List of 10 Safe Investments in India

Over the past few days I’ve received a few comments whose central theme is safety of returns while providing moderate returns.

I think the bad performance of the stock market over the past few years has made people search for instruments where return of capital is more important than return on capital, and these questions are a result of that mindset.

In this post I’ll be listing out 10 instruments that I think are quite safe for investing along with their tenure, expected return, tax applicability and other notes. If you think something else should be on this list, please leave a comment.

| S.No. | Investment | Tenure | Expected Return | Tax Applicability | Comments |

| 1 | Bank Fixed Deposits | Few days to several years | Usually over 8% | Taxable at the investor’s slab | Bank failures are rare in India so bank fixed deposits are a very safe way to invest your money.You know the rates up front so there is no uncertainty there.Taxes can eat into your returns though, especially if you are in the high tax bracket, but even then a FD that compounds quarterly and is done for a long maturity will yield well.Here is a link to a post which has the list of some of the best bank fixed deposits that are available in India right now. |

| Â 2 | Tax Saver Bank Fixed Deposits | 5 years or more | Â Usually over 8.5% | The amount that you invest in tax saver FD is deductible from your taxable income up to a limit of Rs. 1 lakh under 80C. The interest income itself is taxable. | Like the bank fixed deposit, this is also a very safe and certain investment.The drawback is that money is locked in for at least 5 years, and the positive is that you get some tax benefit to juice up your return.Here is a link to some of the best tax saver fixed deposits available in India right now. |

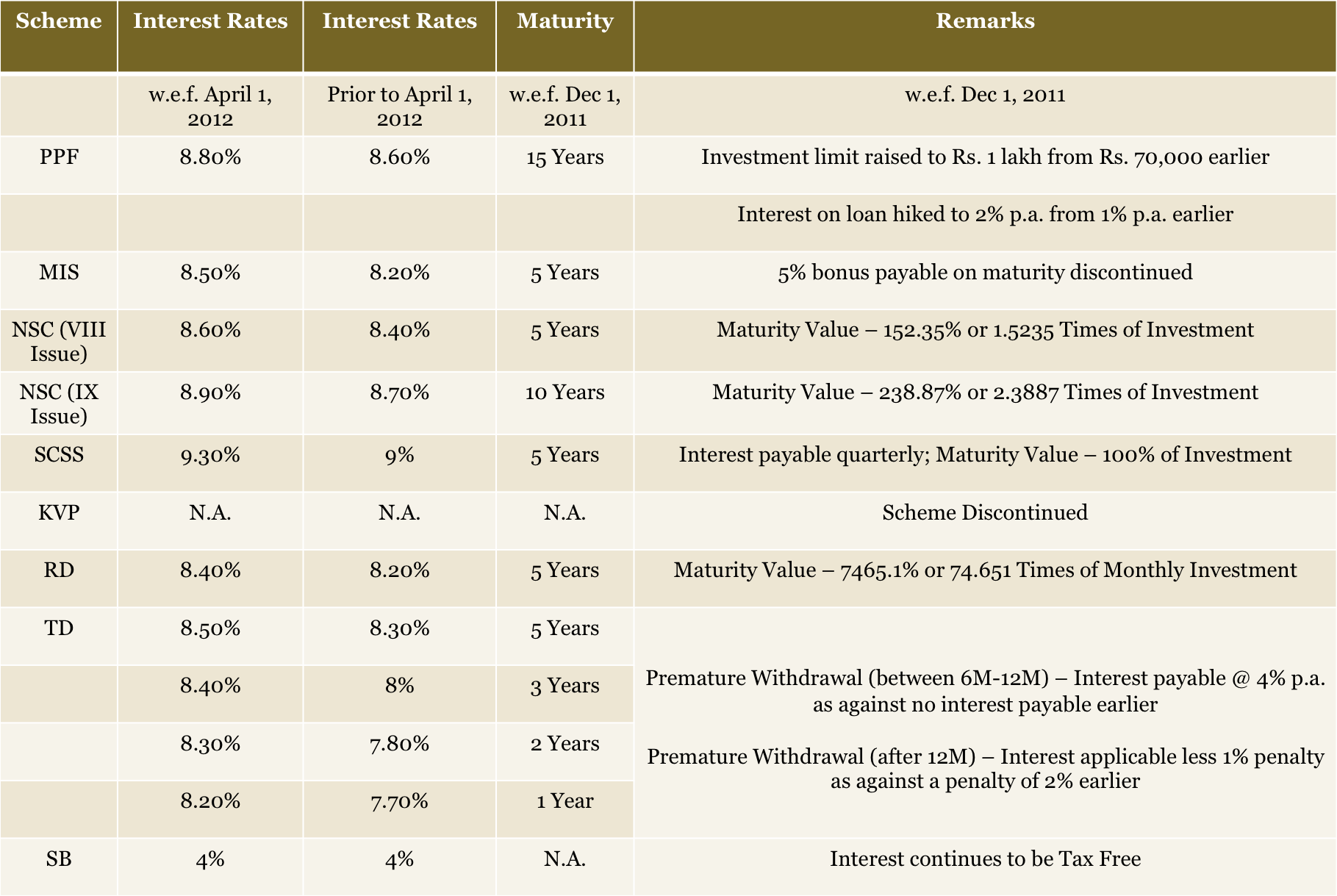

| Â 3 | Public Provident Fund | Â 15 years | 8.8% | The amount you invest is eligible for 80C deductions and the returns are tax free too. | This is also a very safe investment, and the returns are spectacular, specially for someone in the 30% tax bracket.If you don’t mind the 15 year wait period then no other fixed income investment can match the PPF return for the safety it offers. |

| Â 4 | NSC IX Issue | Â 10 years | 8.9% | Interest income is taxable. | This is another safe investment with decent returns.Here is a post with this and other post office scheme details. |

| 5 | Senior Citizens Savings Scheme | Â 5 years | 9.3% | Interest is taxable, investment amount is eligible for 80C deduction. | A lot of readers have commented here over the years about how useful the SCSS is along with the monthly income scheme of the post office for their parents, and relatives and this is a good option as well.Here is a link to an image that has the interest rates for this and comparison with other similar instruments. |

| Â 6 | Monthly Income Scheme | 5 years | 8.5% | Interest income is taxable | This is useful if you are looking for an instrument that gives you a monthly income.Here is link to a post about MIS. |

|  7 | Tax Free Bonds | They trade on the stock exchange so you can buy or sell any time. | Usually upwards of 8% | Income is tax free | I would say that these bonds aren’t as safe as a bank deposit or a post office deposit but they can still be categorized as fairly secure instruments.If you buy these bonds from the stock market right now, they are trading at higher than their face value so your effective yield will be less but then there is always a chance to make capital gains if interest rates come down.Here is a good link on the NSE website that has quotes of all these bonds. |

| Â 8 | Fixed Maturity Plans | 1 year or more | Not fixed but usually comparable to fixed deposits | This is tax efficient when compared with FDs. Read more for details. | Although these are fixed income instruments, there is absolutely no guarantee or indication of what the returns will be like.To that extent, they are very different from the other instruments mentioned in this list.Even then, they are specially attractive to people in the higher tax bracket due to their eventual FD like returns and tax advantage.Read more about FMPs here. |

| 9 | Debt mutual funds | Varying maturities and can be bought and sold anytime. | Not fixed. | Tax on capital gains and dividends. | These are like FMPs in the sense that the returns are not fixed, so they are not meant for you if you can’t handle the uncertainty.Their popularity stems from the fact that they are flexible to buy and sell and have given decent returns in the past. |

| 10 |  Corporate NCDs | Varying maturities |  Higher than fixed deposits. | Interest is charged according to your slab and capital gains are also applicable. | These are higher risk compared with the other instruments mentioned in this list, especially if you invest in a NCD of a company which doesn’t have robust finances.The higher risk means that their return is higher as well and they can be used to juice up your fixed income portfolio but you need to be careful while buying them.This post about 6 things to keep in mind while investing in company NCDs is a good way to get started on this topic. |

| 11 | Savings Account | No Maturity | 4 – 7% | Interest is tax free up to Rs. 10,000 and then charged according to your slab. | A reasonable place to keep your short term funds, but if you have a lot of money in a savings account then you need to consider a FD or some other instrument that can yield higher. |

{kind=link}

All these options are widely known and based on what you want to do and what the rest of your portfolio looks like, you can pick and choose one or more for safety and reasonable returns.

Finally, would you like to add anything to this list?

Update: Added Savings Account per Ankur’s suggestion, please excuse the inaccurate title.

Hi Manshu,

I have a doubt regarding the PPF. Is every installment of our contribution locked in for 15 years ? or it’s just the account is locked for withdrawal for 15 years from date of opening ?

Regards

Hi MangoMan – I think it’s the age of the account and not every installment, but now I don’t feel so certain.

Can anyone else please confirm this?

Hi MangoMan/Manshu,

Its the account that is locked for 15 years not the installment. You ppl are getting confused it with tax saving mutual funds( ELSS) where each installment is locked for 3 years.

Hope this clears your confusion.

Thanks for the clarification Ravi – much appreciated.

The tenure is 15 years and it is not like each installment is locked for 15 years.

Though the tenure is for 15 years, you can make partial withdrawals from 6th year onwards and a loan window is open from 4th year onwards. So, the whole investment does not get locked-in for 15 years.

That’s a great point Shiv – thanks a lot!

A clarification:

Account is for 15 years of the close of the financial year in which you opened the account

So, if you opened it in FY 2006-07 you will be able to withdraw it 15 years later, starting March 31, 2007 (end of this financial year). That means PPF matures on April 1, 2022.

A clarification:

Account is for 15 years of the close of the financial year in which you opened the account

So, if you opened it in FY 2006-07 you will be able to withdraw it 15 years later, starting March 31, 2007 (end of financial year). That means PPF matures on April 1, 2022.

Thanks Manshu,Ravi,Shiv,bemoneyaware,

Actually the doubt came to mind because of the info from summary page of my perfios account for PPF. They are showing maturity date for my PPF account as (1-Apr-2027) which is 15 years from the last deposit (interest credited) into the account on 31-mar-2012.

My account exits since 2006. So, i got little confused on that.

Regards

Thanks for asking the question because only after you asked the question did I realize that this thought had never occurred to me before.

Thanks BMA.

Another query that I had is with regards to the lock-in period once the original 15 years are completed and say you have withdrawn the amount..

Scenario:

– My father opened a PPF account in my name around 1992.

– I started working in 2004 and began contributing to the PPF account to save on tax under 80C

– The PPF account matured in 2007.

– I wanted to buy a property in 2011 and hence withdrew all the amount from the PPF account in CY 2011.

Now the question that I have is:

1) Do I need to open a new PPF account or can I continue with the same PPF account?

2) If I’m allowed to continue with the same PPF amount, start contributing to it on a yearly basis..would a revised lock-in period of 15 years be applicable on it?

After complete 15 financial year, PPf account matures and one can withdraw the maturity amount and close the account. However, if one wish to extend this account it can be done so for a 5 years. indefinite extensions are possible but withdrawal of money has some restictions like after initial 15 years you can’t withdraw closing balance in full and during the extended period of 5 years only one withdrawal is possible

Hats off ! Very good compilation. Addresses the issues of Liquidity, Returns, Risk and Taxation beautifully.

Thanks – it was a bit harder than I expected since I had written about all these instruments earlier. I’m still waiting for someone to point out something that I missed.

Hi Manshu… I think there is a scope to include Company FDs and NPS here but then you’ll have to change the headline of this post. Probably you could have merged company FDs with Corporate NCDs.

Hi Shiv,

Are there any good company fixed deposits that you are aware of? I didn’t think of it originally but after you mentioned it, I tried to think of some examples but couldn’t come up with a single one.

NPS could be there, a bit tricky as you can also invest in equity, insanely long lock in, no clarity on how you get money and how you invest it, oh well, just leave it for the time being. I’ll add if the situation improves.

Hi Manshu,

How about HDFC, Shriram Transport Finance Corp, Gruh Finance, LIC Housing Finance, ICICI Home Finance as examples ?

Regards

But these aren’t open for subscription currently are they?

All of them except Gruh Finance are shown as active on the following FundsIndia page: https://www.fundsindia.com/content/jsp/corporate/DepositLP.do

I haven’t tried them myself though.

From Gruh Finance site, it looks it’s available currently as the rates are mentioned as effective from May 2012.

Regards

Nice article..good job !!!

Are Tax saving bonds like HUDCO or IRFC available in secondary market??

Is it worth to invest in them thru secondary market ??

Tax saving bonds only save tax if they are bought directly from the issuer and not the primary market.

But I’m not sure if you really mean tax saver bond, or tax free bonds?

I think Sameer wants to ask it about Tax-Free Bonds because HUDCO & IRFC dont offer Tax Saving Bonds.

Sorry…i mean tax-free bonds…

Yeah, so those I think they do make sense to buy, specially if you are in the 30% tax bracket. Very good after tax yield there.

which is most profitable in long term?..tax free or tax saving bonds

Hi Manshu .

thankyou for this compilation ,I would like to know your view on Tax free bond and corporate Bond .In the comment section you mentioned that these are not as safe as Bank ,But these are Ratings driven in most cases AAA ,So why would you think that these are not as reliable as Bank ,After all I think bank can also fault .Want to know your views .

Thank

Curious Reader

The reason I say that is because RBI also insures your account to the tune of Rs. 1 lakh and that’s additional protection, plus RBI won’t allow a bank to fail so easily because it affects so many other parts of the economy. If the government can’t let Air India fail, it’s very likely that it will protect banks which are far more important.

Then, not all companies are AAA, many corporate bonds that come out are in far worse shape than AAA companies. There are only a few AAA issues overall.

Lehman Brothers had a ‘A’ rating a month before bankruptcy and Enron didn’t have its rating downgraded till it was too late. Same for Fannie Mae.

While rating agencies have improved but ultimately there are always devious companies who find ways to hide their real status.

Our humble saving account could be the safest and the most liquid investment now after tax exemption in budget. Specially if u get hold of 6-7% returns

Added that – Thanks!

Hi Manshu… I think quoting expected returns of 6-7% on Savings A/cs. would misrepresent the actual picture as all of the banks except 5 low CASA banks – Yes Bank, IndusInd Bank, Kotak Mahindra Bank, Karnataka Bank and Ratnakar Bank, are still offering only 4% returns. So, it would be better to rewrite it as 4-7%.

I had not thought of that Shiv, but it makes total sense. I’ve made the change – thanks for your advice.

Hi Manushu,

Could you pl. confirm this by an example.

If a assesse over 10 lakhs salary income, if he maintains Rs 8 Lakhs in financial year in Kotak bank and earns interest of approximately Rs 47,500/-

(1) Is this interest Tax free, where TDS is not deducted?

(2) While filing Income tax returns, should he mention it , or not?

You are liable to pay tax on this since your income is above the limit.

Interest on Bank SB account up to Rs 10000 is exempt from Tax

I am sorry.You have already mentioned this in your main post.My apology.

Bah, how can you club all debt mutual funds together?! There are govt long/short funds (which are nothing like FMP) and then there are corporates ultra short term, short term, etc. Certainly, govt bonds should be a separate topic when talking about safe investments. And, mutual funds are only the vehicle. The universe of debt mutual funds as a whole would subsume all other debt-like instruments/strategies listed in this table.

Govt Bond funds are not exactly safe investments as due to long duration (10-20 years) they have highest exposure to interest rate risk. Its definitely not for the faint hearted

Good point. But, not all govt bond funds are long duration. There are govt short term funds which should be among the top safe investments. And, longer duration bonds are very good complements to equity in a portfolio, as a diversifier (in which case, one needn’t worry too much about the interest rate risk). Those looking to avoid really long term interest rate risk can look at 3-5 year maturity mutual funds. But, yes, there is a basic amount of familiarity one should ideally have before getting into these. Agree on that.

Just wondering, rise in interest rates would be detrimental to both equities and bonds, as prices for both will fall. How would it be a diversifier?

I guess the argument is that if the economy is in a downturn, equities will suffer, rates will be cut because of which bonds rally. And, vice versa, when the economy comes out of a downturn, equities rebound, rates go higher.

I was also thinking of this chart from the US (S&P 500 vs Long term bond fund TLT): http://www.google.com/finance?chdnp=1&chdd=1&chds=1&chdv=1&chvs=maximized&chdeh=0&chfdeh=0&chdet=1341897815286&chddm=497352&chls=IntervalBasedLine&cmpto=NYSEARCA:TLT&cmptdms=0&q=NYSEARCA:SPY&ntsp=0

The worst performance of the long duration bond funds (in the last 10 years via valueresearchonline) was about 7-10% in 2009 when the equity markets did tremendously well.

I suppose there are lead/lag effects. Too high interest rates will eventually hurt equities too – is that what you were thinking of?

Wow. thats quite an exhaustive & data backed analysis. Thanks. I want to take an Indian context. Rate cuts have not taken full shape as yet, economy is slow (equities are down from highs). Interest rates fall will be an extended process (gradually over 1-1.5 year from now) benefitting bonds, does it mean during this period, equities will also remain down? By that logic, recent run up to 17.5k on sensex is unwarranted?

That’s a fair point DJ. I am making a list of debt mutual funds, and will link to that from this post when done.

If it makes sense at that time to include all of these here, I will do so but at this point I want to treat them as a different category.

Its certainly not exhaustive, but food for thought, hopefully. There is no perfect reverse correlation 🙂 The latest economic cycle in the US may well be different from future economic cycles in India, or for that matter in the US. Long term bonds are the only safe asset during deflation – deflation is a rare threat, so this cycle could be different.

If you believe that rates will continue to fall in the next year, that would mean the economy will remain sluggish or stagnant (or else, RBI will not be cutting rates) – in which case, it is reasonable to expect that Sensex may be range bound or lower.

However, what is reasonable, doesn’t have to happen! I’m sure there are times when both bonds and equities rally, or both go down. They would both go down during extremely high inflation + low growth, in which case other diversifiers like real assets (real estate, gold) and short term debt funds may be useful.

Agreed, the only good thing is that interest rate direction are relatively easier to predict than equity market factors.

By Govt Bond Funds I presume you mean Gilt Mutual Funds. If this is so, an investor at any point of time can exit from the Fund at the prevailing NRV.He need not wait up to the maturity date. Am I correct please?

However if you mean Govt bond Fund mean DIRECT(not thro the MF route) investment by the investor what you say is true because of lack of development of Secondary market for Bonds , entry and exit from bond investments for a a retail small time investor is not possible.Am I correct please? I have always wondered whether a small time investor can buy or sell GOVT Bonds at all?

Do you mean investments in Gilt Mutual Funds or direct Investment.If it is thro Mutual Fund I wonder how it can be considered as not safe. The units can at any time be sold or purchased at the current NAV.

Can you please tell me how a small time retail investor buy or sell Govt. Bonds directly.

Practically secondary Bond market does not exist in India.Perhaps the Govt does not want these types of investors.

LIC have an immediate annuity plan called Jeevan Akshay scheme.Under this scheme you pay an initial amount as premium and get back from LIC a fixed amount(monthly,Quarterly or Annual) for life. There are about 7 options for you to decide.Depending on the option selected the periodical annuity you receive will vary.Do a Google search to know full details.

I want to know, that should i invest in the pension scheme of HDFC Bank or LIC

hey, it’s a great article. i wanted to know that is it fair to invest entire wealth in a single fixed deposit of lets say bank of india who have above 9 % interest. i want a long term safe savings option. for example if i have 30 lacs should i invest all in one fd or anything else?

Banks going down is really rare in India but still if I had to do such a thing, I would split it up in 3 or 4 different banks at least and play it safe.

Thanks Manshu,

I tried surfing websites and read articles to start planning my financial future.I must admit your articles and opinions are clear and brief.Its well compiled and easy to understand.I am a working woman aged 31 with 30k income.no saving ,no liabilities but now i will get hold of myself and be wise in spending and investing.looking forward to your next post.

Thanks Shalini, I’m glad to hear that. You no liabilities so that’s a good thing and age is on your side so that’s a good thing as well. I think a lot of people in that age group have big liabilities and struggle to control debt and high expenses.

I notice that the post you’ve posted your comment is an old one and just wanted to let you know that there is almost one new post every day on the site and you can subscribe through email, Facebook or follow on Twitter, Feed or whatever else suits you.

Thanks!

I

Good one.. Checkout this for best investment options for 2013: http://www.myfamilyinvestment.com/2012/12/best-invesment-options-for-2013.html

Sir, I am 23 year with annaul gross income of 4-5 Lac. I am thinking to buy LIC ” Jivan Anand” policy for 25 year with 20000 INR as premium per year. Main aim behind it is at age of 48, I will have handsome money in my hand and my life will be secure.

Please advise on whether premium is o.k with my income and age?

Sir my age is 28yr &earning 24k p/m , i m invest 5k in [email protected] and3500 in mf reliance smal cap & reliance grwth retail(G)…required ur suggestion should i invest in mf / Rd…any other..

boss if u could update the columns it will be a great help

it is the holy grail capsule form of investment decision ..

thankyou ..

Hi,

Apologies for posting so late, but i came across this link just now. I received 1.5lakh from mutual fund investments and I want to invest it (by dividing the amount into parts) to gain maximum returns. Can you suggest something?

thanks

very nice details. You know i am searching it and got best info from ur article. thanks a lot.

NHB Suvrridhi FD-100% owned by RBI

Int Rate 9.25%(9.85%0 for seniors)

80 C benefits Rs 1 Lakh

5 Years lock in

sir my query is suppose I invest 10,000/- in reliance liquid fund -cash plan-growth for a week how much gross amount I will receive after seven days i.e. 10,000+

After a week you won’t get that much more and I’m not sure what the question here is because there isn’t any investment that can offer you much in just 7 days.

Hi Manshu… I think what Mr. Arvind wants to ask is about the safety of liquid funds. If he invests in a liquid fund, I think he wants to know whether he’ll surely get more than his investment of Rs. 10,000 or if the value could even fall below Rs. 10,000.

If my interpretation of your query is right Mr. Arvind, I want to tell you that generally liquid funds never give negative returns and they have very very rarely given negative returns in the past (only on a very few occasions) and that too, very small negative returns due to some panic situations.

Reliance liquid fund generated 0.16% last week, so, had you invested in it, your investment could have grown to Rs. 10016 in one week.

Trying to explore –

I have a flat worth around 60 L today. I wanted to know should I retain it, as there would not be much appreciation on this now; or else sell the same, and invest the money else where (as a safe investment). I wish to park this money & see it grow for the next 10 yrs.

kindly suggest options..

[email protected]

This is a difficult question and I don’t know if I can answer it for you, real estate has been going good for the past decade or so and will perhaps continue to do well in the near future as well. If you take money out of there you will have to pay taxes and also there aren’t many safe investments that can beat inflation.

It’s secure to invest money in the Bank. But My question is that when there are lots of sources are available to make money online. So this are secure?

No most of the sources available to make money online are scams and you should be very careful with them.

Can you please let me know what are the sources of making money on line?

I want to save some amount from my salary every month and invest it.

Could you please suggest, should I invest in SIP or Recurring Deposite?

Thanks.

Nice figure out investment plans

Hello

I have a question on PPF.

Back ground:

My father-in-law has opened a PPF account for my daughter and my wife as guardian in Post Office in 2006. While opening the PPF account he has mentioned my daughter’s name as D. XXXXX and my wife name as D.XXXX.

Now, I wanted to transfer the PPF to ICICI bank. Both my wife (SB Account) and my daughter (Kids SB account) has savings bank accounts with Full Names, ie., My wife’s name as Surname Lastname and my daughter’s name as Surname Middlename Fullname.

As far as I know while transferring, Post Office will send the cheque to ICICI with the balance amount and because of the name difference, Will there be any problems while transferring?

If it is a problem for transfer, Is there any other way to fix this issue? (like can I change both the names at Post office first then transfer?)

Your answers are greatly appreciated.

Thanks in advance

Srini

Hi sir

Could u please confirm me that my investment in a chandigarh based company rich infra india ltd is safe or not.they are taking money on the name of plot sale in unknown place as fixed deposit and recurring deposit like sahara.and giving gurantee of 16% per annum return.

Regard’s

nice article shiv 🙂

i appreciate the efforts put in by you in spreading the financial knowledge

request you to extend this particular article by suggesting a list of investment options age-wise

Hi Kiran,

This article is contributed by Manshu, so you should thank him instead. 🙂

hi,

I M blessed with a son recently.

I want to deposite 1 lac lumpsum for 15 year

which is the best possible means of good return.

Hi Manas,

Equity is the best long term investment. You should invest this amount in 3-4 well performing diversified equity mutual funds.

Hey!!

Well.. I barely know about investment schemes but the person I want to marry need to earn money, for my parents to agree upon our relationship.

Currently me and my boyfriend are pursuing Bachelor of Engineering from a government college, final year.

We both are average in studies.

He is better at communication skills used in marketing than technical, so he has started a part time job at Arena Animation with just 72000 p.a. from this week.

I belong to an upper middle class family and he belongs to a middle one.

So he needs to buck up his socks for marriage which hopefully occurs after about 4 years or so.

See I know that I am asking an immature question but I liked your compilation and replies.

Please suggest me something by which we can put each penny at the right place from now , so that we can have a safe future. Is putting some part of money in a savings account each month enough? Or there are other better ways?

Thanking you,

Best regards.

Hi Sagarika,

Your savings account will earn 4% for you in a year, so even if you keep the whole of Rs. 6,000 per month in a savings account, you’ll end up adding hardly anything to your money.

Rather you should invest this amount either in a recurring deposit to earn safe 8-9% returns or route the same into stock markets through equity mutual funds to earn higher returns.

I would rather advise you to go for a balanced fund which invests in a mix of equity & debt. If the current Modi government is able to change the fortunes of India’s economic & fiscal condition, then I think you would end up earning some handsome returns on your investments and convince your parents about your relationship and marriage.

Hey,

I have just started my career. I have very less income. I am thinking of investing my money. Which would be more preferable and more profitable- investing in SIP or RD?

If I invest in SIP, is there a possibility of incurring loss in any case?

Please do clarify on this ASAP. It would be very helpful.

Thank you in advance. 🙂

Hi Prameeth,

SIP in equity mutual funds carry potential of generating higher returns as compared to fixed deposits or recurring deposits. So, one should go for equity SIPs in order to earn higher returns.

Also, as their returns depend on equity market returns, risk of loss is also there in the short to medium term. But, in the long term, as the stock markets ultimately move up, you should end up earning handsome returns.

Hi Manshu & Shiv,

First of all thanks to both of you for sharing valuable info on investments and for your guidance.

I need your valuable guidance for below:-

I want to start investing in market and searching for a way to begin with. At this initial stage i can invest Rs. 20k to 25k PM. So please guide me for same.

Thank You,

Makarand

one more thing, those investment options should benefit in Income Tax deduction.

Thank You,

Hi Makarand,

I think Equity Linked Saving Schemes (ELSS) is the best investment to have an exposure to the markets and get income tax deduction at the same time. It is better to start an SIP of Rs. 10K-12K in ELSS and rest you can invest in open-ended equity schemes.

Sir,

I am an employee earning 3 to 3.5lakhs. per annum.I have a daughter of 3years old.I have a saving of Rs 4lakhs.

I want your kind suggestion to secure my child’s future alongwith mine with this amount of limited funds.Awaiting fot your kind response.

Dear Alam, please deposit in FD account….

Does anybody know how many, if any, bond issuing companies have gone bust in last 20 yrs. That would be a reality check if such a thing is really to be expected.

Can u suggest a few leveraged ETFs in India.

Hi Manshu.. Great compilation. You may include Kisan Vikas Patra here.

However, if you are including NCD then you may also include corporate fixed deposits. But these instruments cannot be compared with something like NSC and PPF in terms of safety as they are always prone to default from issuing companies. In last year, we have seen various such cases of default especially coming form Real estate companies.

Hi

Please suggest me a good plan for my Daughter age 4 years . I can invest per year Rs 24000/- my age is 37 years.

I need to 100% risk free plan which is having higher to higher returns,

I want to know about 15 years bond ,what the minimum time period to withdrawal this bond,6time multiple bond .plz send me kind advise I want to withdrawal my money ,I’m in financial problem

My investment is in sahara plz advise m

SIR IAM INTERESTED IN SHARE MARKET. BUT I DO KNOW ANYTHING ABOUT THAT PLS HELP ME.

Dear friend

My name is Mr.George Wilson from England I have investment

plan in your country India please I need a genuine partner

that will partner with me if you are interested.

kindly contact me for more information

Email:[email protected]

Regards

George Wilson

Hi George Wilson

Do you still need a partner if so can give a brief of the investment plan in India

Rgds

viru

dear sir,,

My name is lakhwinder singh ,my father is government employs. He will retired after two year. My question is how my father invest there money after retirement.

Hi there to every one, it’s truly a pleasant for me to go to see this website, it contains helpful Information.

That was a wonderful write-up. I have similar smart investing ideas. Please check the following link https://jagahuntblog.wordpress.com/2016/06/11/3-hotspots-to-invest-in-visakhapatnam/. You would be also glad to view my website http://www.jagahunt.com/site.htm?city=Visakhapatnam.

Useful information

My investment is in sahara plss advise