PFC Tax Free Bonds Review

Power Finance Corporation (PFC) will be launching the second public issue of tax-free bonds this financial year (FY 2012-13) from the coming Friday, December 14th, 2012. The company plans to raise Rs. 1,000 crore in this issue with an option to retain oversubscription to the tune of Rs. 3,590 crore, making the total size of the issue to be Rs. 4,590 crore.

PFC plans to use the proceeds for company’s lending purposes, debt servicing and

working capital requirements, subject to the terms and conditions of the CBDT Notification.

Details of the Issue

Categories of Investors

As with all these issues, the investors would be classified in the following four categories:

Category I – Qualified Institutional Buyers (QIBs)

Category II – Non-Institutional Investors (NIIs) or Corporates

Category III – High Net Worth Individuals (HNIs)

Category IV – Retail Individual Investors (RIIs)

40% of the issue is reserved for the retail investors, another 20% of the issue is reserved for the high net worth individuals (HNIs) i.e. for the individual investors investing above Rs. 10 lakhs. 25% of the issue is reserved for the institutional investors and the remaining 15% is for the corporate investors.

Rate of Interest/Coupon Rate

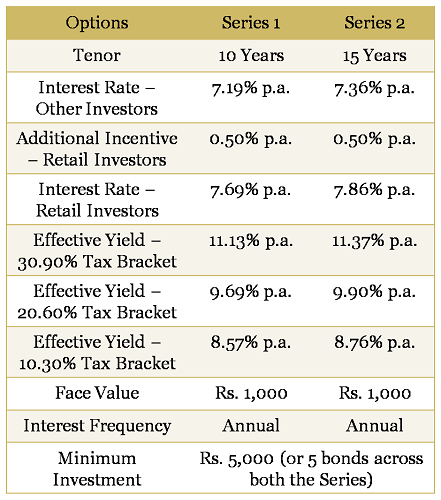

There is not much difference between this issue and the REC bonds issue which closed on Monday, December 10th. PFC will pay a base coupon rate of 7.36% and 7.19% per annum to the Category I, II and III investors with a maturity period of 15 years and 10 years respectively.

As with the REC bond issue, PFC will also pay an additional coupon of 0.50% p.a. to the retail investors over and above the base coupon rate, making it 7.86% and 7.69% per annum respectively. Interest will be payable annually as there is no cumulative interest option.

But, the additional incentive of 0.50% will be payable to the original allottees only who invest in these bonds during this offer period. In case these bonds are sold or transferred by the original allottees, except in case of transfer of bonds to legal heir in the event of death of the original allottee, the coupon rates will be revised downwards to the base coupon rates.

The interest earned will be exempt from tax under section 10 (15)(iv)(h) of the Income Tax Act, 1961.

Retail investors can invest up to Rs. 10 lakhs in the issue and still get the additional coupon of 0.50%. The company has decided to keep the minimum investment requirement of Rs. 5,000 (or 5 bonds of face value Rs. 1,000).

Listing, Safety and other features of the Issue

Demat account is not necessary to invest in these bonds. Investors have been given the option to apply these bonds in physical form also. Like last year, PFC bonds are going to list only on the Bombay Stock Exchange (BSE).

NRIs and foreign nationals among others are not eligible to invest in this issue. The allotment will be made on a “first-come-first-served†basis.

The issue has been rated ‘AAA’ by CRISIL and ICRA. The issue is secured in nature and in the event of default, the bondholders can claim a charge upon the assets of the company in connection with these bonds.

The issue will close on December 21st, 2012. The bonds will get allotted and listed within 12 working days from the closing date of the issue.

How 7.86% is fixed and will the forthcoming tax-free bond issues carry higher rate of interest?

This financial year, there is a ceiling on the coupon rates these companies can offer based on the reference Government Securities (G-sec) rate. The coupon rate for ‘AAA’ rated issuers cannot be more than the reference G-sec rate minus 65 basis points (bps) or 0.65% in case of retail investors and G-sec rate minus 115 bps or 1.15% in case of QIBs, corporates and HNIs.

The reference G-Sec rate is the average of the base G–sec yield for equivalent maturity reported by the Fixed Money Market and Derivative Association of India (FIMMDA) on a daily basis prevailing for two weeks ending on the Friday immediately preceding the filing of issue’s prospectus with the designated stock exchange and the Registrar of Companies (RoC).

So, if the 10-year benchmark G-sec rate is 8.17% p.a. payable semi-annually, the reference G-sec rate would be equal to (((1+(0.0817/2))^2) – 1) * 100 = 8.34% p.a. Hence, 65 bps less than 8.34% p.a. is 7.69% p.a. payable annually.

Keeping this ceiling and slow economic growth into consideration, I do not think the future tax-free bond issues would be able to carry a higher rate of interest. In fact any interest rate cut by RBI due to an unexpected and further fall in economic growth would force the issuers to lower their coupon rates.

About Power Finance Corporation Limited

Power Finance Corporation is a listed Government of India undertaking with 73.72% stake held by the govt. The company provides financing to state electricity boards (SEBs), state generating companies and independent power producers (IPPs) for a range of power-sector activities including generation and distribution.

Performance of the PFC tax free bonds issued last year

Tax free bonds issued last year have given quite handsome returns to the investors in the range of approximately 15%-20% annualised. PFC tax free bonds closed at Rs. 1,086.10 on December 11th, 2012 carrying a YTM of 7.43%. These bonds paid a mid-year interest also on October 15th, 2012.

Given the current YTM of 7.43%, the rate of interest of 7.86% or 7.69% is still attractive for the retail investors in the 30% or 20% tax bracket with medium-term to long-term perspective.

REC has got a good response for its bond issue from the retail and HNI investor categories, probably because it was the first issue of these popular tax-free bonds. The timing of PFC issue is interesting as the RBI will be announcing its next monetary policy measures on December 18th. In case there is a rate cut by RBI, then the issue will become quite attractive for the retail investors and they can expect an appreciation in the market price of these bonds.

What is the interest payout date for these bonds?

I know its annual interest payment but interest will be paid in which month?

-Anix

Hi anix… PFC has not announced the interest payment date as yet. They will probably do it at the time of allotment.

Was googling about tax free bonds and came across your blog. But I heard mutual funds give more returns than these bonds. then why to opt for them. also came across this article. will be helpful for those planning to invest in bonds.These are the upcoming bonds coming up this financial year – http://www.find.fintotal.com/List-of-Upcoming-Tax-Free-Bonds-2012-13/3899

Thank you for the link, it will definitely help !! We also have the list of companies issuing tax free bonds this year – https://www.onemint.com/2012/11/12/tax-free-bonds-notification-2012-13/ and would soon be posting an article “Tax Free Bonds Calender 2012-13”.

Different assets classes have different risk-reward characteristics. Investors prefer tax-free bonds over mutual funds as the returns are fixed in these bonds and volatile in mutual funds. There is a very low risk of you losing money with these bonds.

Any idea about the allotment date & listing date of tax free bonds this year like REC & PFC ?

Thanks, Karthik

Not yet Mr. Karthik, but the bonds will get allotted and listed within 12 working days from the closing date of both the issues.

Dear Mr. Shiv,

Thanks for your valued data.., Can you please help to know when and where can I buy this bonds in Bangalore preferably, and what is the maximum one can invest in this bond.

Your immediate reply will be highly appreciated.,

Regards,

Narayan

Hi Narayan… You can download the application form from the link pasted above in the post and submit the duly filled form, along with the investment cheque, PAN card copy, address proof copy and a cancelled cheque, at the following address in Bangalore: A.K. Capital, 509/510, 5th Floor, Brigade Tower, No-135, Brigade Road, Bangalore – 560 025. You can contact me at +919811797407 for further assitance, if required.

Dear Narayan… Retail investors will get an additional 0.50% p.a., if they invest less than or equal to Rs. 10 lakhs. There is no upper limit of investment.

Will these bonds give tax exemption over and above 1 lac currently under sec 80? till last year there was a special tax concession upto 20k for investing in infra tax free bonds.

Amit

No, these tax-free bonds do not provide any tax exemption.

PFC tax-free bonds closing date has been extended to December 27th.

This is interesting, so they haven’t even got enough people to subscribe to these till now?

The problem is ‘People’ are investing but “Smart Money” is not coming. Also, REC got the first mover advantage.

Hmmm interesting. Thanks.

Shiv/Manshu – But why did REC list at a premium and PFC is not subscribed yet? Beats me. As in, both are AAA and offer similar coupon rates!

Hi Neel… REC has listed at a discount and not at a premium. 7.88%/7.38% REC bonds got closed at Rs. 992 on the BSE with only 372 bonds got traded. Am I missing something Neel? PFC issue is yet to get fully subscribed as there is no institutional interest at all.

My bad. You are right. I looked up the REC bond issued earlier(8.32%). That thing had interest built in. I should have checked for the 7.38% one. Thank you for the response.

That is fine, you are welcome Neel!

If we buy X bonds now, then after 10 years PFC will buy them back at the prevailing price. Till that point PFC will deposit the same interest amount for these X bonds annually. Is this correct ? How do they beat the inflation during the coming 10 years if the interest rate is fixed ?

Hi Karthik… After 10 years, these bonds will get extinguished and PFC will pay you back your principal investment at the “Face Value” of these bonds and not at the “Prevailing Price”. Though, on the maturity date, the prevailing price will be equal to the face value only.

You will get the same interest amount for your X no. of bonds annually. These bonds are not “inflation-indexed bonds” and none of these companies are committed to provide the investors any such bonds.

Thank you Shiv. How does these bonds benefit investors ? What is the real power in these bonds ? Could you please enlighten me further ?

Hi Karthik… First of all, these bonds are ideal for the HNIs who fall in the 30% or 20% tax brackets and want to invest in safe fixed income instruments like Bank FDs, Post Office schemes etc. Secondly, these bonds can provide you some capital appreciation in case interest rates fall further from here.

Take the case of my family’s investments done last year in NHAI bonds. These bonds got issued on January 25th, 2012, as the Deemed Date of Allotment. In 11 months time, these bonds have appreciated 10% and have given 5.67% interest on the Face Value of Rs. 1,000, which makes it “17%+ annualised returns”. As the interest rates fall further, the value of these bonds will appreciate further.

But, I think this year’s bonds will not be able to match last year’s performance. But still, investors in the high tax brackets should subscribe to these bonds, if they have longer horizon and require fixed and safe investment. These bonds might not appreciate much in value.

Shiv = This is in continuation of your comments under “REC Tax free bonds” regarding their listing today @ Rs 990 – Rs 995 (closing rates). The volumes were zero in NSE and about 1000 for Series 1 and 2 total). The rates are as expected. The REC listing rates today are comparable to secondary market rates for bonds issued about a year back. They all give yield to maturity of about 7.4%. The volumes are also decent.

I am writing this under “PFC Tax free Bonds” because at this stage it is relevant for investors in double mind about their investment for bonds. My opinion is subjective and may be relevant for certain class of investors, but my advice to retail investors planning to sell the bonds with in a year would be to think twice as they might end up making loss of capital. The falling rates will make marginal difference. With large number of bonds still in the pipeline, the liquidity will also an issue.

Absolutely, I totally agree with you Mr. Batra! I shared similar views a few days back when I wrote this post – https://www.onemint.com/2012/12/04/should-you-book-profits-in-last-years-tax-free-bonds-to-invest-in-new-tax-free-bonds/

But still I think the investors, who did not subscribe to the last year’s bonds, should invest in these bonds with a medium-term to long-term perspective and that too, investors in the higher tax brackets only (30% & 20%). I expect these yields to fall 0.5-1% in the next 6 months-2 years.

Have these bonds started trading? I am unable to see anything on BSE after 961749.

Where can I get their latest prices?

PFC tax-free bonds are yet to get listed. 961749 is the scrip code of 7.38% REC tax-free bonds. I expect PFC bonds to get listed by Monday or tuesday, January 14th or 15th.

PFC Tax-Free Bonds allotment has been done. You can check the allotment status from this link – http://www.mcsdel.com/index001.asp

hi Shiv:

I cannot find the allotment date and interest payment date details anywhere. I would need this to arrive at the YTM for the PFC bonds.

Could you please help.

Thank you,

Akshay

For those who have been allotted the bonds in IPO, the YTM is the interest rate.

Thanks for the info Mr. Arun! YTM changes every passing day with a change in the market price of these bonds and a decrease in the maturity period. I hope you agree!

I agree with you Shiv. My answer was in reply to query from Mr Akshay Thakkar who purchased the bonds in IPO and would apply if keeps till maturity. If he decides to sell his query would no longer be applicable.

Hi Akshay… the allotment date is 4th January, 2013 and the interest payment date is 4th January every year.

Thanks Shiv.

Arun, I was asking with the perspective of buying the bonds in the secondary market. Unfortunately, BSE website sucks as compared to the NSE which also displays the YTM for the traded instruments and hence you have to manually calculate the YTM

Akshay = I normally calculate YTM using EXCEL sheet. If you give your email id, I can tell you how to do it.

Hey Shiv,

Can you please let me know if there is any lock in period of these bonds as i have invested in these and intending to sell these bonds now.

regards

Shekar

Hi Shekar,

There is no lock-in period with these bonds, you can sell them whenever you want.

Hi,everyone.

I haven’t received interest till now for 2016. Has anyone received it.

For 830pfc

Hi Dr. Puneet,

I think you should have received it today. If not, you should contact the Registrar.