ELSS – Equity Exposure + Tax Savings = Deadly Combination in a ‘Down’ Market

This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

A few days back I was watching CNBC-TV18 in the morning when the markets were about to start trading. Udayan Mukherjee and Mitali Mukherjee were talking to Prashant Jain about his expectations from the stock markets in 2013. Let me tell you Prashant Jain is the Chief Investment Officer of HDFC Mutual Fund and the fund manager of two of HDFC MF’s most popular schemes, HDFC Top 200 and HDFC Equity Fund, among others.

Let me also tell you that I try to regularly follow Prashant’s thoughts on investment environment and earnings expectations.

He shared his views that the markets are trading at a forward Price/Earnings (P/E) multiple of 13.5 to 14.5 times, based on the FY14 Sensex earnings per share (EPS) of Rs. 1350 to Rs. 1450, which is below the average P/E multiple of 17 times. As per him, the retail investors always lose money in the stock markets because of their poor timings of entering and exiting the stock markets.

He further said that it is unfortunate but the stock markets always get retail investors’ investments when the P/E multiples are on a higher side, say above 17-18 times and they always cut their holdings when the markets just start their journey to newer highs and the P/E multiples are on a lower side, say around 13-14 times.

If you analyse the current markets scenario when the Sensex has risen past 19000 levels, many of the investors are doing exactly the same what Prashant is suggesting. On the one side, they are either redeeming their mutual funds or surrendering the mis-sold ULIPs or cutting their holdings in stocks/booking profits too early. On the other side, they are increasing their asset allocation towards the debt/gold instruments like fixed deposits, tax-free bonds, NCDs, Gold ETFs etc.

Some investors think that if the markets have risen from 16000-17000 levels to 19000-19500 levels, it is better to sell their investments in mutual funds or shares as the markets will again fall to sub-17000 levels due to some reason and these stocks will again take 2-3 years to reach these levels.

Is this a prudent investment strategy to earn above average market returns? Definitely Not. It is next to impossible to predict the definite direction of stock markets. A common investor should invest in the markets when the markets are cheap and continue investing till the markets remain cheap. When to sell? The answer is very simple – when the markets are expensive or the P/E multiples are above reasonable levels, say above 20-22 times.

But honestly speaking, it is very difficult to follow it practically because when the markets become expensive, the growth in EPS is very strong and we get driven away by some rosy pictures getting published daily in the newspapers. Also, our greed grips us so strongly that we are just not able to book profits.

So, when the markets are down, it offers a very good opportunity for the investors to invest in direct equity or equity linked investment products. Moreover, if any of these instruments provide you an additional tax benefit u/s. 80C also along with completely tax-free returns on maturity/redemption, I think it makes it a perfect investment for most of the investors.

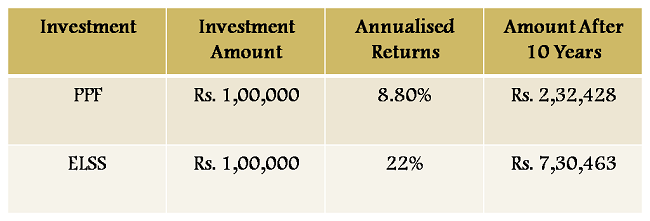

As per a CRISIL report published earlier this year, it showed that Equity Linked Savings Schemes (ELSS) have been better investment options than PPF, NSC etc. It showed that these schemes delivered an average annualised returns of around 22% in the last 10 years. PPF at present earns 8.80% per annum for you and that is also tax free at maturity.

The table below shows a comparison between ELSS and PPF. With similar returns of 8.80% and 22%, your Rs. 1 lakh invested today in PPF and ELSS would become Rs.2,32,428 and Rs. 7,30,463 respectively after 10 years.

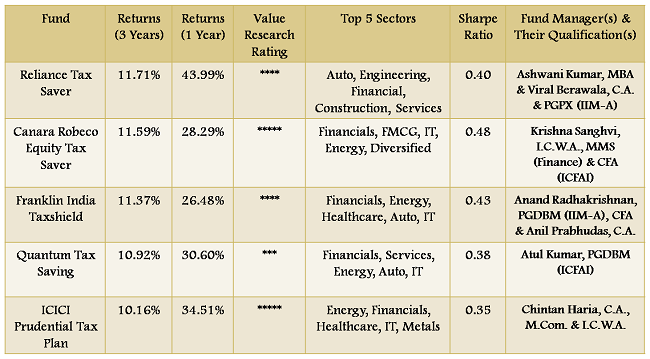

Some good performing ELSS have delivered very good returns in the past 1 year period. But, I think investors should also observe their long-term performances. The table below shows the list of five such schemes with their 3-year and 1-year performances.

With a lock-in period of 3 years, I think tax saving mutual funds (ELSS) as a category should outperform all other tax saving products in the next 3-5 years. But, for that, the corporate profitability should improve and the government should start taking steps in the right direction. Lets see how these funds deliver in the times to come.

I fail to understand the connection bet the content of the article and its title.

Hi pattu… It was some technical error due to which the latter half got missed out in the morning. It has been rectified now.

What is the co-relation between the title and the content ..???????

Hi man… Please check the article again, I hope it makes sense now!

The latter part of the article didn’t come through in the morning.

“tax saving mutual funds (ELSS) as a category should outperform all other tax saving products in the next 3-5 years”

This has pretty much been the case since the inception of ELSS, and is irrelevant to ‘up’ or ‘down’ markets and to star manager comments

I think it makes more sense to invest in ELSS in a ‘Down’ market, as compared to an ‘Up’ market, when the PE multiples look more reasonable. Investors need encouragement to invest in equity/equity linked investments when the market are down. They easily get scared in a Down market and euphoric in an Up market.

I apologize for the error where only half the article was published in the morning. It was my error where I copy pasted only half the article from the source and didn’t proof read.

@shiv and Manshu

This triggers a question inside me!!

Should we need to stick on to the Tax saving Mutual fund after the lock(22 percent returns in last 10 yrs) in also or we take out put it in the Diversified equities?

I think its better to shift to diversified eq schemes. Since DTC is about to be implemented wherein ELSS will loose its position under sec 80c, MF managers may or may not give required attention to this schemes later on or they may merge the schemes to their own div.eq. schemes.

Hi Vignesh,

I think these tax saving mutual funds should ideally perform as good as diversified equity funds. So, if you do not need to reinvest your existing investment in ELSS for this year’s tax saving investment, I think it is better to remain invested in these funds. Also, if your ELSS is not performing, then you should opt to redeem it and then invest the proceeds in some good diversified funds.

thanks shiv and kartavi

You are welcome Vignesh!

I think its better to shift to diversified eq schemes. Since DTC is about to be implemented wherein ELSS will loose its position under sec 80c, MF managers may or may not give required attention to this schemes later on or they may merge the schemes to their own div.eq. schemes.

Hi Kartavi… We are hearing this from the last 2-3 years that DTC will come and that will happen or GST will come and something dramatic will happen. I think even if the DTC gets implemented from the next financial year, it is not going to affect your existing investments retrospectively. Whatever happens with these schemes will happen in the best of investors’ interest for sure.

OK. thanks

Further, I want to say, ITS RIGHT ARTICLE AT RIGHT TIME. Thanks again.

After reading this, I got confidence in my decision: “not only to maintain SIP of last year but to increase to the extant possbile for next year”. Thanks.

Great, you are most welcome Kartavi !!

Yeah.. i was not sure to continue with my SIP in ELSS or not before reading this..this article has helped to boost my confidence in ELSS funds.. i was going through other posts to decide where to put the money to complete the 80C section. but i guess now i know..

You are investing in ELSS systematically on a regular basis, that is great Mr. Shankar! That is what Prashant Jain, Manshu and other good financial advisors recommend for almost all common investors. At the same time, it is equally (or probably more) important to balance your asset allocation (book profits from equity linked investments regularly) when the market valuations become expensive. Please dont become greedy when the markets become expensive and the investors become euphoric.

Yeah I agree with that. I don’t see how they can implement DTC with so many open points still remaining and even if they did they won’t touch anything retroactively.

Yes, it is a ‘deadly’ article.

I always like ELSS than any other tax saving instrument.

Thanks Umesh! I prefer PPF in an ‘Up’ market.

….” I prefer PPF in an ‘Up’ market “….

How and why.. pl explain.

Because there is “No risk of capital Loss” with PPF. Markets can fall when they are overvalued.

That’s a good question.

Hmm… In the last 5 years, ending December 27th, 2012, ELSS as the category has given an annualised return of -0.57% i.e. if I had invested Rs. 1,00,000 in ELSS on December 28th, 2007, my investment would have degrown to Rs. 97,180. On the other hand, the same investment would have crossed Rs. 1,50,000 in PPF by now. Not a perfectly valid answer, but still this is what I have to say.

I agree with that reasoning but I was only saying that it was good of Kartavi to ask that and make you spell out the reason else it would be open to assumption.

Yes, Thanks to both of you Shiv and Manshu. But question is ” how the people like us can know that the market is UP or DOWN at present and what will happen in next 5 years ?” Please tell us for present juncture of time … what should we do… invest in ELSS or in PPF ?

Please check this video – http://www.moneycontrol.com/video/mf-interview/hdfc-mfs-prashant-jainwhy-retail-investors-always-lose_795117.html?utm_source=Article_Vid

Prashant Jain tells investors to focus on the PE ratio. India’s forward PE ratio has historically averaged 16-18 times. It becomes expensive when it crosses 20-22 times. Currently it is at around 14.5 times 1-year forward earnings.

So, it makes ELSS my preferable choice this year for tax savings, if I were to opt for only one out of these two. In reality, I have invested PPF for my tax savings/tax-free returns and actively investing in direct equities.

One more for your reference – http://www.thehindubusinessline.com/features/investment-world/indian-investors-dont-own-enough-equity/article4253167.ece

Thanks for the link, I gone through the above article. Its really eye-opener.

But, how and from where, we can know the ‘India’s forward PE ratio’ / ‘One year forward PE multiple of the broad market’ since people like us can neither analyse nor calculate by self, such things.

I’ll add a word of caution here that times like this when most people are recommending stocks are usually not the best times to invest Kartavi.

The best times to invest are when you post comments where you ask should you exit out of mutual funds and invest in bank FDs like this comment:

https://www.onemint.com/2011/01/14/banks-with-high-interest-rates-on-fixed-deposits/comment-page-2/#comment-165985

The market is up 20% from that time.

You should either invest regularly at all times or not invest in the market at all. Have you invested anything in the stock market in the past one year when it actually saw a 27% rise?

Please check this link – https://www.onemint.com/2011/09/21/nifty-pe-ratio-chart-and-how-to-get-to-this-data/

You can get the trailing PE Ratio this way from the NSE website, but you will have to forecast earnings growth for the coming years to get forward PE multiples. Every research house has its own growth numbers, so it varies with each of them.

Thanks shiv, its really good advise about ELSS+PPF+direct equity.

Your post and comments, have supported our decision about continuing the SIP in MF in upcoming year… but people like us can’t do maths like forward PE on our own. And hence it may be true that we do not exit from equity investments (MF also) at reasonably right time. Could u pl have a post whenever u find that the forward P/E multiples are above reasonable levels, say above 20 times.

(Ref to your comment [which has no REPLY link] on December 30, 2012 at 7:31 pm )

Yes Manshu, I not only stick to SIP and equity investment, but started new SIP in 4 M.F.

(1 Large, 2 Mid&Small, 1 Balance) which is at 18% return as on today.

Based on your following two posts and discussion there on

1. my-thoughts-on-equities-fixed-deposits-and-gold (Aug-11) and

2. Which is the best place to invest (Nov-2011).

I further, maintained a balance of FD, PF, MF, Gold, Cash (45%, 27%, 18%, 9%, 1% of

the investments respectively) with a goal like Child-Education, marriage, retirement etc.

Started buying GOLDBEES (1 unit every month) for next 10 yrs, for upcoming marriage in family.

Did not buy GOLD for investment purpose.

Did not buy a house for an investment purpose.

Manshu, your posts are very clear and to-the-point and indeed it has helped many middle class / small investors like me.

Further, as per your advise “You should either invest regularly at all times or not invest in the market at all†… this year also I am going to keep continue those 4 SIPs and see that my investments will remained balanced in same proportion(%) and …… will not bother any predictions or PE complexities. Please correct me.

This is good allocation, and it’s great to see that you haven’t exposed yourself to a lot of volatility. Even if the market or gold were to come down you wouldn’t be affected by it a lot.

This is obviously good, and I posted my comment to see if you are just going to start investing in equity right now because if that were the case, it would’ve been really bad.

The market will go down again, no body knows when, but just like earlier, it will go down sometime in the future too, and a lot of people make money mistakes because they don’t understand that but invest in the market when it is up, and sell when it is down, which is the worst thing you can do.

You however seem to have struck a good balance.

Credit goes to your posts and comments. Thanks to you.

Hi Shiv

Very good!!!

Comparing selectively. Comparing selective time period of 5 years, while PPF is a 15 year instrument.

Sorry my friend, you cant compare a 3 year instrument with a 15 year instrument, in a 5 year time frame.

Yes if you want to compare, then you can compare the returns of this ELSS (invested in December 28th, 2007, at the peak) after 15 years (if one remain invested for 15 years).

OR as you said “I prefer PPF in an ‘Up’ market”

And UP market doesnt mean PEAK, every time.

But why not wait for a correction in the market, why invest in UP market.

Hi Umesh… Probably you are right. To me, both ELSS and PPF are instruments with infinite time horizons. I think every investor should have both these investments in his/her tax saving/investment portfolio and use them as per market conditions. When the markets are Down, go for ELSS and when the markets are Up, go for PPF.

3 years for ELSS and 15 years for PPF are just lock-in periods/maturity periods. After 3 years, ELSS becomes an open ended diversified equity scheme which one may hold till whatever time he/she wants. PPF is also extendable for 5-5 years.

Whenever markets have fallen from euphoric levels, they have taken their own time to recover back. I would always prefer peaceful 8-9% returns as compared to even 10-12% volatile returns which give me sleepness nights. I think I need more than 15-20% equity returns to make me invest in equities, which I think I can get only when the markets are cheap and ‘herd’ mentality is not following the stocks or equity linked investments like the present market conditions.

I had selected 5 years because I think markets were euphoric 5 years back. And it was not intentional. I just went to Value Research and picked 5 years returns on December 27th, 2012. If I had used point-to-point returns fron ‘Peak’ to the lowest levels of the markets, then the returns would have been more negative.

My 2 cents:

Each year is a different year, macro and micro economic trends (both global and local) dictate what should be one’s investment policy. ELSS’s are usually close ended funds so once invested, one is locked for a couple of years either due to the mandatory lock in or due to the exit load. They may have been the toast of 2012, they might not be in 2013, we don’t really know. But still I think the comparison of ELSS and PPF is a very valid one and very significant in the topsy turvy stock markets. Its a great investment strategy to think about and one that will go lengths to make a balanced and attractive portfolio.

The other point I wanted make was that its actually easy to say to track the market in terms of PE multiples; this maybe can be done for stocks but how does one do it for MF’s? How does one determine if a MF is expensive or not? At least a common man who has some finance knowledge will not be able to do, I am pretty sure. If there is a way, I would be surely very interested in knowing about it.

Hi Gaurav… It is easier to get that info for MFs. Please check the “Portfolio P/E Ratio” for HDFC Equity from this link – http://www.valueresearchonline.com/funds/portfoliovr.asp?schemecode=219

But you are right that it is not easy for the common investors to do it easily themselves.