these NCDs with good volumes & high yield.

You just cannot expect good service & knowledgeable advice from a sales-oriented industry. This industry is struggling to survive.

You can trade/invest in these NCDs only through your broker or through your online trading A/c. You’ll have to do a lot of google search to find a suitable NCD as per your requirements. Here is one such link to find NSE-listed NCDs/bonds – http://www.nseindia.com/live_market/dynaContent/live_watch/equities_stock_watch.htm?cat=SEC

Hi,

Where do I find info about future up coming Fixed Maturity Plan or Secured bonds / debentures to be offered by corporate where NRI are eligible to invest? I would like to know about such products in ‘pipeline’ which would offer double digit rate of interest.

Reserve bank circular does permit NRI to invest in FMP or corporate bond, then why some company (like info India ltd) does not allow NRI from USA AND CANADA to invest in their bonds?

Your reply to my email address at [email protected] is highly solicited and would be much appreciated.

Hi Prakash,

You can check this link to get info about currently running or upcoming FMPs:

http://www.valueresearchonline.com/funds/fmpnfo.asp

For Secured NCDs or Bonds, you can subscribe to our Newsletter and you’ll keep getting information about the latest or upcoming issues:

http://feedburner.google.com/fb/a/mailverify?uri=onemint%2Ffeed

There are certain laws in the US or Canada which prohibit companies, which have their base in these countries, to solicit business sitting here in India. Probably that is the reason why certain companies do not offer their bonds to NRIs. But, the current NCD issue of IIFL did allow NRIs to invest in its NCDs.

Muthoot NCDs to get listed on the BSE on September 30th i.e. Monday.

Source – http://www.bseindia.com/markets/MarketInfo/DispNewNoticesCirculars.aspx?page=20130927-9