This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

As National Housing Bank (NHB) tax-free bonds issue is about to get launched from Monday, Indian Railways Finance Corporation (IRFC) would also be coming out with its issue from January 6. Like many of the investors, I am also disappointed with the coupon rates IRFC has announced to offer and also with its decision not to offer the 20-year option.

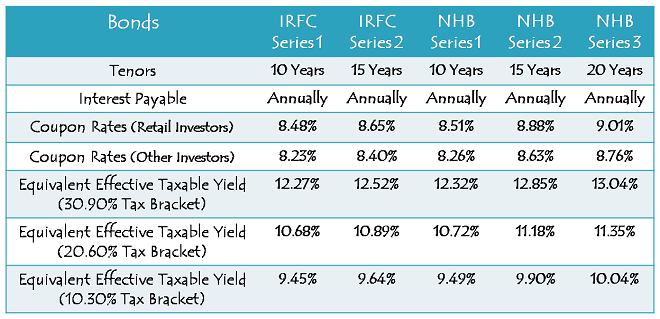

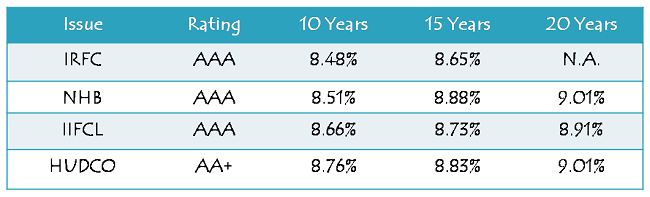

If any of you doesn’t know already, IRFC has decided to offer 8.48% per annum for the 10-year option and 8.65% per annum for the 15-year option. These rates are lower than the rates NHB issue will carry i.e. 8.51% p.a. for 10 years and 8.88% p.a. for 15 years. As both these issues are ‘AAA’ rated and both companies are government organisations, I think people would be more enthusiastic about NHB bonds.

Though at one place in the prospectus the closing date has been mentioned as February 20, 2014, it has been stated as January 20, 2014 at all other places. Looking at the illustrative example it gets clear that it is indeed January 20th.

Size of the Issue – IRFC is authorised to issue tax free bonds worth Rs. 10,000 crore this financial year, out of which it has already raised Rs. 1,337 crore through a couple of private placements. With base issue size of Rs. 1,500 crore, IRFC plans to mop up all of the remaining Rs. 8,663 crore with this issue, including the green-shoe option to retain additional Rs. 7,163 crore.

I would call IRFC move to be brave enough to target such a large amount to be raised within a span of just eleven working days, which others have not been able to do even with two tranches of longer durations.

Coupon Rates on Offer – People who were hoping to get even higher interest rates and planning to diversify their portfolio with this issue and the NHB issue, have been left disappointed by the interest rates IRFC has fixed to offer. Coupon rates of IRFC have been 0.23% lower with the 15-year option and 0.03% lower for the 10-year option as compared to the NHB issue. As always, the non-retail investors will get 0.25% less rate of interest every year.

As compared to IIFCL as well, which is currently offering 8.66% p.a. for the 10-year option and 8.73% p.a. for the 15-year option, the rates are lower. So, the investors can still subscribe to the IIFCL issue if they haven’t already, as it is still undersubscribed in the retail investors category.

Rating of the Issue – IRFC is the financing arm of the Indian Railways with zero non-performing assets. It earns assured net interest margins (NIMs) from the Ministry of Railways (MoR) and other related entities like Rail Vikas Nigam Limited (RVNL) and RailTel.

Most importantly, in case of any default or shortfall in the money required to redeem these bonds, the MoR will be required to fund the payments due to the bondholders. So, there is minimal risk involved with these bonds and probably that is the reason all rating agencies, CRISIL, ICRA and CARE, have assigned ‘AAA’ rating to the issue.

NRI/QFI Investment – Non-Resident Indians (NRIs) are eligible to invest in this issue, on a repatriation basis as well as on a non-repatriation basis. Qualified Foreign Investors (QFIs) are also eligible to invest in the issue.

Investor Categories & Allocation Ratio – The investors have been classified in the following four categories and each category will have certain percentage of the issue size reserved during the allocation process:

Category I – Qualified Institutional Bidders (QIBs) – 10% of the issue i.e. Rs. 866.30 crore is reserved

Category II – Non-Institutional Investors (NIIs) – 30% of the issue i.e. Rs. 2,598.90 crore is reserved

Category III – High Net Worth Individuals including HUFs, NRIs & QFIs – 20% of the issue i.e. Rs. 1,732.60 crore is reserved

Category IV – Resident Indian Individuals including HUFs, NRIs & QFIs – 40% of the issue i.e. Rs. 3,465.20 crore is reserved

Listing – The company has decided to get these bonds listed on both the stock exchanges i.e. National Stock Exchange (NSE) as well as the Bombay Stock Exchange (BSE). The bonds will get allotted and listed within 12 working days from the closing date of the issue.

Minimum & Maximum Investment – Unlike NHB, the face value of a bond in this issue has been fixed at Rs. 1,000 and as always, the minimum investment would remain Rs. 5,000 i.e. at least 5 bonds of Rs. 1,000 each. Retail Investors’ investment limit stands at Rs. 10 lakhs, beyond which they will be considered as HNIs and will get a lower rate of interest.

Demat not Mandatory – An investor, as per his/her own choice, can subscribe for these bonds in either of the forms, demat or physical. Though it is mandatory to have a demat account to sell these bonds, you may subscribe to them in certificate form as well and can get them converted to demat form whenever you want.

Interest on Application Money & Refund – IRFC will pay interest to the successful allottees on their application money, from the date of realization of application money up to one day prior to the deemed date of allotment, at the applicable coupon rates. Unsuccessful allottees will get interest @ 5% per annum on their refund money.

Interest Payment Date – IRFC has decided to make its first interest payment on April 15, 2014 and subsequent interest payments will also be made on April 15 every year.

What would make you invest in this IRFC bond issue?

With NHB offering higher rate of interest for all maturity periods from Monday and IIFCL, HUDCO still open for subscription with higher rate of interest, what is that one thing which you think differentiates this IRFC issue from the rest of the issuers? Please share your views about it and let’s see if it makes sense to other investors also.

Application Form of IRFC Tax Free Bonds

NHB Tax-Free Bonds – Bidding Centres

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in IRFC tax-free bonds, you can contact me at +919811797407

Shiv,

Could you pls tell me what’s the record date for annual interest payment in the case of IRFC-Jan 2014 Tax Free Bonds ?

Thanks.

Hi Shiv

I have a question for HUDCO. N 2. Bond issued on. 05 / 03 / 2012. – 8.20 %

If I purchase from the market what will be my coupon interest rate for Trust a/c. (. A O P. ).

It will be same as 8. 20 %. Or. Less.

Please response me.

Thanks

Hi Paresh,

You will get 8.20% p.a. rate of interest if you buy 15-year HUDCO bonds in your trust’s name.

Very surprising that Sonia Gandhi has not opted for the Demat mode.

Sonia Gandhi loses her IRFC bond certificate worth Rs. 10 lakhs:

http://www.business-standard.com/article/elections-2014/sonia-gandhi-loses-tax-free-railway-bonds-worth-rs-10-lakh-114042400537_1.html

When was this issue (opened on 6th Jan 14)of IRFC Tax free bonds actually closed and when will the successful applicants get the bonds?

Hi Setty,

It got closed on February 7th. Investors must have received the allotment advice by now; not sure how many have received the bond certificate.

Thanks for the information Shiv.

You are welcome!

Do you think Tranche 2 has a coupon rate of 8.80 %. Or more because 10 yrs G. Sec was 9.26 % yesterday. G Sec was between 9.19 %. To. 9.23 % since last few days.

I have already invested in recent IIFCL. 8.80 % bond.

Now I would like to invest more , so should I invest in IREDA. Or. IRFC if they give minimum 8.80 % coupon rate.

I have invested some amount in IRFC at the coupon rate 8.65 % last issue.

NHB has got approval for raising another 1000 crores in this fiscal.

Has anyone got refund from IRFC?

Is tranche-II confirmed for Feb 24 ?

Not yet.

IRFC tax-free bonds have got listed on the BSE & NSE today i.e. February 21.

Here are the BSE & NSE codes for the same:

8.48% 10-year bonds – BSE Code – 961829, NSE Code – N9

8.65% 15-year bonds – BSE Code – 961830, NSE Code – NA

Deemed date of allotment has been fixed as February 18, 2014. Interest will be paid on April 15th every year.

Has IRFC allottment started?

Yes…..I received my allotment today

The bonds have been credited to my Demat yesterday night.

Is IRFC tranche 2 likely in 2013-14? since they have collected less than half of the total issue size from tranche 1.

In a Business Line article, IRFC has stated that they will come up with an issue before 31st March. So, it looks like there will be another tranche coming up. They might collect more funds if the coupon rate is better than the previous issue.

Yes, it is highly likely that IRFC will come up with the tranche II of its tax-free bonds.

Is the basis of allotment finalized yet?

Everyone should get full allotment since none of the categories are oversubscribed

That’s right, everyone will get full allotment.

Hi SB,

The issue got closed only on Friday and it will take some more time for the allotment to get finalized.