This post is written by Shiv Kukreja, who is a Certified Financial Planner and runs a financial planning firm, Ojas Capital in Delhi/NCR. He can be reached at skukreja@investitude.co.in

India Infrastructure Finance Company Limited, commonly known as IIFCL, has launched the third tranche of its tax-free bonds from Monday i.e. February 17. I know I am late in covering this issue, but I was undergoing some rigorous travelling over the weekend and also, my train back to Delhi got approximately 16 hours late. It was supposed to reach New Delhi Railway Station (NDLS) early morning on Monday at 07:20 but it actually reached the destination at 23:00 hours.

Getting over with the painful experience I had, I am back with this review. So, this is the third and most likely the last public issue of tax-free bonds by IIFCL for the current financial year. The company has already raised Rs. 7,176.21 crore through private placements and tranche I and tranche II of its earlier public issues. So, whatever is left over from its authorised limit of Rs. 10,000 crore, IIFCL has set that figure as its target to be raised in this public issue i.e. Rs. 2,823.79 crore.

The issue will remain open for subscription for almost a month to close on March 14. Here are the issue details which might interest you as an investor:

Rating of the Issue – Four rating agencies, ICRA, Brickwork Rating, CARE and India Rating, have rated this issue and as with its previous issues, this issue is also ‘AAA’ rated.

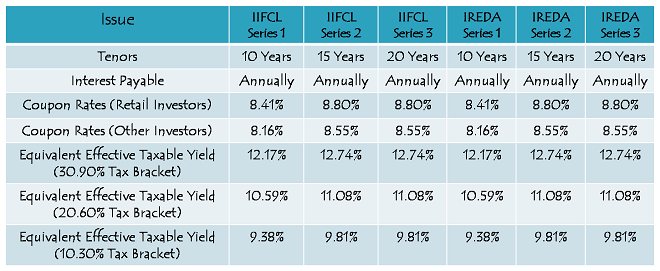

Coupon Rates on Offer – Interest rates, which this issue of IIFCL carries, are absolutely same as the rates which IREDA is offering i.e. 8.80% per annum for the 15 and 20 year options and 8.41% per annum for the 10 year option. As both these issues are ‘AAA’ rated, their interest rates are 20 basis points (or 0.20%) lower than the ‘AA’ rated rated Ennore Port issue.

NRI/QFI Investment – Non-Resident Indians (NRIs) as well as Qualified Foreign Investors (QFIs) are not eligible to invest in this issue.

Investor Categories & Allocation Ratio – The investors have been classified in the following four categories and as always each category will have certain percentage of the issue reserved during the allocation process:

Category I – Qualified Institutional Bidders (QIBs) – 15% of the issue i.e. Rs. 423.57 crore is reserved

Category II – Non-Institutional Investors (NIIs) – 20% of the issue i.e. Rs. 564.76 crore is reserved

Category III – High Net Worth Individuals including HUFs – 25% of the issue i.e. Rs. 705.95 crore is reserved

Category IV – Resident Indian Individuals including HUFs – 40% of the issue i.e. Rs. 1,129.52 crore is reserved

Allotment on First Come First Served Basis – Subject to the allocation ratio mentioned above, allotment will be made on a first come first serve (FCFS) basis in each of the investor categories, based on the date of upload of each application into the electronic system of the stock exchange.

Listing – These bonds from IIFCL will get listed only on the Bombay Stock Exchange (BSE) and that too within 12 working days from the closing date of the issue.

Interest on Application Money & Refund – As with most of these issues, IIFCL will also pay interest to the successful allottees on their application money at the applicable coupon rates, from the date of realization of application money up to one day prior to the deemed date of allotment. Unsuccessful allottees will get interest @ 5% per annum on their refund money.

Interest Payment Date – Interest payment date in this case is linked to the deemed date of allotment and that is why it is yet to get declared. Once the allotment gets done, I’ll update it here on this post itself and also the one which carries the interest payment dates of all the bonds which have got issued during the current financial year.

Demat not Mandatory – As most of the investors are aware, investment in these tax-free bonds don’t require you to mandatorily have a demat account to apply for these bonds. You may subscribe to them in certificate form as well like a fixed deposit. and can get them converted to demat form whenever you want.

Lock-in Period, Premature Redemption – As these are not any tax saving bonds, there is no lock-in period with these bonds and if you take these bonds in your demat account, you can sell them whenever you want on the BSE once they get listed for trading. But, if you take these bonds in physical/certificate form, you cannot redeem these bonds back to the company before their maturity period gets over.

Among the three issues which are currently open for subscription, I would personally prefer the IIFCL issue the most, the IREDA offer as my second option and the Ennore Port issue I would give it the third rank. But, in order to diversify their tax free bonds portfolio, I think the investors would like to give this issue a miss as they might have already applied for the IIFCL bonds in its previous offerings.

Application Form of IIFCL Tax Free Bonds

Note: As per SEBI guidelines, ‘Bidding’ is mandatory before banking the application form, else the application is liable to get rejected. For bidding of your application, any further info or to invest in IIFCL tax-free bonds, you can contact me at +919811797407

Day 14 (March 7) subscription figures:

Category I – Rs. 36 crore as against Rs. 423.57 crore reserved

Category II – Rs. 160.54 crore as against Rs. 564.76 crore reserved

Category III – Rs. 264.02 crore as against Rs. 705.95 crore reserved

Category IV – Rs. 437.35 crore as against Rs. 1,129.52 crore reserved

Total Subscription – Rs. 897.91 crore as against total issue size of Rs. 2,823.80 crore

Day 13 (March 6) subscription figures:

Category I – Rs. 36 crore as against Rs. 423.57 crore reserved

Category II – Rs. 156.54 crore as against Rs. 564.76 crore reserved

Category III – Rs. 263.32 crore as against Rs. 705.95 crore reserved

Category IV – Rs. 428.90 crore as against Rs. 1,129.52 crore reserved

Total Subscription – Rs. 884.76 crore as against total issue size of Rs. 2,823.80 crore

Day 12 (March 5) subscription figures:

Category I – Rs. 36 crore as against Rs. 423.57 crore reserved

Category II – Rs. 156.39 crore as against Rs. 564.76 crore reserved

Category III – Rs. 262.32 crore as against Rs. 705.95 crore reserved

Category IV – Rs. 418.53 crore as against Rs. 1,129.52 crore reserved

Total Subscription – Rs. 873.24 crore as against total issue size of Rs. 2,823.80 crore

‘AAA’ rated NHB tax free bonds issue is getting opened on March 7th with the following coupon rates – 8.50% p.a. for 10 years, 8.93% p.a. for 15 years and 8.90% p.a. for 20 years. Issue size is Rs. 1,000 crore and will get closed on March 18th. NRIs cannot apply in this issue.

Day 11 (March 4) subscription figures:

Category I – Rs. 36 crore as against Rs. 423.57 crore reserved

Category II – Rs. 152.04 crore as against Rs. 564.76 crore reserved

Category III – Rs. 257.83 crore as against Rs. 705.95 crore reserved

Category IV – Rs. 410.39 crore as against Rs. 1,129.52 crore reserved

Total Subscription – Rs. 856.27 crore as against total issue size of Rs. 2,823.80 crore

Day 10 (March 3) subscription figures:

Category I – Rs. 36 crore as against Rs. 423.57 crore reserved

Category II – Rs. 151.64 crore as against Rs. 564.76 crore reserved

Category III – Rs. 257.68 crore as against Rs. 705.95 crore reserved

Category IV – Rs. 401.55 crore as against Rs. 1,129.52 crore reserved

Total Subscription – Rs. 846.88 crore as against total issue size of Rs. 2,823.80 crore

Day 9 (February 28) subscription figures:

Category I – Rs. 36 crore as against Rs. 423.57 crore reserved

Category II – Rs. 150.80 crore as against Rs. 564.76 crore reserved

Category III – Rs. 255.33 crore as against Rs. 705.95 crore reserved

Category IV – Rs. 386.63 crore as against Rs. 1,129.52 crore reserved

Total Subscription – Rs. 828.76 crore as against total issue size of Rs. 2,823.80 crore

Day 7 (February 25) subscription figures:

Category I – Rs. 36 crore as against Rs. 423.57 crore reserved

Category II – Rs. 140.03 crore as against Rs. 564.76 crore reserved

Category III – Rs. 247.23 crore as against Rs. 705.95 crore reserved

Category IV – Rs. 345.06 crore as against Rs. 1,129.52 crore reserved

Total Subscription – Rs. 768.33 crore as against total issue size of Rs. 2,823.80 crore

Day 6 (February 24) subscription figures:

Category I – Rs. 36 crore as against Rs. 423.57 crore reserved

Category II – Rs. 135.53 crore as against Rs. 564.76 crore reserved

Category III – Rs. 236.83 crore as against Rs. 705.95 crore reserved

Category IV – Rs. 318.10 crore as against Rs. 1,129.52 crore reserved

Total Subscription – Rs. 726.47 crore as against total issue size of Rs. 2,823.80 crore

http://www.indiainfoline.com/Markets/News/bonds/5873400379

Upcoming Issue!

Thanks Jitendra!

Day 5 (February 21) subscription figures:

Category I – Rs. 35 crore as against Rs. 423.57 crore reserved

Category II – Rs. 133.24 crore as against Rs. 564.76 crore reserved

Category III – Rs. 214.91 crore as against Rs. 705.95 crore reserved

Category IV – Rs. 271.02 crore as against Rs. 1,129.52 crore reserved

Total Subscription – Rs. 654.18 crore as against total issue size of Rs. 2,823.80 crore

Day 4 (February 20) subscription figures:

Category I – Rs. 35 crore as against Rs. 423.57 crore reserved

Category II – Rs. 125.04 crore as against Rs. 564.76 crore reserved

Category III – Rs. 202.45 crore as against Rs. 705.95 crore reserved

Category IV – Rs. 231.46 crore as against Rs. 1,129.52 crore reserved

Total Subscription – Rs. 593.95 crore as against total issue size of Rs. 2,823.80 crore

Irrespective of the amount invested, interest earned on these bonds,

are they completely tax free on the hands of the investor. I have

recently dis invested from my equity portfolio. Can I invest the

amount on these bonds, without any tax implications. I have only

booked loss in capital market.

Yes, the interest is completely tax-free, irrespective of the amount invested.

I have invested Rs 800000 in IIFCL tranche II which came in december 2013. now I want to invest another Rs 7 Lac in this series . So does that meke me HNI or I will be treated as retail investor

Yes Amol, that will make you an HNI. You should invest in Tranche III to remain a retail investor.

Not sure about your reply. If he invested 8 L in last issue, he can invest another 7 lakhs in current issue and continue as retail investor.

Hi George,

While replying to this query, I was not sure what Amol meant with “this series”. I thought he wanted to invest more in Tranche II. Please check the second part of my reply. I made it clear that to remain a retail investor and earn higher interest, he should invest in Tranche III only.

Fine Shiv. I was also making sure considering the ambiguity in the first part of the answer.

Yes, you are right, my reply seems ambiguous in the first observation.

Day 3 (February 19) subscription figures:

Category I – Rs. 35 crore as against Rs. 423.57 crore reserved

Category II – Rs. 73.08 crore as against Rs. 564.76 crore reserved

Category III – Rs. 184.91 crore as against Rs. 705.95 crore reserved

Category IV – Rs. 185.25 crore as against Rs. 1,129.52 crore reserved

Total Subscription – Rs. 478.24 crore as against total issue size of Rs. 2,823.80 crore

please send e if any news in this bond

Day 2 (February 18) subscription figures:

Category I – Rs. 35 crore as against Rs. 423.57 crore reserved

Category II – Rs. 72.06 crore as against Rs. 564.76 crore reserved

Category III – Rs. 166.96 crore as against Rs. 705.95 crore reserved

Category IV – Rs. 139.52 crore as against Rs. 1,129.52 crore reserved

Total Subscription – Rs. 413.53 crore as against total issue size of Rs. 2,823.80 crore

Day 1 (February 17) subscription figures:

Category I – Rs. 35 crore as against Rs. 423.57 crore reserved

Category II – Rs. 60.44 crore as against Rs. 564.76 crore reserved

Category III – Rs. 119.81 crore as against Rs. 705.95 crore reserved

Category IV – Rs. 72.06 crore as against Rs. 1,129.52 crore reserved

Total Subscription – Rs. 287.31 crore as against total issue size of Rs. 2,823.80 crore

Shiv, thanks!

For me your last para of the post is most useful … where your views on ‘relative priorities’ between these 3 open issues is given. Appreciate that.

Thanks KS for that and I am glad that some of the times my opinions help OneMint readers in taking their investments decisions.

Thanks for the effort, we appreciate it:)

Thanks for your kind words !! 🙂