This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

To err is human. Sometimes we make mistakes and we suffer. Sometimes others make mistakes and again we suffer. When we suffer due to our own mistakes, it is perfectly acceptable. But why is it so that we always need to suffer even when others commit mistakes or errors? That is where CIBIL Dispute Resolution process comes into the picture to help us.

A few days back, Paul and R Srinivas, two of the readers of OneMint, posted their comments/queries on one of the previous CIBIL posts. While Paul wanted somebody to take proactive steps to create more awareness about CIBIL credit score and Credit Information Report (CIR), he also pointed out something which constitute mistakes that we commit. This is what Paul had to say about it:

The people who have credit are also not aware of a credit score – especially even people working in IT/Post Graduates – they seems so detached from all these. They spend on credit cards, never pay back, switch jobs, cut cards without paying up – and finally end up with the worst credit score.

R Srinivas has been suffering due to mistakes committed by others i.e. the banking staff. Probably the banking staff did not send its report for CIBIL to update Srinivas’ records.

I have taken the CIR Report online and see that I have some settlements which were done 2-3 years back. I have all the letters provided by the Banks. They were around 5 Credit Cards and 1 PL. Due to some issues, I could not pay on time. But I have cleared all of them and have been provided with Settlement letters and in some has been mentioned that it will be updated in CIBIL report in 45-60 days. But it has already past 1 year and nothing has happened. Now if I apply for a loan it is getting rejected.

Could you please guide me how I can get my name cleared in CIBIL. I have been maintaining my bank accounts very well and my 2-wheeler loans as well. I assume that the score need for a Loan is above 750. Is that Correct.

Also can I contact Bank Ombudsman. Will they be able to clear my Name ?

CIBIL cannot be a party to all kinds of disputes. We need to understand that CIBIL is just a repository of credit information of all the customers of CIBIL’s members which include banks, financial institutions, non-banking financial institutions (NBFCs), housing finance companies (HFCs) and credit card companies.

CIBIL is not the owner of customers’ credit information i.e. it just collects this information from all its members and provides all the collected information to the same members whenever they require it. CIBIL cannot correct or make changes to these records on its own except the changes which fall in its purview. CIBIL makes changes to your credit information only when it is confirmed by the respective lending institution(s).

There can be more than one reason for these kind of mistakes/errors and some of them are:

1) Disputes where CIBIL Dispute Resolution process can help:

Data entry errors either by the bank or CIBIL – Rectification of CIR is required: There are human errors in which either some of your personal information is inaccurate or some of your account details are wrong. The fields that can be rectified are – * Name * Date of Birth * Gender * Income Tax ID * Passport Number * Voter’s ID * Telephone Number(s) * Address * State * PIN * Account / Loan Type * Account Status * Ownership Type * Date of Last Payment * Date Opened * Date Closed * Sanctioned Amount / High Credit * Current Balance * Amount Overdue * DPD / Asset Classification

Non-updation of data either by the bank or CIBIL – Updation of CIR is required – Sometimes the staff of a bank or CIBIL just skip to update the data of settlement of a disputed credit facility, probably like how it happened in Srinivas’ case. In these cases, you can raise a dispute with CIBIL to get the data updated.

Updation in your personal identification information – Ensure that you have provided updated and accurate documents to the bank or CIBIL – When there is some updation in your own personal information, you should get it updated in CIBIL’s records as well, submitting your relevant documents.

Ownership mismatch of an account or Duplicate account – Rectification of CIR is required – If you find that some personal details or one or more account(s) on your CIBIL report do not belong to you or one or more account(s) are getting reflected more than once on the report, you can initiate a dispute request. CIBIL will look into the matter and update the information if required.

2) Disputes where CIBIL Dispute Resolution process cannot help:

Non-payment of outstanding amount on your loan or credit card including penalty charges – If you have a dispute with a lender itself regarding the outstanding amount on your loan or any other such matter, to which neither of the party is getting agreed, in that case, CIBIL will not be able to raise your request.

Non-updation of data within 45 days of making a payment – Lenders report information to CIBIL on a monthly basis, which would mean that the latest payment, which the lender is still to report, will not reflect on your CIBIL credit report.

Non-payment of outstanding amount on an “add-on†card – If an add-on card has been issued in your name to make you an authorised user of that card, then you are not liable to make payments against the outstanding amount. The primary card holder is responsible for payments on both the cards, primary as well as add-on credit card. But the fun ends here. If the primary card holder defaults on the payments for the add-on card, this will get reflected as a default on the CIBIL reports of both primary and add-on card holders. CIBIL will not be able to rectify your report, even if it was not your responsibility to pay for it.

Details of a closed account – CIBIL need to maintain all the accounts, delinquent accounts as well as good standing accounts, for a minimum period of 7 years from the date the account was last reported. CIBIL will not remove these details, even if you desire so.

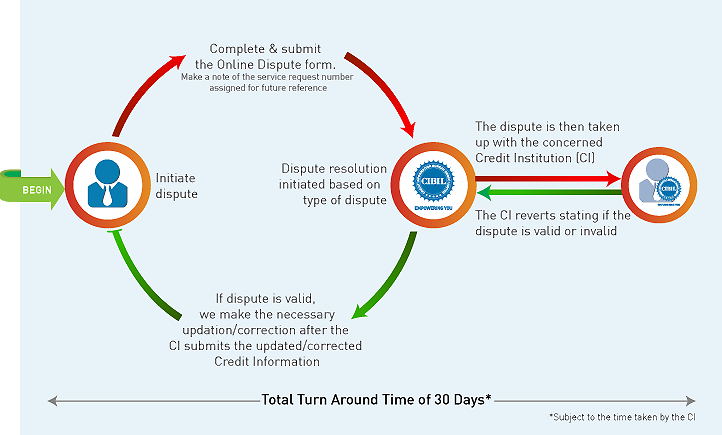

Understanding CIBIL Dispute Resolution Process

It usually takes 30 days for a dispute to be resolved through CIBIL’s online dispute redressal mechanism. The process might test your patience as CIBIL depends on the concerned lending institution for this updation/rectification. Once a dispute request is raised, CIBIL will route your request to the CIBIL Dispute Resolution Department for analysis which will try to resolve the complaint itself, if that is possible without approaching the lender. Most of the times, the mistakes are not from the CIBIL’s end but are from the lender’s end.

If the updation/rectification falls beyond CIBIL’s purview, then it will send the dispute request to the relevant lending institution for resolution in whose purview the matter falls. Once the lender checks its records and responds back to CIBIL, either positively or negatively, CIBIL will then update its records. You will receive an email notification informing you of the results of the dispute request. To get your updated CIBIL report, you will again have to shell out Rs. 470 to purchase it.

How to raise Dispute Request

The easiest way to initiate a dispute request is by submitting a duly completed On-Line Dispute Form. You need to identify the erroneous information and mention a brief description of the error in this form. You will also be required to provide your personal details which must be accurate for CIBIL to initiate the dispute process and communicate the process outcome to you.

A dispute request can be raised based on a CIBIL report having a unique 9 digit “Control Numberâ€. This number is displayed on the top right hand side of every report and it would be a new number whenever a fresh report is generated. This number and the date on which the CIBIL report got generated are mandatory inputs for you to submit your request as it helps CIBIL to identify the report on which you would like to ‘dispute’ information. You can ask the lender to provide you with this control number in case A unique Dispute ID would get generated once you submit the form.

I hope it must be clear to all of us by now how to raise a dispute request when there are mistakes/errors in our CIBIL report. It is the duty of CIBIL to help you resolve your dispute request and most importantly, the process is very simple.

My Cibil record showing two where an all i have only one loan on my name from HDFC kindly requesting youll to update the cibil which will help me to apply for loan ,