National Pension System (NPS) – Save Tax u/s 80CCD (1B) worth Rs. 15,450

This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

We all want to save taxes. We all invest to save taxes. Some invest in PPF, some in ELSS, some in NSC, some invest in 5-year bank fixed deposits. But, we all know the maximum investment limit for saving tax under section 80C is Rs. 1,50,000. So, we all want to save more tax, over and above 80C. But, there are only a limited number of investment options which provide tax exemption other than 80C. One of those options is NPS – National Pension System.

Introduced in Budget 2015, your contribution in NPS can save you tax of up to Rs. 15,450, if you are in the highest tax bracket of 30%. NPS provides an additional deduction of Rs. 50,000 from your taxable income. Interested? Read on.

So, let’s start our journey to know more about this tax saving investment avenue and see whether it truly makes sense to invest in it or it is better to pay tax and invest in mutual funds to earn higher tax-free returns.

How to open an NPS account?

Online Account – There are 2 ways to open an NPS account online – one, directly through NPS Trust’s website and two, through an intermediary, like your bank, ICICI Direct, HDFC Securities etc.

Offline Mode – You can also approach a POS (Point of Service) and get this account opened.

Documents Required – PAN card copy, address proof copy, 2 passport-size photographs, investment cheque and Duly Filled Subscriber Registration Form.

Exclusive Tax Benefit u/s 80CCD (1B)

If you decide to invest in NPS, you can avail a tax exemption of Rs. 50,000 from your taxable income. As the minimum investment requirement is Rs. 6,000, you can contribute any amount between Rs. 6,000 and Rs. 50,000 to save tax.

Which Account is eligible for Rs. 50,000 Deduction – Tier I or Tier II? – Your contribution to Tier I account is eligible for up to Rs. 50,000 tax deduction u/s 80CCD (1B). Tier II account does not entitle you to any tax deduction.

Minimum/Maximum Annual Contribution – As per the NPS rules, you need to contribute at least Rs. 6,000 in this account in a financial year. However, you can do so in multiple instalments and minimum contribution in a single contribution is Rs. 500.

However, there is no upper limit on your contribution to NPS. You can contribute any amount to your NPS account. But, as far as tax benefit is concerned, you can have only up to Rs. 50,000 in tax deduction.

Six/Seven Pension Fund Managers – These are the pension fund managers (PFMs) which are managing the subscribers’ money in NPS at present.

- HDFC Pension Management Company

- LIC Pension Fund

- ICICI Prudential Pension Fund

- Kotak Mahindra Pension Fund

- Reliance Pension Fund

- SBI Pension Fund

- UTI Retirement Solutions

Seven Annuity Service Providers – These are the insurance companies which would provide you pension as you retire at 60 years of age.

- Life Insurance Corporation of India (LIC)

- SBI Life Insurance

- ICICI Prudential Life Insurance

- Bajaj Allianz Life Insurance

- Star-Daichi Life Insurance

- Reliance Life Insurance

- HDFC Standard Life Insurance

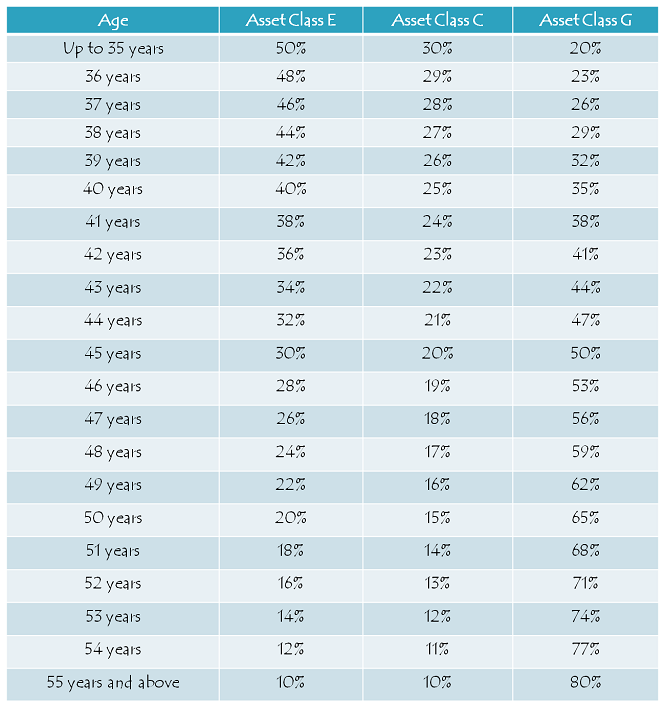

Where your money gets Invested? – Your NPS contribution will get invested in Equity (E), Government Securities (G) or Corporate Debt Securities (C) either as per your own choice (Active Choice) or as per your age (Auto Choice).

Active Choice – Under “Active Choice”, you can have your money invested in these three asset classes as per your own choice. You can allocate your money among these three asset classes (E, G or C), but there is a cap of 50% for Equity (E) investment allocation.

Auto Choice – Under “Auto Choice”, your money gets invested based on your age i.e. the higher your age as the subscriber, the lower would be the allocation for Equity.

Returns – As NPS is completely market driven, there is no guaranteed/defined return in this pension scheme. Returns get accumulated throughout its tenure and get paid as annuity or lump sum benefit on maturity.

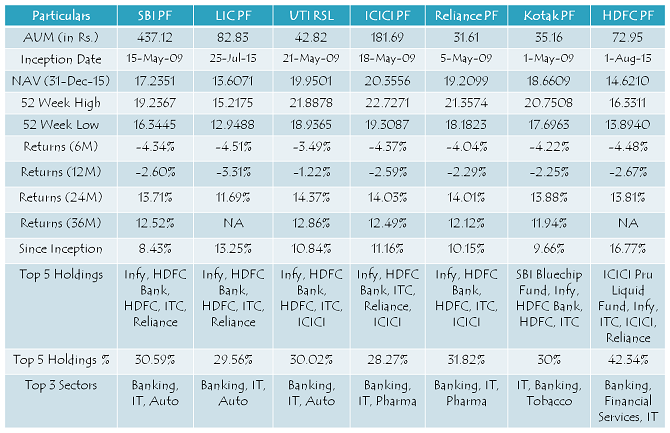

Historical Equity Returns of NPS (Returns as on 31st December, 2015)

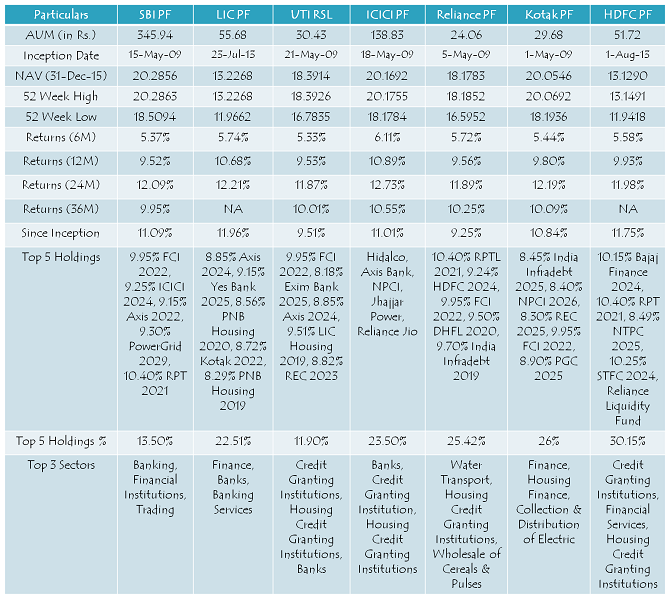

Historical Corporate Debt Returns of NPS (Returns as on 31st December, 2015)

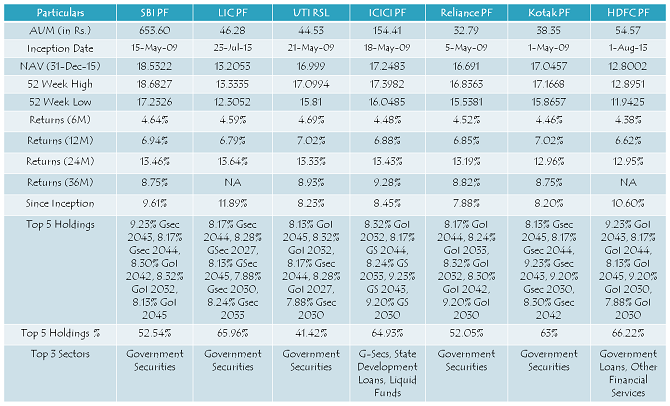

Historical Government Securities Returns of NPS (Returns as on 31st December, 2015)

Charges – This account attracts a processing charge of 0.25% of your contribution amount, subject to a minimum charge of Rs. 20, plus service tax as applicable. So, if you contribute Rs. 6,000, then Rs. 20 + service tax will be the charges. In case your contribution is Rs. 50,000, then a charge of Rs. 125 + service tax will be deducted from your account.

Exit – As you turn 60, you will be required to use at least 40% (maximum 100%) of your accumulated savings to buy a life annuity from an insurance company. Rest 60% or less, you can withdraw as lump sum amount. If you decide to exit before 60 years of age, you will have to buy an annuity with 80% of your accumulated savings, rest 20% amount you can withdraw as the lump sum benefit. Both, annuity income as well as the lump sum withdrawal, will be taxable.

In case of death before 60 years of age, entire pension corpus will be paid to the nominee of the subscriber.

Should you invest in NPS?

Please check this post – Should you invest in NPS Post Budget 2016?

Also, if you think I have missed to cover any important aspect(s) of NPS, then please share it here, I’ll try to include it in the post above.

Thanks for the new post.

Many of us are aware of the benefits of NPS but their service is very poor if not disaster which dissuades public at large. I filled up online application on http://www.enps.nsdl.com. At the time of payment, gateway did not work, It has been five days now and still I cannot make payment. Nothing works – Query on email, facebook, their toll free number, their landline number. Nothing Works. They are non-contactable.

Hi Pankaj,

I understand your concern, but we can’t change these things. As service standards here in India are poor, I think most of our public sector activities should be privatised. But, there are many NPS accounts already opened, so if you are facing problems, it is better to get it opened offline and afterwards fund/operate it online.

Pls tell me how to transfer the amount from tier 2 to tier 1 in nps….is it possible through nps app…..Nd after how many days one investment reflects in account….as even after 3 days it doesnt reflect in my account

It is still ok for me that I was not able to make payment. If after payment, something goes wrong, then ……………..

The form you have included in the link is old form and is no longer accepted by banks. You have to fill in the new form. I gave my old form and after a month the bank told me that my form has been returned because it is a old form. I have to give them now new form.

Thanks Amd for pointing it out, I have replaced it with the new one.

The last part of buying a life annuity makes this very unappealing.Also is interest taxable?

Yes Harinee, annuity income is taxable as per the current tax rules. But, as it is a pension plan, I think annuity payments should be accepted as a fundamental feature of this scheme. But, if the government decides to make it flexible, it would be a welcome move.

Can we invest in tier1 by mobile app..to get additional tax rebate f 50000.

Waiting for your analysis on to go with it or not. Please provide your analysis at the earliest.

Thanks

Hi Shiv,

Thanks for the very informative post, as always.

Could you please address the following questions:

– Is the taxation applicable on the entire corpus or just the capital gains? If it is prior, then this is just a case of deferred taxation.

– Is taxation only at the end, and as per the tax bracket or at any special rate?

– In what range does the RoR from an annuity plan typically fall?

– Is the annuity corpus returned to the nominee after death?

– Finally, what are your thoughts on annuity RoR 25-30 years from now?

Overall I don’t find this as a very attractive proposition due to following reasons:

– Taxation

– Annuity condition

– Equity maxed to 50%

A quick back-of-the-envelope calculation shows that if a 35 year old invests 50,000 per year in equity until he’s 60, and the tax-free corpus builds to 2 crore, the IRR is 17.9%. Alternatively, if he invests 35,000 each year (considering 15,000 tax benefit of 80CCD) in NPS, and the corpus builds to 2 crore, which becomes 1.43 crore post taxation (assuming 30% tax rate on the capital gains), the IRR is only marginally higher equal to 18.0%.

Your thoughts are welcome.

Thanks,

PP

Thanks PP,

1. Yes, it is a case of deferred taxation, both annuity income as well as lump sum withdrawal are taxable.

2. Lump sum withdrawal would be considered as capital gain and annuity income would be treated as regular income and would be taxed accordingly.

3. Historical returns are mentioned in the tables above.

4. Yes, corpus amount is payable to the nominee after the subscriber’s death.

5. As India grows, I think return should be in the range of 3-6% 25-30 years down the line.

6. Your reasons for not liking this scheme are genuine, but to be fair, I think we expect too much from the government and ultimately everything gets spoilt a few years down the line.

7. I’ll respond to your calculations soon.

Dear Shiv – Got a doubt about my own (employee) contribution. As part of my CTC, I’ve allocated INR 1,000 per month which comes under Employer Contribution to NPS. Aligning with this, I’ve got my PRAN no and getting the annual account statements. But if I want to get my own investment benefit (under employee contribution), do I need to create one more NPS or can I continue to invest on the same existing one. It’ll be great, if you kindly provide a clarity on this regard.

Hi Rajaram,

You are not required/allowed to open another NPS account to get tax benefit u/s 80CCD (1B). You can make your own contributions in the same account and avail tax benefits.

Are return tax free, also is it advisable to lock the amt till the age of 60

Hi Sahil,

Annuity income and lump sum withdrawal, both are taxable. It is what you need to decide whether you want to stay invested in such a scheme or not which matures as your turn 60.

Hi- i understand that the returns on maturity (at age 60) are taxable. However, for people who will be retired at 60 and may not have significant income at age 60, the lumpsum returns may not fall in the taxable range. Is this understanding correct?

Can v have one mint app…jus a suggestion..

Never thought about it Krunal, but any special benefit of having an app?

Many benefits. You can be in everyone’s mobile.

you can send notification to them whenever you like, or whenever you post new article.

You can directly get in touch in real time as you can have an option to have their email id / number as login credentials.

HI

I had filled up online aplication at eNPS. After failed transaction( due to mistake on my part), it took 5 working days for payment gateway to reset. And then I was able to do the payment transaction at eNPS. After Payment by netbanking,PRAN number was automatically generated. Now KYC will be done online automatic by my bank without my intervenion (Hope So).

Also I will have to send print out of online application after affixing photo and signature to Mumbai.

Thanks Pankaj for sharing this info!

I think there is no case to invest in the NPS if entire amount [that is my principal too] is taxed at withdrawal. Typically only the earnings over and above my contributions should be taxed else I think the outgo in the form of tax will be much higher at withdrawal – especially when [at withdrawal] is when you need your money most.

Comments?

Heard that govt is planning to bring NPS under EEE. May be in this budget.

What do you mean by EEE?

See link

http://www.businesstoday.in/moneytoday/cover-story/direct-taxes-code-national-pension-scheme-tax-benefits/story/190167.html

NPS requires you to compulsorily purchase an annuity so that you get some money in lump sum and the balance in annuity. Broadly, the lump sum and annuity are both taxable under the I-T Act as NPS follows an Exempt-Exempt-Taxable (EET) concept.

Under the proposed Direct Taxes Code (DTC), NPS will be covered under the Exempt-Exempt-Exempt (EEE) regime, wherein the investor will enjoy tax benefits when contributions are made.

The accumulations to the fund will continue to be taxfree; withdrawals from the fund are proposed to be exempt.

However, there is confusion if along with lump-sum withdrawal, earning from annuity (which is mandatory under NPS) will also be tax-free.

Budget 2016 has made a portion of NPS withdrawal tax exempt, so it is a relief for the subscribers to an extent. Moreover, if you invest the remaining 60% for buying annuity, it is completely tax exempt.

Pls compare balanced funds of Mutual funds Vs NPS – I understand balance funds of Mutual funds also follow similar kind of investment pattern like NPS – but in mutual funds – withdrawal will be tax free and at NPS -we have to pay tax – pls advise

In NPS additional 50000 is available for tax deduction under 80CCB and commission is also very less.

Thanks for sharing valuable information, indeed analysis.

Regards,

http://www.expertmile.com

Hi To get I-PIN number to check NPS balance? PRAN number is recently issued.

You should get it by post.

Or try CRA helpline 1800 222 080.

or lodge complaint online https://cra-nsdl.com/CRA/cgmsMenuOnloadForSub.do

or email at [email protected]

or contact your POP

You may get delayed reply. but der hai, andher nahi.

You can below link to reset your Ipin

https://cra-nsdl.com/CRA/raisePasswordSubscriber.do?ID=null&getName=Change%20Password

Or try CRA helpline 1800 222 080.

or lodge complaint online https://cra-nsdl.com/CRA/cgmsMenuOnloadForSub.do

or email at [email protected]

or contact your POP

You may get delayed reply. but der hai, andher nahi.

I want to get circular or GO regarding tax benifits U/s 80CCD for NPS contribution.

Waiting for your analysis on to go with it or not. Please provide your analysis at the earliest.

Hi Vincent,

Here you have the link to my analysis covering NPS post Budget 2016 – https://www.onemint.com/2016/03/25/post-budget-2016-should-you-invest-in-nps/

dear shiv

what will be the tax on corpus amount payable to the nominee after the subscriber’s death.if it is tax free then it means that although the annuity income is taxable,but the purchase price will be tax free..

Hi Dr. Puneet,

The entire corpus is tax-free for the nominee in case of the subscriber’s death.

Can I invest 50000 in one go – lumpsum in NPS in the last month and get the additional tax benefit under 80cccd. I have not yet opened a account and plan to do it now. With only one month to go, I would like to invest the max 50K in one installment instead of monthly deduction now. Will it get the tax benefits..?

You are correct. Now there is no time. You should invest in one go. After submitting of all docs, considerable time is spent on opening NPS account. But initial subscription given will be considered.

Yes Prathamesh, you’ll get the tax benefit u/s 80CCD (1B).

Lic rs 80000 tuition fee rs40000. nps 10% contributions 40000 can I get benefit of rs 80 ccd(1b) for rs 10000 my self Lalchand mob.9813935300 ,9813935342

dear sir,i am a govt doctor.i have deposited 1,50,000-00 in PPf and my PRAN contribution is Rs 76000 in F.Y.2015-16.please tell me can i avail Rs 50000 rebate u/s 800=CCD(1B) or i have to pay extra Rs 50,000-00 in Tier 1 account

If u have made 76000 contribution, it will be most prabably in tier 1 account. If it is, 50000 is eligible for 80CCD1B

Dear Sir,

Please clarify my doubts stated below.

1. I am serving in GOI sector and have my own PRAN account. Regarding tax benefit, how do I make sure that the deposited amount (Rs 50,000) goes under 80CCD(1B)? I could not find any column assuring the to-be-deposited Rs 50,000 as covered under 80CCD(1B).

2. I do not have Internet Banking facility. Can the payment be made using others’ bank account, using my PRAN?

Hi Ramesh,

1. If you are contributing to your Tier I account, then you’ll get Rs. 50,000 tax deduction.

2. You need to contact NPS for clarification regarding third party payment.

plz tell me the procedure of nps investing

also the benefits time to time

Hi Abhishek,

Please check this link for eNPS investment – https://www.onemint.com/2016/03/28/how-to-invest-in-nps-online-enps/

Very clear concept you have shown. I am very much impressed. Thanks for this much of information. I too was little bit confused that if I had invested under section 80C of income tax rebate schemes of other than NPS(tier-1) like LIC, PPF, ELSS, Bank FD of 5years etc. and Rs. 150000/- investment is already completed then on 1st contribution of Rs. 50000/- in NPS tier-1 account; whether I would be eligible under section 80CCD(1B) of income tax or not for additional tax rebate.

Thanks Rajiv for your kind words!

Dear sir,

As I am an LIC agent , is it possible to give NPS to my customer.

If possible , please let me process and other details .

Thanks in advance,

Hi Usha,

You need to contact PFRDA or NSDL for the same – https://www.npscra.nsdl.co.in/contact-us.php

Hi Shiv, I want to ask the following questions. please take pain to answer.

I am a bank employee.

1. Does both the employee and employer contribution to NPS comes under the 1.5 lakh saving limit.

2. If the 1.5 lakh saving limit is already achieved (excluding NPS) does the employee contribution to NPS falls into the extra saving of 50,000 in 80CCD.

Hi Deepak,

1. NPS contribution does not fall under 80C. It is over and above Rs. 1.50 lakh tax exemption.

2. If you are making contributions in your Tier I account, then you can avail tax deduction of Rs. 50,000 u/s 80CCD (1B), over and above Rs. 1.50 lakh tax deduction u/s 80C.

I am still not clear. My PF, housing loan principal and insurance is sufficiently covers 1.5L of 80C. Now If I make contribution of 50k in tier 1 account and my employer makes contribution of 10% of basic +DA then will my contribution get into 80CCD benefit for 50k and so will employer? Will both be exempted from tax?

Hi Shiv,

I am a govt. Teacher. I have deposited rs. 150000 in ppf and an amount of rs. 51000 has been deducted from salary by my employer through NPS tier 1 account which is 10% of my basic and da. Am I eligible to have benefit of 80 cccd 1b or I’ll have to deposit more under NPS. PLZ clarify….

See, whatever you invest in nps, only Rs.50000 is eligible for 80ccd(1B) over and above Rs.150000 u/s 80c. So, as per me its not beneficial to invest more as far as the income tax rebate is concerned. Also, it doesn’t matter how the money has been deposited; it’s a permanent retirement account number provided by the government where your money is going to deposit. You need not to worry about its eligibility at all. Thanks.

Hi Divyendu,

Your employer’s contribution will provide you tax deduction u/s 80CCD (2). For tax deduction u/s 80CCD (1B), you need to contribute up to Rs. 50,000 yourself from your taxable income.

Sir

I have same query?? What’s you finally understand about that? Please tell me your suggestion about all that.

Hey shiv,

Please resolve this. My employer and I both contribute approx 20000 in my current pension and pf account each. I would like to invest in NPS a sum of Rs. 50000 would I have to open a new account??

Hi Krishan,

It is not allowed to open two NPS accounts. You can contribute up to Rs. 50,000 to your existing NPS account and claim tax deduction u/s 80CCD (1B).

Please advise the maximum age limit for the investor.for investing RS. 50,000/ per year.

I am 75+ can I invest to avail the benefit 150,000 + 50,000.for inome tax benefit.

Hi Mr. Nagee,

NPS investment can be made only up to 60 years of age. You cannot make NPS investment.

I am a state government servant and have my pran number and active tier 1 account . How I can invest 50000rs in NPS. Thanks

Hi Pankaj,

Just contribute to your existing Tier I account from your taxable income and you can claim tax deduction u/s 80CCD (1B) – https://enps.nsdl.com/eNPS/InitialExistingUser.html

Hi shiv

As you had mentioned that you are working on if one should invest in the same or not and will be updated soon. I couldn’t trace that part, is it already updated, or yet to be updated

Jinay

Hi Jinay,

Here you have the link to my NPS analysis – https://www.onemint.com/2016/03/25/post-budget-2016-should-you-invest-in-nps/

Hi Shiv,

Thanks for this post. I dont see it as a viable option for investment as both annuity and withdrawals are taxable.

Why do they tax annuities. I hope they change it somewhere in the upcoming Budgets/.

Thanks Amardeep!

Withdrawals are not taxable if you buy annuity from the taxable portion of NPS corpus. So, only annuity is taxable. Let’s see if they make any further changes in future.

If 14.5% service tax + .25% transaction charge ie a total of approximately 7,000/_is deducted if we invest 50,000/_ then what is the benefit of investment?

That is what you need to decide Amol whether it is beneficial or not!

I think this calculation is crystal clear.

Formula is given below:

Let your own NPS contribution is X

Case1: X >= Rs.50,000/-

a) First you set aside from X, Rs.50,000/- for 80CCD(1B)

b) Rest amount i.e., (X – 50,000)* will be added to your 80C block under Rs.1,50,000/- (Tot Sec 80E)

* minimum of (X-50,000) or 10% of your (pay+Grade Pay+da) would be considered for addition to 80C block. It may happen when you pay more NPS in Tier I

Case2: X < 50,000

only X amount will be set aside for 80CCD(1B)

No NPS amount is available for section 80C i.e., in Max Rs.1,50,000/- block

He will get benefit= + X only in 80ccd(1b)

You can refer page 33 of circular by income-tax dept, govt of India. Below is the URL. Hope you got it.

Thanks.

http://incometaxindia.gov.in/communications/circular/circular20_2015.pdf

Regards,

rajiv

Based on above, this example illustrates the thing well. Say, for the salaried income of an employee of CENTRAL GOVT. The following are the tentative Income and savings detail for the A.Y. 2016-17:

1. Gross Income: 950000/-

2. Savings:

a) PPF: 1,50,000/-

b) NPS (own share): 74696/- (within 10% limit of total salary)

c) NPS (employer share): 74696/- (within 10% limit of total salary)

He can claim deductions as per the following details:

1. u/s 80C: 1,50,000/-

2. u/s 80CCD(1B): 50,000/- (from the amount invested in NPS, own share)

3. u/s 80CCD(2): 74696/-

4. Total deduction: 2,74696/-

So, the taxable income remains = 675304/-.

Please respond if it helped you. I myself studied for a week to clarify. Thanks

Thanks Rajiv for posting this example, it would really help the investors!

Just Posted – Should You Invest in NPS Post Budget 2016? – https://www.onemint.com/2016/03/25/post-budget-2016-should-you-invest-in-nps/

Hello Shiv,

Thanks for your wonderful about investing on NPS.

I know its only 3 days to go. Can i successfully subscribe and get the account opened before 31st of this month through eNPS. i have my aadhar card with correct address details.

If this whole process takes more than 4 days, then its no point in trying it out.. isnt it?

Thanks,

Chandan

Thanks Chandan!

Yes, you can invest in NPS today itself. Just check this post – https://www.onemint.com/2016/03/28/how-to-invest-in-nps-online-enps/

Thanks Shiv,

Have a question for you:

i just successfully opened the NPS account with both tier 1 and 2 options.

i had made an initial contribution of 1k each to above 2 accounts.

Now i want to make a contribution of 49k for tier 1 for tax benefits.

if i select contribution section and enter my PRAN and DOB, its showing invalid entries. i dont if there is a lead time in getting my new PRAN authenticated in their system or will it happen only after i submit the hardcopy of the registered form?.

Hi Chandan,

I am not 100% sure why this is happening, probably you are right that it is taking a lead time to get your details authenticated. It would be better if you could contact their customer care support for it. Please share their response and your experience dealing with them.

Thanks Shiv.

I did send an email on the same to [email protected] which got bounced saying. this mailbox is full and rejected my email. :-). look at the plight of their customer support.

Yeah, I know. It is everywhere like this here in India. Please try their customer care no. once.

Hello Shiv,

contribution option can be logged in successfully after 3 hours of getting the PRAN account.

i did it but couldnt make any payment as the payment gateway for both credit and debit card were unsuccessful.

netbanking is not possible with private banks like icici, hdfc or scb.

Keep trying, you’ll get success! 🙂

First contribution is possible only with the netbanking of the bank whose details you have given while registering on eNPS.

Subsequent contribution can be from any netbanking/ credit or debit card.

Thanks Pankaj for this info!

My husband is a school teacher and in his school they have to submit saving details in the month of february after that clerk is not accepting changes, if he open tier 1 account in a day or two can he mentioned in his return this saving because form 16 will show different calculation.

Hi Apoorva,

That is not a problem. He can still claim deduction u/s 80CCD (1B) while filing his tax return after March 31, 2016.

Hi Shiv ,

One query , 50 K amount invested from now till 31st March can be claimed in ITR AY 2016-2017 . I hope this is right . Also I would say one part is taxation on 60 % of annuity amount should also be considered , which mean . If the corpus is Rs 100 at 60 years of age , person can withdraw Rs 40 as Tax free, and remaining Rs 60 (40% is taxable in case if he want to withdraw, and rest 60% Annuity mandatory) . So Suppose Rs 100 is corpus and person is in 30 percent bracket , then he can withdraw 40+(40 percent of Rs 60) *.7o % . rest in annuity

Hi Gaurav,

Out of Rs. 100, 40% lump sum withdrawal is tax-free. Also, it is mandatory to put Rs. 40 for annuity, so this Rs. 40 is also tax free. The remaining Rs. 20 is taxable if withdrawn as a lump sum amount. If this Rs. 20 is also invested to buy annuity, then 100% corpus is tax-free. Only annuity income is taxable.

Can you explain ‘Exit’ in layman’s language? I just couldn’t get words like annuity and all. What exactly will happen at the retirement?

Or, what can I get if I decide to get before retirement?

If I have a basic salary of 25K per month i.e. 3 Lac per annum, then can I claim a tax exemption of 50K under section 80CCD(1b)? Is the contribution under this section also capped by the formula ‘10% of Basic + DA’ (which is 30K in my case)?

Hello,

I did transaction in NPS on 30 March and my unit got purchased on 4th april.

Am i able to have tax benefit on this amount.

As on transaction detail of month march i am not seeing contribution done on 30th march.

Even I did transaction on 30th March but it is showing 30th march only as the transaction date.

i made transaction from enps site .. and by using SBI online..

have you done the same…

Actually i have received one male from cra which says statement of account for march and in that statement i am not seeing that entry .. are you able to see your entry there

I did transaction on eNPS using IDBI netbanking. Today I recieved monthly transaction statement on my email ID and I can see my entry. Try to see your holding statement at https://cra-nsdl.com/CRA/

and log in using your PRAN no. If you do not have password “Ipin”, you can generate online using forget password option. Then try to see holding statement online.

Thanks Shiv for the article.

I am employed in a private company and according to the rules upto 10% of my basic I have declared to contribute to my PRAN directly from my salary . Now this 10% amount comes to be say 30K per annum . I have 20K window more to invest and I have already invested 1.5 L/A under 80C. In this case where this 30K I can show ?

Can I invest 20K more under 80ccd(1b) directly from my account without consulting employeer as I have already reached the limit of 10% of basic ?

Please help me regarding this .

Even in my case the PRAN is generated on 25th Mar 2016. However the units are allocated only on 4th april. I had sent the cheque along with application form.

Not sure whether i will get Tax benefit as the units allocated only on 4th april as per the statement. Pls clarify

Rgds

Anil

Dear Sir

Thanks for information of NPS , from where we will get the best return,

I am in private sector

Regards

Rajesh

Dear Sir,

Post retirement (Age 60), what is taxable.

a) Whole Corpus (Principle + Interest)

b) Only Interest.

As per my understanding whole corpus (a) is taxable.

But how can my invested amount be taxable?? Ideally taxes should be levied on interest, as in case of FD..

I joined the scheme when I was 58 and retired at 59 years. I was informed that post retirement if your corpus value is less than 2 lakhs there wont be any tax deduction, and you can claim the whole amount. Request Mr. Shiv to kindly add his valuable comments on the same.

Dear Shiv, could you please describe the details about u/s80ccd(2) & u/s80cce for NPS.

Sir i m a government servent and i have investment of 150000 under section 80c, ie, LIC,PLI,PPF etc. and 50000 in 80 ccd-1b in nps through treasury in tier 1 account.is it valid? How can i show my form 16?

I am in HP govt service. From 1998 to 2007 I was under contact and regularized since 2008 and covered under NPS scheme. In the AY 2016-17 I have invested Rs.150000/- in PPF, insurance etc except my share in NPS Rs.60000/- Now I want to claim Rs.50000/- u/s 80CCD(1B) but my employer has refused to claim this deduction and issued me Form 16 without considering Rs.50000/- u/s 80CCD(1B). Please clarify if I could get deduction u/s 80CCD(1B) at the time of filing my return.

If one has resigned from a company and is on a 1 year sabbatical, should he /she continue investing in National Pension Scheme to keep it active?

Are there any benefits? And is there some minimal amount per year (or per month) that an NPS account holder should continue to invest (much like PPF?

Kindly clarify the situation and provisions for such an individual who has still not attained retirement age of 58 years.

Dear sir,

Regarding NPS as govt.declared add. 50000 investing in Nps but I m PSU employee and Omg contribution already deducted every month in Nps and near about 45000 now amount contributed. Can I claim this is the New tax benifit as declared by gov. Or I can invest another 50000 for get the tax benefit other than80c? If the amout contributed every month consider as this tax benefits than I can this invest ment not consider in 80c.

hello sir

My name is sanjay and i am a govt. servant and Govt. deduct Rs.50,000 annually from my salary as NPS. Also it contribute Rs.50,000/- towards my NPS as employer’s share. Now i want to know whether i am eligible for tax rebate on Rs.50,000/- under section 80 CCD (1B).

thanks in advance.

Sir i am cg employee. I have LIC+Housing loan principal repayment+ tax saver MF = savings More than 1.5Lakhs, my contribution to NPS is 72,000 into tier- 1 which is 10% of my salary. Can i claim 50,000 under 80ccd 1b or not? Please inform me.

Sir i am cg employee. I have LIC+Housing loan principal repayment+ tax saver MF = savings More than 1.5Lakhs, my contribution to NPS is 72,000 into tier- 1 which is 10% of my salary. Can i claim 50,000 under 80ccd 1b or not? Please inform me.

Dear Sir

I have come to know about NPS contribution only now. can I contribute now and claim the same in the income tax return before this July 30th? Please tell me fast…

Dr. Prasad Pannian

Hi, If i claim employers contribution in NPS to 80CCD(2), do i need to include employers contribution in my gross salary also or gross salary will be excluding employers contribution.

example-(hypothetical)

my gross salary- 8lac(gross salary from my salary slips)

my NPS contribution- 60K

Government NPS contribution-60K

Than i claim 80 CCD(2)

my gross salary will be 8lac or 8.6 lac????????

Does NPS contribution by self comes under 1.5 Lac limit describe under 80c or it is above this…??

Hello sir, is there any benefit of pqyment gateway charges – 0.80% and service tax 15% so when I deposit amount that charges are debited in my amount. So there are any benefits for this service tax charges.?

Dear Sir

I have a NPS account and i am a PSU employee. My husband contributed additional 50000 in my NPS account from his salary account. I Just want to know whether my husband can claim deduction under 80ccd(IB) for contribution made in my NPS account through his account.

Sir i am teacher in delhi college. I have LIC+Housing loan principal repayment+ tax saver MF = savings More than 1.5Lakhs, my contribution to NPS is 140000 into tier- 1 which is 10% of my salary. Can i claim 50,000 under 80ccd 1b or not? Please inform me.

Dear shiv,

Thanks for the informative article. However, still not clear on one aspect:

My employer deducted 10% of basic salary every month and deposited with NPS. In addition, I deposited Rs 50,000 to NPS which is eligible for 80 CCD (1) and 80 CCD(1B). However, please tell me under what head do I claim benefit for 10% of salary deduction which my employer deposited with NPS every month. Please note that this is part of my CTC and hence my contribution and not employer’s contribution. Can I claim this under 80CCD(2) – Employer Contribution in NPS? Thanks in advance.

Please help to clarify taxation on withdrawl of Tier 2 corpus.

Also clarify if there is any lock-in in tier 2.

Hello sir,

I am working in Judicial Department in Gujarat, and now i have been selected in the U.P. services, will i be required to close my current NPS account which i just opened 7 months back. Additionally, I invest in PPF account to the tune of 1.5 Lakhs, what is the additional tax benefit that i am entitled to through NPS investment.

thank you.

Hello Sir,

I have a question… Assume below case :

My 80 C Investment = 1,50,000 ;

Thus, Tax Deduction under 80C (including 80CCD (1)) = 1,50,000.

My 80 CCD(1B) NPS Investment = 80,000 ;

Thus Tax Deduction under 80 CCD(1B) = 50,000.

What is Tax implication to the remaining Rs 30,000 in NPS ?

Are the returns on that Rs.30,000 taxable. Or it remains invested in the account and Tax is Applicable at the Time of Corpus Withdrawal (Pre-Retirement or Post-Retirement).

Pl. Clarify.

KVP

i shall be 60 years old in Feb.2017.Ihave opened my NPS tier 1 account in January 2016 and deposited 50000 rupees and have claimed tax benefit under 80 CCD(1b)for financial year 2015-16 and again depositd 50000 rupees in August 2016 for claiming tax benefit under 80CCD(1b) for Financial year 2016-17. My NPS accont will mature in Feb2017 as i will be 60 years old in Feb. 2017.

My Question-

1- My date of retirement from service is on Feb 2022 after achieving 65 Years

age. My NPS account will mature in Feb 2017 as mentioned above while my

retirement is Feb2022. Will i be eligible for 40% Tax exemp on NPS corpus withdrawl from on closure 0f my NPS account in Feb 2017 as i will become 60 years old. I have opened the account under All citizen- non government account. Please Reply

I have invest 666665Rs in LIC pension last year after retirement 60year . I am getting pensionRs5000/month. Pension money can be calculate in income? If yes how much can be exampted &in which code. Post pension also I am getting RS6300 /month . so please advise me.

sir I m a central government employee and not covered under nps. now i started investing in nps at my own in tier i. will i be eligible for additional deduction of Rs. 50000 under 80 CCiB

Sir,

I have deposited 50000 in her NPS from my bank account. Who is entitled for deduction? Myself / Wife / or any one of us.

I am bit confused , please clarify, if I had invested under section 80C of income tax rebate schemes of other than NPS(tier-1) like LIC, PPF, ELSS,SSA etc. and Rs. 150000/- investment is already completed then on 1st contribution of Rs. 50000/- in NPS tier-1 account; whether I would be eligible additional tax rebate for Rs.50000/-.??

please advice

While creating NPS accont online thru e-NPS and at the time of first contribution – online payment link got failed and it could not be succeed first contribution. Then it was retried thru Registration but unable to do the same as registration process was over, but PRAN number could not be generated.

Pl suggest what to do for making first contribution and generating PRAN number ?

I do have an NPS account for which the employer is contributing for NPS (i.e., 10% of Basic) under 80CCD(2) Employer NPS. Am I eligible for additional Rs. 50,000/- under Sec80CCD (Deductions under Chapter VI-A). If so, how do I contribute into my current NPS a/c to get the income tax benefit for the additional Rs. 50,000/- contribution under Sec80CCD. Thanks

my question is RS 12500 deduct GPF from my salary , i can invest 50000 in NPS and that amount i can claim in income tax rebate

Can we avail tax benefit under section 80CCD, if the account / registration/ investment is opened in the name of wife/spouse.

I want to invest 25000 this year and 35000 next year, then 20000 next year. Is it possible for NPS SCHEME.

I am a state govt. employee having GPF account. I have joined my service in March 1991. Now can i invest Rs. 50,000/- in NPS account to get IT relief through 80 ccd 1(b) after my investment of Rs. 1.5 lac in 80C .

I am 60 years old, can I invest in 80ccd (1B) ?

Sir, I want to deposit 50, 000 in enps tier I to get rebate under 80ccd. During contribution via enps Voluntary option and tier II are displayed . Is contribution in voluntary and tier I the same as Tier I is not displayed.

Dear Shiv,

Could you please describe the details about u/s80ccd(2) & u/s80cce for NPS.

Also please describe the new ‘Asset Class A’.

Dear Sir

I am 49 Year, Holding LIC JEEVAN NIDHI Pension policy .

Will above policy cover under NPS,

I had already invest 1.5L-80C /13000 – 80D

sir,

while submitting tax return what document to be kept for nps proof ,50000 tax benefit.I already took NPS last year

My date of birth is 9th Feb 1945

Can I join this fund for the benefit of income tax under 80(CCD(1b)

Sir,

I am a Central Government Employee, joined after 01-04-2004, thus falls in NPS. Deduction in Tier-1 account is approx Rs. 65,000/- . If I deposit in PPF a/c Rs. 1,50,000/- then will I be eligible to claim Rs. 50,000/- as deduction in 80CCD(1B) out of that Rs. 65,000/- deposited in Tier-1 account.

Dear Sir,

i am haryana state govt. employee & joined in govt. job in dec. 2008. govt. deduct 10%of (basic+da) from my salary which is around 5200 rs. per month & deposit in my NPS account tier-1 . 1 had invested 150000(one lack fifty thousand) in ppf account in may 2017. pl. guide can i consider nps amount 5200×12=62400 out of which 50000 rs. under 80CCD(1B ) or i have to deposit 50000 additional to take rebate under 80ccd(1b).

Regards

Rajiv Gupta

9416338855

i am bank employee and my own contribution(emloyee contribution) to tier-I is 60000/- which is contribution through my salary and i have invested rs.1.5 lakh in 80cc beside this 60000/-.can i claim tax benefit of rs.50000/- out of this 60000/- under sec 80ccd(1b) or i will have to invest additional 50000/- to avail tax benefit of 50000/- under 80 ccd(1b).please guide me.

i am in state gov job..and 10% of gross salary is already deducted at source to nps account.

i want to deposit more 50000 beyond 1.5lakh savings..

how should i proceed ?

I would like to invest in NPS at the age of 57+.What is my option after 60 years with tax.Kindly explain

Dear Mr. Shiv,

can you please clear, that a private sector employee can open NPS account individually to avail additional benefit Rs.50000/- u/s 80ccd who is already a member of EPF.

I am working as Sr. Manager in a private limited company and also a member of EPF, 12% my contribution and 12% employer contibutes. Now I have consumed 150000/- u/s 80c and 25000 u/s 80D, can I eligible to invest individually in NPS to get additional benefit u/s 80ccd(1), 80ccD(2) and how much should I invest?

please advice

regards

Kuljeet Singh

sir i am bank employee since 1999 having pension option.now my query is that can i open NPS for which i can get income tax deduction under 80 cc(d). please clarify

whether we can transfer money from pnb gmail.comthro net banki

whether we can transfer money from pnb thro net banking as pnb is not included for making payment.

My query is about Swavalamban Scheme

I have read somewhere that contribution has no upper limit

Secondly i am depositing money 12000/- per year from last 3 years, but till date i do not know about the status of my contribution.

I am having PRAN No.

Where do i check the status.

Kindly help me.

How can I know that how much money my nps account have please tell me..

sir, i am a central government employee under nps. I invested 160000 rs ( in ppf, pli and lic), and 110000 in nps which is 10 percentage of my gross salary. Now i want to know that can i avail additional tax benefit of 50000 rs under 80ccd1b in 110000 rs from nps.

please suggest me.

Regards

Dear Sir

My question to you is, I am a teacher in a gov. Added school and there’s a 50000 plus deduction towards nps tire 1. So when i file returns can put this deduction under 80CCD(1) and the reaming 1.5 Lks so total 2Lks.

Kindly guide me about the same

Hello Shiv, Can you please describe the details about u/s80ccd(2) & u/s80cce for NPS.

hi

my query is about wrong entry in my NPS Account.

Actually in my NPS account there was two time entry for same month and it happen for two month. what is procedure to correct it.

ppf 150000.employee contribution 117000. can i take benifit of 50000 of 80ccd 1b

sir my ppf invedtment is 150000.

my employe deduction in nps id 117000.

can i take 200000 lac tax benifit.

i am govt. employee since 2001 & under old pension scheme under GPF. Can open NPS account and avail 50000 rs. rebate in 80ccd(1B). PLEASE CLARIFY.

1. If LIC premium paid by Wife by Cheque and policy under her name. Can Husband claim deduction u/s 80C from his ITR?

2. If LIC premium paid by Wife by CASH and policy under her name. Can Husband claim deduction u/s 80C from his ITR?

Note:- Wife is a House wife or not claim LIC deduction from her ITR.

A person who is covered under old pension scheme may get benefit u/s 80ccd 1b under new pension scheme or not. If yes guide to open new account under NPS and the process of investment.

If any individual opt for NPS and continue the scheme till he/she attends 60 yrs age. After that if individual wish to withdraw the lump sum (60%) amount and rest 40% in annuity, In this case whether the 60% lump sum amount will be taxable at the hand of employee?

How will this help in taxation? and How can I know that how much money my NPS account have?

Kindly help!

Thanks for pointing it out, I have replace it through the new one.