This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

After REC and PFC, IIFCL will become the third company to launch its tax-free bonds this financial year from December 26th. But, unlike REC and PFC, this will be IIFCL’s first issue of tax-free bonds as the company did not have any such issue last year. The issue will close on January 11th.

The company plans to raise Rs. 1,500 crores from the issue with an option to retain oversubscription up to Rs. 9,215 crores.

Despite of the fact that different companies are issuing these tax-free bonds, still as per the CBDT notification, they are bound to keep all of the terms quite similar to each other. There are few terms which are different.

What’s different or unique in this issue?

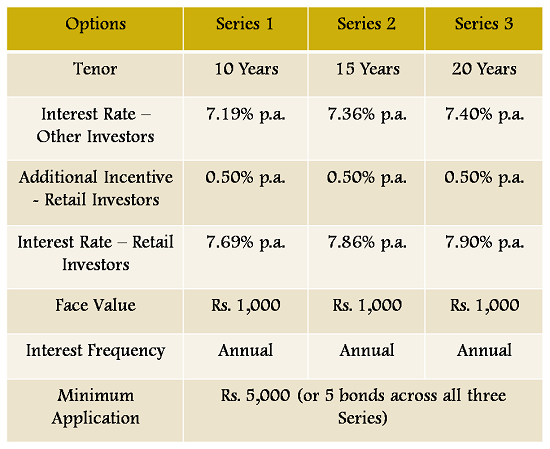

20 Year Option: IIFCL is the only company which has been allowed to issue tax-free bonds with an additional option of 20 years along with 10-year and 15-year options. IIFCL is offering 7.90% per annum for its 20-year option.

NRI Investment: Also, REC and PFC did not allow NRIs to apply for these bonds during their offer period. But, NRIs can participate in the IIFCL issue. They can apply for these bonds both on repatriation basis as well as non-repatriation basis.

Terms of the Issue

Apart from the 7.90% p.a. 20 year option, IIFCL will pay 7.69% and  7.86% per annum for the 10 year and 15 year options respectively. These rates are applicable for the Retail Investors category only and all other investors will get 0.50% p.a. less i.e. 7.40%, 7.19% and 7.36 for QIBs, corporates and HNIs for 20, 10 and 15 years respectively.

Again, the additional incentive of 0.50% will be payable to the original allottees only who invest in these bonds during this offer period. In case these bonds are sold or transferred by the original allottees, except in case of transfer of bonds to legal heir in the event of death of the original allottee, the coupon rates will be revised downwards to the base coupon rates.

The investors have the option to apply for these bonds either in the demat form or physical form and thus, demat account is not mandatory to apply for these bonds.

The issue is secured in nature and has been rated ‘AAA’ by CARE, ICRA and Brickwork Ratings. The bonds will get listed only on the Bombay Stock Exchange (BSE) and that too, within 12 working days post closure of the issue.

The minimum amount of application is Rs 5,000 with face value of Rs 1,000 per bond.

40% of the issue is reserved for the retail investors, another 30% of the issue is reserved for the high net worth individuals (HNIs) i.e. for the individual investors investing above Rs. 10 lakhs. 15% of the issue is reserved for the institutional investors and the remaining 15% is for the corporate investors.

About IIFCL

India Infrastructure Finance Company Limited (IIFCL) is not a well known company among the investors as it is a relatively new company to have come into existence. IIFCL is a wholly-owned company by the Government of India, which got incorporated in early 2006. It has been created with an objective of providing innovative financing solutions to promote and develop world class infrastructure in India.

As per S. K. Goel, the Chairman and Managing Director of IIFCL, this issue might be the last such issue from IIFCL as the Finance Ministry is not too happy with the Government losing huge tax revenue with their tax-free status. If this is the case, then the investors in the highest tax brackets should not wait too long for the other issues to invest in.