As the government decides to sell stakes in PSUs in the coming months, you are going to see a slew of companies coming out with their stock offering and with the current economic environment, it is very easy to get carried away and invest a disproportionate amount of money in IPOs.

I’m already seeing the excitement around IPOs build up although the retail participation so far has been nothing compared to what we have seen in the past.

If you remember the MOIL IPO – the retail part of that was subscribed about 3o times over!Â

For most people, it is ridiculous to think about something that happened two years ago, and guess what? Most people continue to make the same mistakes over and over again.

Nothing about IPO investment has changed, and in the coming months, you will most likely see sentiment pick up and over-subscription levels reach ridiculous highs.

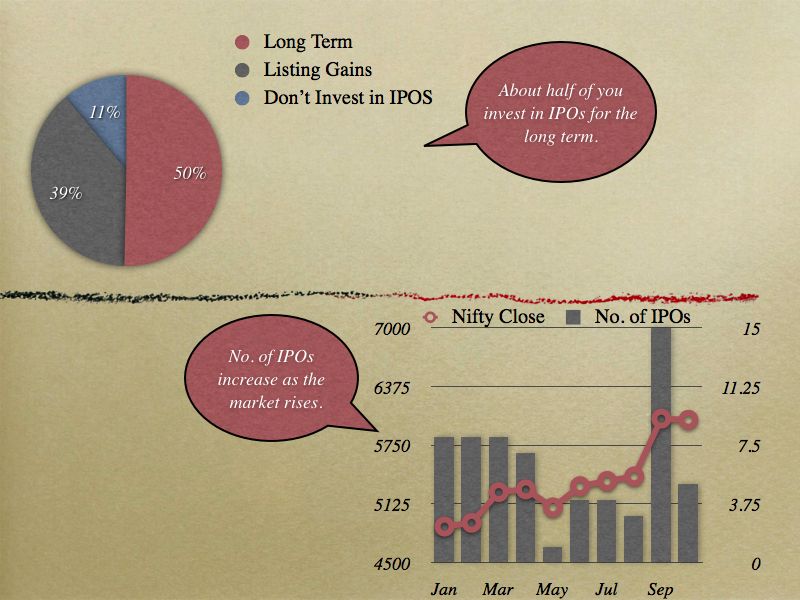

When that happens, consider this chart that I made over two years ago.

What this chart shows is that the number of IPOs rise when the market conditions improve, and that makes total sense when you think about it. Promoters are interested to extract maximum value out of their stakes and why would anyone who can wait sell their stakes when the markets aren’t doing well?

But at the same time, when the market goes down, all these stocks also go down with it, and that results losses on stocks you bought in IPOs and also much worse, stocks that you bought just after the IPO.

I took the MOIL example for this post because the company was doing and is doing quite well and the oversubscription was so high that people got allocated only a few shares, and then after listing bought more of it, and suffered losses on those too.

As the frenzy surrounds you in the next few months – Â be patient and at the very minimum avoid investing in any IPOs that have bad fundamentals.

Short answer:

I don’t know, and if I did, I certainly wouldn’t have wasted time writing a blog.

Long answer:

Shiv told me a few days ago that he’s getting calls from clients asking what they should do in this rally, and people have a feeling that they’ve been left out on the sidelines and what’s the next course of action for them.

For anyone who has spent any amount of time near the markets, you shouldn’t be surprised with these type of questions, and especially the timing of these type of questions. People get interested only when something goes up, and when it’s down, no one is willing to buy anything.

I believe this is a good time to to think about what you will do when the market falls next.

That’s usually my approach, I’m a regular equity investor, but I’ve pared down my investments in the past few months, and I’m building up cash so that I can take advantage of the next downturn. This does’t mean I expect the market to go down any time soon, just that I feel it won’t be a one way journey where if you don’t invest now, you will never be able to invest at these prices (I Â have not stopped completely because I know I can be wrong). I’ve never bought that argument.

In my opinion, having a plan on what you will do when the market falls next is going to be a lot more useful than trying to find out when will Sensex hit 25,000. Before you look for answers, you need to ensure that you’re asking the right question.