This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

Two power sector companies are inviting your applications for their tax-free bonds – PFC 8.92% bond issue is already open, the issue size is Rs. 3,875.90 crore and has received an extremely good response from the investors by getting subscribed to the tune of Rs. 2,639.30 crore in just two days time. NHPC is entering the field for a competitive fight from October 18th with a smaller issue size of Rs. 1,000 crore.

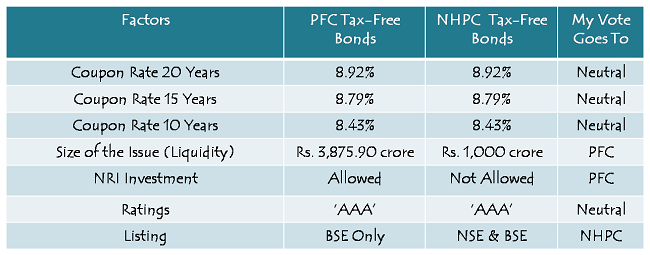

As far as the features of these two issues are concerned, the fight is so close that it has become extremely difficult for retail investors to make a decision. There are so many features which are absolutely same in both the issues and there are other features which are similar, but do not have much relevance to be considered. Just have a look at the features which are same and which are mildly different:

With interest rates exactly the same, both being PSUs and with features so similar, it becomes extremely difficult to make a choice based on just the features of these two issues. So, I thought of doing a fundamental comparative analysis between the two companies.

Profile of PFC & NHPC

PFC got incorporated in 1986 as a financial institution to finance, facilitate and promote India’s power sector development. It is a Central Public Sector Enterprise (CPSE) and got declared a Mini-Ratna enterprise in 1988 and entitled Navratna status in 2007.

PFC provides loans for various power-sector activities, including power generation, power distribution, power transmission and plant renovation and maintenance. PFC finances state electricity boards (SEBs), power generating companies of states and independent power producers (IPPs).

NHPC got established in 1975 to execute all aspects of hydroelectric power project development, from concept to commissioning. It was declared a Mini-Ratna Category-I CPSE in 2008 and has recently sought Navratna status from the government.

To be eligible for ‘Navratna’ status, a company needs to have a score of 60 out of 100, based on certain parameters which include net profit, net worth, total manpower cost, total cost of production, cost of services, Profit Before Depreciation, Interest and Taxes (PBDIT), capital employed etc.

As a Mini-Ratna Category-I entity, NHPC has been granted autonomy to undertake new projects. NHPC has developed and constructed 17 hydroelectric power stations and has current total generating capacity of 5,676.2 MW which is approximately 14.4% of the total hydel generating capacity in India.

It has power stations and hydroelectric projects located predominantly in the North and North East of India, in the states of Jammu & Kashmir, Himachal Pradesh, Uttrakhand, Arunachal Pradesh, Assam, Manipur, Sikkim. and West Bengal.

Credit Ratings of PFC & NHPC

International credit rating agencies Moody’s, Fitch and Standard & Poor’s (S&P) have granted PFC long-term foreign currency issuer ratings of “Baa3”, “BBB-” and “BBB-“, respectively, which are at par with the sovereign ratings for India.

NHPC has also been assigned “BBB-” rating by Fitch. S&P had also given “BBB-” rating to NHPC and removed it from ‘CreditWatch’ in September 2009, based on its assessment of NHPC’s “very strong” link with the government. S&P expressed its opinion that “there is a high likelihood that the government of India would provide extraordinary support for the company in the event of any financial distress”.

S&P also said that the ongoing support from the government is reflected in a tripartite agreement between NHPC, state electricity boards and the government, which largely mitigates the risk of any delay in payments from NHPC’s customers – the state electricity boards (SEBs) that have weak credit profiles.

Financials & other factors to consider

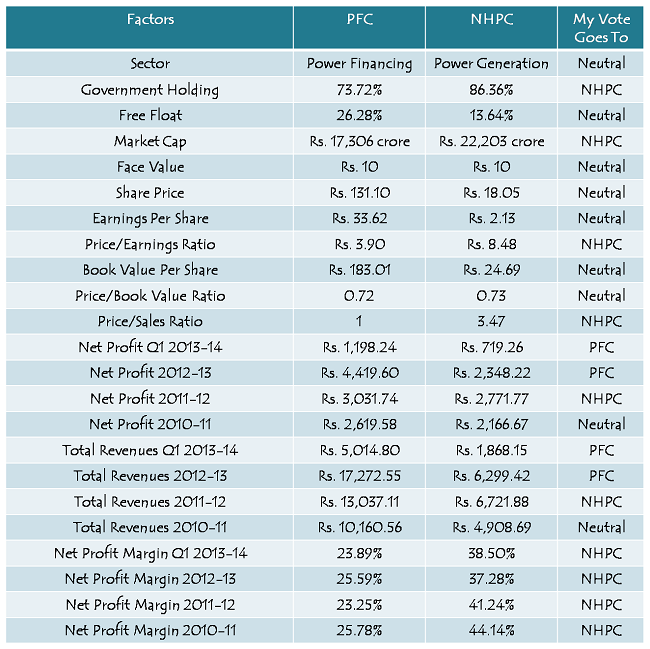

NHPC is a bigger company with a market cap of Rs. 22,203 crore based on its 15th October’s closing share price of Rs. 18.05. On the other hand, market cap of PFC is Rs. 17,306 crore with its share price being Rs. 131.10.

NHPC is also a less riskier company and it gets reflected in its PE ratio. The market is ready to pay NHPC a higher price for buying its shares based on its earnings, as compared to PFC. NHPC is trading at a P/E Ratio of 8.48 times as compared to PFC which is trading at 3.90 times.

PFC’s P/E Ratio of 3.90X is too low and it makes me feel that the market either believes PFC’s earnings to decline considerably at some point in future or some of the borrowers to default on their loan/interest payments.

Final Opinion

I am not a power sector expert. But, as a retail investor, I think NHPC is a better company to invest your money in the power sector. As a common consumer of electricity, this is what I understand – I buy electricity from a private power distribution company in Delhi, which in turn buys it from a power generation company like NHPC etc. Power generation business is a capital intensive business, for which companies like NHPC get capital infusion from the governments, loans from the power financiers like PFC, REC etc. and carry internal accruals by generating profits.

For NHPC, it is better to take money directly from us, the retail investors, rather than we giving money to PFC and then PFC lending it to NHPC at a higher rate. PFC’s fortunes hinge on the power producers like NHPC. If power producers are doing well, PFC would do better, but, if they are not doing good, PFC cannot do anything about it. This relationship is somewhat similar to real estate developers and project finance companies.

The fortunes of these power producers also depend on its cost of the factors of production, like labour, raw materials, technology, machinery etc. Most power plants here in India are coal-based, for whom it becomes a problem if coal supply gets interrupted or they have to import expensive coal due to its scarcity or falling value of rupee. For NHPC, the raw material cost is minimal.

My views might reflect very basic understanding because I don’t know how exactly things get carried out. I could have done some deep research on the functionalities & technicalities of the power sector companies, but then it would have become too complicated for me as well you to understand. So, personally & marginally, I prefer NHPC tax-free bonds over PFC tax-free bonds. Which one is your preference? Please share it share.

I have applied for 17 NHPC 8.92% bond but only 6 got allotted to me, what difference does it make if i buy the bond @1010 Rs in secondary market compared to initial 6 allotted bonds

It doesn’t make much difference, if you buy these bonds from the secondary markets, except that you’ll have to shell out some brokerage to buy these bonds.

I think you must have applied for these bonds on October 22nd, that is why you’ve got less no. of bonds than you had applied for.

Dear Shiv,

I missed the NHPC & PFC bonds due to a temporary cash flow scenario. Are there any other Tax free bonds on offer in the near future?

Regards,

AR

Dear AR,

Yes, there will be many more such companies to issue tax-free bonds in the months to come. NHB, NTPC & NHAI are up next to issue such bonds. I think all these issues should show up in December.

Hi Shiv,

Do you think the interest rate offered for future bonds will be at least at par with the PFC/NHPC?

Thanks,

DPP

Hi DPP,

Looking at the G-Sec yield at 8.85% again, rising fiscal deficit at 76% of the Budgeted Estimates, rising inflation and the govt’s failure to control all these things, I think we can expect similar rates. But none of the issues is to be launched in the next 10-15 days, so can’t predict future rates/yields as of now.

Dear Shiv

where can we check the latest subscription status of PFC bonds

Dear Dheeraj,

Here is the BSE link from where you can check the subscription status:

http://www.bseindia.com/markets/publicIssues/DisplayIPO.aspx?id=728&type=DPI&idtype=1&status=L&IPONo=783&startdt=10/14/2013

Dear sir,

As on today, NHPC bond issue subscribed 360% and PFC 480%

what is the possibility of of getting allotment in retail category if applied tomorrow

with regards

Santosh

Hi Santoshg,

You won’t get any allotment in NHPC tomorrow onwards, as the retail category has got subscribed more than the reserved portion of Rs. 400 crore. You can go for PFC bonds tomorrow and you’ll get full allotment.

Though it is not specific to any company, please read this generic article on TFB (if you have not done already):

http://economictimes.indiatimes.com/personal/finance/savings/centre/analysis/ET-Wealth-Should-you-invest-in-tax-free-bonds-or-prepay-home-loan/articleshow/24392511.cms

Yeah, I saw it yesterday, did not get time to read it. I think it depends on the interest rate expectations whether you should go for home loan prepayment or these tax-free bonds.

Did you find anything interesting in the article Amlan?

Yes Shiv!

If one is in the 30% tax bracket and the yearly home loan interest component is less than 1,50,000/- it may be a good idea to invest in TFB than prepaying home loan in case one has some surplus money! 🙂

Great !!

I am little confused on these. I see that HUDCO is quoting less than its listing price. Wouldnt you get a higher yield if you bought HUDCO from the secondary market? I remember these being tax-free too.

Hi harineem,

What confusion? Which HUDCO bonds are you talking about?

Ok HUDCO seems up today. I was referring to this page

http://nseindia.com/live_market/dynaContent/live_watch/equities_stock_watch.htm?cat=SEC

It has a listing of bonds and some are quoting below par. Wouldnt your yield be higher if you bought ones like that e.g IRFC or NHAI today?

Yes harineem, yield is higher than the previous year’s coupon rates, but it is still lower than the current coupon rates. None of them is offering more than 8.92%.

Hi Shiv,

First of all thanks for spending your time to help retail investors like me through those articles. When I feel I am in dark and try searching in Google often I land into articles you have posted already. It is almost like philanthropy you are doing on regular basis.

I have certain queries.

1> Does it really matter to research financial health of a PSU on top of a AAA credit rating given by all 3 agencies. I know this is rating at the time of issue and may change in coming years but what can be the concern for a retail investor like me to research on top of credit rating? Possibility of default or delayed interest payment in future? I am sure you have access to lot historical data. Can you give such example of default/delay for TF bonds by a Govt PSUs ever?

2> What consideration can lead to opting for 10 years bond instead of 20 years. Even I prefer to block money for only 10 years, should I not go for 20 years bond and enjoy higher interest rates? After 10 years I can sell out (provided that bond is liquid/tradable after 10 years and assuming buying/selling in secondary market is not complex thing for a retail investor) or I choose to continue. Here I am trying to understand what consideration can lead me opting for 10 years bond.

Secondly, why are PSUs ready to pay more for 20 years bond? And should it also influence allocation? Suppose I apply for 10 years bond on first day of the issue and later it gets oversubscribed. Can they give preference for a 20 year application over mine? Or allocation is purely FCFS basis and no preference on higher tenure application? I am surprised that those Govt organizations are so confident in thinking that after 10/15 years we will still be developing country with high interest rate and there is no chance for them to borrow fresh money with lower prevailing rates from market.

3> You provided details data of PFC/NHPC subscription. Is subscription status public information and if so what is the internet source of this data?

This is the first time I am writing to you. I thank you in advance for all articles you will write in future. Like past, I may not reach you but read them and thank you (and onemint) silently.

Thanks a lot Pinaki for your kind & motivating words! I am feeling honoured. 🙂

Also, thanks for your participation here and I would like you to do that regularly, for us to have such intelligent queries/inputs. Silence is useful on many occasions, but is a problem for us as it makes us demotivated.

All your queries are quite interesting and I think I can do a post on these queries. In case I am not able to do a post, I’ll answer them here again. Till that time, here are my short responses to some of your specific queries:

1. “Example of default/delay for TF Bonds by any Govt PSU” – Earlier, it was the RBI which used to issue 8% or 6.5% tax-free bonds. These PSUs are issuing tax-free bonds only for the last 2-3 years. So, no history of any default so far.

2.”Suppose I apply for 10 years bond on first day of the issue and later it gets oversubscribed. Can they give preference for a 20 year application over mine? Or allocation is purely FCFS basis and no preference on higher tenure application?”

My response – Yes, allocation is purely on FCFS basis and there is no preference for a higher tenure application.

3. Yes, subscription status is publicly available and that is what ‘bidding’ is meant for. Here is the source of bidding information –

http://www.bseindia.com/markets/publicIssues/DisplayIPO.aspx?id=731&type=DPI&idtype=1&status=L&IPONo=786&startdt=10/18/2013

http://www.bseindia.com/markets/publicIssues/DisplayIPO.aspx?id=728&type=DPI&idtype=1&status=L&IPONo=783&startdt=10/14/2013

Hi,

It is very interesting to note how different people are responding to the TF bonds currently available in market. Shiv done very well to compare the companies and SWOT analysis based on data available with him. I agree with him on many points. But my suggestion to new TF investors is to look at a diversified portfolio of TF bonds which will give coupons in different months and also have a diversified risk in terms of liquidity etc. When Shiv compared NHPC, he mentioned PFC gives loan to NHPC. It is also true that PFC gives loan to multiple power companies and hence a portfolio by itself in power sector. Similarly , if one is looking for short term investment, it is worth buying NHAI TF bonds from secondary market which is trading below par and offering 8.4% for 8.5 years. This also helps in diversifying your portfolio and also maximum traded TF bond currently available in market. If some one is looking at investing 30-40 Lakhs, it is better for them to opt for retail rather than taking the HNI route. Retail will ensure 100% allocation compared to HNI. As Shiv mentioned all this companies are rated AAA and have government backing. But when we look at subscribing, look for bonds which is having maximum subscription in retail segment. Check for daily subscription. It will be good if Shiv gives the detailed breakup all series. For example some one chose 10 years to make it short term. Maximum subscription is in 20 years and this means you will have more liquidity in secondary market for 20 years considering that more bonds are available in market. Hope this helps some of the readers.

Some very interesting & useful points George! Thanks a lot!

Dear Shiv,

As PFC is having a portfolio of loans to Power Companies, it is not safer (less probability of going bust-as all power companies may not shut-down simultaneously) compared to NHPC which is a single power company ?

Thanks

Dear TCB,

I think you’ve read Business Line’s analysis of NHPC bonds today. Yes, it is corect to say to an extent that PFC’s lending portfolio is diversified as it lends to various state electricity boards (SEBs) & other power producers, but then I think it is better to be a PSU power producer rather than a PSU power financier in this country. I think India doesn’t have a problem of financing infrastructure, what is lacking is quality manufacturing & quality infrastructure. India has huge scope for power producers as whatever gets produced here, there are ready buyers for that. We cannot afford to stop producing power here.

But, then the next & the biggest problem is politics. Politicians are ready to give everything free of cost to the general public here in the name of “poor janta”, just to show off that they are not doing it for ruling them for 5 more years. Most of the SEBs here are run by the government and whichever have been privatised, they also work under the government’s influence. So, I think there is no real benefit of diversification here for PFC. Power sector financiers like PFC, REC etc. have been forced to recast their loans to SEBs many a times in the past.

Now, tell me one thing, when the govt. has allowed various companies in the infra space, like NHPC, NTPC etc. to raise money directly from the general public, why would they go to the power financing companies like PFC, REC for their loan requirements. It is cheaper for them to raise money directly or go overseas to do that.

Also, I have written above that “If power producers are doing well, PFC would do better, but, if they are not doing good, PFC cannot do anything about it”. So, the situation in the past 2-3 years has been very bad for the power sector, which is now getting somewhat better very recently. So, let’s see how it goes. Moreover, this is just my personal opinion and there is a good probability that my view is wrong.

Day 1 (October 18th) subscription figures for NHPC:

Category I – Rs. 420 crore as against Rs. 150 crore reserved

Category II – Rs. 632.63 crore as against Rs. 200 crore reserved

Category III – Rs. 390.89 crore as against Rs. 250 crore reserved

Category IV – Rs. 171.82 crore as against Rs. 400 crore reserved

Total Subscription – Rs. 1,615.34 crore as against total issue size of Rs. 1,000 crore

Day 4 (October 18th) subscription figures for PFC:

Category I – Rs. 360 crore as against Rs. 581.38 crore reserved

Category II – Rs. 1,223.30 crore as against Rs. 775.18 crore reserved

Category III – Rs. 977.84 crore as against Rs. 968.98 crore reserved

Category IV – Rs. 665.81 crore as against Rs. 1,550.36 crore reserved

Total Subscription – Rs. 3,226.95 crore as against total issue size of Rs. 3,875.90 crore

Thanks for this analysis, Shiv. On other websites, they have mostly compared based on coupon rates and little has been said about company profile etc. This is only article that I came across which is actually comparing financials of both the companies on various parameters.

I have some apprehension about power sector finance companies in India. Since they mostly lend to SEBs and many SEBs are not in great shape with respect to recoveries/defaults. Big defaults that SEBs have come from sick industrial units or politician backed units or co-operatives. SEBs can not to much there. They can only flex muscles on common household customers have recoveries of Rs. 200-300. Anyways, what is your opinion about bonds from power sector finanace companies? Does there performance really matter viz-a-viz security of capital. Specifically since those are backed by GOI?

Thanks Shiv! I’d like to believe that the requirement of not being an NRI just applies at the time of buying and if the NRI status changes in the future it should still allow me to hold on to these bonds and earn tax free income in India.

However, assuming that I’ll be required to sell these bonds, can I selectively sell them to my parents?

– PP

Even I hope so! My point is that a resident Indian needs to get his/her bank account, trading account & demat account closed/updated whenever he/she leaves the country & attains the NRI status. So, whether you are allowed to transfer it to your NRI A/c. or not, I am not sure. It is better to apply for PFC Bonds.

Yes, you are allowed to sell these bonds to your parents as they are separate legal entity.

Hi Shiv,

I understand that NHPC is not allowing NRI investment. If I buy them currently as a resident Indian and become an NRI (or a foreign national) sometime in near future, would there be any implications on earning interest and/or selling these bonds?

Thanks,

PP

Hi PP,

I have no idea how Indian taxation laws deal with such cases and how other countries take it. But, I think the maximum that you would be required to do is to sell these bonds or pay interest on this income in the foreign country, that is it.

Any views on Tata Global Beverages Low coupon Bond?

Hi Rajeev,

As of now, I don’t have any details about this bond issue and moreover, most likely it would be raised overseas through private placement. It would not be offered to the general public here in India.

Hi Rajeev,

Tata Global Beverages has raised Rs. 325 crore issuing its low coupon bonds through a private placement.

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=622cac5f-3cfb-49de-978a-727c4adf48ac

Thanks Shiv for the comparative analysis!

I agree with your comments/inputs and my personal vote also goes for NHPC.

I normally invest in TFBs through SBI S/B online a/c (e-Services -> Demat & ASBA Services -> IPO (Debt) -> Accept) and they list the upcoming IPOs in advance. But somehow NHPC is still not listed there!

Thanks Amlan for sharing your views here!

Probably SBI is in the process of uploading it and the same gets done by today some time. If it does not get introduced on time & you need any assistance in applying for it on Day 1, just let me know I’ll get it done for you.

Thanks Shiv. I am always amazed at the time you spend to analyze and write these posts just to benefit non-financial people like us. Thanks again.

Thanks a lot harineem for your motivating words! Whatever extra efforts I put for these posts are for this kind of motivation only.

Hi shiv,

One more opinion I would like to take,is it advisable for individuals who are non-tax payer to invest in these bonds?

and secondly those investors who are now in non-tax payer bracket but in future very much likely to be in tax-bracket?

Hi Saurabh,

1. Personally, if I am considering capital appreciation in the value of these bonds, then only I’ll invest in these bonds as a non-tax payer. Otherwise, I’ll prefer NCDs of private companies yielding higher rate of interest.

2. It depends how soon one expects to be a tax-payer.

Thanks a lot for answering my queries.

You are welcome!

Thanks for all your posts which help us making financial desicion.

I have a small question

What if i invest in these Tax Free Bonds through demat, but need to sell them early as i might need money urgently ? lets say i have to sell them 9 months later. would i still get the interest for the 9 month period if sold before the interest pay date ?

I do understand that there will be a bid -ask as the bonds will not be very liquid but would i get a return for a 9 month duration.

Hi Gaurav,

With tax-free bonds, interest gets accrued throughout the year, but gets paid only once a year and that too, only to those investors who hold these bonds till the “Ex-Interest” date of the bonds. So, if you sell these bonds 9 months from now & before the ex-interest date, then you’ll not get the accrued interest.

But, that doesn’t mean you’ll not get any return on your investment. These bonds will appreciate in value during this period and keeping all other factors constant, the appreciation should be equal to the accrued interest.

Also, as these bonds have different interest payment dates, you will have to take that also into consideration, like NHPC has April 1st as the interest payment date for its bonds, whereas REC will pay it on December 1st.

Many thanks for this valuable comparison,was eagerly waiting for it.

So,NHPC it is then,bond opens tomorrow

You are welcome Saurabh!

Liquidity will be better in PFC, because of larger 3876Cr issues, vs 1000 from NHPC. Given more number of units, dont you feel trading volume will be better? You’ve appreciated NHPCs additional NSE listing, but I feel it will further dilute selling chances

Hi,

Please check the 4th point in the same table. I have preferred PFC for its bigger issue size & liquidity. I think listing on both the exchanges is a positive for any security, I might be incorrect in my assessment and you might be right in your assessment.

Thanks again Shiv for your valuable inputs.

NHPC is also expanding its business from harnessing power from solar, Wind rather than only depending on Hydroelectric power generation. This will help NHPC in long run. My vote goes to NHPC.

You are welcome Amit!