NHAI’s 8.75% or 8.52% vs. IRFC’s 8.65% or 8.48% – Which Issue is Better?

This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at [email protected]

As the NHAI issue opens today, many investors have not been able to decide which issue they should go for – NHAI 8.75%, 8.52% or IRFC 8.65%, 8.48%. This comparison also becomes significant as no other company has even filed the draft prospectus for its issue. Before I do the comparative analysis, let’s check once again why these tax free bonds have become so popular with the investors.

Investors’ response to the tax-free bonds this financial year has been quite better as compared to the last financial year. The reasons are simple:

Higher Rate of Interest – Last year, these tax-free bonds were carrying lower rate of interest rates, broadly in the range of 7-8%. This year, their interest rates have been higher by around 1%. At the same time, interest rates on other saving instruments, like bank fixed deposits (FDs), post office schemes, company FDs etc., are more or less stable or just slightly higher.

Thanks to the higher G-Sec rates, it is natural for the investors to opt for 9.01% tax free bonds from the National Housing Bank (NHB) as against 9% fixed deposit interest rates from the State Bank of India (SBI) or from some other banks.

Removal of “Step Down” Clause – Till last year, these bonds carried the “Step Down” clause, as per which the buyer(s) of these bonds from the secondary markets are entitled to a lower rate of interest as compared to the first allottees. This is not applicable with the bonds issued during the current financial year.

This is also the reason why the bonds issued last year attract a very low trading interest, which I think should not be the case with this year’s tax free bonds going forward.

Lower Rate Differential – Differential between the rates offered to the retail investors and the non-retail investors got fixed at 0.25% per annum this year, which stood at 0.50% till last year. Non-retail investors considered it to be on a higher side and their participation was quite limited last year. This year, non-retail investors’ participation has been considerably better, especially with NHPC, NTPC and NHB.

Losses in Gilt/Income Funds – Bloodbath in the debt markets or a steep fall in the NAVs of debt mutual funds, due to some incorrect policy measures by the government and the RBI and also QE3 tapering announcement by the US Fed, also led to a shift in the investors’ interest towards these tax free bonds.

Investors of these tax free bonds know that they are going to get at least some fixed interest income every year in their bank accounts, even if there is no capital appreciation or even if the interest rates move higher from the current levels, resulting in a notional capital loss.

So, with very few options left available for the current financial year, the investors at present are asking themselves:

NHAI 8.75% or 8.52% vs. IRFC 8.65% or 8.48% – which issue should I invest in?

In terms of interest rates, it is very much clear that NHAI is offering higher rate of interest than IRFC, so it is relatively better. But, is it that simple? Certainly not, at least not for a common investor. How are these two companies different and which company is fundamentally better? Let us try to do some analysis.

Though not strictly comparable, I’ve tried to do a comparison between IRFC and NHAI on certain parameters. While IRFC is the wholly-owned financial arm of Indian Railways, NHAI is an autonomous body of the Government of India. Both these companies are strategically important for the Government of India (GoI).

IRFC got constituted in December 1986 for the purpose of raising the necessary resources for meeting the developmental needs of the Indian Railways. NHAI got operationalised in February 1995 for the development, maintenance and management of India’s national highways.

While IRFC has been classified as the Infrastructure Finance Company (IFC) by the RBI, NHAI is the nodal agency for the development and maintenance of national highways across the country, which makes it an infrastructure developer itself.

Financial Position of IRFC and NHAI

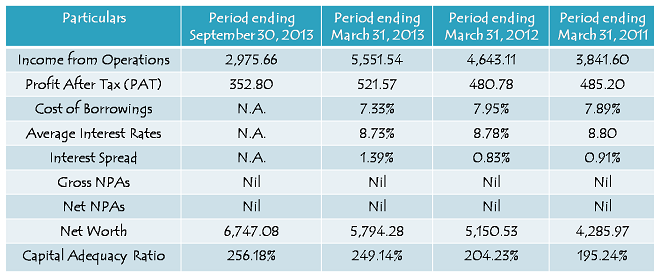

IRFC has a net worth of Rs. 5,794.28 crore as on March 30, 2013, whereas the same stands at Rs. 81,053.11 crore for the NHAI. As IRFC lends almost all its borrowings to the Indian Railways for financing rolling stocks, it has zero non-performing assets (NPAs).

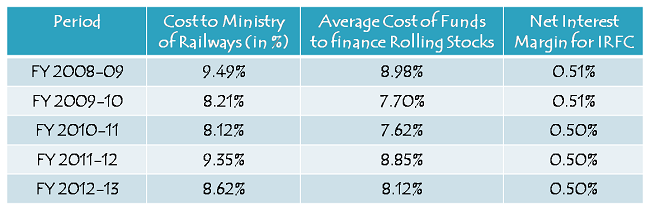

IRFC, on an annual basis, enters into a standard lease agreement with the MoR and earns an assured net interest margins from the MoR which has remained 0.50-0.51% in the last five fiscal years. MoR also bears the interest rate risk as well as the exchange rate risk. As it also gets regular capital infusion by the government of India, it got Rs. 600 crore during FY 2013.

Also, here are certain financial numbers of IRFC over the past few years:

As NHAI has been running into operational losses for the last few years, it is not practical to analyse its profitability position and make a comparison with that of IRFC. But, NHAI is a bigger organisation and has a total capital employed at Rs. 1,13,331 crore and capital work in progress (CWIP) at Rs. 1,06,440 crore as on March 31, 2013.

NHAI has been mandated by the GoI to implement National Highway Development Project (NHDP) with an estimated investment of about Rs. 2.48 lakh crore, spread over seven phases. NHDP envisages improvement of approximately 54,500 kms of national highway network.

As it is very difficult to conclude which organisation is better between the two in terms of overall financial performance and operational efficiency, personally I think NHAI issue is a better one as it offers a higher rate of interest, the size of the organisation can be considered as too big to fail and its strategic importance in India’s road & highways development is too significant to ignore.

Which one do you think is better between the two and how long do you think the NHAI issue will last? Please share your views.

Based on the details provided by Shiv I will prefer NHAI over IRFC. 🙂

Great !!

I prefer NHAI over IRFC for following reasons

1) NHAI definetely scores on higher interest rates

2) Trading volume for previous NHAI bonds are better than IRFC

3) NHAI issue size is small and is more likely to be fully absorbed by Market compared to IRFC

4) Possibility of IRFC coming to market for future tax free bonds is higher compared to NHAI. Last year , NHAI didnt opt for TFB at all. That makes NHAI bonds more scarce in market triggering more demand

Regards

Ramadas

1. Agree

2. That is because NHAI issue was bigger and did not carry the step down interest feature.

3. Agree

4. Agree

Whats so special about NHAI issue?! People have gone crazy!!!

Its already subscribed 2.77 times on day 1.

There is nothing crazy about it. GSecs were trading below 9% and improved CPI and WPI makes them more attractive. Retail is still not touched half way mark. The other investors are fully subscribed.

Many of the banks were on leave today and I expect the retail also to be closed tomorrow.

I think it will take 5-6 days for the issue to get closed.

Good comparison Shiv. I like your conclusion that finally all points remaining same, one should look for higher interest rates. We should wait and see whether there would be any more bonds which offers good returns like NHB which got closed in just 1 day which offered 9.01% returns.

Thanks Suresh!

Also, I never meant that the higher interest rate is the only reason for my preference for the NHAI bonds. NHAI is a bigger & better organisation as well. It is an infrastructure developer like Indian Railways, rather a financier like IRFC.

I don’t expect any ‘AAA’ rated issue this financial year to offer similar or higher rates than NHB or even NHAI. Now, only IIFCL Tranche III, IRFC Tranche II and IREDA issues are left which would be ‘AAA’ rated.

@Shiv, are there any more tax free bonds in pipeline for coming months? What is your outlook regarding the interest rates they may offer?

Hi Prat,

There are a few companies which should come up with their tax free bond issues, but I have no idea when they’ll launch it.

Also, I think interest rates are headed lower, but then it all depends on the government, how they tackle the inflation problem as well as the high fiscal deficit concerns. Till date they have taken no prudent steps to control either of these and now they are planning to increase the number of subsidised cylinders from 9 to 12, just because Rahul Gandhi wants it.

Hi Shiv,

Sorry an unrelated question related to using ICICIDirect website for demat, if someone can throw an answer for this one.

1st Question:-

I had acquired bonds for TaxFree bonds for NTPC recently, with my ICICIDirect account.

I see them in my account, in “ICICIDirect”, however you need to explicitly “Allocate” them into your Demat Account to get it appeared in your portfolio, even though they appear in your account. Somewhat weird.

On top of it, even though I “Allocated” those bonds, they don’t appear in my portfolio of Demat Balance of Bonds.

Any one experience this weird behavior, and resolution for same, to ensure it appears in your portfolio of “Demat Bonds Balance”

2nd question:-

Also do this online brokers charge per transaction, even for buying securities such as “Tax free bonds, mutual funds, IPO etc.”. I was under impression that they charge only for shares from secondary market, and not for other transaction

Hi Prash,

Ans to your first question

This happened to me as well, the TF bonds allocated appeared in demat section of ICICI bank account linked to ICICI Direct. It did not appear on the portfolio within ICICI Direct. There is a delay of more than a month from the date of allocation to automatically appear in the portfolio. Not sure of why the bonds did not appear within the portfolio I contacted the customer care, I was asked to manually add the bonds in my portfolio, which I did, but after a month from the date of allocation, I had twice the number of bonds allocated in my portfolio and I had to delete the entry I made manually.

Answer to your second question

I haven’t been charged for cash purchases in primary market for TF bonds, equity (IPO/FPO) . Mutual funds I am not sure of, I guess there isn’t any charges for NFO, but anything other than NFO for instance SIP it is rs 33 and one time purchase it is rs 112

Hi Prash,

I endorse all of what Shri. Nagendra says. Regarding your last question, be warned that ICICIDIRECT charges stiff brokerages for secondary market tax free bond purchases, of the order of 1.37%. In comparison, for share transactions, the brokerage is less than half of this. Do note that high transaction costs can eat into your yields when you buy TFB’s in the secondary market. For example, using very approximate calculations, a 9% tax free bond is equivalent to a 8.88% bond purely due to the brokerage charged by ICICIDIRECT even when the bond has been bought at par value (i.e., no premium).

For buying on selling in secondary market ICICI Direct charges 1% brokerage. SBI Cap charges only 0.5%.

I think even 0.5% is too high. It should not be more than 0.25%.

Unfortunately ICICI Direct is very expensive and no choice for those who have Demat account with them

But then investors can always change their broker(s) or get one more demat-trading account opened and opt for a low cost option.

Hi Shiv and others,

Thanks for providing inputs on this issue.

So a followup question, can someone legally have more than one demat accounts . For e.g one with ICICIdirect, one with SBI etc.

This provides us the flexibility to switch broker based on the current transaction fee structure they provide, and also avoids any monoply to stick with just one ( for e.g icicidirect in my case)

Ofcourse, I would need to explore other online brokers for above exercise, but checking if we can open multiple demat accounts at first place.

Thanks,

Prash

Yes, you can have multiple demat account.

Just like saving bank account there are no restrictions of the number of Demat Accounts a person can have (even with same Depository). But banks can limit number of accounts. For example ICICIDirect allows 5 demat accounts; but the first name in all accounts should be EXACTLY the same. The names of joint holders may vary

More details on What is Demat Account : Brokerage,Charges,Comparison

Please let me know of few brokers offering lower brokerage (including AMF)and a good service.

Thanks

That is one thing I won’t be able to do. Everybody has his/her own experiences with the brokers.

The brokerage also depends on the service. ICICI Direct is having online trading which is a proven site. There may be service providers providing lower brokerage but service may not be all that great (Avalailability & speed of application etc. ). One is only looking for TAX free bonds trade, then it may be a good idea to have lower brokerage Demat provided high value holding and transactions.

Sorry, a typo: ICICIDIRECT’s brokerage is around 1.13% not 1.37% as shown above. Interestingly, the increased brokerage is a gift it has given to investors in 2013; my purchases in 2012 March indicate a saner brokerage of 0.55 or 0.6 percent.

A little off-topic but since I see lot of mention of G-Sec. How do you invest in G-Secs directly? Does icicidirect allow it? Also how do you know the rates for these(couldnt understand NSE listing except coupon rate)?

Most of the people take benefit of GSec through buying Debt funds. But RBI is encouraging the retail customers and you can buy them through IDBI. They are the only one facilitating GSec bonds buying and selling. You can view the GSec bond rates in https://www.ccilindia.com/OMMWCG.aspx

Thanks George for your inputs!

Hi Harinee,

Here you’ve the link to check the Business Line’s article “How to invest in G-Secs”, I hope it helps.

http://www.thehindubusinessline.com/money-wise/how-to-invest-in-gsecs/article4813998.ece

Thanks Shiv and George for the reply. Will look it up

You are welcome.

What are the possibilities of listing gains if one invests in IRFC, considering the current interest trends, forthcoming issues before 31st March and other factors ?

IRFC issue size is larger than NHAI and the extension of closing date to 7th Feb indicates a very low possibility of IRFC coming out with another issue before 31st March.

For NHAI of course the higher public response indicates a good chance of listing gains.

Listing gains depend on the interest rates in the market and the coupon rates these bonds are offering. NHB and HUDCO both have given equal listing gains despite huge investor interest for the NHB bonds.

Hi Shiv!

Can you explain how to invest in these, minimum investment required and lock in?

http://www.business-standard.com/article/companies/despite-slowdown-investors-pump-money-into-realty-funds-114011500692_1.html

Hi Simple,

I’ll try to cover it in the first week of February.

Good comparison Shiv, shows how many parameters are there. Impressed by the research on IRFC.

Thanks Kirti for your encouraging words!

Hello Shiv,

I’m new to this type of investment. My question is that the tax free bond gives the mentioned return for e.g. 8.75% for 15yrs back after the maturity? or they give less rate of interest?

My concern is if tax free bond providers are giving the fixed amount at the time of maturity then why to compare 2 different providers? Whichever is giving higher rate of interest select that one.

Hi Chintan,

NHAI will pay 8.75% tax-free interest every year on a fixed date throughout this period of 15 years. This rate of interest is fixed and is not going to change at any point of time. On maturity it will pay back your investment amount.

Comparison between two issuers is necessary because the business fundamentals, credit quality and promoter support of two companies might vary to a great extent. It is not the government itself, it is the government owned companies which are issuing these bonds.

Hi Shiv,

Can u pls help selecting between REC Taxfree bonds ( Closing on 14-03-2014 )& HUDCO ( Closing on 19-03-2014 ) ?

since I have invested in both co. last year equally now where shd i invest before 11-03 -2014 as i have some spare liquidity on this date ?

Awaiting your prompt & RELIABLE Reply…

Thanks a lot for valuable guidance…

Hi Aryan,

I think both these issues are equally good. Personally, I would go for the REC issue as it carries a better credit rating and I expect better liquidity when these bonds get listed on the exchange.

thanks for useful guidance as usual. Pls tell me is it worth buying 1 or 2 year old tax free bonds like IIFCL { 20 yrs Rs. 890/bond} available much below par ( discounted due to poor interest in comparison with current range of 8.62 to 9 % ) or it doesn’t give any cost v/s benefit advantage ?

{ also PFC at Rs. 915/Bond 20 yrs ..}

I think if u factorise its the same rate of int. but still i want confirmation & advise from an expert like you…

Thanks for your conceptually clear guidance always,

Aryan.

Thanks Aryan for your kind words !!

The investor needs to go for those bonds which give the highest yield to maturity (YTM). Whichever listed bonds I have seen, all are giving lower YTM. So, I think it is better to go for these bonds from the primary market. But, you can be opportunistic also. If possible for you to track these bonds closely, look out for some sudden & deep discounts in the secondary markets.

thanks. can you pls explain how to check YTM for theses bonds from time to time ?

Hi Aryan,

Please check this NSE link – http://www.nseindia.com/live_market/dynaContent/live_watch/equities_stock_watch.htm?cat=SEC

It has the “YTM at LTP” column which you can check for many of these listed TFBs.

Hello Shiv,

Can u plz help me? I have some IRFC & IIFCL tax free bonds in demat form. How can I sell those bonds in open market? If I close my demat account, whats happens to my Bonds?

Please reply..

Hi Tushar,

You can sell your IRFC/IIFCL bonds as you sell your shares in the secondary market. Contact your broker if you need any assistance in selling them. Also, you cannot close your demat account if there is even a single security in the account.

Shiv,

My Broker is not available right now. My demat a/c is in ‘edelweiss capital’. How can I identify my bonds for selling? I heard, I can Sell those in BSE, how?

Call Edelweiss customer care on 1800 102 3335 and ask them to help you sell your bonds on the BSE/NSE. Without broker, it is not possible to sell any of your dematerialised securities. If you have your online login id, password, you can sell these bonds yourself.

Thanks..

You are welcome !!