This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

After raising Rs. 300 crore from the markets in September and another Rs. 300 crore in November this year, Muthoot Finance has again decided to approach the investors to raise another Rs. 500 crore. The company has launched its issue of secured and unsecured non-convertible debentures (NCDs) from today and it is scheduled to remain open for one month to close on January 27, 2014 i.e. last Monday of next month.

The base size of the issue is Rs. 250 crore and the company has the right to exercise its green-shoe option to retain another Rs. 250 crore. Muthoot’s last issue in November got closed in six working days time, I think that is why the company has increased the issue size this time around. The company would like to repeat its success this time also.

Most of the features of the current issue, including its coupon rates for the retail investors, are exactly the same as they were in the first two issues. Let us again have a look at all of these features.

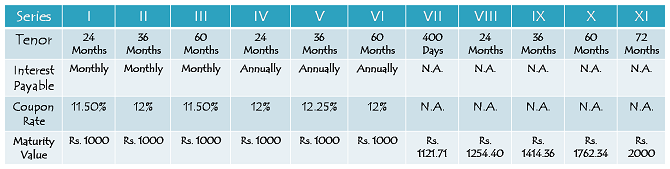

Coupon Rates – Muthoot has not made any changes to its interest rates and not even the variety of maturity periods. Once again it has eleven interest payment options – monthly, annually and cumulative. Like it did in its earlier issues as well, the company offers to double your investment amount in 6 years’ time i.e. 72 months with an effective yield of 12.25% per annum. Again, NCDs issued under this option are ‘Unsecured’ in nature.

The company will offer interest rates ranging from 11% to 12.25% with different maturity periods and different interest payment options. The table below has all these rates:

Coupon Rates for the Institutional Investors – I would call this issue to be a follow-on offer of NCDs by Muthoot. The company has decided to offer the same lower rate of interest to the institutional investors which they got offered last time. They will get coupon rates which would be lower by 75 basis points (or 0.75%) across all the options, except option VII. The difference is of 0.25% in this option.

Ratings & Nature of NCDs – CRISIL and ICRA are the two rating agencies which have rated this issue. Both have assigned ‘AA-/Negative’ rating to this issue. All these NCDs would be ‘Secured’ in nature, except NCDs issued under option XI which offer to double your money in six years.

Demat/Physical Option, TDS & Listing – Investors have the option to apply these NCDs in physical form as well as demat form with options I to VI. Applicants will be allotted these NCDs only in demat form if they go for options VII to XI i.e. you cannot apply for these NCDs in physical form under options VII to XI.

As you know these NCDs are taxable as per the tax slab of the investor, TDS will be applicable if the interest amount exceeds Rs. 5,000 in a financial year. As always, NCDs taken in demat form will not attract any TDS on the interest income. Also, these NCDs will get listed only on the Bombay Stock Exchange (BSE).

Minimum Investment – Minimum investment has been kept at Rs. 10,000 i.e. 10 bonds of Rs. 1,000 face value.

Categories of Investors & Allocation Ratio – The investors have been classified in the following three categories and the change in the allocation ratio in this issue is the only noticeable change I have observed as compared to the last issue.

Category I – Institutional Investors – 5% of the issue is reserved

Category II – Non-Institutional Investors, Corporates – 5% of the issue is reserved

Category III – Retail Individual Investors including HUFs – 90% of the issue is reserved

Muthoot’s last issue in November got a very poor response from the institutional investors and that is probably the biggest reason why the company has decided to increase the allocation ratio for the retail individual investors.

NRI Investment – Similar to its previous issues, non-resident Indians (NRIs) are not allowed to invest in this issue as well.

Liquidity is a major issue with these kind of NCD issues. Though these NCDs get listed on the stock exchanges, people don’t easily find buyers for them.

Gold prices have been witnessing sharper cuts in the international markets in the last 15-20 days and as the US economy improves further from here, they are expected to go down further.

Also, as the current account deficit (CAD) has been under control here in India in the past 2-3 months, there is a talk going on in the markets that the Indian government will soon reduce the import duties on Gold. This will result in a fall in gold’s domestic prices, which I think will not be a good news for Muthoot.

Interest rates are again ruling at multi-year highs. In the current scenario in which the investors have options like tax-free bonds yielding 9%+, I wonder why investors go for these NCDs. I still think these bonds are not bought by the investors, rather they get sold by the agents or brokers to their customers.

Application Form of Muthoot NCDs

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in Muthoot NCDs, you can contact me at +919811797407

Dear Mr. Shiv,

I read your articles and found interesting.I am a senior citizen.I lost most of my savings in share (equity)market. If I would have kept in my saving a/c at % I would have earned.

Now lot of NCD issues and come and currently running.I prefer monthly /quarterly interest issues like pensions.Are Mannapuram/Muthut finance safe to buy from market?Are they pay interest regularly?

Kindly advice me on this line.

Dear Mr. Shah,

I would say, for a senior investor like you, it is better to avoid such NCDs from the issuers like Muthoot, Manappuram etc. I don’t know which tax bracket you fall in , but you should rather invest in tax free bonds or other safer instruments like post office schemes, debt mutual funds or bank FDs. As far as stock market returns are concerned, I think most of the retail investors invest at a wrong time and that is why they lose their hard earned money in equities.

Dear Shiv, There are two other NCD’s due to launch this month (Manappuram Finance and SREI Infra), Can you compare them all in a post please?

Also Muthood and Manappuram Finance focus on same business.

Dear Nagendra,

I’ll cover Manappuram NCD issue and SREI Infra NCD issue in the next 2-3 days. I’ll do the comparative analysis in the post itself.

Hi Shiv,

Are you going to do any post on SREI NCD issue opening on 30th December?

Thanks

Hi Ikjot,

I need to cover three bond issues in three days – IRFC tax-free bonds, Manappuram NCD issue and SREI Infra NCD issue. Let’s see how I do that.

You are doing great service Shiv and I wish you all the best.

Thanks a lot Ikjot for your wishes !! But, not all people share the same views as you have. People want to blame me for misguiding readers here. 🙂

To be honest since I have started reading your posts always found them to be genuinely honest and in the best interest of the investors. Though there will always come people who deliberately will try to put you down , the leg-pullers that they are. Maybe because they are jealous of the success your website is enjoying but it’s all due to your hard work and honest commitment. I would say only one thing ‘Keep calm and carry on’ …you are doing fantastic work…All the best once again.

You are right, thanks for these confidence boosters !! Thanks !!

I think the frequency at which these NCD are invited may create suspicion. I think this is the siplest way to pay out their earlier investor. SEBI should come out with hard rule and regulation . One company should not be allowed to invite multiple NCD in a year , maximum one in three years

Though it is a noble idea, but then no company with genuine requirements will be able to access the capital markets.

To whole onemint team,

I recently subscribed to this blog. You are doing a wonderful job friends. All posts written from the eye of the common small investor with full knowledge and expertise of the upper level.

I will try to be interactive reader on this blog.

Thanks all.

Thanks a lot Kalpesh for your kind and motivating words !!

Thanks a lot Shiv for the excellent advice on this website.I wonder how people (like you) spend time on writing articles for free on an unbiased and easy to understand way. :)-

Thanks a lot Ankit for your kind words !! 🙂

The reasons you have mentioned at the end of the post keep us away from this bonds. I think middle class people should not invest their hard earned money just because of the promise that it would become double in 6 years. Alas! They are the first ones who get attracted by these words. One can invest in this who has the ability to take extra risk.

Hi Uday,

You are right in your assessment Uday! I would say these kind of NCDs are not bought by the investors, they are actually sold (I would call it mis-sold) to them by their agents (or so called investment advisors or RMs). These are riskier investments and just for 1-2% extra returns, risk-averse investors should not subscribe to these bonds.