This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

As National Housing Bank (NHB) tax-free bonds issue is about to get launched from Monday, Indian Railways Finance Corporation (IRFC) would also be coming out with its issue from January 6. Like many of the investors, I am also disappointed with the coupon rates IRFC has announced to offer and also with its decision not to offer the 20-year option.

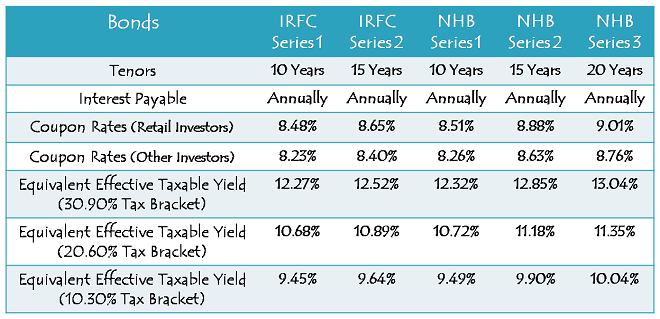

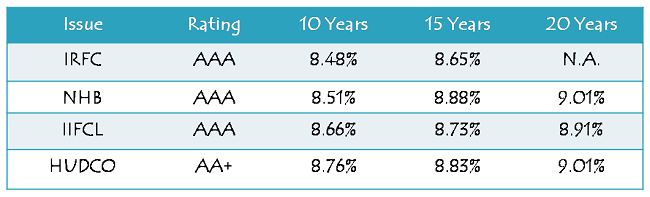

If any of you doesn’t know already, IRFC has decided to offer 8.48% per annum for the 10-year option and 8.65% per annum for the 15-year option. These rates are lower than the rates NHB issue will carry i.e. 8.51% p.a. for 10 years and 8.88% p.a. for 15 years. As both these issues are ‘AAA’ rated and both companies are government organisations, I think people would be more enthusiastic about NHB bonds.

Though at one place in the prospectus the closing date has been mentioned as February 20, 2014, it has been stated as January 20, 2014 at all other places. Looking at the illustrative example it gets clear that it is indeed January 20th.

Size of the Issue – IRFC is authorised to issue tax free bonds worth Rs. 10,000 crore this financial year, out of which it has already raised Rs. 1,337 crore through a couple of private placements. With base issue size of Rs. 1,500 crore, IRFC plans to mop up all of the remaining Rs. 8,663 crore with this issue, including the green-shoe option to retain additional Rs. 7,163 crore.

I would call IRFC move to be brave enough to target such a large amount to be raised within a span of just eleven working days, which others have not been able to do even with two tranches of longer durations.

Coupon Rates on Offer – People who were hoping to get even higher interest rates and planning to diversify their portfolio with this issue and the NHB issue, have been left disappointed by the interest rates IRFC has fixed to offer. Coupon rates of IRFC have been 0.23% lower with the 15-year option and 0.03% lower for the 10-year option as compared to the NHB issue. As always, the non-retail investors will get 0.25% less rate of interest every year.

As compared to IIFCL as well, which is currently offering 8.66% p.a. for the 10-year option and 8.73% p.a. for the 15-year option, the rates are lower. So, the investors can still subscribe to the IIFCL issue if they haven’t already, as it is still undersubscribed in the retail investors category.

Rating of the Issue – IRFC is the financing arm of the Indian Railways with zero non-performing assets. It earns assured net interest margins (NIMs) from the Ministry of Railways (MoR) and other related entities like Rail Vikas Nigam Limited (RVNL) and RailTel.

Most importantly, in case of any default or shortfall in the money required to redeem these bonds, the MoR will be required to fund the payments due to the bondholders. So, there is minimal risk involved with these bonds and probably that is the reason all rating agencies, CRISIL, ICRA and CARE, have assigned ‘AAA’ rating to the issue.

NRI/QFI Investment – Non-Resident Indians (NRIs) are eligible to invest in this issue, on a repatriation basis as well as on a non-repatriation basis. Qualified Foreign Investors (QFIs) are also eligible to invest in the issue.

Investor Categories & Allocation Ratio – The investors have been classified in the following four categories and each category will have certain percentage of the issue size reserved during the allocation process:

Category I – Qualified Institutional Bidders (QIBs) – 10% of the issue i.e. Rs. 866.30 crore is reserved

Category II – Non-Institutional Investors (NIIs) – 30% of the issue i.e. Rs. 2,598.90 crore is reserved

Category III – High Net Worth Individuals including HUFs, NRIs & QFIs – 20% of the issue i.e. Rs. 1,732.60 crore is reserved

Category IV – Resident Indian Individuals including HUFs, NRIs & QFIs – 40% of the issue i.e. Rs. 3,465.20 crore is reserved

Listing – The company has decided to get these bonds listed on both the stock exchanges i.e. National Stock Exchange (NSE) as well as the Bombay Stock Exchange (BSE). The bonds will get allotted and listed within 12 working days from the closing date of the issue.

Minimum & Maximum Investment – Unlike NHB, the face value of a bond in this issue has been fixed at Rs. 1,000 and as always, the minimum investment would remain Rs. 5,000 i.e. at least 5 bonds of Rs. 1,000 each. Retail Investors’ investment limit stands at Rs. 10 lakhs, beyond which they will be considered as HNIs and will get a lower rate of interest.

Demat not Mandatory – An investor, as per his/her own choice, can subscribe for these bonds in either of the forms, demat or physical. Though it is mandatory to have a demat account to sell these bonds, you may subscribe to them in certificate form as well and can get them converted to demat form whenever you want.

Interest on Application Money & Refund – IRFC will pay interest to the successful allottees on their application money, from the date of realization of application money up to one day prior to the deemed date of allotment, at the applicable coupon rates. Unsuccessful allottees will get interest @ 5% per annum on their refund money.

Interest Payment Date – IRFC has decided to make its first interest payment on April 15, 2014 and subsequent interest payments will also be made on April 15 every year.

What would make you invest in this IRFC bond issue?

With NHB offering higher rate of interest for all maturity periods from Monday and IIFCL, HUDCO still open for subscription with higher rate of interest, what is that one thing which you think differentiates this IRFC issue from the rest of the issuers? Please share your views about it and let’s see if it makes sense to other investors also.

Application Form of IRFC Tax Free Bonds

NHB Tax-Free Bonds – Bidding Centres

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in IRFC tax-free bonds, you can contact me at +919811797407

Day 11 (January 20) subscription figures:

Category I – Rs. 287.30 crore as against Rs. 866.30 crore reserved

Category II – Rs. 590.98 crore as against Rs. 2,598.90 crore reserved

Category III – Rs. 496.89 crore as against Rs. 1,732.60 crore reserved

Category IV – Rs. 943.01 crore as against Rs. 3,465.20 crore reserved

Total Subscription – Rs. 2,318.17 crore as against total issue size of Rs. 8,663 crore

Looks like IRFC has extended the closure date by 3 weeks (to 7th Feb 2014).

That’s correct. IRFC issue closing date has been extended to February 7th, 2014.

Hi Shiv

Some questions on IRFC which i am not able to find satisfactory answers. I thought you will have some idea on those and posting this in this forum. Appreciate your inputs

Do you know from where IRFC gets money to pay us interest? I understand IRFC finances rolling stock of railways and transfers the assets to Indian Railways. Now , how does IRFC gets yearly interest to pay investors? Does Indian Railways budget that much amount in their budget to give to IRFC? When the bond gets matures , how will it eventually pay back investors? Considering this bond size , 15 years down the line , just wondering how will IR raise 10000 crore to pay back IRFC. Government will certainly ensure this bond is paid back , still there should be better processes within IRFC to get back bond amount from IR

Regards

Ramadas

Hi Ramadas,

It is a fairly simple query. The process is very much similar to a car loan. IRFC raises money from institutional/corporate investors or retail investors like us. Ministry of Railways (MoR) purchases rolling stock for the Indian Railways (IR) and the stock remains the asset of IRFC. The stock is leased to IR and the lease rate is close IRFC’s finance cost plus its net interest margin of 0.50% p.a. approximately.

As per the lease agreement, Ministry of Railways is required to pay up the shortfall in the funds IRFC needs to redeem these bonds. How good these processes are, only IRFC will be able to tell. One can file for an RTI to get more info.

Thanks Shiv. Appreciate your inputs

Regards

Ramadas

You are welcome!

what are the chances of extension of IRFC beyond 20th Jan?

My guess would be as good as yours SB, but I think they should extend it.

Day 10 (January 17) subscription figures:

Category I – Rs. 287.30 crore as against Rs. 866.30 crore reserved

Category II – Rs. 541.78 crore as against Rs. 2,598.90 crore reserved

Category III – Rs. 475.02 crore as against Rs. 1,732.60 crore reserved

Category IV – Rs. 900.39 crore as against Rs. 3,465.20 crore reserved

Total Subscription – Rs. 2,204.50 crore as against total issue size of Rs. 8,663 crore

Dear Shiv,

I hv applied for IRFC cat.IV, series I on 10th jan. When will I know my allocation status?

Generaly how many days they takes for allication after the issue closed?

Hi Tushar,

IRFC issue is still open. If it gets closed on January 20th, the company will allot you the bonds within 9-10 working days.

Day 9 (January 16) subscription figures:

Category I – Rs. 187.30 crore as against Rs. 866.30 crore reserved

Category II – Rs. 535.07 crore as against Rs. 2,598.90 crore reserved

Category III – Rs. 456.28 crore as against Rs. 1,732.60 crore reserved

Category IV – Rs. 875.84 crore as against Rs. 3,465.20 crore reserved

Total Subscription – Rs. 2,054.49 crore as against total issue size of Rs. 8,663 crore

Day 8 (January 15) subscription figures:

Category I – Rs. 187.30 crore as against Rs. 866.30 crore reserved

Category II – Rs. 529.25 crore as against Rs. 2,598.90 crore reserved

Category III – Rs. 438.83 crore as against Rs. 1,732.60 crore reserved

Category IV – Rs. 850.58 crore as against Rs. 3,465.20 crore reserved

Total Subscription – Rs. 2,005.95 crore as against total issue size of Rs. 8,663 crore

I have never done partial withdrawal of the application. I will suggest to call the Registrar number or email them to find out about partial withdrawals. You can find the Registrar details in the Prospectus document.

Thanks Shiv and Sanjay for your detailed clarification!

Last question – is partial withdrawal possible? For ex. if someone has initially applied for 200 bonds, now wants to withdraw to the extent of 100 bonds and retain the application for 100, will that be possible through the withdrawal letter format recommended by you?

Day 7 (January 14) subscription figures:

Category I – Rs. 185.30 crore as against Rs. 866.30 crore reserved

Category II – Rs. 507.80 crore as against Rs. 2,598.90 crore reserved

Category III – Rs. 423.92 crore as against Rs. 1,732.60 crore reserved

Category IV – Rs. 820.70 crore as against Rs. 3,465.20 crore reserved

Total Subscription – Rs. 1,937.71 crore as against total issue size of Rs. 8,663 crore

1. The refund will go directly to the bank linked with your Demat Account.

2. I am not sure whether any interest will be paid on the withdrawal applications.

Thanks Sanjay!

And 1) how will I get the refund? by ECS to my bank account

2) Will Interest till date of refund be paid?

Hi SB,

1. Probably Sanjay missed that you applied for these bonds in physical form. You’ll get the refund credited directly to your bank account through ECS.

2. No interest gets paid on the applications which are withdrawn by the applicants.

Question on cancellation of application for IRFC tax free bonds: If someone has applied for IRFC tax free bonds, physical form, payment by cheque and cheque encashed, can he/she be able to cancel the application and get refund of amount paid (before allottment)?

Dear SB,

You can cancel the application..please prepare a letter in below format..take a print sign the document. Email and Fax the letter to Issue Registrar.

To

xxxxxxxxx

Subject – Application withdraw – ______ Tax Free Bond

I have applied for the ______ Tax Free Bond for the issue opened on ________. I would like to withdraw my application, please don’t allocate any Bonds against my application.

My application details are mentioned below:

Application Number xxxxxx

Depository Name CDSL

Beneficiary Demat Number xxxxx

PAN

Applicant Name

Investor Category Retail (41)

Total Application Amount

Bonds Applied For

Cheque No

Bank Name

Enclosing the signed scanned copy of application withdrawal request for your reference. Please acknowledge the request and confirm for the application withdrawal.

Regards

(Sign here)

Name

Address –

Ph –

Email –

Please don’t forgot to fax this document…

Thanks a lot Sanjay for sharing this info and also the format!

Hello friends,

Any idea about how to withdraw if the application was made through ICICIDirect ? I might have to call them and check.

Mr Rajan has decided to hike the rates for long term. So I wonder there may be better opportunities in near to medium term than IRFC.

Shiv, waiting for your review of the RBI policy and guidance !!!

Day 6 (January 13) subscription figures:

Category I – Rs. 185.30 crore as against Rs. 866.30 crore reserved

Category II – Rs. 505.26 crore as against Rs. 2,598.90 crore reserved

Category III – Rs. 422.23 crore as against Rs. 1,732.60 crore reserved

Category IV – Rs. 802.59 crore as against Rs. 3,465.20 crore reserved

Total Subscription – Rs. 1,915.37 crore as against total issue size of Rs. 8,663 crore

Sir,

Should we expect IRFC TFB tranche II in the current financial year?

Regards…

Hi Shub,

If IRFC decides not to extend the current issue beyond January 20th, then I think we’ll have its tranche II as well. But, I think they’ll extend it. Inflation data this week will be important for the G-Sec rates.

Só does that mean – IRFC can survive irrespective of indian railways!!

No, I never meant that. IRFC finances Indian Railways for the acquisition of new rolling stock and earns assured net interest margin in lieu of that. Indian Railways is the lifeline of India and I don’t think it can ever stop. No government can afford to stop the services of Indian Railways. Indian Railways is the responsibility of the Indian Government and IRFC is the responsibility of the Indian Railways. I think the financial standing of IRFC is better than Indian Railways.

Just to add, IRFC is the financing arm of Indian railways just like NHB/HUDCO supports in housing. If Indian Railways goes into trouble , the GOI steps in. Railway budget takes care of Indian Railway and it is not seen as a profit making organization. Like Shiv mentioned, Indian Railway is the lifeline of the country. If you look at it from this view, Indian railway is run by GOI, IRFC is run by Indian Railway. This implies that IRFC is directly under MOR. Similarly NHAI is also to be looked at servicing organization more than a profit making organization. Both this issues, our trust will be on the GOI. So on paper both IRFC and NHAI is having same level of security. But in public mind NHAI bonds are more attractive considering that they issue Capital gains bonds through out. Since India is looking at developing more roads, NHAI will have more visibility in future. Railways is also looking at FDI investments. I personally feel , considering the nature of secured bond, these bonds are more safe than the rest of the debt components these companies will have.

http://m.rediff.com/news/slide-show/slide-show-1-there-is-no-money-to-run-the-railways/20140109.htm

I am cautious in IRFC!!

Though there is a difference between the way Indian Railways run and the business of IRFC, but I too have my doubts on the financial management in these public sector enterprises. That is why I preferred NHB over IRFC.

Good Day Shiv

Can NRI invest in NHAI tax free bonds that will open on Jan 15 th 2014.

Regards

Brian

Thanks Brian and you too have a wonderful day today!

NRIs are not allowed to invest in the NHAI’s tax-free bonds this time around. So, they have only IRFC bonds to invest at this point in time.

Day 5 (January 10) subscription figures:

Category I – Rs. 160.30 crore as against Rs. 866.30 crore reserved

Category II – Rs. 494.08 crore as against Rs. 2,598.90 crore reserved

Category III – Rs. 409.74 crore as against Rs. 1,732.60 crore reserved

Category IV – Rs. 748.39 crore as against Rs. 3,465.20 crore reserved

Total Subscription – Rs. 1,812.51 crore as against total issue size of Rs. 8,663 crore

Shiv one question? Is there any limit on individual retail investors for investing in Bonds/debentures during a financial year? As I understand , the limit for Capital gains bond is 50 Lakhs.

No, there is no such limit on investment in these bonds/debentures. The limit of Rs. 50 lakhs is there only for the tax saving capital gain bonds.

Thanks Shiv for the clarification.

You are welcome!