This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

After India Infoline Finance Limited (IIFL), the 98.87% subsidiary of India Infoline Limited (IIL), successfully raised Rs. 1,050 crore from its 12% NCD issue in September this year, its own wholly owned subsidiary India Infoline Housing Finance Limited (IIHFL) has now come up with its issue of non-convertible debentures (NCDs).

Before we check out more about the company and its financials, let’s take a look at some of the main features of the issue first.

Coupon Rate – The issue is simply uncomplicated. It is offering only one choice of coupon rate i.e. 11.52% per annum payable monthly and that too, only for 60 months. Effective yield comes out to be 12.15% per annum. But, mind it that it is taxable as per the tax slab of the investor and is also subject to TDS, if taken in physical form.

Size of the Issue – Base size of the issue is Rs. 250 crore and the company has the right to exercise the green-shoe option to retain oversubscription to the tune of another Rs. 250 crore, thus making it a Rs. 500 crore issue.

NRI Investment – Non-Resident Indians (NRIs) are not allowed to invest in this issue.

Opening/Closing Date – The issue is scheduled to open on Thursday, 12th of December and will remain open for subscription for just 7 working days to close on Friday, 20th of December. The company has the option to close it earlier or extend it beyond the closing date, depending on the investors’ response to the issue.

Minimum Investment – If you want to subscribe to this issue, you need to invest at least Rs. 10,000 i.e. 10 NCDs worth Rs. 1,000 each.

Listing – The company has decided to list these NCDs on the National Stock Exchange (NSE) as well as on the Bombay Stock Exchange (BSE) and the listing will happen within 12 working days from the closing date of the issue.

Demat A/c. Not Mandatory – Though these NCDs will get listed on the stock exchanges, it is not mandatory to have a demat account to invest in this issue. You can subscribe for these NCDs in physical form as well, like you invest in bank fixed deposits (FDs) or post office schemes.

Only the investors, who subscribe for it in demat form, will be able to sell/trade them on the stock exchanges and will not be subject to any TDS on the interest income.

No Put/Call Option – The investors subscribing for these NCDs in physical form will have no option to redeem/sell them before maturity, as the company has not given put option to its investors. At the same time, the company will not be able to call its option to return investors’ money before the maturity period.

Credit Rating – CRISIL and CARE have been appointed as the credit rating agencies and have rated the issue as ‘AA-/Stable’ and ‘AA-’ respectively.

Categories of Investors – The company has decided to categorise investors in the following three categories:

Category I – Qualified Institutional Bidders (QIBs)

Category II – Non-Retail Investors including HUFs, Corporates etc.

Category III – Retail Investors including HUFs investing Rs. 10 lakh or below

Category Reservation – 50% of the issue size i.e. Rs. 250 crore, has been reserved for Category III retail investors, 35% i.e. Rs. 175 crore for Category II non-retail investors and 15% i.e. Rs. 75 crore for Category III institutional investors.

Allotment on FCFS Basis – As with most of these issues, allotment in this issue will be made on a first come first serve (FCFS) basis.

Interest Payment Date – IIHFL has decided to pay interest on the investors’ money on a monthly basis, but has not fixed the date of interest payment as yet. Interest payment will start from one month after the deemed date of allotment and will keep on getting paid on the same date every month.

Profile & Financials of India Infoline Housing Finance Limited (IIHFL)

India Infoline Housing Finance Limited (IIHFL) is a wholly owned subsidiary of India Infoline Finance Limited (IIFL), which is a 98.87% subsidiary of India Infoline Limited (IIL). As its name clearly indicates, the company offers housing loans and loans against property (LAP).

IIHFL received the certificate of registration from the National Housing Bank (NHB) to carry on the business as a Housing Finance Company (HFC) on February 3, 2009, which makes it a company with short operational history.

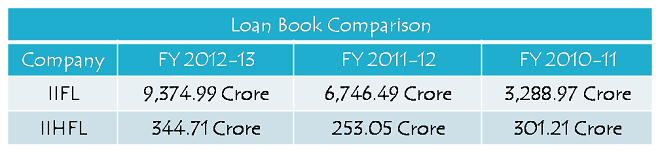

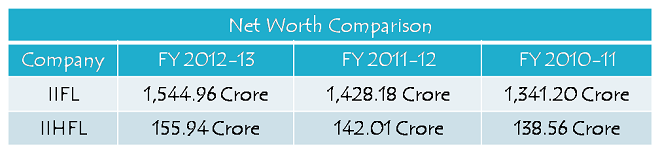

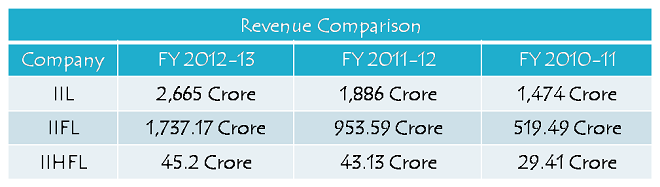

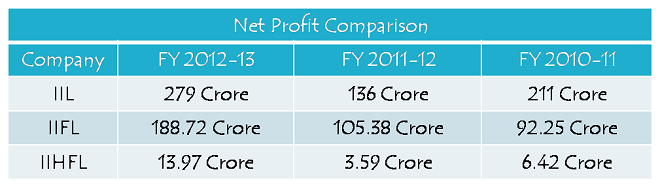

To measure the scale of its operations, I tried to do some comparison of its financials with that of its parent company, IIFL and IIL, the parent company of IIFL. Here are certain tables which carry some relative data for comparison:

These tables clearly show that IIHFL is a very small company relative to IIFL and IIL. Also, though the company deals in secured financing only, which ensures lower NPAs and lesser recovery related problems, its business model is very much concentrated to a single segment i.e. housing loans and loans against property. This makes it more vulnerable to adverse market conditions including intense competition, an economic downturn or a sudden downward movement in real estate prices.

IIFL, in its September issue, offered coupon rates of 12% per annum. It is really surprising for me to see the parent company offering higher rate of interest and its subsidiary, of a much smaller size, offering a lower rate of interest @ 11.52% per annum.

Personally, I won’t put my money into this issue and won’t advise any of my clients either, except somebody who is not liable to pay any taxes and wants regular income on a monthly basis.

Application Form for IIHFL NCDs

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in IIHFL NCDs, you can contact me at +919811797407

Dear all,

Does anybody has to say anything about this issue now. Because i have purchased it. Each month received interest. In Dec. 2018 it ll mature. Should i wait for maturity or sell it

poor analysis, no mention of maturity date for a bond issue!

my error – 60 months mentioned in article.

Dear Mr Shiv.

If the NCD/ Bonds are “Secured” is there still any risk involved How ?

Hi Saksham,

Yes, there are certain risks, like if the company defaults on its interest payments and the value of those assets, against which these NCDs are secured, goes below the outstanding liability of the issuer, then the investors might not be able to recover their investments fully.

IIHFL NCDs got listed on the NSE & BSE today, January 1, 2014. 11.52% 60-month NCDs listed at Rs. 991, hit a high of Rs. 996.70, low of Rs. 987 and closed at Rs. 989.15. Total NCDs traded on the NSE were 479.

BSE code for these NCDs is 934932 and the same with the NSE is N1. Deemed Date of Allotment has been fixed as December 27, 2013.

IIHFL NCDs issue to get closed today i.e. December 18th.

Thank you for giving the information.

You are welcome!

I dont understand how can they be competitive in home loan market if their own cost of funding is so high at 12.15pc.?

Good to see your comment after a long time Ankur !!

IIHFL’s prospectus shows its Average Cost of Borrowings to be 12.16% and Net Interest Margins (NIMs) to be 8.09% for the half year ended September 30, 2013. This shows that IIHFL’s major lending is happening in tier II, tier III cities and that too, majorly for LAP or sub-standard loans.

Hi Shiv, yes, I visited the site after long; when someone asked me how is IIFL bond issue. So if they are charging 20%+ from borrowers, it is possible that the LTV is high or the property is illiquid/inferior. Any idea, what is the break up of their portfolio into actual home loans and LAP.

Given, its miniscule presence in home loans, I dont think this co can sustain in business for long. Somehow, i dont get the logic of broking companies, getting into home loans

I could not find the break up of their lending portfolio Ankur. In fact I would say IIHFL’s disclosures in the prospectus are inadequate to be comfortable.

I think this company is at a nascent stage. Only time will tell whether it will be able to sustain in this business for long or not, but at present it is at a more riskier stage.

A broking company is getting into loans business because broking business itself is in a very bad shape. HSBC closing its retail broking business is a big example.

Hi Shiv,

Apologies if I’m missing something. How come a company with net worth of approx 155 crores is allowed to collect funds in range of 500 crores from the market? Do they have assets worth 500 crore to secure these NCD’s? I really appreciate your help because I’m new to these type of investments hence have very little knowledge.

Regards

Hi Ikjot,

As of March 31, 2013, IIHFL’s Net Worth was Rs. 155.94 crores which increased to Rs. 301.49 as on September 30, 2013. It has a total debt of Rs. 264 prior to this issue, so its debt to equity ratio is 0.88 (Rs. 264 crore / Rs. 301.49).

Post this issue, its debt would get increased to Rs. 764 crore and its debt to equity ratio would become 2.53. It is normal for financing companies. IIHFL’s parent company IIFL has debt to equity ratio of 6.65.

Thanks Shiv for explaining in such detail. Based on your recommendation, I’ve decided to skip this one.

You are welcome Ikjot!

Please be advised that assets and net worth are not the same. Net worth is equity which is equal to assets – liabilities. So if IIHFL has equity of 155 crores then obiviously it’s assets will be more than 155 crores unless they have no liabilities.

This is a bad issue and believe me after one year no one is going to get any money out of this. All the money will be down the drain. there are too much of litigation and directors past history of frauds and misappropriation is a clear indication that all the money invested will be lost. Hardly you can even recover the principal.

Hi SBSinha,

If you are so sure about it, can you please share some sources of such large scale frauds or misappropriations ??

Dear Mr Kukreja,

It is all on the internet sites. If you notice from the nature of frauds it is all about trading on clients a/c without authorization, risking others money without authorization, all kind of misappropriation of funds. Besides this as the entire Funds is mortgaged against the properties which is not in the near future is likely to give a return of the kind of promise that has been made.

If the motive of the issuer is unethical then the issue will definitely be oversubscribed but it is like a suicide. The issue will oversubscribe not on fundamentals but on greed and I can bet after five years you can’t recover your principal.

Dear SBSinha,

I am sure we are living in India and cannot expect the closest of scrutiny in these kind of matters, as all these are very common here. That is the reason I prefer to take more risk in equity markets here and avoid such riskier NCD issues of private companies.

Probably your concerns are perfectly genuine, but then IIHFL is a registered HFC under NHB and it is the regulator’s responsibility to monitor its operations. Investors themselves need to understand the risk factors before investing with such companies.

Dear Mr Kukreja, Tell me honestly if you have to rate on a 1-10 rating on getting the promised return as well as the principal back what rating you will give to this NCD. Lets bench mark 10 as “Definitely” to 0 as ” Definitely Not”.

Regarding Company being registered so was Satyam, So was Usha Rectifier and so was Essar Oil. what happened to all these.Do you think SEBI does not know about the financials about the company or CARE do not know the financials of that company. And do you believe that financials of Satyam were not known to SEBI and PWC and IT officials and PF officials etc. All the bankers, SEBI , Rating Agencies and the Auditors are hand in glove to make the fraud happen. Every one gets the share.

Regarding registration IIHFL is not yet registered with NHB.

Tell me one company in the recent past who has given such a monthly return and given the principal back.

I would give a rating of 1 on this issue.

Dear, SBSinha,

As I’ve already mentioned in the post that personally I won’t put my money in this issue. I think it is a better way to express my opinion about this issue rather than rate it from 1 to 10. I would not like to do that as some people would take it as an advice.

We all watch movies. I am sure you also do that. It is not the duty of the censor board or the government to stop a bad movie from getting released. It is up to an individual whether to watch it or skip it. Similarly, the offer document or the prospectus clearly asks you to read the risk factors before investing. It is up to you how you take it.

You might be absolutely right in your assessment about this company but then if companies like IIHFL get banned from raising money from equity or debt markets, then no company would be able to grow bigger.

Out personal views match :).

Call me paranoid but as a general rule name ‘Infoline’ itself is red flag for me.

Hi Binish,

I don’t hold anything against the group, but I think rates/yield should be 12.5% to 14% for me to invest in such NCDs from a new company like IIHFL. IIFL’s 12% NCDs (2-3 months old) are quoting at Rs. 999. So, why should I pay Rs. 1,000 for IIHFL NCDs?