Atal Pension Yojana – Government Guaranteed Pension Scheme for the Unorganised Sector

This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY)

Pradhan Mantri Suraksha Bima Yojana (PMSBY)

88% of India’s total labour force of 47.29 crore belongs to the unorganised sector, in which the workers do not have any formal provision of getting a regular pension payment on retirement. Moreover, due to increasing labour wages and better medical facilities, these people also face a risk of increasing longevity. So, this work force would require some kind of assured income guarantee to sustain itself in the coming years.

Launching Atal Pension Yojana (APY) from June 1, 2015

To encourage workers in the unorganised sector to voluntarily save for their retirement, the government of India will be launching a new scheme, called Atal Pension Yojana (APY), from 1st June, 2015. Finance Minister Arun Jaitley announced this scheme in his budget speech on February 28th.

This scheme will replace the UPA government’s Swavalamban Yojana – NPS Lite and will be administered by the Pension Fund Regulatory and Development Authority (PFRDA). The benefits of this scheme in terms of fixed pension will be guaranteed by the government and the government will also make contribution to these accounts on behalf of its subscribers.

Under this scheme, a subscriber would receive a minimum fixed pension of Rs. 1,000 per month and in multiples of Rs. 1,000 per month thereafter, up to a maximum of Rs. 5,000 per month, depending on the subscriber’s contribution, which itself would vary on the age of joining this scheme.

The minimum age of joining this scheme is 18 years and maximum age is 40 years. Pension payment will start at the age of 60 years. Therefore, minimum period of contribution by the subscriber under APY would be 20 years or more.

The Central Government would also co-contribute 50% of the subscriber’s contribution or Rs. 1000 per annum, whichever is lower, to each eligible subscriber account, for a period of 5 years, i.e., from 2015-16 to 2019-20, who join the NPS before 31st December, 2015 and who are not income tax payers. The existing subscribers of Swavalamban Scheme would be automatically migrated to APY, unless they opt out.

Who is eligible for Atal Pension Yojana?

Any Citizen of India, aged between 18 years and 40 years, who has his/her savings bank account opened and also possesses a mobile number, would be eligible to subscribe to this scheme.

Government Funding – Indian Government would provide (i) fixed pension guarantee for the subscribers; (ii) would co-contribute 50% of the subscriber contribution or Rs. 1,000 per annum, whichever is lower, to eligible subscribers; and (iii) would also reimburse the promotional and development activities including incentive to the contribution collection agencies to encourage people to join the APY.

Who is eligible for Government Co-Contribution in Atal Pension Yojana?

Subscribers of this scheme, who are not covered under any other statutory social security scheme and are not income tax payers, would be eligible for the government’s co-contribution of up to Rs. 1,000 per annum.

Social Security Schemes which are not eligible for Government Co-Contribution

- Employees’ Provident Fund (EPF) & Miscellaneous Provision Act, 1952

- The Coal Mines Provident Fund and Miscellaneous Provision Act, 1948

- Assam Tea PlantationProvident Fund and Miscellaneous Provision, 1955

- Seamens’ Provident Fund Act, 1966

- Jammu Kashmir Employees’ Provident Fund & Miscellaneous Provision Act, 1961

- Any other statutory social security scheme

Minimum/Maximum Pension Payable – This scheme will pay a minimum pension of Rs. 1,000 per month and a maximum pension of Rs. 5,000 per month, depending on the subscriber’s own contribution per month.

Minimum/Maximum Period of Contribution – As the minimum age of joining APY is 18 years and maximum age is 40 years, minimum period of contribution by the subscriber under this scheme would be 20 years and maximum period of contribution would be 42 years.

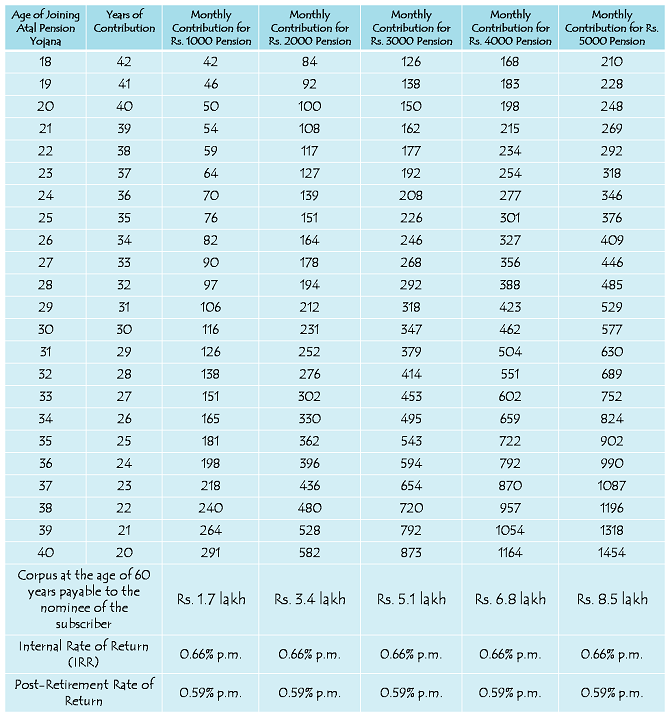

Atal Pension Yojana – Contribution Period, Contribution Levels, Fixed Monthly Pension and Return of Corpus to the Nominees of Subscribers

Internal Rate of Return (IRR) – Thanks to the government funding of Rs. 1,000 per annum per subscriber account for 5 years, your account would generate an IRR of approximately 0.66% per month or 8% per annum. This pension amount per month is fixed and the government has made it clear that if the actual returns on the pension contributions are higher than the assumed returns, such excess return will be credited to the subscribers’ accounts, resulting in enhanced pension payment to the subscribers.

Minimum Contribution – A subscriber aged 18 years will have to contribute a minimum of Rs. 42 per month in order to get Rs. 1,000 pension per month starting 60 years of age. For a 40 years old subscriber, his/her minimum contribution would be Rs. 291 per month. The contribution levels would vary and would be low if subscriber joins early and increase if he joins late.

Maximum Contribution – A subscriber aged 40 years will have to contribute Rs. 1,454 per month in order to get Rs. 5,000 pension per month starting 60 years of age. For a 18 years old subscriber, his/her contribution for Rs. 5,000 monthly pension would be Rs. 210 per month.

Can I increase or decrease my monthly contribution for higher or lower pension amount?

The subscribers can opt to decrease or increase pension amount during the course of accumulation phase, as per the available monthly pension amounts. However, the switching option shall be provided only once in a year during the month of April.

What will happen if sufficient amount is not maintained in the savings bank account for contribution on the due date?

Non-maintenance of required balance in the savings bank account for contribution on the specified date will be considered as default. Banks are required to collect additional amount for delayed payments, such amount will vary from minimum Re. 1 to Rs. 10 per month as shown below:

(i) Re. 1 per month for contribution upto Rs. 100 per month

(ii) Rs. 2 per month for contribution upto Rs. 101 to 500 per month

(iii) Rs. 5 per month for contribution between Rs. 501 to 1,000 per month

(iv) Rs. 10 per month for contribution beyond Rs. 1,001 per month.

Discontinuation of payments of contribution amount shall lead to following:

After 6 months account will be frozen.

After 12 months account will be deactivated.

After 24 months account will be closed.

Subscriber should ensure that the Bank account to be funded enough for auto debit of contribution amount. The fixed amount of interest/penalty will remain as part of the pension corpus of the subscriber.

Post-Retirement Rate of Return – Considering a retirement corpus of Rs. 1.7 lakh and monthly pension of Rs. 1,000, this scheme is going to generate a return of 0.59% per month or 7.1% per annum for its subscribers. I think this return is also on a lower side.

Nomination Facility – This scheme will also provide the nomination facility to its subscribers. In case of the subscriber’s death after attaining 60 years of age, the whole corpus generating the pension income to the subscriber would be returned back to the nominee of the subscriber. In case of untimely death of the subscriber before 60 years of age, the balance would be returned back to the nominee of the subscriber.

Where to open APY Accounts – You need to approach points of presence (PoPs) and aggregators under existing Swavalamban Scheme. These agencies would enrol you through architecture of National Pension System (NPS).

Points of Presence & Aggregators

Application Form – Here you have the links to the application form for subscribing to Atal Pension Yojana – Application Form in English – Application Form in Hindi

I think a subscriber should opt for a minimum monthly contribution of around Rs. 167 or so, which would make it approximately Rs. 2,000 annual contribution. 50% of Rs. 2,000 i.e. Rs. 1,000 would be contributed by the government as well. So, the subscriber will get the maximum benefit of government funding.

As mentioned above, the scheme would start from June 1, 2015. So, interested people will have to wait till then to open an account. If you have any other query regarding this scheme, please share it here.

Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY)

I think earlier launched Swabalamban Yojana is also going to merge with this Atal Pension scheme. This is really good to see that Govt. is really working hard to promoting pension schemes.

Yes, it is mentioned in the article above – “The existing subscribers of Swavalamban Scheme would be automatically migrated to APY, unless they opt out”.

Yes, the intent of the government is clear, execution/efficient implementation holds the key. That is one thing where we need ministers like Mr. Suresh Prabhu or DMRC’s Mr. Sreedharan.

IT will be a great favour for working class of unorganised sector,pl let me know weather can we participate in bringing those people under this scheme and what is the procedure and our role and our remuneration for our services rendered

All these details will be announced by the government in due course, I think around the launch of this scheme.

If a person enters on atal pension yojna in earlier age and afterwards he gets any job and becomes an income tax payer, what will be the fate of this scheme

This is a good question. As of now, I have no idea about it, I’ll let you know as & when I get any info.

I am a student. My father wants me to open an APY A/c. with Sbi. Now the question is if I get a job on completion of education and become a tax payer and enjoying other pensionary benefits shall I be eligible for all the benefits of the scheme. Please let me know

Detel

Pls info to people how can opening the account in Post Office Or Bank… and who was eligeble to this scheme

This scheme will be launched on June 1, 2015. I am not sure whether you are getting confused between this scheme and Sukanya Samriddhi Yojana.

I want know more about this scheme. Can apply my wife this scheme? She is a home maker.

I am not sure about it, but I don’t think a home maker would be eligible for this scheme.

Yes. She can join provided she is not having account in any other government social security schemes like Provident fund etc.,

Today, on 16 March,2015. my age is above 45 yes than I can’ t apply to APY. What is the option for me ?

I think PPF is one of the best option for you. After 15 years, as you complete 60 years, you’ll get tax-free maturity amount.

Only option is, she has to enroll herself right away in Swavalamban scheme before the launch of APY. All swavalamban accounts will get migrated to APY automatically after 1st Jun 15.

paharo par patthar thorane wale mazadooro ke liye free vima hai kaya

My mother age is 45 years. can she open this APY account ?

No, she is not eligible to get benefits under this scheme.

What about if her age is 40 ?

She has to enroll herself right away in Swavalamban scheme before the launch of APY. All swavalamban accounts will get migrated to APY automatically after 1st Jun 15.

weather tds is aplicable in a post office rd account

Till date, no TDS is applicable on a Post Office RD account.

I am not sure about it, but I don’t think a home maker would be eligible for this scheme. & How apply APY?

Atla Pension Yojana would be operational on June 1, 2015. Around that date, you’ll get to know how to apply for this scheme.

yes she can provided she is not a account holder of any government social security schemes like Provident fund etc.,

mala agent hone ahye .tare mala information daywa.kolhapur.

plz told where i open apy account with detail

As mentioned above in the post, the scheme would start from June 1, 2015.

ecs hona chaiye a/c kha par kholna he

Account June 1, 2015 se khulenge.

how open APY account address and detail in indore

You can open the account from June 1, 2015.

Full detail this yojana

Complete details are there in the post above.

How can I join Atal pension yojona

You can open an account from June 1, 2015 by visiting points of presence (PoPs) and aggregators under existing Swavalamban Scheme.

my husband is now 22 years if he contribute 1000 p.m then on which date and what amount we will get?? and on which conditions ??

Your husband cannot contribute more than Rs. 248 approximately in order to get Rs. 5,000 as he retires at the age of 60 years.

Those who are above 40 years of age and want to join APY can join Swavalamban Yojana immediately before the launch of APY. Their accounts will automatically get merged with APY after 1st June 15.

yes she can provided she is not a account holder of any government social security schemes like Provident fund etc.,

ye sab pagal banaya ja raha hai isase to post office mai rd kar do aur rd mature ho jaye to post office mai rd kar do har mahine vyaj wali isase jaldi pension bhi le lo aur vyaj bhi jyada hogi. pension bhi jyada milegi.

Dear Sir ,

Mene NPS me account Khulvaya he. or me har saal 1000 rs. contribution kar raha hu, sir muje kab tak Government Contribution milega, 2017 tak ya 2020 tak??.

or muje andajit kitani Pension Milengi Retirement ke bad?

NPS is not a pre-defined pension scheme. If you are in Swavalamban scheme then you will be migrated to APY and you will have to pay contribution as per new rules applicable to APY and accordingly your pension after 60 will be determined. Govt. contribution for Swavalamban is upto 2017 but we have to wait and see what govt. Stand will be on accounts migrated to APY.

Sir sawalambhan mein Jo plan hai vo bhi change ho jayega kya .kuki ushme pension limit 16000 hai

Swavalamban Yojana ke existing subscribers ko Atal Pension Yojana mein migrate karne ka provision hai, unless wo migrate na hone chahein.

Interesting part of this migration of Swavalamban accounts to APY is how Swavalamban account holders who are above 40 years of age will be accommodated in APY and on what terms is a big question mark ? as they will have less than 20 years of contribution period to retirement age of 60 years.

I am 24 years. I want to enter in this scheme but have a query if i can’t continue till 60 years,what will be?

Account will be frozen unless revived. Every year charges will be deducted from the balance available till it becomes 0. Even then if any amount remains in the account on attaining 60 years then that will be returned or annuitized to provide pension.

Interesting part of this migration of Swavalamban accounts to APY is how Swavalamban account holders who are above 40 years of age will be accommodated in APY and on what terms is a big question mark ? as they will have less than 20 years of contribution period to retirement age of 60 years.

1 . Corpus at the age of 60 year payable to the nominee of the subscriber

Here i have some question

1 . curpus subscriber ke death pe hi milega ya ager wo alive hai 60 pe to milega ya nahi

2 . suppose subscriber death is on 55 corpus nominee to turant milega ya after 5 year

2 . private company me job krne wale iska account open krwa sakte hai ya nahi although unka TDS etc deduct hota hai

Rizwanji, ye scheme unorganised sector mein kaam karne waalon ke liye hai.

1. 21 saal baad jo corpus hoga, usi se hi to pension generate hogi. Corpus subscriber ki death pe uske nominee ko milega.

2. Subscriber ki death pe paisa mil jaayega, nominee ko 5 saal wait nahin karni padegi.

In The Atal Pension Yojana after 60 years getting 1 year pension if I died then what will be? will I get total amount back?

You will not get anything because money/wealth of this physical world after your death may not be valid in eternal world (Heaven or Hell wherever you go). But, your nominee will get the complete 100% annuitized amount.

My question was In The Atal Pension Yojana after attaining 60 years of age getting 1 year or less than 1 year pension if I died then what will be? will my nominee get total amount back?

Yes. Your nominee will get the corpus. You can refer to the table published for APY scheme. As APY is pre-defined pension scheme, while joining APY itself you can decide how much pension you want at 60 years (between Rs.1K to 5K). Depending upon your age at entry, how much pension you want, your contribution amount varies, you have to make pre-defined contribution till 60 years of age. Even the corpus which accumulate in your pension account is pre-determined. So, your nominee will get the pre-defined corpus amount on your death.

Where can I apply for APY scheme? Is it started now?

APY scheme will commence from 1st June 15. You can approach aggregator or POP-SP who are facilitating opening of NPS accounts after 01.06.15 to open APY account.

NPS account is monthly starting 100 rs but APY is .monthly 1000 rs how to possible poor people .

APY mein minimum monthly contribution is Rs. 42 and not Rs. 1,000.

what is difference between NPS and APY ? What monthly contribution for NPS ?

Please in through the scheme details of both NPS and APY, you will come to know the difference.

I am Pondicherry. How i will be agent to APY and NPS. Before launch APY can i get PRAN card?

i have a NPS a/c holder

pls. convert APY.

Hi, I was working in corporate and quit when i was 32 (2008) to pursue spiritual interest… at the time of working i had opened PF account which is still active. Post quitting my income is way below the IT slab. My question is whether i am eligible for AYP?

If you are still a member of EPS (i.e., holding pension scheme certificate under form 10C) of EPFO to avail pension after attainment of 50 years or 58 years then you are not eligible for APY. If not then you are eligible.

Thank you…

& for how many years pension will be paid? that is from age 60 till what age will AYP subscriber get pension?

Under APY scheme, after attainment of 60 years pension will be paid till death of the subscriber. After which, the entire corpus will be paid/returned to the surviving nominee.

Thank you…

Can I change name of nominee after oppening a APY account?

Yes, you can change your nominee after account opening.

sir meri mom ko abi 48 age hai agar mai mom ke swavalamban a/c open karta Hu abi kya vo a/c attal scheme me migration hota hai kya

Kyu ki swavalamban be max age hai 55 our attal scheme mai 40

Yes. It should migrate and merge with APY as per availabe publications on the scheme details of APY. In Swavalamban scheme entry age is between 18 to 60 and not 18 to 55.

Hi Sir, thats a very informative article.thanks for easy explanation. I have a small doubt.. I see APY giving fixed pension but compared to swavalamban, returns are very less. So can we open New swavalamban account after June 1st, 2015??.

No. Swavalamban scheme ceases to exist post 1st Jun ’15.

Sir, in your personal opinion, which scheme gives more benefits to common man (swavalamban or APY??) and also they didn’t mention earlier about removal of swavalamban until budget speech in 2015? wouldn’t they have to give more time to enroll peoples above 40 years and other subscribers in last days ……

Swavalamban is a market dependent scheme. Returns may be higher or lower but not assured. In APY, though the returns are lower, it is assured and pre-defined. Which one to consider better is all dependent on ones perception and risk appetite. With respect to giving more time to 40+ to enroll is a government’s decision which one can’t question and there might be some solid reason or logic behind government decision.

KAB TAK MARKET ME ATAL PENSION YOJANA IYEGI

Ye yojana 1st June, 2015 ko launch hogi.

Where I open APY ?

Any Bank or Post office?

I am enrolled in NPS Lite. Here I have the freedom to deposit lumpsum or at any time as per my convenience. But from the chart of APY, I figure that it can possibly be Monthly deposits /fixed contribution. Also, I am assuming that Swawalambhan is more market oriented than APY. So, my question is that can I still voluntarily choose NPS Lite after APY comes into force, or will it become mandatory to either choose or Leave. I opened NPS Lite in December, 2015, and should be getting Govt. contributiton for three years. Is it possible that the govt. contribution will be also ceased, if I do not change to APY.

I know its too early to ask till we get full Plan of APY, but all the subscribesrs must be having this query.

Also, Can I apply for Online Facility for Swawalambhan Scheme, and do I have the right to change my PFM and my share in E,C, G Pattern as in NPS Regular or am I subjected to Govt. Plans.

I am 30 Years and I want that I continue 50 % in Equity for 10-15 years, or As and when I feel.

It is too early to assess the probabilities of APY unless complete details are spilled out by government. All NPS Lite swavalamban account holders have to wait fingers crossed till government comes out with details on terms and conditions with which it will migrate Swavalamban accounts to APY.NPS Lite module is purely/entirely off-line for subscribers as of now and you can neither login to your PRA to find SOT (statement of transaction) nor make any online contribution to account. You are entirely dependent on your aggregator (NL-CC,NL-AO & NL-OO) and you have to approach your aggregator for each and every information you seek on your account. With respect to PFM and choice of investment, it is all pre-determined by your aggregator while they were becoming aggregators to the NPS Lite module and you will not have any individual option to make choice like in normal NPS account.

SIR,

Today Morning, I had visited my Branch to Deposit for NPS Lite and to get my Statement, but the Bank Manager told that they cannot give the statement.It will be mailed to address by July-August. Or I can ask for a statement through registered mail or phone.

Can you please shed some light on what procedure to follow and how to check whether the amount deposited has been collected and track the performance for the Scheme.

PFRDA has issued a circular in the month of February to all aggregator wherein it has granted NL-CC access to CRA system. All NL-CCs are required to acquire their access to CRA system through their NL-AO or NL-OO. Once they get access, they can login to CRA system and generate SOT (i.e., statement of Transaction) to subscribers upon request. Most probably your aggregator NL-CC office (Branch where you opened your a/c) may not be aware of this. Please take a print-out of the circular either from PFRDA or NSDL website, show it to them and make a demand for the statement. They are obligated to honour your request.

hello sir

this is yasin khan now I have pop branch of nps by abhipra capital dehli

pleaes tell me that all pran card will be murged on APY or not. is it compulsory ?

and which is beneficial to people NPS Or APY ?

Yasin, not all PRAN cards will be merged to APY. Only PRANs pertaining to NPS Lite Swavalamban will be migrated and merged with APY unless subscriber doesn’t opt out. NPS regular (i.e., NPS all citizen module, NPS of govt. employees) will all remain intact without any change or migration or merger. Migration and merger applies only to NPS Lite Swavalamban accounts.

Sir Abi NPS swavlamban chail rahi h.

Ab naye atal ka form bharege kya wo aggregater se hi milega kya .or NPS ka 1000 to bank wale to jama hi nahi karte asi yojna ka fayda sir

NPS swavlamban band ho jayegi kya

I am pran card holder in private sector with swavalamban active position. And my age is 41 year old .if that marged that with APY and how?

SIR , MERY DATE OF BIRTH 01-07-1975 HAI. AUR MUJE AFTER 60 YEAR 15000 RS. KI PENSION CHAHIYE… TOH PLZ BATAYE KI MUJE PER MONTH KITNA INVEST KARNA HOGA.

sir abi jo nps card aa rahe h. ab jo naye card aayege un card par atal pension ka naam aayega ya card hi nahi aayege

I am join new utal pension yojna

Dear sir,

1) APY ke liye bhi PRAN card banana hoga kya?

2) Agar swavalamban yojna ke logoko APY me convert kiya gaya to unko APY ke antargat penssion kam milegi, kyuki swavalamban me 1000/- to 12000/- per year bharneki suvidha thi aur 1000/- anudan per yr 2017 milne wala tha. fir APY me to aisa nahi hoga.

fir ye to sarasar DHOKHA hua logoke ke sath.

kal chalke APY me bhi aap badal karenge aur kuch naya layenge.

Aisa hote raha to Govt. ki Yojna pe bharosa kis buniyad par karenge log?

3) APY me jo paisa bharna hai wo koi bhi bank deposit legi kya, ya uske liye bhi logoko bhatakna padega.

4) Aaj BJP ki sarkar hai isliye UPA ki swavalamban yojna ko APY me convert kiya ja raha hai, Agli bar Sarkar Badal Gayi to kya Firse APY badal ke koi aur penssion yojna banai jayegi kya?

Aisa Kabtak Khilwad kiya jayega logo ke sath.

Kuch To Ek Fix Karke Banao.

Confuse Nahi Confirm Yojna Banao taki logka bharosa tika rahe..

pls let me know how can we become an agent in Post office to sell their accounts as well as Atal pension scheme………..

pls let me know how can we become an agent in L.I.C.I to sell their accounts as well as Atal pension scheme………..

What if I become a tax assesse after joining the APY? Kindly clarify.

Hi Ajitha,

Yours is a tricky query for me and I have no idea about it. I’ll try to figure it out.

sir,

I request to pls new AOY maigratte the older swawlamban pension for NPS joined. all PRAN account attech the all saving bank account.all indias citizen benefits long time,& than not attech saving account big loss govt. & all indians citizen.

regard,

kapil

APY ATEL PENSION YOJNA

Sir I want to know how I become an agent and take agency of apy

provided agency apy

contact : 0120-6999093

Dear all

Request for you all

please do’t give any amount to any agent for become an authorization, affiliation, or agent

you can apply to agreegator or Pop’s to become a agent ou affiliation

it’s has no fee.

Regards

Yasin khan

09179955550

where this scheme can be opened in bank or post office please let me know i want to poened this scheme and and what are its procedure to get this scheme

You can open the account Preferably in Bank after 1st Jun 15. Application for APY is already published in PFRDA website under News & Events section on 10th April. You can download the application by visiting website http://pfrda.org.in, fill and keep it ready for submission on 1st Jun 2015.

Pls let me know whether its possible to withdraw partially whenever the subscriber need as a loan…

No Chiranjib, it is not allowed to withdraw any money before 60 years of age nor any loan is allowed to be taken. Money can only be withdrawn in exceptional circumstances i.e. in the event of the death of the subscriber or any terminal disease.

Sir

As per the Govt.decleration under caption”GOVERNMENT FUNDING IN iii). that will engage agency to promoted the scheme of APY for collecting the customer on incentive basis, I myself like engage for the said job and also interested for getting FRANCHAISEE .So let me know where and to whom I will apply to the govt. Body for the same and also like to know the financial involvement

Thanks

With regards

Amal Biswas

where this scheme can be opened in bank or post office please let me know i want to poened this scheme and and what are its procedure to get this scheme

Hi Abhijit,

You need to approach banks or other service providers which are registered as points of presence and aggregators for this scheme. Here is the list of all those PoPs and aggregators – https://npscra.nsdl.co.in/download/subscriber-corner/entities-in-NPS/POP-POP-SP/POP-SP%20–%20Details%20–%2017.03.2015.zip

atal pesion yojana

information atal pesion yojana

atal pension yojana imformation

singrauli mp

I very happy about Atal Pension Jojana . But age of 18 to 40 age people only eligible.I am intrest to join this yojana but my age is 48 . My request is please consider and help above 40 years people. Thanking you Sir / Madam

Thank you for this pension yojana.

I am a private tutor , can I do APY scheme?

yes u join this apy

Hi Surajit,

If you are not a tax payer and not covered with any of the statutory social security schemes, then you can subscribe to this scheme.

dear shiv my birth date is 5-5-1975 so am I eligible for this scheme

Hi Nitesh,

As you are still 40, you are eligible for this scheme.

and weather the pension amount is tax free or not

Pension amount will not be tax-free and will be taxed as per your tax slab.

Since last 2 year we r involve with NPS lite swavalamban yojna. We processed around 5000 NPS lite ac. Now we r in confuse abt this fatal yojna. Can u tell me the difference between the 2 yojna.

Hi Sujit,

It will try to compare these two schemes in detail with a post.

I need 2 confirmation regarding APY:

1. No matter till what age the subscriber will be alive,he/she will get the pension as per subscribed plan till his/her death.

2. Apart from pension benefit,Entire corpus money will be returned back to the nominee after subscriber death.

Hi Tariq,

1. Yes, that is correct.

2. Yes, that is also correct.

sir,

any person aged 34yrs., getting salary from private concern and also if he is taxpayer, could he be eligible for atal pension yojna. what amount he should invest per month for this scheme to get maximum benefit.

Hi Shrenik,

If you are a tax payer, then you are not eligible for this scheme.

sir, who alredy join in nps tiar I &II . can this person also joined atal pension scheme plz tell me i am confused…..

No Javed, the subscribers of NPS tier I & II are not eligible for this scheme. Only the existing subscribers of Swavalamban Scheme – NPS Lite are eligible to be migrated to this scheme.

I am 46, can I start the atal pension yojana….

No Mr. Anil, you are not eligible for this scheme at 46 years of age.

Yes

Dear sir

Pension statrts from age 60yr for how many yrs

It can be withdran in beween or any loan fascility on it

Kindly clear it

Hi Dr. Thakur,

Pension will be paid to the subscriber till the time he/she is alive, there is no age cap for your pension payments. If the subscriber dies after 60 years of age, then the whole corpus will be paid back to the nominee.

Also, neither you can withdraw any money in between before 60 years of age nor any loan facility is there. Money can only be withdrawn in exceptional circumstances i.e. in the event of the death of the subscriber or any terminal disease.

Sir,in the schem of apy corpus amount will be paid to nominee at the age of 60(subscriber)or at the death of subscriber.

Hi Eswar,

If the subscriber dies after 60 years of age, then the whole corpus will be paid back to the nominee. If the subscriber dies before 60 years of age, then whatever balance gets accumulated in the account along with the interest will be paid back to the nominee.

I want to know about if i will get death after registration then gov will give pension to the nominee?

Hi Mr. Krishna,

It is a pension plan for the subscriber of this scheme and no pension is paid to the nominee. If the subscriber dies after 60 years of age, then the whole corpus will be paid back to the nominee. If the subscriber dies before 60 years of age, then whatever balance gets accumulated in the account along with the interest will be paid back to the nominee.

plz support APY.

PlZ. Joint APY

Hi,

I dont know if I am calculating correctly.

For Example:

An Indian national of age 30 is depositing Rs 577 / month in a Bank RD at 8.75% interest (instead of APY scheme) he will accumulate Rs 7,89,376 interest and Rs 2,07,720 as principle. Totalling to 9,97,096. If he keeps the same amount in Bank FD @ 8.5% interest per annum he can earn Rs 10,037 / month instead of pension guranteed of Rs 5000 / month by the APY scheme. Additionally on the death of that person the nominne can get Rs 9,97,096 from Bank FD instead of Rs 8,50,000 guranteed by the APY.

So is the APY scheme really worth ?

If we consider your example, the following points are to be considered first:

1. There are no financial products in India which offer Recurring Deposit (i.e., RD) for a tenure of 30 days. At max. you can have it for 10 years and not beyond that. Beyond 10 years you may renew RD but may not be at same interest rate.

2. Since it is a long term investment (i.e., 30 years), if interest rate remains constant or increases in the financial market then only return on investment in APY will be less as per your example/illustration. In case, if the opposite happens and interest rates reduces in the financial market due to lesser inflation or deflation, your pension or corpus in APY will not get reduced and remains the same as assured by GOI.

So, there are both positives and negatives in the scheme and it all depends upon individual perceptions on the long term investments.

exactly 7000 a month and that is 2000 more than this scheme but if the pension amount is tax free in atal pension scheme then only I & my wife will apply in this scheme so please suggest me

It may be EET or EEE by the time you attain 60 years. One cannot speculate on that presently. A subscriber has to consider all pros and cons before investing in long term instruments/products like APY.

For 1000 pension plan the total corpus value is 1.7 lakh. If this divided by 1000 the total number of months of pension will be 170 months i.e. almost 14 year. What would happen if person lives for hundred year (pension duration 40 years) will the Govt give the pension till that age.

Yes Tariq, pension will be given till the time the subscriber is alive. After his/her death, the whole corpus (Rs. 1.70 lakh in this case) will be paid back to the nominee. Rs. 1,000 is the pension amount which Rs. 1.70 lakh of corpus would be generating for you.

Thanks shiv for replying . So you mean apart from getting the pension till the time of death, the corpus money is quiet separate and will be given back to the nominee for sure.

Yes, that is correct.

Hello Shiv, you have been sharing great information,thanks for this. People are very much curious to know that if this pension scheme will really have the edge on other scheme like Post office RD,PPF,FD etc in terms of monetary benefit . Can you give some analysis or any link where some one did this analysis. I know that apart from monetary benefit other factor do matter but here i want to focus on monetary benefit.

Thanks Tariq,

I think, from returns point of view, this scheme is not a great scheme. I have done some calculations in the table pasted above. Returns getting generated in this scheme are way below PPF or SSA and I think it would be lower than NPS also.

Pl real informaction atalpansion yojna

thanks shiv and can I open this scheme in any branch of my bank or only at home branch and is there any tds on pension amount

Hi Nitesh,

You need to approach banks or other service providers which are registered as points of presence and aggregators for this scheme. Here is the list of all those PoPs and aggregators – https://npscra.nsdl.co.in/download/subscriber-corner/entities-in-NPS/POP-POP-SP/POP-SP%20–%20Details%20–%2017.03.2015.zip

Hi I am in 40plus not 41 can I join in this plan

Yes Prabira, it seems that you can subscribe to this scheme.

Nomination is eligable, pls confirm

Yes Debjit, nomination facility is available.

Hi! I am mamita mishra working in a private sector. My date of birth is 01-12-1974.can I avail APY from 1st June2015?

Hi Mamita,

If you are not a tax payer and not covered under any of the statutory social security schemes, then you are eligible for this scheme.

Dear Sir,

My DOB is 09.01.1975. Am I eligible for Atal Pension Yojana?

I have paid tax on interest on FD in my name with SBI. Am I disqualified for the scheme.

Please let me know.

Regards

Tapashi

Hi Tapashi,

This scheme is designed for low income group workers working under the unorganised sector. So, tax payers or workers covered under any of the statutory social security schemes are not eligible for this scheme.

Sir,

I am a housewife with 4.50 lacs in FD on monthly interest, on which tax has been deducted. Still I am disqualified? Why? Kindly clarify.

Hi Tapashi,

I am not saying whether you are qualified for this scheme or not. As you mentioned that you paid tax on interest on FD, it makes you a tax payer. You need to further get it clarified with any of the aggregators / points of presence whether you are eligible for this scheme or not.

my wife have a mis of 4.50 lacs in post office and ppf account and a newly opened demat account with no trading or investment so now weather she is eligible for this scheme or not and she no other income she is a house wife and she don’t pay any income tax and what statutory social security scheme means

Hi Nitesh,

I can suggest somebody’s eligibility only based on certain basic terms of this scheme. In order to confirm one’s eligibility, he/she needs to approach the appointed aggregators or points of presence. Here is the list of all those PoPs and aggregators – https://npscra.nsdl.co.in/download/subscriber-corner/entities-in-NPS/POP-POP-SP/POP-SP%20–%20Details%20–%2017.03.2015.zip

This link is not working.

And Thanks for this link.

Please visit this link – https://npscra.nsdl.co.in/pop-sp.php and click on POP-SP Details

i nps govt isuued a PRAN CARD to customer,, Like that in apy,, Customer will get PRAN CARD or not

Hi Sujit,

Nothing has been announced in this matter as yet.

Sir I am a govt employee covered under Hp fund scheme am I eligible for APY

Hi Niyaz,

Any Citizen of India can join APY scheme. The following are the eligibility criteria,

(i) The age of the subscriber should be between 18 – 40 years.

(ii) He / She should have a savings bank account.

(iii) The prospective applicant should furnish his/her mobile number details to the bank during registration.

Government co-contribution is available for 5 years, i.e., from 2015-16 to 2019-20 for the subscribers who join the scheme during the period from 1st June, 2015 to 31st December, 2015 and who are not covered by any Statutory Social Security Schemes and are not income tax payers.

Hi,

I am totally confused in one point. No where it is written that if a person has EPS, s/he won’t be able to join the APY . Only it has been written that if a person in under coverage of any social security scheme like EPFO and EPS and s/he is a tax payer then, s/he won’t be eligible to get the govt contribution. correct me if I am wrong.

Hi Avik, you are right in your assessment. I was wrong when I was under the impression that this scheme is only for the workers in the unorganised sector and it is not for everybody. My assessment was based on the scheme details when it got announced in March.

Shiv, you have been saying in the comments below that persons who are paying income tax cannot join APY. From my reading of APY scheme details on NPS website, my understanding is that government co-contribution of 50% or Rs 1000/- will not be contributed for IT payers, and anyone can participate in APY. Can you confirm this. Thanks,

Sorry John, you are right in your observations. I was under the impression that this scheme is only for the workers in the unorganised sector and it is not for everybody. But, if a person is a tax payer or covered under any other social security scheme, then the government will not contribute its share of up to Rs. 1,000 in that account.

I and my wife are not paying any income tax at present but what if we both become taxpayers after joining this scheme

Not sure how the government is going to track these things.

Sir,

I have already subscribed in NPS Lite Scheme from FY 2014-15.

I am submitting Rs. 5000 p.a. on 1st week of April and plan to do so till possible.

I find APY monthly payment tedious as it is highly possible that there are insufficient funds for some months. Can we ask the Banks to deduct the amount at one go, rather than every month.Would you suggest me to switch to APY or continue with NPS Lite Scheme.

And I shall be grateful if you could let me know the Pros and Cons of both NPS Lite and APY.

Hi Satish,

I have never analysed NPS Lite and don’t know much about that scheme, so won’t be able to advise you about that. Also, I think there is no provision for a one time deduction in APY, but I think monthly contribution amount is too low. I would say one should keep one year’s contribution amount in that account so that there is sufficient balance in it.

Dear Sir/madam

i want to be a agent for this scheme

pls let me know how can we become an agent in Post office to sell their accounts as well as Atal pension scheme………..

NABIN SARMAH

GUWAHATI

9706231283

Hi Nabin, I have no idea about it. You need to contact the PFRDA or their aggregators for the same.

i m a govt. servant and elligible for pension after retirement . is my wife who is housewife elligible for Atal Pension Yojna. seeking for early reply.

Hi Mr. Vinod,

If your wife is 40 years or below, then she is eligible for this scheme.

sir in ur above conversation,i notice that according to u, !!nterest calculated in table of apy Is low ,what u suggest to join the scheme???

Hi Reshma,

I don’t think this is a good scheme from returns point of view. Even with government contributing 50% or Rs. 1,000, whichever is lower, the return this scheme would generate for you is just 0.66% per month. This doesn’t seem lucrative to me.

If we r contributing for 5000 pension amt now but in future if we not able to pay for high ,can we cut to less amt at any time

Yes Reshma, you can decrease or increase your monthly contribution, but only once a year in the month of April.

Hi,

Thank you prime minister for helping the poor people with such a scheme. However the only drawback with this plan is the age limit is only till 40. This should be extended till 45-50. I want to take this plan for my mother however since her age is above 40 i am unable to subscribe. Would be great if you consider people below age group 50 in this plan.

In APY scheme , after the death of the subscriber after suppose 70 years whether the nominee is eligible for pension along with corpus amount . And after the death of nominee what will happen…..

Hi Avijit,

After the demise of the subscriber, the nominee will get back the corpus amount. No pension will be paid to the nominee.

its very confusing shiv my birth date is 5 – 5 – 1975 so am I eligible for this scheme or not some bank staff are saying yes & some are saying no so please clear my doubt

As per the terms of the policy, you are eligible for this scheme as you are still 40. Not sure how they are taking cases like yours.

Sir,

My Wife DOB: 18.01.1975, Whether she is eligible to enroll/ join in Atal Pension Yojana (APY) launching from June 1, 2015. Please give your reply to my email-id. Thanking You.

Hi,

As per the terms of the policy, any citizen of India, aged between 18 and 40 years of age, is eligible to subscribe to this scheme. As your wife is 40 years old, she is eligible for this scheme.

My date of birth 17. 08. 1956

Can I join this scheme?

No Mr. Thomas, you are not eligible for this scheme.

thanks shiv my wife is 36 and she have a mis of 4.50 lacs in post office and ppf account and a demat account is she eligible for government contribution of 50% and what amount I have to pay monthly 990 for a pension of 5000 or 50% less @ 495

my wife is 36 and she have a mis of 4.50 lacs in post office and ppf account and a demat account is she eligible for government contribution of 50 % and what amount I have to pay monthly 990 for a pension of 5000 or 50 % less @ 495

Hi Nitesh,

You’ll have to check it with any of the aggregators regarding your wife’s eligibility. Your wife’s contribution will depend as per the pension amount you people seek at the age of 60 years. The government will contribute either 50% of your annual contribution or Rs. 1,000 per annum, whichever is lower.

and weather any minor saving account details is required and the total amount of 8.50 lacs will be direct credited in their bank account and weather any certificate we will get after joining this scheme

Nominee’s bank details will not be required immediately, it might be required whenever some unfortunate event occurs. A statement of account will be issued to the subscriber for his/her contribution.

Hi kukreja sir

1.Is this scheme started or not because when I asked in sbi bank they said scheme will start from 1st june. Is it right sir?

2. And when subscriber died during contribution period so corpus amount will get to nominee and if subscriber died after 60 year so can nominee will get corpus amount with pension or only pension or only corpus amount.

Hi Atul,

1. Yes, this scheme will start from June 1, 2015.

2. Nominee will get only the corpus amount and no pension will be paid to him/her.

Sir,one should invest in this apy or not ???

It is a personal choice Reshma. To me, it is not a great scheme.

can we opt for a same nomiee for me and for my wife so that he can get total of 17 lacs after us

Yes, that is possible.

I am a central employe under new pension scheme (CPF) and tax payer so I am eligible for atal pension yojna

Yes, you are eligible for this scheme, but you are not eligible for the government contribution.

me and my wife have a joint account where she is first holder and second I so can I give this saving account details in both forms

I have no idea about this Nitesh. You need to check it with the bank.

Hello Shiv,

After 60th year, both are alive (Main holder and spouse), in this case each get pension amount or main holder only. Please clarify.

Hi Balaji,

Only the subscriber will get the pension amount and not the nominee.

and can I give my mobile number in my wife’s pension form

Yes, you can do so.

my wife is 36 and I have opted for 5000 pension on her name now my query is if something happens to my wife after 5 years then can I get 5000 pension without paying 990 every month and after me her nominee will get 8.50 lacs because I have also applied for 5000 pension so in this case weather I am eligible to get total pension of 10000

No, if something happens to your wife, you being the nominee are not entitled to any pension. You’ll get your wife’s principal investment back along with the interest earned on it.

hi i am 29 year old and i am eligible to get pension from EMPLOYEES’ PROVIDENT FUND ORGANISATION. after 60 year can we join APY and get benefit plz confirm.

Hi Zoha,

You can subscribe to APY, but your account will not get the government contribution.

and after my wife in which account the pension amount will be credited because we both have separate account in different banks

Only your wife will be entitled to her pension.

untill which age they will provide this monthly pension, upto 80yrs? 90 yrs? if the person was died, does nominee will get the pension? if so upto at age?

Pension will be paid till the pensioner is alive and after him, the corpus amount will be paid back to his/her nominee. No pension will be paid to the nominee.

Does this has income tax rebate?

Do you have any calculator for calculating with my age?

Yes, the premium will be eligible for a rebate under section 80C. Please check this link, it has contribution table as per different ages – http://www.jansuraksha.gov.in/files/apy/ENGLISH/FAQ.pdf

Sir my age is 38 I am shopkeeper also pay income tex am I eligible for apy

Hi Jatinder,

You can subscribe to APY, but your account will not get the government contribution.

Sir my age is 38 I am shopkeeper also pay income tex .can you tell which pension plan I can take

will be thank you

jatinder

You can subscribe to NPS.

Sir ,government contribution means in this ply

Your query is not clear Reshma.

Hello Sir,

My Age is 34, I am PF holder, Kindly suggest the Atal Pension Yojana is good for me else which pension plan is suitable for me. Please advice.

Hi Balaji,

I think NPS is a better pension plan as compared to APY.

dear shiv my birth date is 5 – 5 – 1975 so i am more than 40 or less than 40 because you have said that more than 40 are not eligible for atal pension scheme so please clear my doubt

Hi Nitesh,

You are just 40 years old and as per the terms of this scheme, you are eligible. How aggregators define 40 years for this scheme, it is still not clear to me. You need to contact the customer care team for confirmation.

I have a joint account where she is first holder and second I so can I give this saving account details in all the 6 forms or I have to open a new account where first name is I and second she because some banks are asking to open a new account with first name if he or she wants to apply all these 3 scheme

I am not sure about it, but I think even the second account holder would be eligible for getting his/her account linked for this scheme.

Dear Shiv Kukreja JI,

I post a comments on 21-04-15 in regards to get the franchise of APY directly from the Government but not from any other sources. But you sir did not give any reply in this regards. You know better , if any chances or opper-tunity declear from any govt. a group of people come in front as a middle man . Like this I contacted with a person nearby my area he demanded three types of rates on three types of agency. Like CITY LEVEL, DISTRICT AND STATE. On enquiry I found some information Mr Yashin Khan of Abhipra Enterprise of MP STATE that not to pay any amount to any body as it is free to get the POP- SP.Now I am in confusion what to do.Awaiting your early reply on the issue. Thanks

With regards

Hi Amal, I have no idea about it. You need to contact the PFRDA or their aggregators for the same.

Sir

where can I open nps a/c . What is the prosisior of a/c opening

nps give me pension hole life?

Hi Jatinder,

Please check this link, it has the list of POP-SP – https://npscra.nsdl.co.in/pop-sp.php

dear shiv ji,

my date of birth is 28.08.1987 so let me clear whether my nomine get total corpus amount after getting of pension for few months and then my death

Hi Pinal,

After your death after 60 years of age, your nominee will get the whole corpus.

I have deduct EPF from my salary. Is i applicable to take Atal Pension yojna for 5000.

Hi Navish,

Any citizen of India can subscribe to APY, but if you are already a subscriber of EPF, your account won’t get the government contribution.

My son’s birth date is 28/8/1997

Can I get benefits of scheme

I did not get your query, you are mentioning your son’s DoB, but seeking benefits for yourself ??

my form of atal pension scheme is ready but some toll free number are saying yes & some are saying no as my birth date is 5 – 5 – 1975 and what if I submit the form if I am eligible for this scheme then 1454 will be deducted automatically from my saving account and if not then no amount will be deducted so shiv is this the right strategy or is there any risk @ at the time of 60 I can’t get any pension even my monthly instalments are dedicated so guide me

I think you should wait some more time till further clarity emerges in this matter.

Hi Shiv,

I am 35+ years old farmer , wants to go for APY for 5000 rs/month pension scheme. So my query are below :

1. After completion of 60 years Applicant will get 5000 rs /month and nominee will get 8.5 Lakh rupees , it’s right ??

2. If Applicant will be no more after some years(Like 5 or 10 years), then what will happen about deposit amount ?

Please help to clear my doubt , Thanks in advance.

2.

Hi Arun,

1. The nominee will get Rs. 8.5 lakh only when the subscriber’s is no more. The subscriber will get the pension money till the time he/she is alive.

2. Rs. 8.5 lakh in itself is the balance amount (principal + interest earned). So, if the applicant dies after some years, the nominee will get Rs. 8.5 lakhs.

Thanks Shiva!

1. I have one physical Handicap unmarried sister (Age 30 years),she is getting PA pension by government (approx 200 Rs/month).Is She eligible for this??

2. If Applicant will be no more after some years(Like 5 or 10 years) means not completed 60 years, then what will happen about deposit amount ?

Thanks Shiva!

1. I have one physical Handicap unmarried sister (Age 30 years),she is getting PA pension by government (approx 200 Rs/month).Is She eligible for this??

1) After the death of subscriber after 60 yrs. Spouse ko pension milega kya ? 2) husband & wife can eligible separately in APY ? 3) A contractual employee under Govt. project but not income tax payer and not covered by any statutory social security schemes at present ( May be covered by any statutory social security schemes and pay income tax in future), now he/she eligible for APY or not? 4) what is the meaning of unorganized sector ? if a person not interest to take the pension after attaining 70 yrs, but want to refund the corpus, is it possible ? 5) if the monthly contribution stop before attaining 60 yrs due to financial crisis, than shall i can refund the deposited money with interest & when it possible ? if husband service at govt org. with avail pension facility , so his wife can eligible for APY ? ……satya.

1. No, nominee ko pension amount nahin milega.

2. Yes

3. Yes, he/she is eligible for APY.

4. I do not have the precise definition of the Unorganised Sector.

5. You need to check it with the aggregators.

6. Yes, his wife would be eligible for APY.

1. I am 28 now. Do we have an option to change our nominee after few yrs?

2. Can we open APY in any branch but for the same bank?

3. Can we have same nominee for 2 different APY accounts?

4 . say after 60 yrs subscriber dies , will the nominee get pension amount every month or lumsum pension amount or both :)?

1. Yes Vishal, you will have the option to change your nominee.

2. Did not get your query.

3. Yes, you can have the same nominee for 2 different APY accounts.

4. The nominee will get the corpus amount only, no pension will be paid to him/her.

Hi

My date of birth 12 April 1992 then i want to open APY so please help me

How to that’s account.

Hi Mukesh,

Your query is not clear.

Hi

Sir,

I am 30yr old..if i contribute my monthly amount for 10yrs..after 10yrs if i dies,then my wife will get pension or nominee will get corpus or will retun back what amount i paid?

Hi Saju,

In this case, the nominee will get your contributed amount + interest earned on that.

if husband died before 60 then her wife will get her husband’s pension right shiv @ total pension she will get 10000 till she is alive and after 60 the nominee will get 8.50 lacs is this correct

No Nitesh, wife will not get her husband’s pension amount. She will get the corpus amount of Rs. 8.50 lakhs, if her husband dies after 60 years or the balance amount with interest, if he dies before 60.

1. What schemes come under statutory social security schemes?

2. I have Lic policy and I can still open APY right?

3. Is adhaar card mandatory? In APY form adhaar number is not mandatory though?

Thanks

Vishal

Hi Vishal,

1. EPF, Coal Mines PF, Assam Tea Plantation PF, Seamens’ PF, Jammu Kashmir Employees’ PF & other statutory social security schemes fall under this category.

2. Yes, you can subscribe to APY. LIC policy is not a statutory social security scheme.

3. Aadhaar Card is not mandatory to subscribe to APY.

and if I am wrong than if balance amount will be paid to the nominee then how much interest they will give on the total amount that the holder have given to this scheme till his death before 60

I have no idea what rate of interest will be paid if the husband dies before 60.

1.when will be starting Form filling process of APY in bank?

2.can we open PMJJBY PMSBY in one bank(ex. In sbi) and APY in other bank(ex. In Bank of india) saving account?

3.If subscriber will died between contribution period so in that case nominee will get corpus amount or only paid preemium+interest earned?

Hi Atul,

1. June 1, 2015 is the date when they will start accepting APY forms.

2. Yes, that is possible.

3. Only the deposited amount + interest earned thereon will be payable on death before 60 years of age.

Sir,

Is it possible to open NPS and APY for same individual..

if Yes,then minimum how many years i have to contribute in NPS

You need to contribute till the age of 60 years in an NPS account.

Yes, you can open both NPS and APY, but you won’t get the government contribution in APY. Also, NPS Lite – Swavalamban Yojana would be merged with APY w.e.f. June 1, 2015.

some financial website & toll free number are saying that after husband”s death after age 60 here wife will get her husband’s pension of 5000 and if wife also passes away then the corpus of 8.50 lacs will be given to nomine so is this correct

Can you please share the link of one of those sites or the toll-free number Nitesh?

Are there any similar or better pension schemes available at this moment?

Also i am just a MBA student so am i eligible? What exactly is unorganized sector? What documents will be required as a proof to show that the person is from unorganized sector?

sir,Is there any last date of this scheme???

There is no last date as such for this scheme Reshma.

Not only U take somuch effort and give all this info

But u answer to every question (even if it is answered earlier).

Its really great of u.

Thanks Mr. Rao for your kind & encouraging words!

what instalment I have to pay for wife’s pension for 5000 I have to pay monthly 990 or 1087 her birth date is 10 – 11 – 1978

I think it should be Rs. 990.

Why NPS is a better pension plan as compared to APY ? Please discus. Because i have no idea about NPS scheme.

Hi Satya,

I think NPS has the potential to generate higher returns than APY.

the be aware money and the toll free number 18001801111& 1800110001 these all are saying that after age 60 if something happens to husband his pension of 5000 and if wife is alive after 60 then her pension amount of 5000 total 10000 she will receive till her death and after her death the nominee will get 17 lacs please clear my doubt

Hi Nitesh,

I would like to stand corrected on this. You are right, the spouse will also get the pension amount in case the husband dies after 60 years of age. But, on the death of both of them (subscriber and spouse), the pension corpus would be returned to the nominee(s).

hiii,

I want Open Atul Pension Yojna policy but this policy not available in our bank of baroda, mumbai 400 004

now what should i do……

Hi Manish,

Please check this link, it has the list of POP-SP where you can get your APY account opened w.e.f. June 1, 2015 – https://npscra.nsdl.co.in/pop-sp.php

sir, Nps is for unorganized sector ???,n where it is open plz tell procedure n amount n years

Hi Resham,

Atal Pension Yojana (APY) and NPS Lite are for the unorganised sector. You need to contribute up to the age of 60 years in APY and here is the list of POP-SP for opening APY account – https://npscra.nsdl.co.in/pop-sp.php

I pay provident fund which is compulsory and is deducted at source and my employer contributes to it is as well on my behalf.

so is it that i would not be eligible for this Atal Pension Yojana

Hi Jai D,

All citizens of India are eligible for APY. But, if you are already covered under EPF, then you will not be eligible to get the government contribution.

Sir i have ppf account can i enroll with apy. please reply me as soon as possibe. As i have submitted apy form to my bank.

Yes Mohit, you are eligible for APY. But, if you are a tax payer or covered under any other social security scheme, then you won’t get the government contribution of Rs. 1,000 per annum.

Sir

I have following questions

1. I am a defence personnel, am i eligible for this.

2. If i am not eligible will my wife will be eligible who is a housewife.

3 is there any maturity amount will we get

4 if i or my wife eligible what amount monthly we had tp pay if we opt 5000

Hi Pritam,

1 & 2. Every Indian citizen is eligible for this scheme. But, if you are a tax payer or covered under any other social security scheme, then you’ll not get the government contribution of Rs. 1,000 per annum.

3. After 60 years of age, your nominee will get the corpus of Rs. 1.70 lakhs to Rs. 8.50 lakhs.

4. Contribution amount will depend on the subscriber’s age.

1. I have my bank account in ICICI bank. Can I apply for APY in ICICI bank

2. I am working in private sector and my EPF is deducted from my account & company also contribute and I am income tax payer. can I apply for APY

3. I am tax payer. Can I get government contribution in APY account

4. If any one not get government contribution then how much he need to pay to get same benifite

1. Here is the list of POP – SP where you can get the APY account opened w.e.f. June 1, 2015 – https://npscra.nsdl.co.in/pop-sp.php

2. Yes, you can apply for this scheme. But, you’ll not get any government contribution.

3. No

4. This is something I don’t know. Either the contribution amount would be higher or the pension amount would be lower.

Dear sir, my self working in private company,I want to open atal pension scheme for my wife,account holder of UCO bank, cooch behar, west Bengal,India,pin-736101,several times I am going to above said bank,unfortunately bank unable to give this form

Please do the needful.

Hi Mr. Sauren,

Here is the list of POP – SP where you can get the APY account opened w.e.f. June 1, 2015 – https://npscra.nsdl.co.in/pop-sp.php

Can 1 apply for this ataal pension yojana even if I have some other ongoing pension plans or vice versa

Yes, you can get yourself enrolled for APY even if you have other pension plans. But, you won’t get the government contribution of Rs. 1,000 per annum.

Can I open Atal pension yojna in the name of my wife.

Hi Vinay,

Every Indian citizen is eligible for this scheme.

Hi shiv sir,

If in future I will get gov job then empolyer will enroll me in NPS (National Pension Scheme) and I have atal pension yojna then will both scheme valid for me and will gov contribution continue to my account in APY at the same time

Hi Atul,

This is something I have no clue about. You’ll have to approach any of the administrators with this query.

How to apply all these schemes through online.. It will be very useful for techies if allowed to apply the schemes through online, If there is any such let me know.

Thanks

Hi Naveen,

You can apply PMJJBY & PMSBY through net banking platform of your bank, but APY is still not there on any online platform.

Hi sir, i want to enroll in apy scheme, pls guide after 60 yrs. Pension will start but pls tell me we wil get this pension till are death or it would be for some partucular perior or age like we will get till the age of 70 etc. Also pf is deducting frm my salry is i m eligible for this scheme my age is 28. Pls help thanks

Hi Radhika,

You or your spouse will get this pension amount till you both are alive. After you, your nominee will be paid the corpus amount.

Also, you are eligible for this scheme, but you are not eligible for the government’s contribution.

Hi sir

I have some question.

I work in privet company & my PF & EPF dedctect is i eligible.

If i am not eligible my wife will be eligible who is housewife. & who was nominee & who get maturity amount.like my child.

Hi Shital,

1. Every Indian Citizen is eligible for this scheme. But, in your case, you are not eligible for the government contribution of up to Rs. 1,000 per annum.

2. Your wife will get the pension amount after you and your nominee will get the corpus amount after you & your wife.

I am from karnataka that i am one important information of Atal Pension Yojana that i am an 40Years Old and my Date of Birth is 10/April/1975 at present date i can join for this APY Because Age joing APY is Minum age is 18 Years to Maximum age is 40 Years so please send me the required details that i can join for the APY .

I AM WAITING FOR YOUR SENDING INFORMATION.

THANKING YOU

SANTHOSH D B

KARNATAKA

28/05/2015

Hi Santhosh,

I think you are eligible for this scheme, but you need to confirm it from any of the aggregators appointed for this scheme.

Dear Sir,

I am 6 Feb 1975 born, will you please guide me whether I am eligible for this APY or not because while calling them 1800…. executive not able to answer, telling me to confirm with bank.

Regards,

Yogesh Joshi

Hi Yogesh,

I think you are eligible for this scheme, but you need to confirm it from any of the aggregators appointed for this scheme.

but no one has the answer to this question I have submitted my apy form in the bank if on Monday the system will accept my form than is ok and it will not then it’s bad luck for me because my birth date is 5 – 5 -1975 weather I have done the right thing shiv

As per my knowledge, you are eligible for this scheme. I don’t know whether you have done the right thing or not by applying for it without having confirmation.

now i am unmarried, and i opted for atal pension yojana scheme with my brother as nominee. is it possible to change the nominee after i got marry?

Yes Dhanaraju, you can change the nominee anytime you want.

Hi sir

I have some question.

I work in privet company & my PF & EPF dedctect is i eligible.

but IDBI bank said that you are not eligible APY

Hi Bhavenesh,

As per the rules of APY, every citizen of India, aged between 18 and 40 years of age, is eligible for this scheme.

Sir currently in m working with a company and my EPF is deducted but soon I would be leaving my job. Can I get the government benefits

Hi Namrata,

You can get the government benefits if you would be a non tax payer as well.

Dear Sir,

I am NPS Lite Subscriber and have PRAN Card. Is my NPS Lite Account will automatically migrated to Atal Pension Yojna? If so how can I come to know (verify) that?

Hi Sagar,

You would get an SMS/email regarding the same. You can also contact your POP – SP for the same.

no amount deducted from my & my wife’s saving account for apy scheme why shiv

You need to contact the POP – SP for the same Nitesh.

kay 01 June ke bad atal pension Open hoga

Yes Manish, Atal Pension Yojana mein account open ho rahe hain.

dear

sir

i want to know if i death after 60 years then what will get my nominee from Atal Pension Yojana

Your nominee will get the corpus amount of up to a maximum of Rs. 8.5 lakhs and a minimum of Rs. 1.7 lakhs.

i want to know if i death before 60 years then what will get my nominee from Atal Pension Yojana

Your nominee will get the balance amount with interest.

Sir Currently in i am working with a company and my epf is deducted but soon i would be leaving my job.can i get the goverment benifit?

2.I have another question,if i again join another job,there is also deduct epf,then my apy will be continue.

Hi Anup,

1. If you would become a non-tax payer, then only you will be eligible to get the government contribution.

2. In that case, you will not be eligible for the government contribution.

Sir, I want to enroll APY but if I get a good government job after few years, what will be the status of APY, whether it will be continued or not becoz its not for the NPS holders and I shall be the NPS holder after getting a government job.

Hi Ajay,

In that case, you will not be eligible for the government contribution of Rs. 1,000 per annum.

Sir,

i want to know if i death before 60 years then what will get my nominee from Atal Pension Yojana

Whatever balance amount is there in the account along with the interest earned would be given to the nominee.

If i do APY and if i death before 60years than what my nominee(he/she) continued give APY premium or not and what nominee get?

Whatever balance amount is there in the account along with the interest earned would be given to the nominee. No further amount would be required to be invested.

Sir,

I have two queries regarding the atal pension yojna, please clarify:

i) Can my wife(housewife) apply for this yojna, specifying myself(government employee) as the nominee.

ii) Starting 60yrs of age for how many years she will get the pension? For example i am opting for 5000 as the pension amount, will she get it till her death or maximum of 8.5lakhs. (850000/12*5000)

Hi Sarbojit,

1. Yes, every citizen of India can apply for APY.

2. Pension will be paid to the subscriber and his/her spouse till they are alive. After their death, Rs. 8.50 lakh will be paid to the nominee of the subscriber.

my instalment of 1454 has been deducted from my saving account so then it is 100% sure that I will get all the benefits of atal pension scheme as my birth date is 5 – 5 1975 so there was a little confusion that weather my form will be accepted or not and tanks shiv for your guidance

That’s great, congrats!

Hi i am NRI am i eligible for APY scheme ???

No Anish, NRIs are not eligible for this scheme.

If i do APJ and after 1 or 2 years i unabble to give my premium than what happen? Plz ans

The account will become inactive and your returns will get affected.

sir

I am now 20 years, as the scheme I need to pay 248/- for 40 years or one year? every the monthly contribution will increase or not?

Hi Babu,

You need to deposit Rs. 248 for 40 years. Contribution will remain the same throughout these 40 years.

Hi,

I would like to know if after I am 60 years, other than the pension will I get any other lump-sum amount too in APY?

Thanks,

Jones

Hi Jones,

You’ll get only the pension amount every month, your nominee will get the corpus amount after you.

Sir,i aplay for PMJJB on 31st may.but no money deducted from my account.deducted only 12 rs for pmsby.how can i chek my application accepted or not.

Today i done APJ but i want to know that how can i check my APJ online. Pla ans

Hi Gaurab,

You will get SMS updates & physical statements for your investment made.

Hi Hari,

You need to check it with your bank.

Today i done APJ but i want to know that how can i check my APJ online. Pla ans

Online facility is still not there.

Sir,

I am a govt. Service holder .I ask u my perents atol pension yogana .acceptable

I am a student of 25 age.As of now i am not paying any income tax.now if i will take the scheme and after 2 years i started paying IT then will i need to inform bank to stop the contribution from govt.

Hi Sudeep,

I have no idea how the government will have these checks.

Hiii…Shiv Sir..

I want a enroll a APJ. But I have a little confusion. please let me know. I am working aw privet sector company and where deducted EPF. Can I eligible for pension and after me my spouse will get corpus fund 8.5 Lacks.

Hi Mr. Kedar,

You & your wife will be eligible for pension after 60 years of age. Your nominee will get the corpus of Rs. 8.5 lakhs after you.

Can we change the nominee in this scheme?

can we change the nominee in APY?

Yes, you can change the nominee in this scheme.

Sir i have done APY @231 but know i want to change my policy premium @500p m what was the process plz ans

Hi Gaurab,

You can increase your contribution amount only once in a year, during the month of April.

Dear Sir,

Kindly let me know Should i Open or Not Atal Pension Yojana Policy Bcoz I have already have LIC POLICY AND PPF ACCOUNT IN BANK.

and 2 Point :

if Government Change Whether this Policy gets change or remind same

Pls Clear it out Bcoz Bank Person Also Dont No Rule of Policy

Hi Manish,

From investment point of view, I think it is not a great scheme. PPF, Sukanya Samriddhi Yojana, Mutual Fund SIPs, NPS etc. are all better than this scheme. If government gets changed, my guess about the future of this scheme is as good as yours.

Dear Sir

After I attain 60 years I’ll take my pension amount say 5000? per month for some 5 years and if I die suddenly , will my nominee get 8.5 lakh as corpus amount then also….??

Yes Nandish, your nominee will get Rs. 8.5 lakh in that case also.

if after 7 or 10 years i want to close APY than what will i get from this ….

You cannot close this scheme prematurely.

if i do this and after year few i was dead before 60years then what will get my nominee from APY

Whatever balance amount is there, your nominee will get that amount.

Hi Shiv,

Is there any Provisions in this Atal Pension Yojna that i don’t take Pension after 60 years but to get Lumpsum amount and if yes then what it could be at age of 35 Years in Rs.5000 Pension plan

Hi Mr. Rajesh,

There is no provision to take lump sum money in this scheme.

Sir my dob is 4/6/1975 but bank manager reply me no pension scheme is launched govt making fool. Ambala mall road main branch sbi manager reply these words i want put a complaint against that manager.

You can make a complaint on SBI’s website also – https://www.sbi.co.in/portal/web/customer-care/complaints-feedback-appreciation

Shiv sir,

Thanks for your previous response and you are doing grt work by responsing each and every query of each person…very appreciable sir…keep giving ans of our query…once again thanks a million sir

Thanks Atul for your encouraging words! 🙂

And sir I have query that

1. Is sbi accepting APY form?

2. If I join in next month so should I have to paid premium of jun and july together or only july

3. What are document should attach with form of APY

1. Only a few selected branches of SBI are accepting APY form.

2. If you join from July, you need not pay anything for June.

3. You just need to have a bank account for APY. No other document is required.

if i do this and after few year i was dead before 60years then what will get my nominee from APY

In case of death before 60 years of age, whatever balance amount is there, your nominee will get that amount.

Hello sir,

I am self employed & already tax payer & i have ppf account also. If i want an amount of rs 5000 as a pension ,Can i opt this scheme.

Yes Akanksha, you can opt for this scheme, but won’t get the government contribution of up to Rs. 1,000 per annum.

sir…..

Abhi mai 23 yrs old hu…..iam eligible to join apy scheme but later i do job and comes in tax slab…..so will my apy scheme continue for me

and also after joining apy.scheme……can i also hv later my ppf account and can i enroll for other pension schemes later..??

Hi Birendra,

As you become a tax payer or get employment with EPF etc., you’ll stop getting the government contribution of upto Rs. 1,000 per annum.

Sir This is Anup from Kolkata,

I have a little confusion regarding APY secheme,Sir currently i am working in a private sector,i have a pf account in at my company,but i know i am eligible for Apy scheme,but i dont understood the goverment contrubution.plz explaing me,

Hi Anup,

Modi government has started this scheme for the workers in the unorganised sector and has committed to contribute up to Rs. 1,000 per annum for 5 years to those account whose subscribers are not tax payers and are not covered under any other social security scheme like EPF etc.

Hi Sir

I am Anup,i am from Kolkata,i am working in a private sector.my EPF deduction every month,if i join APY scheme,then will i get pf benifit double,after leaving the job.

EPF is a different scheme and APY is a different scheme. You’ll get benefits under both the schemes, but, as you are already covered under EPF, you won’t get the government contribution under APY.

Sir, if husband(working)and wife(housewife) both take this plan and if any of one will get dead, can other one will getting 2 pensions.

Yes, the surviving partner will get both the pensions.

What happen if i joined this scheme on age of 18 and die around on my 40 or 50 so what happen with my money what happen wid dis scheme

Hi Shiprana,

Your nominee will get the balance amount in the account.

Hai sir,this is shyamala,iam house wife,can i enroll for this apy scheme?

Hi Shyamala,

Every citizen of India is eligible for this scheme.

I want to know online process for join ing APY from my sbi account .thank .

Hi Pritam,

You need to check with your bank whether they are providing online facility or not.

Sir,