Think of the things that went well for you this year. A rocking birthday celebration, amazing Diwali or Christmas filled with lights, New Year celebration full of fun or the last picnic with friends! The holidays you took with your family & friends were memorable too! So many things happened, and you cherished these memorable moments and events time and again. Amidst all the happy things, did you pay your term insurance premium in time?

If you wish to discontinue your term insurance policy for any reason, you can easily do so, but you are keeping your family’s future at stake while doing so. To maintain coverage, you must continue to pay the premium when due. If you do not do so, the policy will lapse, and your family won’t get the required coverage. Yes, there is no other additional cost, but it is a loss for your loved ones.

What is Term Insurance Lapse?

When you purchase a term insurance policy, you have to pay a certain amount of premium throughout the policy tenure to keep it active. In the insurance terminology, a lapsed policy is that insurance policy for which all the benefits are ceased. For some reasons, if you do not pay the due premium on time, your term plan will lapse. Such situation also arises when the policyholder fails to pay the premium even during the grace period.

How Can You Revive a Lapsed Term Life Insurance Policy?

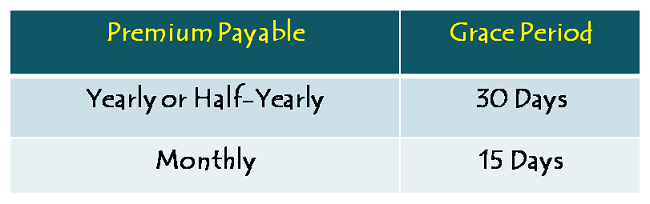

If you have missed the premium payment, your policy will enter into a grace period zone. All term insurers give some grace period to their policyholders to enable them to pay their premiums. For term insurance policies, the grace period can be as follows:

Note, each company has its guidelines, and you should refer to your term insurance document to verify the grace period and other specific rules.

Your term life insurance policy will not lapse if the insurer receives your payment within the grace period. One important point to note is that your lifetime risk is still covered during the grace period. It means, the insurance company is always accountable for paying the sum assured if a valid claim is filed during the grace period.

Let us understand it with the help of an example. Suppose a person fails to pay the premium for a term insurance policy and unfortunately meets with an accident before the grace period ends and loses his life. Now, as the accident has happened within the grace period, the insurance company will have to pay the benefit as and when the family files the claim. However, if the accident occurs after the grace period, the insurer will not pay any benefit to the family.

What Happens After Grace Period?

If you go past the grace period without paying your premium, your term plan will lapse. It means, your beneficiaries will not get any benefit in case of any unfortunate event.

If you decide, you can still apply to revive the policy. If the insurer agrees to reinstate the policy, you will be required to pay the premium due from the end of the grace period. Again, each company has its guidelines for reinstatement.

When a term policy gets lapsed, it can be revived and brought to its full force by payment of the overdue premium (with interest) and a declaration about the current state of health or fresh medical examination. However, a lapsed policy can only be revived if the insurer agrees to do so. Following are the requirements for the reinstatement application:

- Reinstatement Application Form: All companies will ask you to complete a reinstatement application form which is similar to the original application form you filled out at the time of buying the policy.

- Health Statement: It is required to see if anything has changed with your health since your first application, therefore, you will have to submit a health statement.

- New Medical Exam: Most companies won’t require this if you apply for reinstatement within a specified period. But again, it depends on the insurer.

Some Important Points to Note:

All insurance companies advise their customers to pay premiums on time as there is a multitude of premium payment options available. Here are some of the ways through which a policyholder can pay a premium:

- Cheque/DD

- Credit/Debit Card

- Internet Banking

- Wallets, like Paytm

- Wire Transfer

- Phone

A policyholder can issue a standing instruction to his/her bank so that premium gets deducted on a particular date. Further, a policyholder can also visit the insurer’s branch to pay the premium or place a request for a renewal cheque pickup with the insurer.

- Customers can give the mandate to their banks to allow the premium deduction on a specified date

- Insurers have tied up with banks so that their policyholders can pay premiums through their bank accounts. In fact, some banks are allowing people to pay their insurance premiums via ATMs

Don’t Let Your Term Insurance Policy Lapse

It is advised to continue paying the premium until the end of the term so that you can offer financial protection in the form of a sum assured to your family members in case of unexpected events. It is the most necessary backup plan for your life and the one thing that comes to your family’s rescue when life events turn sour.

Further, under Section 80C of the Income Tax Act 1961, any amount paid towards your insurance policy provides you tax deduction upto Rs 1,50,000 in a financial year. However, no tax benefit is available on a lapsed insurance policy.

Remember, term insurance is not for you, but for your family. It is your prime responsibility to take care of your loved ones which you would be able to do only if you pay your premiums on time.

Shiv – As always, an excellent article 🙂

Thanks Bobby! 🙂

really a nice post. Thanks to the author for sharing.

Looking forward to your next post.

Thanks Ashish!