Inflation Indexed National Saving Securities – Cumulative (IINSS-C) – December 2013

This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

India has been struggling with a quite high level of inflation, both at the wholesale level and even higher at the consumer level. While wholesale price inflation is hovering at around 7.52%, high vegetable prices have pushed the consumer price inflation to 11.24%.

With 11.24% retail inflation and 9% (or below) taxable return on deposits, we are earning a negative return and the purchasing power of every rupee we are earning and saving is actually getting eroded.

To enable us earn slightly more than the retail inflation, the Reserve Bank of India (RBI) will issue Inflation Indexed National Saving Securities (IINSS) from today i.e. 23rd of December.

The issue is scheduled to remain open only for seven working days i.e. till December 31st, but the government reserves the right to preclose the issue even before this scheduled closing date. Moreover, the government has not announced the quantum of money it wants to raise from this issue.

What are these bonds and who is going to issue them – the RBI or the Government?

It has been raining bonds for the past four months but this bond issue is different from the earlier issues in many of its features. These are the bonds which would be linked to the consumer price index (CPI) inflation and though the bonds will be issued by the RBI, it would be the liability of the government of India to pay you the interest payments as well as the principal investment at the time of maturity. That ways you can call these bonds a risk-free investment.

Rate of Interest – These bonds will carry interest rate which is not fixed in advance and would be inflation-linked, as the name suggests. In practical words, these bonds will earn half-yearly interest rate which would be calculated by adding 0.75% to the semi-annual CPI inflation.

e.g. if the CPI inflation is 150 today and it is 157.5 six months later, then the investors will earn 5.75% semi-annual return (5% semi-annual inflation + 0.75% fixed rate) and Rs. 1,00,000 invested today would stand at Rs. 1,05,750 at the end of six months.

CPI inflation, which is to be taken into consideration as the reference inflation, will be used with a lag of three months. e.g. September 2013 CPI inflation will be used as the reference CPI inflation for the month of December 2013, when your investment is getting started and March 2014 CPI inflation will be used as the reference CPI inflation for the month of June 2014, when your first due interest will get accrued and get added to your principal investment amount.

Also, this fixed rate of 1.5% would also act as a floor in case the CPI inflation turns negative anytime during its tenure of 10 years.

Interest Payment – These bonds have been named as “Inflation Indexed National Saving Securities – Cumulative, 2013” and here ‘Cumulative’ itself makes it clear that no intermediate interest payments will be made to its investors. There is no such provision to get monthly, quarterly, semi-annual or even annual interest payments with these bonds.

Interest will get compounded semi-annually and will be paid only at the time of maturity along with your principal investment amount. Investors, who want to earn a regular income from their investments, would stand disappointed with these bonds.

Taxability & TDS – These bonds are inflation-linked, but not tax-free. The government is not going to leave its share of taxes and not just only 1.5% fixed interest, the whole interest earned on these bonds would be taxable as per the tax slab of the investors.

But, whether it would be taxable annually or at the time of maturity, it is still not clear to me at present. I think it should be taxed annually, in a similar way the Post Office National Saving Certificates (NSCs) get taxed.

Still one thing is clear, that there won’t be any TDS on the interest payable. Though personally I am not in favour of TDS not getting deducted on any taxable income, as it gives a chance to the tax evaders to get away with it, I think it is a good thing for the investors.

Who is eligible to invest? – Indian retail investors, including individuals, HUFs and specific charitable institutions and universities are eligible to invest in these bonds. Non-resident Indians (NRIs) are not eligible to invest in these bonds, but an investor can nominate an NRI as his/her nominee.

Investment Process – Investors, willing to invest in these bonds, need to approach SBI or its associate banks, other nationalised banks like PNB, Bank of Baroda, Canara Bank, IDBI Bank etc. or private sector banks – HDFC Bank, ICICI Bank, Axis Bank or Stock Holding Corporation of India.

All the formalities, including form availability, acceptance of investment cash/cheque/demand draft/e-transfer, Know Your Customer (KYC) verification, registration of the customer on the RBI’s web-based platform (E-Kuber) and generation of the Certificate of Holding, will be done by these banks.

To compensate these banks for their services, the government has decided to pay 1% of the subscription amount they get mobilised.

Minimum & Maximum Investment – These bonds will carry a face value of Rs. 5,000 and an investor will have to subscribe for at least one bond to invest in these bonds. Maximum investment limit has been set at Rs. 5,00,000.

Lock-in period, liquidity & premature redemption – These bonds will carry a lock-in period of one year for the senior citizens aged 65 years or more and three years for all other investors. Also, these bonds are non-transferable and non-tradable on the stock exchanges, so you cannot sell them to any other investor during their tenure of 10 years.

But, you can redeem these bonds back to the RBI after the lock-in period gets over and that too, only on the coupon due date. To redeem these bonds, you’ll have to forego 50% of the last coupon payable as penal charges.

Bonds as Collateral – If you have an urgent but temporary requirement of funds, then you can use these bonds as collateral against loans from banks, financial institutions and other non banking financial companies (NBFCs).

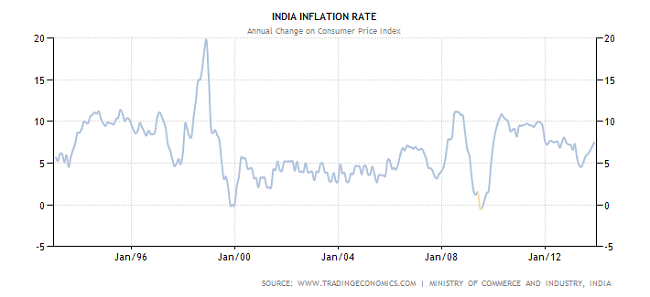

Historical Chart of CPI Inflation

Just check the chart above. It is the 20-year chart of India’s historical inflation based on the consumer price index (CPI). For a good period of time in the last 15 years i.e. from July 1999 to January 2008, the retail inflation remained below the 5% mark. Also, whenever it crossed the psychological mark of 10%, the stay was for a very short period of time and it had an equally sharp reversal.

So, how long we will stay above this important level this time around, it would be quite interesting to observe. If the inflation again falls sharply this time also, like it has happened many a times in the past, then the investors would find themselves trapped with this investment.

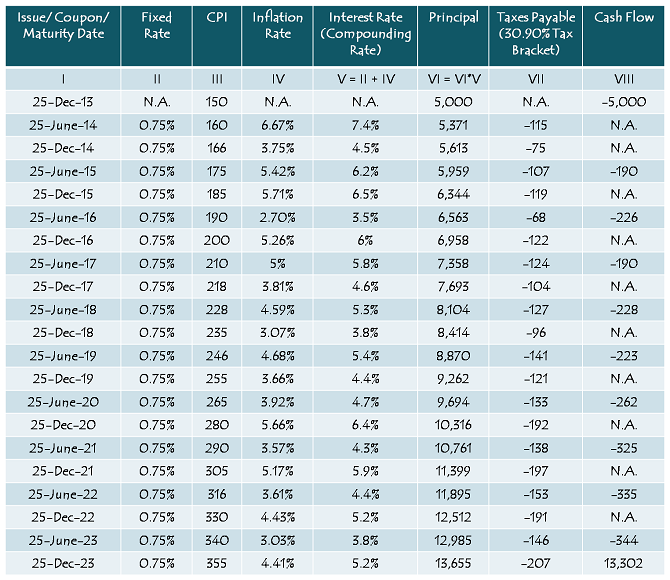

Illustrative Examples of Inflation Indexed National Saving Securities (IINSS)

Example I: After-Tax Cash Flow Analysis with calculation of NPV and IRR

Using the financial calculator for a cash flow analysis of this illustrative example, I got Rs. 5,979 as the Net Present Value (NPV) and 7.2557% as the Internal Rate of Return (IRR).

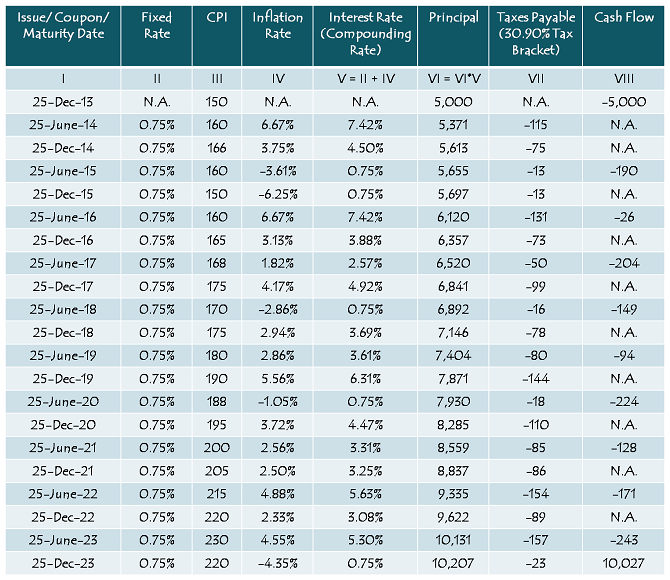

Example II: After-Tax Cash Flow Analysis with calculation of NPV and IRR

Again, with this illustrative example, the Net Present Value (NPV) comes out to be Rs. 3,598 and the Internal Rate of Return (IRR) is 5.0909%.

So, if I compare these two rate of returns with the current coupon rates of tax-free bonds, then it is clearly evident that tax-free bonds seem to be a better investment option. But then these are just illustrative examples and the actual inflation numbers would be quite different from these assumed figures.

Investors, who are not liable to pay any tax on their current income and also on their future income or who fall in the 10% tax bracket and who also think that inflation is not going to come down at least for the next 3-5 years, should definitely subscribe to these bonds.

Due to its unfavourable tax treatment, lock-in period of 3 years, 50% deduction of last year’s due interest in case of premature withdrawal, high uncertainty about inflation and no scope of any capital appreciation, I would personally avoid these bonds and go for the tax-free bonds for my investments.

Also, I could not work on a comparative analysis of these inflation-linked bonds with tax-free bonds in this post, but I would definitely like to do that as soon as possible. I would also like to have some inputs from your side so that all possible points of comparison can be covered and we can reach to a healthy conclusion out of it.

Shiv

As usual an excellent analysis.

I have read somewhere the tax implications will be the same as per any debt mutual fund investment.ie Long term Capital Gains will be taxed on 10% with indexation or 20% without indexation.

However its main draw back is, it does not allow regular interest pay outs.

Also if the Govt is really interested to attract retail investors it should give time say at least one month to enable investors to mobilise the money for investment.

The current schdule is too tight.Announcing on 20-12-2013,opens on 23-12-2013 and closes on 31-12-2013.How many retail investors will have ready cash to invest 1-to 5 Lakhs?

Thanks a lot Mr. Ramamurthy for your kind words !!

There is a lot of confusion w.r.t. the tax treatment of these bonds. I have posted about it as per my best understanding. I would await the finance ministry’s clarification in this regards before recommending my clients to go for it.

You are right, just 7 days time is too short for the issue to attract retail participation.

fab work, as always Shiv…… highlighting the right points , brilliant job…

Thanks a lot Mr. Ashish for your kind words !!

how do we apply for this scheme ? i dont see in HDFC securities.

Hi Pradeep,

It is available with certain banks only as mentioned in the post. I don’t think brokers will be allowed to intermediate in this issue.

Surprised to see that it is available in ICICIDirect (inIPO section). This reduces some paperwork 🙂

That’s great Bhushan, thanks for sharing this info !! I just checked my Kotak Securities and Edelweiss accounts, both don’t offer any such facility.

Good Analysis Shiv. When announced the bond itself , I felt it will not serve the purpose of any investor considering the other options available. 1.5% above CPI. This means considering historic data and also expecting better days ahead, we can expect average 7.5% interest. Once TDS is cut, it is not beneficial for any tax bracket. I also understand that one will have to pay 1% charge to banks while applying for this bond. I read this in RBI circular. The WPI index bonds which is trading at Rs 83 gives 3.5% return. Advantage here is that the bond gives 1.44% interest as coupon for which one will have to pay tax and the remaining will come under capital gain. The WPI bond will give better return for investors that the CPI linked. Over all these bonds are not attractive considering the TF bonds which are available in market. I fully endorse and applaud the analysis of Shiv.

Thank you George for such words !!

Also, though TDS is not applicable with these bonds, but the interest is taxable. So, it is not a great investment option as compared to the tax-free bonds. 1% handling charges are payable to the banks for servicing these bond investments. I am not sure whether it will get deducted from the investors’ investments or the government will compensate these banks from its own kitty. It is the first such issue and I expect the government to issue more such bonds in the coming future.

I think we can get better interest from bank FDs.

Is nomination facility available for these bonds?

Can minor hold these bonds?

Hi Shub,

Yes, the nomination facility is there with these bonds. In fact, it is always there with all the financial investments. Parents or any legal guardian can subscribe to these bonds on behalf of a minor.

Sir, Thanks very much for the reply.

You are welcome Shub!

Dear Sir, I want a guideline of your for Tax saving with high returns.

I am paying Rs.20,000 tax per year but i cant save much more due to i have lots of family expenses………I have no other saving. Only PF fund about 45000 per year…..

So please tell me how much i have to do saving for maximum amount of refund for this year in which only 3 months remaining…

And also tell me good one scheme for regular tax saving scheme in which i will get high returns in short time……..

So give me best tax saving scheme (like LIC,mutual funds,FD which one) with best return and for short period of time.

waiting for your best reply…

Sorry Vimal, but I won’t be able to take such personalized queries here on this forum.

thanks fot your reply

but can u give me ur personal view on my e mail id. [email protected]

thanks.

..

Sorry Vimal, your case warrants proper tax planning and time devotion, which comes under our paid services. If interested, you can contact me on my mail id.

Hi Shiv,

Once again excellent article with lots of details Now it is becoming a norm for me to check your website for update for any new schemes first. And mostly I will follow per your recommendations. It is hard to beat. Thank you for doing this continously.

Regards,

Sundar.

Thanks a lot for these motivating words Mr. Sundar!

Shiv, how do you think RBI/Govt is going to pay such a high interest rate (11.5-12.5% if inflation is 10-11%). RBI borrows from banks at 7.75% (reverse repo rate); Govt borrows at 8.8% for 10y?

Hi Ankur,

If the government is required to pay 11.5-12.5% interest for the full tenure of 10 years, then it will be suicidal for its finances. Even 8.8% borrowing cost is on a higher side for any government. The government is assuming the CPI inflation to fall drastically once things get stabilised somewhat.

I hope the government is thinking in the right direction. But they should also take some proactive steps in this regards, which at least I have not seen them taking for the past many years.

Also, as these bonds are taxable, they are going to get revenue out of taxes also. I think, in the long run, the average borrowing cost of the government will be 6.5-7.5% with these bonds.

Cant an investor pay income tax on the interest on accrued basis every year?

Hello Mr. Ramamurthy,

That is what I think how it should be. I have expressed my views about it in the post also – “But, whether it would be taxable annually or at the time of maturity, it is still not clear to me at present. I think it should be taxed annually, in a similar way the Post Office National Saving Certificates (NSCs) get taxed.”

Hi Shiv

Do these fall in 80C?

Thanks

No

National Housing Bank (NHB) Tax-Free Bonds issue opens on December 30th. Coupon Rates – 8.51% for 10 years, 8.88% for 15 years and 9.01% for 20 years. It is a ‘AAA’ rated issue and closes on January 31, 2014. I am pleasantly surprised with the coupon rates.

Hi Shiv,

I’ve also heard that NHB has priced each bond at Rs 5000 unlike other TFB issues where each bond was priced at 1000. Can you confirm please? Thanks.

That’s correct Ikjot, it has been priced at Rs. 5,000 per bond.

Hi Shiv!

I have applied for IIFCL. Can you tell me is there any way for me to cancel my application?

You had said that since IRFC has filed their prospectus much earlier than NHB, you expect the NHB rates to be much lower. Can you explain why the rates are higher?

Since each bond is 5k, will it have an impact on liquidity after listing?

Is there a reason they have priced each bond at 5k? How does it impact a company if they price their bonds at 1k or 5k?

An unrelated question, in the T+2 rule, are Saturdays included?

Oh & Merry Christmas!!!

Hi Simple, Merry Christmas !!! 🙂

You need to approach your broker or the Registrar of the issue to cancel your IIFCL application. It is possible.

I have no idea why the rates of IRFC bonds are lower because I was expecting these rates to be higher than what they are. When the IRFC rates got announced and as NHB had filed its prospectus much later than IRFC, I was very confident that the NHB rates would be lower. But, lower IRFC rates and higher NHB rates both have surprised me, one negatively and the other positively.

Also, I’ve no idea why NHB has priced its bond at Rs. 5,000 and how does it impact the company. I don’t think it will have any major effect on its liquidity.

Saturdays are not included in the T+2 settlement system.

Hi Shiv! Thanks for the reply. 🙂

I have an unrelated query. In 2012, NHAI had issued its tax free bonds @ 8.20%. At the time of that issue, the retail limit was for 5 lacs and if you bought for more than that, a lower rate of interest would be applicable. Does the rule of 5 lac limit still apply to NHAI and all the other tax free bonds which were issued with that limit?

Disclosure: I do not hold these bonds. I am just asking out of curiosity!!!

Hi Simple,

When NHAI issued tax-free bonds in 2011-12, interest rate of 8.20% was the same for every investor, irrespective of the investor category and the application size and the same rule still applies to those bonds.

Ok. Thanks!

You are welcome!

very cool…………..

Thanks Yatish!

Hi Shiv, can you do review of DWS Inflation Indexed Bond Fund ? It seems to invest in WPI linked bonds rather than CPI linked certificates

http://www.thehindubusinessline.com/money-wise/nfo-dws-inflation-indexed-bond-fund-far-from-making-the-cut/article5590504.ece

Hi Ankur,

Though there is nothing great about this fund to cover, still let me try to do some research about it.

Yes, i think WPI is a very weak measure of inflation. So, this fund may not be useful for investors

WPI indexed bonds are more attractive than CPI linked bond. This is because the difference between CPI and WPI is almost 3 and when CPI reduces they will be close to each other. 3.6% interest on WPI bond will give an average return of 9% and one will have to pay tax only for 1.44% now. At maturity , you may have to pay the tax based on indexation. There is also liquidity for WPI bond and some capital gain is also possible.

At present, I think CPI linked bonds are better return-wise, but don’t know which is going to give better returns going forward. From taxation point of view, WPI indexed bonds are better. So, it is very difficult to make a choice between the two. Already it is very difficult to predict future CPI/WPI inflation.

Mr George; What makes you think i) CPI will reduce and ii) at the same time WPI will not reduce? Essentially, this requires reforms in food distribution to bring down the structural difference.

I am not suggesting that CPI will reduce and WPI will not. The gap between the 2 is very high at present. If you analyse the historical data, you will find a balance some time. When you are buying a 10 year bond and assuming keeping it for 10 years, in the current form WPI indexed bonds will be beneficial for investors who are tax payers. The CPI indexed bond is targeted at small scale investors who are having 10% taxation or no tax. No one can predict exactly how the economy and inflation will span out. But the analysis always based on data and assumptions. At present the WPI indexed bond is assuring 3.72% interest (today’s rate). This suggests an average return of 8-9%.

Interest details and its compounding semi annually need to figured out to investors at periodical interval by RBI Also Taxability and TDS also need to be communicated in black and white to investor immediately after end of financial year i.e. after 31/03/2015 for F.Y. 2013-14. This will enable proper calculation of Taxable Income of the investor. If this is delayed what are options for investors to present their grievance and request for redress the same as far as it relates to interest payments & TDS on these securities and its timely intimation to Investor .

Interest details and its compounding semi annually need to figured out to investors at periodical interval by RBI Also Taxability and TDS also need to be communicated in black and white to investor immediately after end of financial year i.e. after 31/03/2015 for F.Y. 2014-15. This will enable proper calculation of Taxable Income of the investor. If this is delayed what are options for investors to present their grievance and request for redress the same as far as it relates to interest payments & TDS on these securities and its timely intimation to Investor .

Hi

Can you please let me know how can we check the statement of account. I have purchased IINSS-C units but since then never received any information about the interests or the % or inflation rate considered or even a statement of account. I got from Indian Bank but the branch is not aware of how to get the statement. All these banks run camps when the scheme comes however are not fully aware of the details of how to administer it.

Regards

Sanchita

Sir my dad has also invested in this inflation indexed national saving securities -c.as my father expired on 3rd of January I found that print generated by e kuber about that investment.i want to know that how to get that maturity amount and from where as the agency bank of that investment is state Bank of India but they are telling they don’t know above this.plz help me in this.