IIFCL Tax Free Bonds

This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

After REC and PFC, IIFCL will become the third company to launch its tax-free bonds this financial year from December 26th. But, unlike REC and PFC, this will be IIFCL’s first issue of tax-free bonds as the company did not have any such issue last year. The issue will close on January 11th.

The company plans to raise Rs. 1,500 crores from the issue with an option to retain oversubscription up to Rs. 9,215 crores.

Despite of the fact that different companies are issuing these tax-free bonds, still as per the CBDT notification, they are bound to keep all of the terms quite similar to each other. There are few terms which are different.

What’s different or unique in this issue?

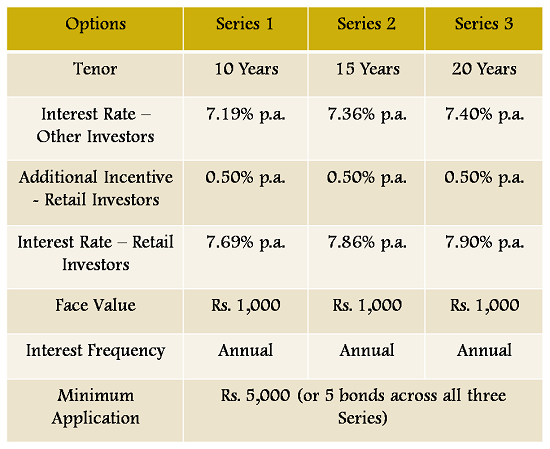

20 Year Option: IIFCL is the only company which has been allowed to issue tax-free bonds with an additional option of 20 years along with 10-year and 15-year options. IIFCL is offering 7.90% per annum for its 20-year option.

NRI Investment: Also, REC and PFC did not allow NRIs to apply for these bonds during their offer period. But, NRIs can participate in the IIFCL issue. They can apply for these bonds both on repatriation basis as well as non-repatriation basis.

Terms of the Issue

Apart from the 7.90% p.a. 20 year option, IIFCL will pay 7.69% and  7.86% per annum for the 10 year and 15 year options respectively. These rates are applicable for the Retail Investors category only and all other investors will get 0.50% p.a. less i.e. 7.40%, 7.19% and 7.36 for QIBs, corporates and HNIs for 20, 10 and 15 years respectively.

Again, the additional incentive of 0.50% will be payable to the original allottees only who invest in these bonds during this offer period. In case these bonds are sold or transferred by the original allottees, except in case of transfer of bonds to legal heir in the event of death of the original allottee, the coupon rates will be revised downwards to the base coupon rates.

The investors have the option to apply for these bonds either in the demat form or physical form and thus, demat account is not mandatory to apply for these bonds.

The issue is secured in nature and has been rated ‘AAA’ by CARE, ICRA and Brickwork Ratings. The bonds will get listed only on the Bombay Stock Exchange (BSE) and that too, within 12 working days post closure of the issue.

The minimum amount of application is Rs 5,000 with face value of Rs 1,000 per bond.

40% of the issue is reserved for the retail investors, another 30% of the issue is reserved for the high net worth individuals (HNIs) i.e. for the individual investors investing above Rs. 10 lakhs. 15% of the issue is reserved for the institutional investors and the remaining 15% is for the corporate investors.

About IIFCL

India Infrastructure Finance Company Limited (IIFCL) is not a well known company among the investors as it is a relatively new company to have come into existence. IIFCL is a wholly-owned company by the Government of India, which got incorporated in early 2006. It has been created with an objective of providing innovative financing solutions to promote and develop world class infrastructure in India.

As per S. K. Goel, the Chairman and Managing Director of IIFCL, this issue might be the last such issue from IIFCL as the Finance Ministry is not too happy with the Government losing huge tax revenue with their tax-free status. If this is the case, then the investors in the highest tax brackets should not wait too long for the other issues to invest in.

Hi,

I want to understand whether in tax free bonds the principal and interest both qualify for deduction under 80 C?

If only interest qualify for 80 C tax deduction, don’t you think tax free saving offered by bank are better option for those in highest tax bracket?

Well a little correction, I mean to say “interest is tax free in tax free bonds instead of interest qualifying for 80 C deduction”

The interest in these bonds is tax free. So there is no tax on interest, neither the principal nor interest is deductible from your taxable income. I’m not sure if you understand this key difference based on your three comments, but if you do then it should be apparent that these two products are not comparable.

Or is your question this: If I’m in the 30% tax bracket and I’ve not exhausted the 80C limit, is it better to invest in a 80C eligible fixed deposit or a tax free bond?

I want to start investing i am totaly new fist time for life place siliguri,west bengal .how much money least needed please assist n how lookin 4wd 4 reply.

Hi Sujit,

Investment amount does not matter whenever a person wants to start investing. You just need to get into the habit of saving and channelising your savings into your investments. There are various investment options available, you just need to decide what kind of investments you want – “high risk-high return” or “low risk-low return”.

Ref: last para

Does it mean that there could not be tax free bonds from IIFCL or any other company after this fiscal?

If so, what is the possibility of this being true?

I already have few tax free bonds in my portfolio but if above is assumed to be true, I would probably go for IIFCL bonds.

Hi Prajju… What will happen after this fiscal will get announced by the Finance Minister in the Budget 2013 on February 28th. But that does not mean there will not be any tax-free bond issues after this issue of IIFCL.

PFC issue closing date has been extended to December 27th, HUDCO issue is opening on January 9th and IRFC issue will also open in January 2013, I think on 21st January. So, till March 2013, I think these issues will keep coming. But if you have to invest, it is better to invest as soon as possible.

Hi Shiv,

Have been reading most of ur blog posts and really appreciate what you are doing.

I invested in the REC bonds through the physical form, as i did not have a DEMAT account in my name.

I was reading somewhere in the comments section, that, it is difficult/impossible to trades bonds in the physical form. So, if 5 years down the line, i have a liquidity crunch, can i redeem these bonds in the physical form, or how do i exactly find a buyer? Or, can these bonds be converted into my demat account, as and when i have one, from the physical form?

I was thinking of investing again, most likely, i will miss the PFC extension date of 27th, however, want to invest in IIFCL, but should i again do it in the physical form, or get a DEMAT account before the last date of the bond issue, which is Jan 11th and invest through that. Would be great if you can throw light on this. Thanks in advance.

Thanks Shishir,

Yes, it is very very difficult to sell all these bonds without a demat account. If you have already taken REC bonds in physical form, you can anytime convert them in demat form by getting a demat a/c. opened.

Getting a demat account opened just for these bonds is not advisable if you want to hold these bonds for 5 years or so. It takes around 20-30 days to get a demat account opened and get physical securities dematerialised, which you can do even after 5 years. But, if you want to use your demat a/c. for other purposes also like equity investment etc., then I would say you should get demat a/c. opened to apply for IIFCL bonds.

Hi Shiv,

Kindly please tell me what is the difference between 10 year, 15 year and 20 year bond. I am 52 year old. Should I take 10 year, 15 year and 20 year IIFCL bond. Please through some light. This is the first time I will be buying tax free bond.

NR Bhatt

Hello Mr. Bhatt,

These are just the maturity periods of these bonds and it depends on an investor for what time period he/she wants to invest. Investors normally require higher interest rate for bonds with longer maturity. In IIFCL’s case, the difference between 15-year and 20-year bonds is very marginal i.e. only 0.04%. I think it makes sense to apply for 15-year bonds.

Hello Shiv

In case we compare NRE FD @9% interest for 10 years or IIFCL bonds @ 7.9% for 20years- which will be more beneficial. Also we cannot see IIFCL bonds in IPO section of ICICI direct for NRIs.-

Hi Rakesh,

I dont know what are the taxation laws of foreign countries as far as NRE FDs and tax-free bonds are concerned, so cant really comment. Otherwise, I think 10-year NRE FDs are better.

Also, I am not sure why IIFCL bonds are not available for NRIs with ICICI Direct. I think there is very little clarity about NRI investments in this issue.

At least in the US you are supposed to declare income from either of these and then be taxed on it so it doesn’t make a difference if the bonds have been designated tax free. I’d imagine other countries also don’t care what the status of these bonds is in India. So, I’d also say that given that thing, FDs are better than tax free bonds.

Thanks Manshu!

A couple of important things I want to share here – liquidity and scope of capital appreciation. I think tax-free bonds provide liquidity in case funds are required in an emergency, whereas I am not sure what are the conditions attached with premature withdrawal of NRE FDs.

Also, 1% fall in interest rates would result in approximately 6-10% appreciation (wild guess) in tax-free bonds. So, the investors are required to consider these factors also.

I think I’ve left myself confused. 🙂

That’s a good point that someone brought up on Twitter earlier when I tweeted this out. I guess there are pros and cons then, but in my mind, I’d still prefer a higher interest rate quarterly compounding FD versus a lower rate bond which may appreciate in the future.

NRE FDs are also allowed to enchased earlier after minimum one year tenure however fd rates will be reduced by one percent and applicable rates will be only for the similar tenure FD. Also another thing against Tax Free bonds you cannot get any Overdraft / Loan however you can avail Loan upto 95% against FD.

Thats not right, you can get overdraft/loan against these bonds. 10 to 20 years is a long time and emergency can strike anytime. Now I’m getting biased towards tax-free bonds.

Thanks for reply. I am asking as far as Gulf NRIs are concerned where there is no tax payable in foregin country as well. I do also feel that 10Yr NRE FDs is a better preposition since it will have cumulative interest whereas in case of Bonds it is not the case so and also the security of NRE FDs with Public Sector Banks. Advantage with the bonds is their 20yr tenure. As far as tax is concerned both are tax free.

QIB portion got subscribed 0.69 times on the first day itself. It shows good demand for IIFCL bonds.

QIB portion has got subscribed 1.44 times on the second day. IIFCL subscription figures are better than PFC and REC so far. This is interesting, great going. Are QIBs diversifying their bond portfolios or IIFCL fundamentals are so good to attract these investors ??

I don’t see how the fundamentals can be so different especially at the level of bonds (not stocks) to attract more attention, it is something else, perhaps the timing or some other factor.

I think the reason is that IIFCL has a clean balance sheet. It has zero NPAs whereas REC and PFC have huge lendings to State Electricity Boards (SEBs) which everybody knows are grossly inefficient.

Shiv = I am not sure if subscription in category one has anything to do for large Category 1 subscription. Various opinions expressed have rightfully said that there is not much to differentiate between various tax free issues. The large subscription is from scheduled banks. I would not be surprised if Government has directed/ pressurised some scheduled banks to subscribe after lackluster performance of REC and PFC, else why should their subscription come on day one. Though the IPO manipulation by corporates was all through implicit, it has been explicit for issues involving Government. Past history stands testimony for this opinion.

Hi Mr. Arun… Probably you are right but I wont buy this logic and I would say this is a negative thinking at this stage (please dont mind). Why would the Govt. do that ?? It is not an issue out of which the govt would get any money. Also, if the govt. wants to pressurise these banks, why only with IIFCL and why not with REC and PFC ?? In IPOs case, it is evident that LIC, SBI etc. are investing due to govt. pressure. But here it is not clearly evident.

Honestly speaking, if I were to invest in any of these three issues, I would have invested in IIFCL issue because of its clean lending.

There can be one more reason. IIFCL has reserved only 15% of this issue for QIBs as against 30% with REC bonds and 25% with PFC.

Govt guarantee, 20-yr period spice up IIFCL bond issue

http://www.moneycontrol.com/news/business/govt-guarantee-20-yr-period-spiceiifcl-bond-issue_799841.html

Q: No bad loans as yet?

A: No. We have a mandate to lend 80 percent to the public-private-partnership (PPP) sector which carries the guarantee of the government and government agencies.

Q: Your loans are guaranteed by the government?

A: Yes.

Probably this is the reason.

I would like to have your comments for the following.

Except Coupon rate difference , what was the difference between last REC TFB and this time. When the allocation showed in Demat, the last one showed 8.13/8.33 suggesting Retail rate as well. This time the allocated bonds showing only lower interest rate (0.5% For retail not shown). I am confused, if the Retail status is based on application for a particular bond REc 10, 15 years or does they look for all the bonds REC, PFC , NHAI etc (Total exceeding 10 Lakhs)

Retail status is based on Rs. 10 lakhs in a single issue. You can invest Rs. 10 lakh each in as many issues as you want and still be considered as a Retail Investor. REC bonds this time carry 7.38% as the Base Coupon Rate and 0.50% additional interest will be paid to the original allottees on the interest payment date as long as these bonds are not sold/transferred.

So, they have just changed the way they display the bond on the trading platform.

Thanks Shiv. Manshu , you are right. The Allotted Bonds labelling shows only the base rate and additional rate for retail investors is not displayed. Shiv is right, there is slight difference last year bonds and this year.

Shiv : What you suggest IIFCL with 7.86% or HUDCO with 8.01 considering the rating and the Balance sheet.

I would rate them equally; probably slightly biased towards IIFCL.

YTM for 8.01% HUDCO in secondary market will be about 7.4% against 7.86% of IIFCL or similar issues to follow. This makes IIFCL preferred one.

How ??

The HUDCO bonds issued in March-2012 are quoting at premium, and therefore give YTM less than 8.01%. The issues in Dec-2012 to Mar-13 bought against IPO will give 7.86% (or less depending upon the market conditions. I can mail you detailed calculations in an EXCEL sheet by email should you so desire.

Arun, No need for any detailed excel sheet. We are talking about the coming issue of HUDCO where they are giving 8.01 % coupon for 15 years bond. March 2012 the YTM is only around 7.65%. May be you have not seen the HUDCO announcement.

my apologies

Tax-free bonds: Are you living in the past?

http://www.thehindubusinessline.com/features/investment-world/personal-finance/taxfree-bonds-are-you-living-in-the-past/article4253148.ece

10-year G-Sec yields closed below 8% today. Taking cues from that and expecting a rate cut by RBI in the last week of Janaury, I think future tax-free bonds should also see a coupon rate cut.

Received REC Bonds certificate. I could not see the date on which interest would be paid.

It is December 1 every year, not sure whether these cos. write the interest payment date on the bond certificate or not. Ideally they should.

Shiv

Only one basic doubt.

Goal: Regular income every year like a passive asset(It is not like the monthly expenses will be covered once the interest from the tax free bonds come,they any how route this amount to any of the investments only). they have a corpus of 5 lakhs.

My father(Retired govt emp(53), 1 st tax slab) and mother(home maker also in the 1 st tax slab) .

I am doing a comparision between the annuity and the Tax free bonds(IIFCL)

Tax free bonds give a standard close to 8 percent tax free returns. But leading annuity provider gives a return upto 7.5 and that too taxable one.

I think for buying a annuity i can buy a tax free bonds. But they are in the 1 st tax slab only.

For annuity i have gone thru this below article and see lot of disadvantages.

http://capitalmind.in/2010/01/low-annuity-returns-in-india/

Is it wise to have a chunk of money in the tax free bonds eventhough they are in the first slab and rather than buying an annuity?

Personally I would avoid both. Your father is retired at 53 ?

Yes. He is retired.

Ok, I thought you had mistkenly quoted it to be 53 instead of 63 or so. Otherwise you could have considered Senior Citizen Savings Scheme from Post Office. You can also consider Gilt/Income Funds as the interest rates are headed lower.

Hi Shiv,

The issue closes tomorrow. I’m planning to buy this today. Since the issue is on first come first serve basis, is there any way to know the chances of allotment? Or should I instead go for HUDCO bonds? Please let me know your thoughts.

– PP

Hi PP… Retail category in IIFCL is still not fully subscribed, you’ll get full allotment for sure.

Thanks Shiv!

You are welcome PP!

IIFCL issue got closed today with 1.93 times oversubscription. QIB portion and the retail investors category have been oversubscribed 8.53 times and 0.67 times respectively. There was huge response from the Commercial Banks.

Reverse trend is there for the HUDCO tax-free bonds issue, the retail investors/HNIs are investing in huge numbers whereas QIBs are not showing great interest.

Received sms that the bonds have been alloted today. Thanks.

Thanks for sharing it Bhaskar!

Hi Shiv, I’ve received an intimation from IIFCL that the “interest on application money on allotted amount” will be deposited directly in my bank account. So this basically seems like interest on the amount I invested from when the received the money until the allotment date. Is this money taxable for the current FY? Thanks!

Hi PP… Yes, it is taxable and subject to TDS also if applicable.

I wanted to apply in tax free bonds,. I am going to retire in the month of Nov 16. will be greatful for your advice on the subject .will be greatful for your reply on email [email protected] and sending the physical forms to Devki Nandan 31 Laajpat kunj Agra 282002

Regards

Devki Nandan

Hi is there any HUDCO tax free bonds are coming in the near future

Will you reply my question’s answer thru my email too.